|

市场调查报告书

商品编码

1644414

嵌入式 SIM(eSIM):市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Embedded SIM (eSIM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

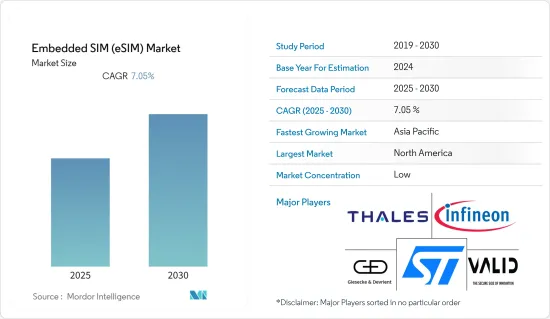

嵌入式 SIM(eSIM)市场预计在预测期内实现 7.05% 的复合年增长率。

eSIM 是一种小型可编程晶片,可直接嵌入智慧型手机、平板电脑、穿戴式装置和其他物联网装置中,无需实体 SIM 卡即可实现远端 SIM 配置。

主要亮点

- 物联网 (IoT) 是 eSIM 采用的主要驱动力之一。 eSIM 为全球部署和管理物联网设备提供了可扩展的解决方案。

- 互联和机器对机器 (M2M) 生态系统的进步是市场成长的主要驱动力。 5G网路的发展也为eSIM的采用创造了新的机会。企业已采用 eSIM 进行 M2M 部署,例如资产追踪、智慧计量、工业监控和供应链管理。

- 对智慧型设备日益增长的需求是推动 eSIM 技术广泛采用的关键驱动因素之一。智慧型设备,包括智慧型手机、平板电脑、联网汽车和各种物联网 (IoT) 设备,在消费和工业应用中变得越来越普遍。

- 安全性和互通性标准化问题正在限制市场的成长。对于传统 SIM 卡,篡改或更换 SIM 卡需要实体访问,这使得恶意行为者更难以破坏连接。然而,由于 eSIM 直接焊接在设备电路上,未授权存取或克隆的可能性会带来重大的安全风险。

嵌入式 SIM (eSIM) 市场趋势

智慧型手机应用领域预计将占据主要市场占有率

- eSIM 消除了对实体 SIM 卡的需求,让使用者更轻鬆地启用和切换行动电话。借助 eSIM,用户可以远端为其设备配置新的运营商配置文件,而无需获取实体 SIM 卡或等待其到达。

- eSIM技术让智慧型手机可以采用双 SIM 卡功能。 eSIM 与实体卡槽结合,可让使用者在同一装置上拥有两个活跃的电话号码,这对于旅客、商务人士和拥有多份行动电话合约的人士尤其有用。

- 对于行动网路营运商来说,eSIM技术在获取新客户方面提供了更大的灵活性。行动网路营运商无需透过零售通路分发实体 SIM 卡,而是可以远端配置 eSIM,从而简化启动流程并降低分发成本。

- eSIM 在实现物联网设备的连接方面发挥关键作用。智慧型手机是各种物联网应用的门户,而eSIM技术提供了一种将物联网设备连接到蜂巢式网路的安全有效的方式。

- 5G 网路的不断发展和物联网设备的广泛应用预计将导致 eSIM 更多地整合到智慧型手机和其他连接设备中。爱立信预计,2022年全球重要物联网和蜂巢式物蜂巢式物联网宽频连线数将达到约15亿。预计五年内此类蜂巢式物联网连接数量将达到 33 亿,且每年保持稳定成长。

预计北美将占据较大的市场占有率

- 北美正在迅速发展物联网设备在各行业的应用,包括医疗保健、汽车、智慧家庭和工业应用。 eSIM 技术在为这些设备提供无缝连接方面发挥关键作用,推动了 eSIM 市场的成长。

- 製造商正在将 eSIM 技术融入许多装置中,包括智慧型手机、平板电脑、穿戴式装置和物联网装置。随着越来越多的设备支援 eSIM,对 eSIM 服务的需求也预计会成长。

- 随着5G网路在北美加速部署,eSIM技术将透过提供无缝连接来补充5G网路功能,使消费者更容易切换通讯业者和计画。根据Cisco预测,到 2022 年,北美将成为使用穿戴式装置实现 5G 连接最多的地区。北美地区的连线数将达到4.39亿,比2017年4G网路连线数多出2.22亿。

