|

市场调查报告书

商品编码

1406214

网路加密:市场占有率分析、产业趋势/统计、成长预测,2024-2029 年Network Encryption - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

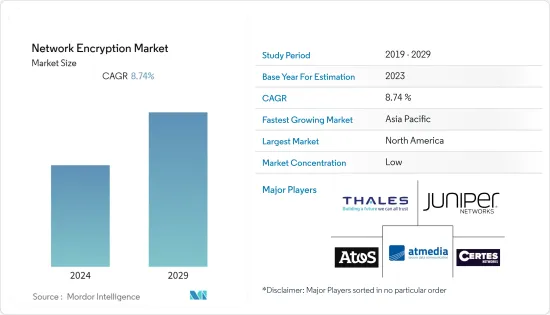

本财年网路加密市场规模预估为41.8亿美元,复合年增长率为8.74%,预计五年内将达到69.4亿美元。

网路加密的成长主要是由于组织对资料安全和隐私的日益关注。

主要亮点

- 互联网、云端运算的发展和网路攻击的增加推动了对更安全的资料通讯和储存的需求。此外,一般资料保护规范 (GDPR) 和支付卡产业资料安全标准 (PCI DSS) 等越来越多的政府法规要求组织实施安全的资料传输方法,进一步推动网路加密的成长。

- 此外,随着各种最终用户行业在业务采用基于物联网 (IoT) 的解决方案,对加密的需求不断增长,以安全地保护透过物联网网路传输的资料,从而支持市场成长。

- 随着新的加密演算法和更好的加密软体的诞生,网路加密产业不断发展。例如,量子电脑破解传统加密方法的潜力使得使用量子电脑无法破解的加密演算法变得非常重要。

- 部署加密解决方案可能既困难又昂贵,尤其是对于 IT 资源有限的企业而言。对于某些组织来说,购买、配置和培训员工使用和维护加密解决方案的成本可能是不使用它的一个原因。此外,某些加密演算法存在技术问题,不适合企业网路。预计这些挑战将在预测期内挑战市场成长。

- 影响市场成长的最重要因素是网路安全漏洞数量的增加、许多组织对云端技术的使用不断增加,以及满足不断变化的监管标准以更好地保护资料的需求不断增加。

- COVID-19 的爆发对网路加密市场产生了重大影响。在家工作的趋势不断增长,增加了对安全远端工作解决方案的需求。随着在家工作的增加,需要安全可靠的虚拟私人网路 (VPN) 和远端桌面解决方案来保护敏感的公司资料。这导致对网路加密产品和服务的需求激增,推动了产业的成长。此外,为了因应与疫情相关的网路攻击和安全漏洞的增加,企业增加了对网路安全的投资。

网路加密市场趋势

通讯和IT领域预计将占据较大市场份额

- 推动全球 IT 和通讯业网路加密的关键因素包括云端使用的增加、光纤通讯投资的增加、网路资料外洩的增加以及严格的政府监管。

- 此外,专用网路的日益普及、网路自动化的趋势以及 5G 网路的推出预计将增加网路流量,并显着需要更复杂的安全措施。网路加密可确保这些网路上敏感资料的安全,并开启新的商机。

- 新兴ICT技术,如智慧工厂、智慧型交通系统、第五代以上行动电话网路、物联网、分散式帐本技术、量子安全通讯等,需要技术和组织措施。

- 5G 技术的引入可能会增加连接到网路的物联网 (IoT) 设备的数量,为骇客进行更广泛、更复杂的攻击提供新的机会。爱立信表示,资料消费量预计将从 2019 年的 35Exabyte增加到今年的 73Exabyte。所有这些因素都在扩大通讯供应商的网路自动化范围,并刺激了对研究市场的需求。

- 此外,全球保全服务的创新扩展启动和采用进一步推动了对网路加密技术的需求。例如,2022 年 10 月,印度政府通讯、电子和资讯科技及铁路部长宣布采用 Infinity Labs Ltd. 开发的专有加密技术 InfiBharat。

- 通讯威胁源自于产业中典型的基于 IP 的威胁与传统技术的组合。随着5G技术的进步,威胁面将会扩大,攻击者将有更多的机会。因此,电信业者网路安全团队正在利用新技术和自动化来简化工作流程,以领先攻击者一步,即使他们面临新的威胁和越来越多的分类警报。我正在寻找一种方法。

