|

市场调查报告书

商品编码

1406907

丙二醇:市场占有率分析、产业趋势与统计、2024年至2029年成长预测Propylene Glycol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

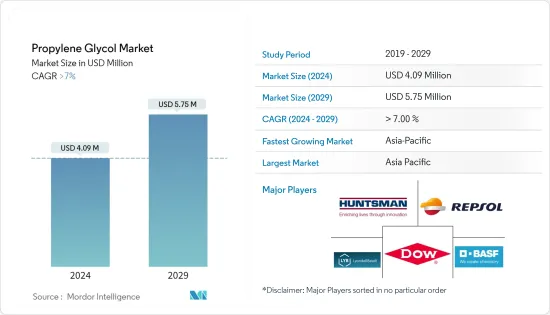

丙二醇市场规模预计到2024年为409万美元,预计到2029年将达到575万美元,在预测期内(2024-2029年)复合年增长率超过7%。

由于全国范围内的封锁、严格的社交距离措施和供应链中断,COVID-19大流行对市场产生了负面影响,对运输、建筑和建造等终端用户行业产生了负面影响,从而影响了丙二醇市场。 。不过,限购解除后,市场稳定復苏。由于丙二醇运输和製药终端用户行业的消费增加,市场已显着復苏。

主要亮点

- 食品加工和添加剂产业的需求不断增加,汽车产业的需求不断增加,以及各个最终用户产业对溶剂的需求不断增加,预计将推动丙二醇市场的发展。

- 由于丙二醇的大量消耗而引起的健康问题预计将阻碍市场的成长。

- 丙二醇生产的工业规模直接合成方法的开拓预计将在预测期内创造市场机会。

- 由于运输、建筑和製药最终用户产业对丙二醇的需求不断增加,预计亚太地区将主导市场。

丙二醇市场趋势

交通运输终端用户产业主导市场

- 丙二醇广泛应用于交通运输领域。它是一种黏稠、无色、无味的液体。吸湿性强,溶于醇、酯、水、胺、酮。与卤代烃的混溶性低,与脂肪族烃不混溶。它在交通运输行业中有着广泛的应用。

- 丙二醇用于生产耐火煞车油和液压液、运输行业中用于发动机冷却等应用的冷媒、油漆原材料的初始原材料、飞机的除冰原材料以及飞机的热载体。高温应用。将被使用。丙二醇也用于製备不饱和聚酯树脂,在交通运输领域发挥多种作用。

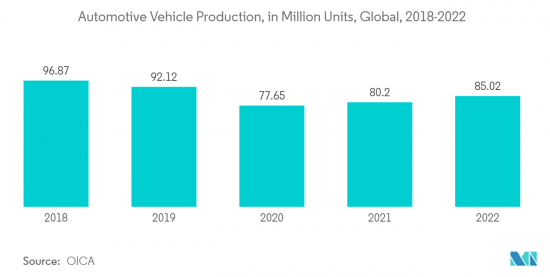

- 全球汽车产量的成长预计将推动丙二醇市场。根据OICA(国际汽车构造组织)预测,2022年全球汽车产量将达8,502万辆,而2021年为8,020万辆,成长率为6%。中国、美国和印度是世界上最重要的汽车市场。

- 美国是仅次于中国的全球第二大汽车市场,在全球汽车市场中占有很大份额。根据OICA统计,2022年美国汽车产量达1,006万辆,而2021年为915万辆,成长率为9%。这加强了汽车产业的成长并刺激了对丙二醇市场的需求。

- 根据波音《2023-2042年商业展望》,到2042年,新型商用喷射机的需求预计将达到42,595架飞机,达到8兆美元。到 2042 年,全球喷射机持有几乎翻倍,达到 48,600 架,每年增长 3.5%。航空公司将用新的、更省油的飞机取代全球约一半的机队。

