|

市场调查报告书

商品编码

1406245

全球溶剂:市场占有率分析、产业趋势与统计、2024-2029 年成长预测Global Solvents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

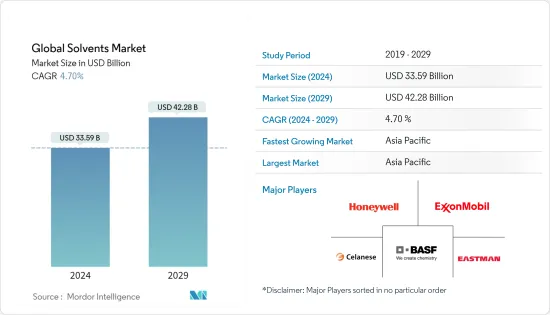

预计2024年全球溶剂市场规模为335.9亿美元,预计2029年将达到422.8亿美元,在市场估算与预测期间(2024-2029年)复合年增长率为4.70%。

溶剂市场受到 COVID-19 大流行的影响,由于遏制措施和经济中断,油漆和涂料以及聚合物和黏剂等行业被迫推迟生产,导致生产和运输放缓。目前市场正从疫情中恢復。预计2022年市场将达到疫情前水准并持续稳定成长。

由于建筑化学品的强劲需求和汽车行业的成长,预计油漆和涂料行业将在此期间在全球溶剂市场的应用领域占据主导份额。

另一方面,化学溶剂会以多种方式对人类健康产生负面影响。它们不仅影响人类健康,而且对环境和动物健康产生严重影响,从而阻碍市场成长。

氧基工业溶剂的开拓预计将为市场成长创造新的机会。

亚太地区是最大的市场,由于中国和印度等国家的消费,预计在预测期内将成为成长最快的市场。

溶剂市场趋势

建筑和汽车行业的巨大需求

- 溶剂用于各种建筑和汽车材料,包括油漆、被覆剂和黏剂。随着对节能建筑和车辆的需求增加,这些产业对溶剂的需求可能会增加。

- 酮由于其低黏度特性和高固态含量而广泛用于油漆和被覆剂。酯类溶剂主要用于油漆作为硬化剂,也用作工业清洗剂。

- 生物基溶剂用于油漆和被覆剂中,以溶解黏合剂和颜色并提供一致性。装饰漆和喷漆中添加乙二醇醚酯等溶剂,以防止它们在空气中干燥。

- 溶剂用于许多建筑产品,例如油漆、稀释剂和黏剂。中国、印度、美国和巴西等国家建设活动的增加预计将推动油漆和涂料应用领域的成长。

- 根据美国总承包商协会的数据,到 2023 年,美国建设产业将蓬勃发展,每年建造的建筑价值估计将达到 2.1 兆美元。

- 印度国家投资促进和便利化管理局的数据显示,印度的建筑业也不断成长,约占该国GDP的9%。不断成长的建筑业正在推动对油漆和涂料的需求,而油漆和涂料是溶剂的重要应用产业。

- 溶剂在汽车工业中也有多种应用。汽油中的添加剂有助于将水从汽油中分离出来。此外,该溶剂有助于燃料更清洁地燃烧,并有助于减少废气排放气体。溶剂可以帮助冰冻门锁除冰、清洗化油器、冷却引擎以及保持内装卫生和地毯卫生。

- 根据国际汽车工业协会(OICA)预测,2022年全球汽车产业较2021年成长6%。全球已开发国家和开发中国家的汽车产量均增加,包括中国、德国、韩国、英国、英国和义大利。 2022年,汽车产量超过8,500万辆。

- 因此,汽车行业的强劲需求为油漆和涂料售后市场的创新创造了有利可图的机会,并迅速增加了溶剂市场的需求。

亚太地区主导市场

- 中国和印度等国家建筑支出的增加以及这些国家工业化的扩张预计将推动该地区溶剂市场的成长。

- 中国、印度、印尼、泰国、越南和韩国等国家拥有蓬勃发展的油漆、被覆剂和黏剂等终端用户产业。预计这些国家将刺激该地区产品的需求。

- 根据中国国家统计局的数据,建筑业产值将从2021年的29.31兆元(4.2兆美元)增加至2022年的31.2兆元(4.5兆美元)。此外,根据住宅及城乡建设部的预测,2025年后中国建筑业预计将维持GDP的6%。

- 在2023-2024年预算中,印度财政部长宣布拨款27亿印度卢比(33.9亿美元)来促进住宅建设。这一分配比前上年度增加了近10%。预计这将为住宅建设提供重要动力。