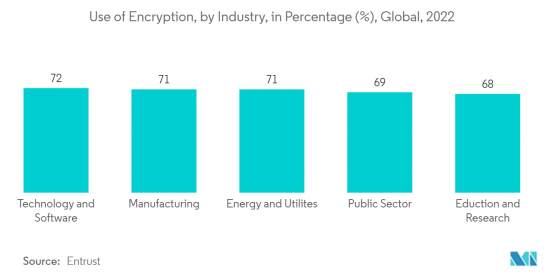

- 根据 Entrust 2022 年全球加密趋势研究,该公司对来自 17 个国家和地区各行业的 6,264 名人士进行了调查。组织依靠公司来保护客户的个人资讯(53% 的受访者)、保护资料免受已识别的威胁(50% 的受访者)以及保护企业智慧财产权(53% 的受访者)(48% )使用加密。 62% 的组织已采用加密策略,这是近 20 年来最快的采用率。

预计北美将占据较大市场占有率

- 北美是一个技术设备精良的地区。美国和加拿大等已开发经济体占据了很大的市场占有率,为各种规模的企业遵守政府规则和法规提供了合适的平台。

- 北美政府制定了法规,要求敏感资料在传输中受到保护。这增加了对满足这些监管要求的网路加密解决方案的需求。 2022 年 7 月,美国国家标准与技术研究院 (NIST) 制定了新的加密标准,旨在抵御量子电脑的攻击。

- 随着该地区高科技产业的不断增长,对网路加密解决方案的需求也不断增长。云端处理普及,企业希望在将敏感资料传送到云端或从云端发送资料保护资料。公司也投入资金进行研发,以开发更先进的网路加密方法。这些投资正在促进该行业的成长。

- 虽然最近修订的 EARN IT 法案将使强加密陷入困境,但合法存取加密资料法案 (LAEDA) 将使数百万人陷入黑暗。它直接攻击我们每天依赖的个人和国家安全工具。

- 此外,随着该地区网路漏洞的增加,对加密的需求也在增加。根据美国政府资料,2022年1月至5月的医疗保健违规数量与去年相比几乎翻了一番。例如,根据新闻报道,2022 年 8 月,印第安纳州的健康资料外洩事件领先全国,超过8,000 万笔记录受到影响,在截至2022 年6 月的13 年期间,所有记录中有25 笔洩露,占近 % 。

网路加密产业概况

网路加密市场碎片化,多个参与者活跃。拥有重要市场份额的领先公司正在利用策略合作计划,并专注于扩大海外基本客群,以提高市场占有率和盈利。 Thales Trusted Cyber Technologies、Atos SE、Juniper Networks, Inc.、Certes Networks, Inc.、Senetas Corporation Ltd.、Viasat Inc.、Raytheon Technologies Corporation、Securosys SA.、Packetlight Networks 均出现在当前市场中,合併后,这些是一些采取收购、合作和产品创新等策略倡议的主要企业。

2023 年 2 月,Atos 宣布推出新的 5Guard 安全性,适用于希望部署专用 5G 网路的组织和希望实现整合自动化的通讯业者。这些公司编配安全措施来保护和捍卫其资产和客户。 Atos 的产品系列包括 Atos 加密解决方案 (Trustway)、识别及存取管理软体、公共关键基础设施解决方案 (IDnomic) 以及 Atos 託管侦测和回应 (MDR) 平台,该平台可近乎即时地识别潜在威胁。回应以提高5G 网路元素、应用程式和工作负载的安全性。

2023 年 1 月,数位基础架构製造商 Equinix 与云端服务製造商 Aviatrix 合作,为企业环境提供高效能加密。透过此次合作,Aviatrix Edge 软体将在 Equinix 全球超过 25 个业务交换资料中心提供。这种解决方案组合由 Equinix Network Edge 和 Equinix Fabric 提供支持,提供最快、最安全的云端连接,让您能够查看多个云端中发生的情况。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 网路安全漏洞增加

- 许多组织越来越多地采用云端技术

- 市场挑战

- 实施网路加密解决方案的成本高昂

第六章市场区隔

- 依部署类型

- 云

- 本地

- 按成分

- 硬体

- 解决方案服务

- 按组织规模

- 中小企业

- 大公司

- 按最终用户产业

- 通讯/IT

- BFSI

- 政府机关

- 媒体娱乐

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第七章 竞争形势

- 公司简介

- Thales Trusted Cyber Technologies

- ATMedia Gmbh

- Atos SE

- Juniper Networks Inc.