- 此外,北美也是世界飞机生产中心。美国是该地区最大的飞机市场。空中巴士公司和波音公司是全国最大的飞机製造商。例如,2022年空中巴士交付了661架商用飞机,年终新增订单1,078架。同样,波音公司也订单了 57 737 架 Max 8喷射机,预计 2025 年交付。

- 因此,由于上述因素,运输终端用户产业预计将在预测期内推动丙二醇市场。

亚太地区主导市场

- 由于汽车、建筑、食品和食品和饮料等终端用户行业的需求不断增加,预计亚太地区将主导丙二醇市场。在该地区,中国、印度和日本是最大的丙二醇市场。

- 丙二醇用于製备不饱和聚合物树脂,用于製造管道和地板等建筑产品。在油漆工业中,丙二醇用作油漆的溶剂。

- 中国是全球最大的建筑市场,占全球整体建筑投资的20%。到 2030 年,中国预计将在建筑方面花费近 13 兆美元。因此,预计国内丙二醇前景乐观。

- 印度政府积极支持住宅建设,为约13亿人提供住宅。未来七年,该国预计将投资约1.3兆美元用于住宅建设,并建造6000万套新住宅。预计到 2024 年,该国经济适用住宅将增加约 70%。

- 此外,丙二醇也用于多种食用物品,包括咖啡饮料、液体甜味剂、冰淇淋、搅打乳製品和苏打水。食品和饮料需求的增加预计将在该地区创造丙二醇市场。

- 中国是该地区最大的食品和饮料市场。根据中国国家轻工业委员会统计,2022年年销售额超过280万美元的主要食品生产企业收益累计超过1.53兆美元。与2021年相比,总收入与前一年同期比较增5.6%,显示食品业成长强劲。

- 由于上述因素,亚太地区丙二醇市场预计在预测期内将大幅成长。

丙二醇产业概况

丙二醇市场本质上是部分一体化的。该市场的主要企业包括(排名不分先后)LyondellBasell Industries Holdings BV、 BASF SE、Repsol、Dow 和 Huntsman International LLC。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 食品加工及添加剂业丙二醇需求

- 汽车产业需求增加

- 各个最终用户产业对溶剂的需求不断增加

- 抑制因素

- 大量食用丙二醇引发的健康问题

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(以金额为准的市场规模)

- 按年级

- 工业

- 食品和饮料

- 药品

- 按用途

- 香味

- 防冻剂/消泡剂

- 不饱和聚酯树脂

- 化学中间体

- 其他用途(抗氧化剂、家用产品等)

- 按最终用户产业

- 运输

- 建筑/施工

- 食品和饮料

- 个人护理

- 药品

- 其他最终用户产业(电子、油漆等)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲

- 亚太地区

第六章竞争形势

- 併购、合资、联盟、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- ADEKA CORPORATION

- ADM

- AGC Chemicals

- BASF SE

- Chaoyang Chemicals, Inc.

- Dow

- Golden Dyechem

- Huntsman International LLC

- INEOS

- Lonza

- LyondellBasell Industries Holdings BV

- Repsol

- Shell plc

- SKC Chemicals

- Sumitomo Chemical Co., Ltd.

第七章 市场机会及未来趋势

- 工业规模直接合成丙二醇的开发

- 其他机会

The Propylene Glycol Market size is estimated at USD 4.09 million in 2024, and is expected to reach USD 5.75 million by 2029, growing at a CAGR of greater than 7% during the forecast period (2024-2029).

The COVID-19 pandemic had negatively impacted the market due to nationwide lockdowns, strict social distancing measures, and disruption in supply chains, which negatively affected the transportation, building, and construction end-user industries, thereby affecting the market for propylene glycol. However, the market recovered well after the restrictions were lifted. The market recovered significantly, owing to the rise in consumption of propylene glycol transportation and pharmaceuticals end-user industries.

Key Highlights

- The increasing demand from the food-processing and additives industry, the growing demand from the automotive industry, and the rising demand for solvents from various end-user industries are expected to drive the market for propylene glycol.