- 此外,该地区石油探明蕴藏量占全球的3%,天然气探明蕴藏量占全球的10%,其中中国持有全部区域的28%。预计这将促进石化产品的生产,进而促进溶剂市场的成长。

- 此外,建设活动的快速增长以及对汽车的强劲需求预计将增加油漆和涂料应用中对溶剂的需求。此外,该地区的个人护理市场正在蓬勃发展,刺激了溶剂市场的成长。

- 根据OICA统计,亚太地区汽车产量为5,002万辆,比去年的4,677万辆成长7%。

- 由于上述因素,预计该地区对溶剂的需求在预测期内将会增加。

溶剂产业概况

溶剂市场本质上是部分一体化的。主要企业(排名不分先后)包括伊士曼化学公司、BASF公司、埃克森美孚公司、霍尼韦尔国际公司和塞拉尼斯公司。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究成果

- 研究场所

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 油漆涂料领域需求快速成长

- 严格法规以尽量减少挥发性有机化合物的排放

- 其他司机

- 抑制因素

- 高製造成本和溶剂性能问题

- 化学溶剂的有害影响

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(市场规模)

- 来源

- 生物基溶剂

- 石化溶剂

- 类型

- 氧溶剂

- 烃类溶剂

- 卤素溶剂

- 目的

- 黏剂

- 画

- 个人护理

- 药品

- 聚合物製造

- 其他用途(印刷油墨、农药、金属清洗)

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太地区其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 中东和非洲其他地区

- 亚太地区

第六章竞争形势

- 併购、合资、联盟、协议

- 市场占有率(%)/排名分析

- 主要企业策略

- 公司简介

- ADM

- Arkema

- Ashland

- BASF SE

- Bharat Petroleum Corporation Limited

- Celanese Corporation

- Dow

- Eastman Chemical Company

- Exxon Mobil Corporation

- Gandhar Oil Refinery(India)Limited

- GROUPE BERKEM

- Honeywell International Inc

- Huntsman International LLC

- INEOS

- LyondellBasell Industries Holdings BV

- Shell plc

- Sasol Limited

- Solvay

第七章 市场机会及未来趋势

- 氧系工业溶剂的开发

- 对生物基产品的需求不断增加

The Global Solvents Market size is estimated at USD 33.59 billion in 2024, and is expected to reach USD 42.28 billion by 2029, growing at a CAGR of 4.70% during the forecast period (2024-2029).

The solvents market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility wherein industries such as paints and coatings, polymers and adhesives, etc., were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily.

The paints and coatings industry is expected to dominate the application segment of the global solvents market over the period due to significant demand for construction chemicals and the growing automotive industry.

On the flip side, chemical-based solvents can negatively affect human health in different ways. They not only affect human health but also severely affect the environment and the health of animals, and this can hinder the growth of the market.

The development of oxygenated-based industrial solvents is expected to create new opportunities for the market to grow.

Asia-Pacific region represents the largest market and is expected to be the fastest-growing market over the forecast period owing to the consumption from countries such as China and India.

Solvents Market Trends

Significant Demand from Construction and Automotive Industry

- Solvents are used in various construction and automotive materials, such as paints, coatings, and adhesives. As the demand for energy-efficient buildings and vehicles increases, solvents demand is likely to increase from these industries.

- Ketones are widely employed in paints and coatings owing to their ability to acquire low-viscosity properties and high solid content. Ester solvents are primarily used in paints as a hardener and find their usage as an industrial cleaner.

- Bio-based solvents are employed in paints and coatings to dissolve binders and colors and offer consistency. Solvents like glycol ether esters are added to some decorative paints and spray paints to prevent them from drying in mid-air.

- Solvents are used in many construction products, such as paints, thinners, and glues. Increasing construction activities in countries such as China, India, the United States, and Brazil are expected to boost the growth of the paints and coatings application segment.

- In 2023, the United States construction industry is booming, with an estimated USD 2.1 trillion worth of structures built each year, according to the Associated General Contractors of America.

- The construction industry in India is also increasing, accounting for around 9% of the country's GDP, according to the National Investment Promotion & Facilitation Agency. This ever-increasing construction industry is driving demand for paints and coatings, a significant application industry for solvents.

- Solvents find various applications in the automotive industry. Additives in gasoline help keep the water separate from the gasoline. Furthermore, solvents assist the fuel burn cleaner, which can help reduce tailpipe emissions. Solvents aid in de-ice frozen door locks, cleaning carburetors, keeping the engine cool, and hygienic upholstery and carpet.

