|

市场调查报告书

商品编码

1406130

货柜装卸设备-市场占有率分析、产业趋势与统计、2024年至2029年成长预测Container Handling Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

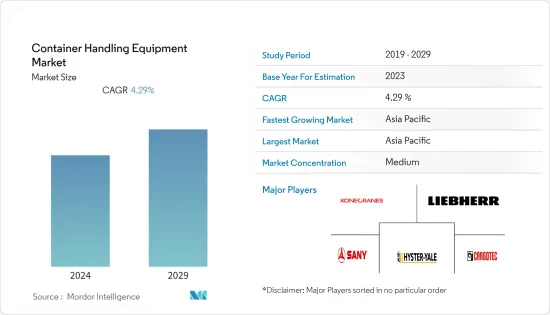

货柜装卸设备市场目前价值 73.4 亿美元,预计未来五年将成长至 94.3 亿美元,预测期内收益复合年增长率为 4.29%。

从中期来看,国际商业的扩张和货运需求的成长决定了近几十年来全球经济的发展。由于全球化和工业化,中国和印度等亚太国家预计将保持最高的成长率,因为它们拥有涉及大规模进出口的大型製造设施。

港口码头自动化趋势的变化、电子商务产业的兴起,以及对电气和混合设备的需求不断增长,重点是生产现场的劳动力预防措施和严格的排放法规,正在推动货柜装卸设备市场的发展。创新的商业机会。

港口码头自动化趋势的变化、电子商务行业的成长以及对电动和混合设备的需求不断增加,重点关注工人安全和生产现场严格的排放标准,推动了货柜装卸设备市场的发展。和创新的商业机会。

货柜货物装卸设备市场趋势

越来越重视货柜装卸设备的电动

全球经济成长和工业化程度不断提高正在推动各行业对货柜装卸设备的需求。销售成长的原因是其应用范围广泛,包括建设业、製造业、港口货物装卸业等。

推动搬运设备销售的另一个因素是电子商务、零售和物流行业的快速扩张,特别是在印度、巴西、新加坡和墨西哥等新兴经济体。

生态效率对于货物和材料处理变得极为重要。随着世界各地的港口和码头不断提高能源效率和减少排放,电动是席捲整个产业的最新趋势。事实证明,港口设施电气化可以显着减少排放气体。随着各国注重减少排放,预计未来几年电动和混合电动货柜的采用将会增加。

此外,一些电子商务公司正在部署新策略来缩短交货时间,例如大力投资自动堆高机和电动堆高机,以加快装载和提货的过程。随着世界各地对柴油车实施更严格的排放法规以控制二氧化碳排放,製造商现在正在提供更环保的堆高机型号。此外,政府在这方面的倡议将在预测期内提振市场需求。

更严格的排放法规可能会要求货柜装卸设备製造商在不牺牲其电力能力的情况下提高其产品的能源效率。根据美国环保署(EPA)新的越野车辆/设备(包括建筑、农业采矿和物料搬运设备)排放标准,所有新购买的堆场卡车和带入港口或联运铁路堆场的非堆场卡车设备必须配备Tier 4 Final 越野引擎或车型年份(MY) 2010 或更高版本的公路式引擎。因此,製造商逐渐在新型货柜装卸机械中采用 Tier 4 引擎技术。

堆高机技术的进步使仓库环境对每个人来说都更加安全。例如,可以透过使其更容易快速转向来降低堆高机事故的可能性。工人不会因受伤而失去工作,生产力也保持不变。此外,较低的事故率意味着更少的堆高机维修。

由于上述全球发展,预计在预测期内对货柜装卸设备的需求将会成长。

亚太地区仍维持市场领先地位

亚太地区由中国、印度等全球主要新兴经济体组成,对原料及最终产品的需求量较大,货柜进出口量较大。

中国是亚太地区主要国家之一,拥有经济成长支撑的最活跃的工业活动。中国有34个货柜港口和2000个小港口。上海是世界上最大的港口,运输能力达4,330万个标准箱。

该国的成长率很高,但逐渐放缓(随着人口老化和经济从投资转向消费、从製造业转向服务业、从外需转向内需的再平衡)。然而,由于中国人事费用和材料成本较低,许多企业在中国生产产品,然后出口到所需目的地。结果,中国已成为世界主要出口国之一。