- 随着该地区的 eSIM 价格大幅下降以及安全国际漫游解决方案相关计划的推出,这将大大促进该地区 eSIM 的采用。支援eSIM的行动电话允许用户从多个国家或漫游计划中进行选择,而多国营运商的价格往往比美国移动的解决方案要贵得多。如果用户出国旅行,他们可以选择营运商的漫游计划。有了 eSIM,更换通讯业者或漫游变得非常容易,因为用户只需扫描二维码或从设备上的选单中选择新的通讯业者。

- 2022 年 12 月,顶级消费科技订阅供应商之一 Grover 宣布推出美国科技租赁客户的 MVNO Grover Connect。透过 Grover Connect,该国客户可以快速启动支援 eSIM 的技术设备。 Grover 也与电信即服务平台的全球领导者之一 Giggs 合作,该平台使任何企业或品牌都可以成为 MVNO,并推出了这项创新的新服务。顾客可以在美国结帐时购买 Grover 的 eSIM,它将很快在欧洲上市。

嵌入式 SIM (eSIM) 产业概览

嵌入式 SIM(eSIM)市场较为分散,主要企业包括金雅拓公司(泰雷兹集团旗下)、Giesecke+Devrient GmbH、义法半导体公司、英飞凌科技股份公司和 Valid SA。市场参与者正在采取联盟和收购等策略来增强其产品供应并获得永续的竞争优势。

2023 年 2 月,Giesecke+Devrient (G+D) 及其合作伙伴 NetLync 宣布推出 AirOn360 ES。 AirOn360 ES 支援权利部署,包括从实体 SIM 卡或 eSIM 到 iPhone 的无缝 SIM 卡传输,从而允许行动电话电信业者提供便利的服务,例如简化的数位启动流程、完整的装置同步或 (e)SIM传输。对于用户来说,eSIM可以实现轻鬆的数位连接或快速迁移现有计划,从而可以在一台设备上使用多个行动电话计划。

2022 年 11 月,义法半导体与泰雷兹合作,为 Google Pixel 7 提供安全、非接触式的便利性。 ST54K 单晶片 NFC 控制器和安全元件与泰雷兹安全操作系统相结合,在嵌入式 SIM、交通票务和数位汽车钥匙应用中提供卓越的性能。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业相关人员分析 营运商、 OEM、系统整合商

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 新冠肺炎疫情如何影响连结性

- 全球支援 e-SIM 的设备出货量调查范围

第五章 市场动态

第六章 市场驱动因素

- 互联和 M2M 生态系的进展

- 对智慧型设备的需求不断增加

- 与传统方案相比,eSIM 具有易用性和可近性

第七章 市场挑战市场挑战

- 安全性和互通性标准化问题

第八章 市场机会

- 对 M2M 传播的极为乐观的预测

第九章:全球SIM卡情势分析(出货量及区域分布)

第 10 章 市场细分

- 按应用

- 智慧型手机

- 平板电脑和笔记型电脑

- 穿戴式装置

- M2M(工业、汽车等)

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 亚洲

- 中国

- 韩国

- 日本

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

- 北美洲

第十一章 竞争格局

- 公司简介

- Gemalto NV(Thales Group)

- Giesecke+Devrient GmbH

- STMicroelectronics NV

- Infineon Technologies AG

- Valid SA

- Idemia(Advent International Corp)

- Workz Group

- Truphone Limited

- Gigsky, Inc.

- ARM Limited

第 12 章供应商定位分析

第十三章 市场展望

The Embedded SIM Market is expected to register a CAGR of 7.05% during the forecast period.

An eSIM is a small, programmable chip embedded directly into devices, such as smartphones, tablets, wearable devices, and other IoT devices, allowing remote SIM provisioning without needing a physical SIM card.

Key Highlights

- The Internet of Things (IoT) was one of the key drivers for eSIM adoption. As the number of connected devices increased, managing physical SIM cards for each device became impartial. eSIM provided a scalable solution for deploying and managing IoT devices globally.

- Advancements in the connected and M2M (machine-to-machine) ecosystem were key drivers in the market's growth. The growth of the 5G network also creates new opportunities for eSIM adoption. Enterprises embraced eSIM for their M2M deployments, such as asset tracking, smart meters, industrial monitoring, and supply chain management.