- The health issues created by the high consumption of propylene glycol are expected to hinder the market's growth.

- The development of industrial-scale direct synthesis methods for propylene glycol production is expected to create opportunities for the market during the forecast period.

- The Asia-Pacific region is expected to dominate the market due to rising demand for propylene glycol in transportation, building and construction, and pharmaceutical end-user industries.

Propylene Glycol Market Trends

Transportation End-User Industry to Dominate the Market

- Propylene glycol is widely used in the transportation sector. It is a viscous, colorless, odorless liquid. It is highly hygroscopic and soluble in alcohols, esters, water, amines, and ketones. It has limited miscibility with halogenated hydrocarbons and is not miscible with aliphatic hydrocarbons. It has a wide variety of applications in the transportation industry.

- Propylene glycol is used to produce fire-resistant brake and hydraulic fluids, coolants used in the transportation industry for applications like engine cooling, and more, as an initial for raw materials of paints, as a raw material for de-icing of planes, and as a heat transfer fluid for high-temperature applications. Propylene glycol is also used to prepare unsaturated polyester resins, with various roles in the transportation sector.

- The increase in the global production of automotive vehicles is expected to drive the market for propylene glycol. According to the Organisation Internationale des Constructeurs d'Automobiles" (OICA), global automotive vehicle production reached 85.02 million in 2022, compared to 80.2 million manufactured in 2021, at a growth rate of 6%. China, the United States, and India are the most prominent automotive vehicle markets globally.

- The United States is the second-largest automotive market in the world after China, which occupies a significant share of the global automotive vehicles market. According to OICA, in 2022, the United States automotive vehicle production reached 10.06 million compared to 9.15 million units manufactured in 2021, at a growth rate of 9%. This enhanced the growth of the automobile industry, which has stimulated the market demand for propylene glycol.

- According to the Boeing Commercial Outlook 2023-2042, the demand for new commercial jets by 2042 is expected to reach 42,595 units, valued at USD 8 trillion. The global fleet will nearly double to 48,600 jets by 2042, expanding by 3.5% annually. Airlines will replace about half of the global fleet with new, more fuel-efficient models.

- Moreover, North America is the hub for aeroplane production in the world. The United States is the largest market for airplanes in the region. Airbus and Boeing are the largest manufacturers of airplanes in the country. For instance, in 2022, Airbus delivered 661 commercial aircraft, registering 1,078 gross new orders by the end of the year. Similarly, Boeing Aeroplane OEM company received orders for 57 of the 737 Max 8 jets, with delivery expected through 2025.

- Hence, owing to the factors mentioned above, the transportation end-user industry is anticipated to drive the market for propylene glycol during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region is expected to dominate the market for propylene glycol with the increasing demand from automotive, construction, food, and beverage end-user industries. China, India, and Japan are the largest markets for propylene glycol in the region.

- Propylene glycol is used to prepare unsaturated polymer resins, which are used to make construction products like duct pipes and floor sheets, among others. In the paint industry, propylene glycol is used as a solvent in paints.

- China is the largest construction market in the world, encompassing 20% of all construction investments globally. China is expected to spend nearly USD 13 trillion on buildings and construction by 2030. This is anticipated to create a positive outlook for propylene glycol in the country.

- The Indian government has been actively boosting housing construction to provide houses to about 1.3 billion people. The country is likely to witness around USD 1.3 trillion of investment in housing over the next seven years, to witness the construction of 60 million new houses in the country. The availability of affordable housing in the country is expected to increase by around 70% by 2024.

- Furthermore, propylene glycol is also used in various edible items such as coffee-based drinks, liquid sweeteners, ice cream, whipped dairy products, and sodas. The increase in demand for food and beverage products is expected to create a market for propylene glycol in the region.

- China is the largest market for food and beverage in the region. According to the China National Light Industry Council, major food manufacturing companies with an annual turnover of over USD 2.8 million reported revenues of over USD 1.53 trillion in 2022. Compared to 2021, the total revenue registered a year-on-year growth of 5.6%, indicating strong growth in the food industry.