近年来,中国港口建设取得长足发展,全球货运量和货柜吞吐量前10名的港口中有7个位于中国。作为上海港的主港,洋山深水港规模庞大,货柜吞吐量至少占总货柜吞吐量的40%。随着四期工程的启用,上海港年货柜吞吐量将超过4000万标准箱,总合美国所有港口年货柜吞吐量的总和。

印度是亚太地区主要国家之一,其进出口活动受到其经济成长的支持。孟买港是全国最大、最繁忙的港口。

据港口、航运和水道部称,印度最繁忙的国营货柜门户贾瓦哈拉尔·尼赫鲁港务局 (JNPA) 处理了 4,177,000 标准箱,高于去年同期的 3,222,000 标准箱。

日本有许多主要的货物装卸设备製造商,当地企业垄断了港口货物装卸设备的设计和製造。他们还有自己的设计、製造和品质标准。因此,其他国家的产品要进入日本市场需要付出很大的努力。

日本正面临人口老化和人口减少的挑战,这就是为什么公司正在投资开发码头和货柜装卸自动化等先进技术,以提高生产力和安全性。此外,为了降低货柜装卸设备的营运成本,人们已经开始采用最新技术对旧设备进行改造。通力起重机和卡尔玛是为旧设备提供改造服务的众多公司中的两家。这包括旧设备的自动化。

随着上述开拓在全部区域的发生,市场可能会在预测期内显着成长。

货柜装卸设备产业概况

几家主要企业主导着货柜装卸设备市场,包括卡哥特科公司、利勃海尔集团、三一集团、海斯特-耶鲁物料搬运公司和科尼集团。本公司大力投资于新的和先进的产品创新的研发。全球製造设施的扩张预计将在未来几年提振市场。例如

- 2023年9月,环球港口在东方港装卸公司(VSC)的远东码头安装了设备。本公司与上海振华重工(ZPMC)签署采购港口货柜装卸设备的谅解备忘录。

- 2022年10月,丰田物料搬运在北美推出更新版丰田三轮电动堆高机。这款新型电动堆高机为其细分市场中最畅销的堆高机带来了新功能和技术。

- 2022 年 1 月,卡哥特科旗下卡尔玛与 Westport AS 签署协议,在挪威提供世界上第一台配备组合充电系统的电动正面堆垛机。该订单还包括一份为期五年的卡尔玛全面保养服务合同,该合约将累计入卡哥特科的 2022 年第一季订单,併计划于 2022 年第四季度初交货。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场驱动因素

- 越来越重视货柜装卸设备的电动

- 市场抑制因素

- 货柜装卸设备的资金成本高且复杂

- 波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔(市场规模)

- 依设备类型

- 堆高机

- 堆迭起重机

- 移动式港口起重机

- 胶轮高架起重机

- 依推进类型

- 柴油引擎

- 电动式

- 混合

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 欧洲其他地区

- 亚太地区

- 印度

- 中国

- 日本

- 韩国

- 其他亚太地区

- 世界其他地区

- 南美洲

- 中东/非洲

- 北美洲

第六章 竞争形势

- 供应商市场占有率

- 公司简介

- Cargotec Corp.

- Liebherr Group

- SANY Group

- Shanghai Zhenhua Heavy Industries Co. Ltd(ZPMC)

- Hyster-Yale Materials Handling Inc.

- Anhui HELI Forklifts Group Co. Ltd

- Hoist Material Handling Inc.

- CVS Ferrari SpA

- Lonking Holdings Limited

- Konecranes

第七章 市场机会及未来趋势

The Container Handling Equipment Market is valued at USD 7.34 billion in the current year and is expected to grow to USD 9.43 billion by the next five years, registering a CAGR of 4.29% in terms of revenue during the forecast period.

Over the medium term, the expansion of international commerce and the rising need for cargo transportation defined global economic development in recent decades. Due to large-scale manufacturing facilities involved in large-scale imports and exports, Asia-Pacific nations such as China and India are predicted to include the highest growth rates as a result of globalization and industrialization.