- The growing demand for smart devices was one of the key drivers that increased the adoption of eSIM technology. Smart devices, including smartphones, tablets, wearables, connected cars, and various Internet of Things (IoT) devices, have become more prevalent in consumer and industrial applications.

- Security and interoperability standardization issues are restraining the market growth. With traditional SIM cards, physical access is required to tamper with or replace the SIM, making it more difficult for malicious actors to compromise the connection. However, as eSIM is soldered directly onto the device's circuitry, the potential for unauthorized access or cloning could be a significant security risk.

Embedded SIM (eSIM) Market Trends

Smartphones Application Segment is Expected to Hold Significant Market Share

- eSIM technology has been increasingly integrated into smartphones, bringing numerous benefits to consumers and mobile network operators (MNOs). eSIM eliminates the need for physical SIM cards, allowing users to activate and switch between mobile carriers more easily. With eSIMs, users can remotely provision their devices with a new carrier's profile without the hassle of acquiring a physical SIM card and waiting for it to be delivered.

- eSIM technology has enabled the adoption of dual-SIM functionality in smartphones. With a combination of eSIM physical card slots, users can have two active phone numbers on the same devices, which is especially useful for travelers, business professionals, or people with multiple cellular subscriptions.

- For mobile network operators, eSIM technology offers greater flexibility in onboarding new customers. Instead of distributing physical SIM cards through retail channels, MNOs can remotely provision eSIMs, simplifying the activation process and reducing distribution costs.

- eSIM plays a significant role in enabling connectivity for IoT devices. Smartphones are a gateway for various IoT applications, and eSIM technology provides a secure and efficient way to connect IoT devices to cellular networks.

- The ongoing development of 5G networks and the proliferation of IoT devices are expected to further the integration of eSIM in smartphones and other connected devices. According to Ericsson, the number of cellular IoT connections with critical IoT and broadband globally in 2022 was approximately 1.5 billion. In five years, the forecast is that the number of cellular IoT connections with the same connection type will continue to rise steadily each year, up to 3.3 billion.

North America is Expected to Hold Significant Market Share

- North America has witnessed a rapid rise in the adoption of IoT devices across various industries, including healthcare, automotive, smart home, and industrial applications. eSIM technology plays a crucial role in providing seamless connectivity for these devices, driving the growth of the eSIM market.

- Manufacturers have incorporated eSIM technology into many devices, including smartphones, tablets, wearables, and IoT devices. As more devices become eSIM-enabled, the demand for eSIM services is expected to rise.

- The deployment of 5G networks in North America has been gaining momentum. eSIM technology complements the capabilities of the 5G network by providing seamless connectivity and making it easier for consumers to switch between carriers and plans. According to Cisco Systems, North America will have the most 5G connections made using wearable devices in 2022. The 439 million connections in North America would be 222 million more than those made to 4G networks in 2017.

- The plans related to eSIM becoming significantly cheap in the region and a secure international roaming solution considerably drive the adoption of eSIM in the region. On phones with eSIM support, the user can select from several individual countries or roaming plans, where the multi-country operators tend to be significantly more expensive than US Mobile's solution. If the user is traveling abroad, he can select the carrier's roaming plan. The user can also buy a local SIM card or a multi-country travel SIM card like KnowRoaming, which is the most expensive. eSIM lets the user scan a QR code or pick a new carrier from an on-device menu, making it much easier to switch carriers or roam.

- In December 2022, Grover, one of the top subscription providers for consumer technology, unveiled Grover Connect, an MVNO for clients renting technology in the United States. The country clients can quickly activate any eSIM-enabled technology gadget using Grover Connect. Also, Grover partnered with Gigs, one of the global leaders in telecom-as-a-service platforms in the world that enables any business or brand to become an MVNO, to introduce this innovative new offering. Customers can purchase a Grover eSIM at checkout in the United States, which will soon be available in its European regions.

Embedded SIM (eSIM) Industry Overview

The embedded SIM (eSIM) market is fragmented, with the presence of major players like Gemalto N.V. (Thales Group), Giesecke+Devrient GmbH, STMicroelectronics N.V., Infineon Technologies AG, and Valid S.A. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

In February 2023, Giesecke+Devrient (G+D) and its partner NetLync launched AirOn360 ES, enabling Mobile Network Operators to deploy Entitlements, including the seamless SIM transfer on iPhone from physical SIM card or eSIM, allowing mobile operators to offer convenient services such as simplified and digital activation processes, synchronization of all devices, or (e)SIM transfers. For users, eSIM allows them to easily connect or quickly transfer their existing plans digitally and provides for multiple cellular plans on a single device.