- Certes Networks Inc.

- Senetas Corporation Ltd.

- Viasat Inc.

- Raytheon Technologies Corporation

- Securosys SA

- Packetlight Networks

- Rohde & Schwarz Cybersecurity GmbH

- Colt Technology Services Group Ltd.

- Ciena Corporation

第八章投资分析

第9章市场的未来

The Network Encryption Market was valued at USD 4.18 billion in the current year and is expected to register a CAGR of 8.74%, reaching USD 6.94 billion in five years. The growth of network encryption is primarily attributed to the increasing concern for data security and privacy in organizations.

Key Highlights

- The growth of the internet, cloud computing, and the increasing number of cyberattacks have led to the need for more secure data communication and storage. Additionally, increasing government regulations, such as the General Data Protection Regulation (GDPR) and the Payment Card Industry Data Security Standard (PCI DSS), require organizations to implement secure data transmission methods, further driving the growth of network encryption.

- Furthermore, the growth in adopting Internet of Things (IoT)-based solutions by the various end-user industries in their operations has increased the need for encryption to secure data transmitted over IoT networks, supporting market growth.

- The network encryption industry has grown because new encryption algorithms and better encryption software have been made. For example, using encryption algorithms that quantum computers can't break is becoming more important because quantum computers could break traditional encryption methods.

- Putting encryption solutions into place can be hard and expensive, especially for businesses with few IT resources. For some organizations, the cost of buying and setting up encryption solutions and training staff to use and maintain them can be a reason not to use them. Also, some encryption algorithms may have technical problems that make them unsuitable for s networks. Such factors are expected to challenge the market's growth during the forecast period.

- The most important factors affecting the market's growth are the growing number of network security breaches, the increasing use of cloud technologies by many organizations, and the growing need to meet ever-changing regulatory standards for better data protection.

- The COVID-19 pandemic significantly affected the network encryption market. As the trend toward working from home grew, there was more demand for secure remote work solutions. With more people working from home, there was a need for secure and reliable virtual private networks (VPNs) and remote desktop solutions to protect sensitive corporate data. This led to a surge in demand for network encryption products and services, boosting growth in the industry. Additionally, businesses increased their investment in cybersecurity to address the rise in cyber-attacks and security breaches related to the pandemic.

Network Encryption Market Trends

Telecom and IT Sector is Expected to Hold a Significant Share of the Market

- Some of the main things pushing the IT and telecom industries worldwide to use network encryption are the growing use of the cloud, increasing investment in optical communication, growing network data breaches, and strict government regulations.

- Furthermore, the growing adoption of a private network, trends in network automation, and the rollout of 5G networks are expected to increase network traffic, requiring more advanced security measures significantly. Network encryption will keep sensitive data safe on these networks, opening up new business opportunities.

- Emerging ICT technologies such as smart factories, intelligent transportation systems, the 5th generation of cellular networks and beyond, the Internet of Things, distributed ledger technologies, and quantum-safe communication need technical and organizational measures to address various threats and risks.

- The deployment of 5G technology will probably lead to increased Internet of Things (IoT) devices connected to networks, opening up new chances for hackers to conduct more extensive and sophisticated assaults. According to Ericsson, data consumption is projected to increase from 35 exabytes in 2019 to 73 exabytes in the current year. All these factors are expanding the scope of network automation among telecom vendors, fueling the demand in the studied market.

- Furthermore, the innovation expansion launch and adoption of security services across the globe have further boosted the demand for network encryption techniques. For example, in October 2022, the Minister for Communications, Electronics & Information Technology and Railways, Government of India, launched InfiBharat, an indigenous encryption technique developed by Infinity Labs Ltd.

- Threats against telecommunications result from a combination of typical IP-based threats in an industry with legacy technology. As 5G technology advances, the threat surface will only expand, giving attackers more opportunities. This leaves cybersecurity teams at telecom companies looking for ways to leverage new technology and automation to streamline workflows to stay ahead of attackers in the face of new threats and an increasing number of alerts to triage.

- According to Entrust 2022 Global Encryption Trends Study, they polled 6,264 people from various industry sectors across 17 nations and regions. Organizations are using encryption to protect customers' personal information (53% of respondents), to protect data against specific, identified threats (50% of respondents), and to protect enterprise intellectual property (48% of respondents). 62% of organizations have an encryption strategy- the sharpest increase in adoption in nearly two decades.