The shifting trends toward automation of port terminals, the rising e-commerce industry, and growing requirements for electric and hybrid equipment, with emphasis on precaution for labor on the production floor and stringent emission norms, provide innovative business opportunities in the container handling equipment market.

The container handling equipment market may see innovative new opportunities as a result of shifting trends toward port terminal automation, the growing e-commerce industry, and growing demands for electric and hybrid equipment, with an emphasis on worker safety on the production floor and stringent emission standards.

Container Handling Equipment Market Trends

Growing Emphasis on the Electrification of Container Handling Equipment

The growing world economy and rising industrialization are driving the demand for container-handling equipment across different fields. Their use in industries like construction, manufacturing, and port handling, owing to the wide range of applications, are the reasons for their increased sales.

Another factor boosting the handling equipment sales is the rapid expansion of the e-commerce, retail, and logistics industries, especially in developing economies such as India, Brazil, Singapore, and Mexico.

Eco-efficiency became extremely important for cargo and material handling. As ports and terminals around the world move toward improved energy efficiency and reduced emissions, electrification is the latest trend sweeping across the industry. Electrification of port equipment proved to reduce emissions hugely. With countries focusing on reducing their emissions, the adoption of electric and hybrid-electric containers is expected to increase in the years to come.

In addition, some e-commerce companies are developing new strategies, including investing heavily in autonomous and electric forklifts to speed up the loading and picking up processes of products as they reduce the delivery time. Stringent emission norms for diesel vehicles across the globe to regulate CO2 emissions led the manufacturers to offer more environment-friendly forklift truck models. Furthermore, government initiatives in this regard boost demand in the market over the forecast period.

More stringent emission regulations may require manufacturers of container handling equipment to improve the energy efficiency of their products without sacrificing their power capabilities. According to the new emission standards for off-road vehicles/equipment (including construction, agricultural mining, and material handling equipment) by the Environmental Protection Agency (EPA), all newly purchased yard truck and non-yard truck equipment brought onto a port or intermodal rail yard must include either a Tier 4 final off-road engine or a model year (MY) 2010 or newer on-road engine. Thus, Tier 4 engine technology is gradually adopted by manufacturers in their new container handling equipment.

Forklift technology advancements make warehouse environments safer for everyone. For instance, reducing the likelihood of forklift accidents can be achieved by making it simpler to make a fast turn. Workers won't get hurt and lose their jobs, and productivity rates can stay the same. Additionally, fewer forklift repairs are required when accident rates drop.

With the development mentioned above across the globe, the demand for container handling equipment is likely to grow during the forecast period.

Asia-Pacific Remains the Market Leader

The Asia-Pacific region consists of major developing economies of the world, such as China and India, where a large volume of containers is exported and imported due to the high requirement for raw materials and final products.

China is one of the major countries in the Asia-Pacific region, with the highest industrial activities being supported by its growing economy. China includes 34 container ports and 2,000 minor ports. Shanghai is the world's largest port, with a capacity of 43.3 million TEU.

The country's growth rate is high but is gradually moving toward moderate (as the population ages and the economy rebalances from investment to consumption, manufacturing to services, and external to internal demand). However, due to low labor and material costs in China, many companies manufacture their products in China and later export them to required destinations. It helped China position itself as the world's leading exporter.

China's port construction developed so greatly in recent years that seven of the world's top 10 ports, in terms of both cargo and container throughput, are in China. As a major part of Shanghai Port, Yangshan Port boasts of a big container throughput, which accounts for at least 40% of the total. The opening of the fourth phase will help the annual container throughput in Shanghai Port surpass 40 million TEUs, which is equivalent to the sum of all US ports' annual container throughput.

India is one of the major countries in the Asia-Pacific region, with import and export activities being supported by its growing economy. Mumbai Port is the country's largest and busiest port.

According to the Ministry of Ports, Shipping and Waterways, India's busiest state-run container gateway, Jawaharlal Nehru Port Authority (JNPA), handled 4.177 million TEUs, up from 3.222 million TEUs during the same time previous year.

Japan contains many of the leading cargo-handling machinery manufacturers, and the local companies made the monopoly on designing and manufacturing the cargo handling equipment for ports in Japan. They had unique standards for design, manufacturing, and quality. Thus, it took a lot of work for the products of other countries to enter the market of Japan.