- Owing to the above-mentioned factors, the market for propylene glycol in the Asia-Pacific region is projected to grow significantly during the forecast period.

Propylene Glycol Industry Overview

The propylene glycol market is partially consolidated in nature. Some of the major players in the market include (not in any particular order) LyondellBasell Industries Holdings BV, BASF SE, Repsol, Dow, and Huntsman International LLC, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Demand for Propylene Glycol in the Food Processing and Additives Industry

- 4.1.2 The Increasing Demand from the Automotive Industry

- 4.1.3 Rising Demand for For Solvents From Various End-User Industries

- 4.2 Restraints

- 4.2.1 Health Issues Created by The High Consumption of Propylene Glycol

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Grade

- 5.1.1 Industrial

- 5.1.2 Food and Beverage

- 5.1.3 Pharmaceutical

- 5.2 Application

- 5.2.1 Flavoring Agent

- 5.2.2 Antifreeze and Deicer Agent

- 5.2.3 Unsaturated Polyester Resins

- 5.2.4 Chemical Intermediates

- 5.2.5 Other Applications (Antioxidants, Household Care, etc.)

- 5.3 End-user Industry

- 5.3.1 Transportation

- 5.3.2 Building and Construction

- 5.3.3 Food and Beverages

- 5.3.4 Personal Care

- 5.3.5 Pharmaceuticals

- 5.3.6 Other End-user Industries (Electronics, Paints and Coatings, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ADEKA CORPORATION

- 6.4.2 ADM

- 6.4.3 AGC Chemicals

- 6.4.4 BASF SE

- 6.4.5 Chaoyang Chemicals, Inc.

- 6.4.6 Dow

- 6.4.7 Golden Dyechem

- 6.4.8 Huntsman International LLC

- 6.4.9 INEOS

- 6.4.10 Lonza

- 6.4.11 LyondellBasell Industries Holdings B.V.

- 6.4.12 Repsol

- 6.4.13 Shell plc

- 6.4.14 SKC Chemicals

- 6.4.15 Sumitomo Chemical Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Industrial-scale Direct Synthesis Method for Propylene Glycol Production

- 7.2 Other Opportunities

丙二醇市场规模、份额、趋势分析报告:按来源、等级、最终用途、地区、细分市场预测,2025-2030 年

丙二醇市场规模、份额、趋势分析报告:按来源、等级、最终用途、地区、细分市场预测,2025-2030 年 2025年全球戊二醇市场

2025年全球戊二醇市场 全球生物基丙二醇市场规模(按应用、最终用户、区域范围和预测)

全球生物基丙二醇市场规模(按应用、最终用户、区域范围和预测) 2025年生物基丙二醇全球市场报告全球丙二醇市场研究报告-产业分析、规模、份额、成长、趋势与预测 2025 年至 2033 年2025 年丙二醇全球市场报告

2025年生物基丙二醇全球市场报告全球丙二醇市场研究报告-产业分析、规模、份额、成长、趋势与预测 2025 年至 2033 年2025 年丙二醇全球市场报告 丙二醇市场规模、份额、成长分析,按来源、按等级、按应用、按最终用途行业、按地区 - 行业预测,2025-2032 年

丙二醇市场规模、份额、成长分析,按来源、按等级、按应用、按最终用途行业、按地区 - 行业预测,2025-2032 年 生物基丙二醇的全球市场:用途·终端用户产业·各地区 (~2032年)

生物基丙二醇的全球市场:用途·终端用户产业·各地区 (~2032年) 全球丙二醇醚市场(2018-2034)全球丙二醇醚市场:产业分析、规模、占有率、成长、趋势和预测(2025-2032 年)

全球丙二醇醚市场(2018-2034)全球丙二醇醚市场:产业分析、规模、占有率、成长、趋势和预测(2025-2032 年)