North America is Expected to Hold Significant Market Share

- North America is a well-equipped region in terms of technology. It has a significant market share because of developed economies like the United States and Canada, and it has the right platforms for businesses of all sizes to follow government rules and regulations.

- The government of North America has put in place rules that require sensitive data to be protected while in transit. This has driven the need for network encryption solutions to meet these regulatory requirements. In July 2022, the National Institute of Standards and Technology (NIST) prepared new encryption standards designed to withstand attacks by quantum computers.

- As the tech industry in the region continues to grow, there is more demand for network encryption solutions. This is because cloud computing is becoming more popular, and organizations want to protect sensitive data while it is being sent to and from the cloud. The companies also spend money on research and development to develop more advanced ways to encrypt networks. This investment is contributing to the growth of the industry.

- While the recently amended EARN IT Act would leave strong encryption on unstable ground if passed into law, The Lawful Access to Encrypted Data Act (LAEDA) is a direct assault on the tool millions of people rely on for personal and national security each day.

- Further, with the increase in network breaches in the region, the demand for encryption increased. United States government data shows that the number of healthcare breaches in the first five months of 2022 has nearly doubled from last year. For instance, according to news reports, in August 2022, Indiana led the nation in medical data breaches, with more than 80 million records affected, which accounted for nearly 25% of all breached records during the 13 years until June 2022.

Network Encryption Industry Overview

The network encryption market is fragmented, with several players operating. The major players with a prominent share in the market are focusing on expanding their customer base across foreign countries by leveraging strategic collaborative initiatives to increase their market share and profitability. Thales Trusted Cyber Technologies, Atos SE, Juniper Networks, Inc., Certes Networks, Inc., Senetas Corporation Ltd., Viasat Inc., Raytheon Technologies Corporation, Securosys SA., and Packetlight Networks are some of the major players present in the current market and undergoing strategic initiatives such as mergers, acquisitions, collaboration, product innovation, and others.

In February 2023, Atos announced the launch of its new '5Guard' security offering for organizations looking to deploy private 5G networks and for telecom operators looking to enable integrated, automated. They orchestrated security to protect and defend their assets and customers. Atos'product portfolio is Atos'encryption solutions (Trustway), identity and access management software; public critical infrastructure solutions (IDnomic); and Atos Managed Detection and Response (MDR) platform that elevates the security of 5G network elements, applications, and workloads by detecting and responding to potential threats in near real-time.

In January 2023, Equinix, a company that makes digital infrastructure, worked with Aviatrix, which makes cloud services, to make high-performance encryption for enterprise environments. This partnership will make the Aviatrix Edge software available in over 25 of Equinix's global business exchange data centers. The combined solution, which uses Equinix's Network Edge and Equinix Fabric, gives you the fastest, most secure connection to the cloud to see what's happening in multiple clouds.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Number of Network Security Breaches

- 5.1.2 Increasing Adoption of Cloud Technologies by Numerous Organizations

- 5.2 Market Challenges

- 5.2.1 High Implementation Cost of Network Encryption Solutions

6 MARKET SEGMENTATION

- 6.1 By Deployment Type

- 6.1.1 Cloud

- 6.1.2 On-premise

- 6.2 By Component

- 6.2.1 Hardware

- 6.2.2 Solutions & Services

- 6.3 By Organization Size

- 6.3.1 Small and Medium-sized Enterprises

- 6.3.2 Large-sized Enterprises

- 6.4 By End-user Industry

- 6.4.1 Telecom & IT

- 6.4.2 BFSI

- 6.4.3 Government

- 6.4.4 Media & Entertainment

- 6.4.5 Other End-user Industries

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia Pacific

- 6.5.4 Latin America

- 6.5.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Thales Trusted Cyber Technologies

- 7.1.2 ATMedia Gmbh

- 7.1.3 Atos SE

- 7.1.4 Juniper Networks Inc.

- 7.1.5 Certes Networks Inc.

- 7.1.6 Senetas Corporation Ltd.

- 7.1.7 Viasat Inc.

- 7.1.8 Raytheon Technologies Corporation

- 7.1.9 Securosys SA

- 7.1.10 Packetlight Networks

- 7.1.11 Rohde & Schwarz Cybersecurity GmbH

- 7.1.12 Colt Technology Services Group Ltd.

- 7.1.13 Ciena Corporation