Japan is facing the problem of aging and decreasing population, which is the reason why companies are investing in the development of advanced technologies such as terminal container handling automation to improve productivity and safety. They also started to retrofit old equipment with the latest technology to reduce the operational costs of container handling equipment. Kone Cranes and Kalmar are two of many companies that provide retrofitting services for old equipment. It includes old equipment automation as well.

The development mentioned above across the region is likely to witness major growth for the market during the forecast period.

Container Handling Equipment Industry Overview

Several key players, such as Cargotec Corp, Liebherr Group, SANY Group, Hyster-Yale Materials Handling Inc., Konecranes, and others, dominate the container handling equipment market. Companies are investing heavily in research and development for the innovation of new and advanced products. The expansion of manufacturing facilities across the globe is anticipated to boost the market in the coming years. For instance,

- In September 2023, Global Ports equipped the Far Eastern terminal of Vostochnaya Stevedoring Company (VSC). They signed a memorandum of intent with Shanghai Zhenhua Heavy Industry Company (ZPMC) to buy portside container handling equipment.

- In October 2022, Toyota Material Handling launched an updated version of Toyota's 3-Wheel Electric Forklift in North America. The new updated electric forklift equipped with new features and technology to the top-selling forklift in the segment.

- In January 2022, Kalmar, part of Cargotec, agreed with Westport AS to supply the world's first electric reach stacker with a combined charging system in Norway. The order also includes a five-year Kalmar Complete Care service agreement, which was booked in Cargotec's Q1 2022 order intake, with delivery scheduled for early Q4 of 2022.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Growing Emphasis on The Electrification of Container Handling Equipment

- 4.2 Market Restraints

- 4.2.1 High Capital Cost And Increasing Complexity of Container Handling Equipment

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value (USD))

- 5.1 By Equipment Type

- 5.1.1 Forklift Truck

- 5.1.2 Stacking Crane

- 5.1.3 Mobile Harbor Crane

- 5.1.4 Rubber-tired Gantry Crane

- 5.2 By Propulsion Type

- 5.2.1 Diesel

- 5.2.2 Electric

- 5.2.3 Hybrid

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 south America

- 5.3.4.2 Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Cargotec Corp.

- 6.2.2 Liebherr Group

- 6.2.3 SANY Group

- 6.2.4 Shanghai Zhenhua Heavy Industries Co. Ltd (ZPMC)

- 6.2.5 Hyster-Yale Materials Handling Inc.

- 6.2.6 Anhui HELI Forklifts Group Co. Ltd

- 6.2.7 Hoist Material Handling Inc.

- 6.2.8 CVS Ferrari SpA

- 6.2.9 Lonking Holdings Limited

- 6.2.10 Konecranes

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2030 年货柜装卸设备市场预测:按设备类型、推进类型、起重能力、应用、最终用户和地区进行的全球分析

2030 年货柜装卸设备市场预测:按设备类型、推进类型、起重能力、应用、最终用户和地区进行的全球分析 货柜货物装卸设备市场:按设备类型、按推进类型、按起重能力、按最终用户:2023-2032 年全球机会分析和产业预测

货柜货物装卸设备市场:按设备类型、按推进类型、按起重能力、按最终用户:2023-2032 年全球机会分析和产业预测 货柜装卸设备市场 - 全球市场规模、份额、趋势分析、机会、预测报告(2019-2029)

货柜装卸设备市场 - 全球市场规模、份额、趋势分析、机会、预测报告(2019-2029) 集装箱装卸设备市场:2023-2028 年全球行业趋势、份额、规模、增长、机会和预测

集装箱装卸设备市场:2023-2028 年全球行业趋势、份额、规模、增长、机会和预测 集装箱装卸设备的全球市场

集装箱装卸设备的全球市场 全球集装箱装卸设备市场研究与预测:按设备类型(叉车,堆垛机,移动式港口起重机,轮胎式龙门起重机),推进类型(柴油,电动,混合动力)区域分析2022-2029

全球集装箱装卸设备市场研究与预测:按设备类型(叉车,堆垛机,移动式港口起重机,轮胎式龙门起重机),推进类型(柴油,电动,混合动力)区域分析2022-2029