In November 2022, STMicroelectronics collaborated with Thales, which powers secure, contactless convenience in Google Pixel 7. The ST54K single-chip NFC controller and secure element combine with Thales secure OS for superior performance in embedded SIM, transit ticketing, and digital car-key applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis Operator, OEM & System Integrators

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the Connectivity Landscape

- 4.5 Coverage on e-SIM Enabled Device Shipments Globally

5 MARKET DYNAMICS

6 Market Drivers

- 6.1 Advancements in the Field of Connected & M2M Ecosystem

- 6.2 Growing Demand for Smart Devices

- 6.3 Ease of Use and Access Provided by eSIM over Traditional Substitutes

7 Market Challenges

- 7.1 Security, Interoperability Standardization Issues

8 Market Opportunities

- 8.1 Highly Positive Forecasts for M2M Adoption

9 GLOBAL SIM CARD LANDSCAPE ANALYSIS (SHIPMENTS & REGIONAL BREAKDOWN)

10 MARKET SEGMENTATION

- 10.1 By Application

- 10.1.1 Smartphones

- 10.1.2 Tablets & Laptops

- 10.1.3 Wearables

- 10.1.4 M2M (Industrial, Automotive, etc.)

- 10.2 By Geography

- 10.2.1 North America

- 10.2.1.1 United States

- 10.2.1.2 Canada

- 10.2.2 Europe

- 10.2.2.1 United Kingdom

- 10.2.2.2 Germany

- 10.2.2.3 France

- 10.2.3 Asia

- 10.2.3.1 China

- 10.2.3.2 South Korea

- 10.2.3.3 Japan

- 10.2.3.4 Australia and New Zealand

- 10.2.4 Latin America

- 10.2.5 Middle East and Africa

- 10.2.1 North America

11 COMPETITIVE LANDSCAPE

- 11.1 Company Profiles

- 11.1.1 Gemalto N.V. (Thales Group)

- 11.1.2 Giesecke+Devrient GmbH

- 11.1.3 STMicroelectronics N.V.

- 11.1.4 Infineon Technologies AG

- 11.1.5 Valid S.A.

- 11.1.6 Idemia (Advent International Corp)

- 11.1.7 Workz Group

- 11.1.8 Truphone Limited

- 11.1.9 Gigsky, Inc.

- 11.1.10 ARM Limited

12 VENDOR POSITIONING ANALYSIS

13 MARKET OUTLOOK

旅游用eSIM的全球市场:2030年前的预测

旅游用eSIM的全球市场:2030年前的预测 eSIM 市场规模、份额、成长分析、按解决方案、按最终用户、按应用、按类型、按地区 - 行业预测,2024-2031 年

eSIM 市场规模、份额、成长分析、按解决方案、按最终用户、按应用、按类型、按地区 - 行业预测,2024-2031 年 eSIM 市场:按应用、产业划分 - 2025-2030 年全球预测

eSIM 市场:按应用、产业划分 - 2025-2030 年全球预测 eSIM:技术发展与市场规模预估-eSIM进入演进与成长的新阶段

eSIM:技术发展与市场规模预估-eSIM进入演进与成长的新阶段 eSIM市场、占有率、市场规模、趋势、行业分析报告:依解决方案、应用、地区、细分市场预测,2024-2032年

eSIM市场、占有率、市场规模、趋势、行业分析报告:依解决方案、应用、地区、细分市场预测,2024-2032年 旅行eSIM的全球市场:2024年

旅行eSIM的全球市场:2024年 eSIM 市场报告:2030 年趋势、预测与竞争分析

eSIM 市场报告:2030 年趋势、预测与竞争分析 全球物联网 eSIM 市场的成长机会

全球物联网 eSIM 市场的成长机会 eSIM 市场规模、份额和趋势分析报告:2023-2030 年按解决方案、应用、地区和细分市场分類的趋势

eSIM 市场规模、份额和趋势分析报告:2023-2030 年按解决方案、应用、地区和细分市场分類的趋势 SIM 卡和 eSIM:市场概况和分析

SIM 卡和 eSIM:市场概况和分析