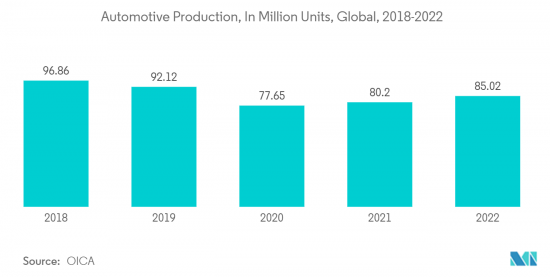

- According to the International Organization of Motor Vehicle Manufacturers (OICA), the global automotive industry grew by 6% in 2022 compared to 2021. Automotive production increased in developed and developing countries worldwide, including China, Germany, South Korea, Canada, the United Kingdom, and Italy. Over 85 million motor vehicles were manufactured in 2022.

- Thus, significant demand in the automotive sector is generating lucrative opportunities for innovation in the paints & coatings aftermarket, surging the need for the solvents market.

Asia-Pacific Region to Dominate the Market

- Increasing construction spending in countries like China and India, along with expanding industrialization in these countries, is anticipated to boost the solvents market growth in the region.

- End-user industries such as paints, coatings, and adhesives flourish in countries such as China, India, Indonesia, Thailand, Vietnam, and South Korea. They are expected to fuel product demand in the region over the period.

- According to the National Bureau of Statistics of China, the value of construction output accounted for CNY 31.2 trillion (USD 4.5 trillion) in 2022, up from CNY 29.31 trillion (USD 4.2 trillion) in 2021. Moreover, as per the forecast given by the Ministry of Housing and Urban-Rural Development, China's construction sector is expected to maintain a 6% share of the country's GDP going into 2025.

- In the budget 2023-2024, the Indian finance minister announced an allocation of INR 2.7 lakh crore (USD 3.39 billion) for boosting housing construction. This allocation increased by nearly 10% as compared to the previous year. This will provide a significant boost to housing construction.

- Additionally, the region accounts for 3% of the world's proven oil reserves and 10% of the world's proven gas reserves, of which China holds 28% of the regional total. This is driving the production of petrochemicals, which, in turn, is expected to fuel the growth of the solvents market.

- Moreover, rapid growth in building & construction activities and strong demand for automobiles are expected to drive the need for solvents in the paints & coatings application. Also, the personal care market is booming in the region and, in turn, fueling the growth of the solvents market.

- According to OICA, the total automotive production in the Asia-Pacific region accounted for 50.02 million units, registering an increase of 7% compared to 46.77 million units produced last year.

- Due to the factors above, the demand for solvents is expected to increase in the region during the forecast period.

Solvents Industry Overview

The solvents market is partially consolidated in nature. The major players (not in any particular order) include Eastman Chemical Company, BASF SE, Exxon Mobil Corporation, Honeywell International Inc., and Celanese Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Surging Demand from the Paints & Coatings Sector

- 4.1.2 Stringent Regulations in Place to Minimize VOC Emissions

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Manufacturing Costs and Performance Issues of Solvents

- 4.2.2 Detrimental Effects of Chemical Solvents

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size In Value)

- 5.1 Source

- 5.1.1 Bio-Based Solvents

- 5.1.2 Petrochemical-based Solvents

- 5.2 Type

- 5.2.1 Oxygenated Solvents

- 5.2.2 Hydrocarbon Solvents

- 5.2.3 Halogenated Solvents

- 5.3 Application

- 5.3.1 Adhesives

- 5.3.2 Paints and Coatings

- 5.3.3 Personal Care

- 5.3.4 Pharmaceuticals

- 5.3.5 Polymer Production

- 5.3.6 Other Applications (Printing Inks, Agricultural Chemicals, Metal Cleaning)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 BASF SE

- 6.4.5 Bharat Petroleum Corporation Limited

- 6.4.6 Celanese Corporation

- 6.4.7 Dow

- 6.4.8 Eastman Chemical Company

- 6.4.9 Exxon Mobil Corporation

- 6.4.10 Gandhar Oil Refinery (India) Limited

- 6.4.11 GROUPE BERKEM

- 6.4.12 Honeywell International Inc

- 6.4.13 Huntsman International LLC

- 6.4.14 INEOS

- 6.4.15 LyondellBasell Industries Holdings B.V.

- 6.4.16 Shell plc

- 6.4.17 Sasol Limited

- 6.4.18 Solvay

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Oxygenated Based Industrial Solvents

- 7.2 Increasing Demand for Bio-Based Products