|

市场调查报告书

商品编码

1407062

移动机器人:市场占有率分析、产业趋势与统计、2024年至2029年成长预测Mobile Robots - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

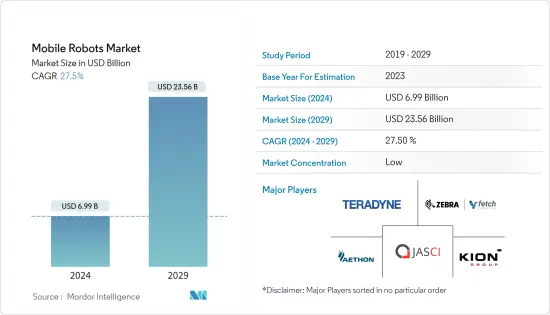

移动机器人市场规模预计到2024年将达到69.9亿美元,预计2029年将达到235.6亿美元,在预测期内(2024-2029年)复合年增长率为27.5%。

随着电子商务在全球范围内活性化,对行动机器人的需求正在扩大。仓库自动化程度的提高以及这些机器人在各个行业中的接受度不断提高,因为它们即使在恶劣的条件下也可以自主操作,预计将进一步推动市场扩张。此外,越来越多地采用自动化物料搬运和熄灯自动化等趋势可能会在预测期内推动市场扩张。

主要亮点

- 电子商务行业的成长以及全球对高效仓储和库存管理的需求正在推动市场成长。例如,根据 IBEF 的数据,印度电子商务市场预计将从 2017 年的 385 亿美元成长到 2026 年的 2,000 亿美元。

- 由于成本下降、运费降低、客户需求增加以及贸易全球化等因素,海运货物的货柜使用量稳定增加。因此,货柜码头已成为物流网路的重要组成部分。为了满足客户需求,船舶能够在港口快速装卸至关重要。

- 移动机器人正成为港口码头日益普及的货柜运输方式。这些无人驾驶车辆在船舶和陆地储存地点之间转移货柜。货柜码头的效率与每艘船舶在港的停留时间直接相关。因此,为了保持竞争优势并提高货柜码头的效率,AGV正在被引入以製定更好的调度策略,同时提高营运效率。

- 随着社交距离成为职场的常态,连网型解决方案和自动化正在帮助日常业务的持续进行。参与Honeywell研究的公司认为有必要使用移动机器人来指导工作解决方案和电脑控制设备。此外,仓库执行软体(48%)、拣货技术(46%)和机器人解决方案(44%)是目前广泛部署的解决方案,预计在不久的将来会有进一步投资。

- 工业环境中的无线通讯系统必须确保资讯的传输和接收在准确的时间范围内进行。然而,由于无线通道和媒体存取控制(MAC)的性质,会出现随机通讯延迟。这种延迟可能会导致网路控制系统的自动引导车辆出现严重的效能问题。

移动机器人市场趋势

自主移动机器人(AMR)推动市场成长

- 直到最近,传统的自动导引运输车(AGV) 仍然是内部运输任务自动化的唯一选择。但现在自主移动机器人 (AMR) 正以更先进、更具适应性且价格实惠的技术威胁 AGV。

- 由于其独特的操作特性和模式,近年来对自主机器人的需求显着增加。自主机器人在汽车和医疗保健等各个工业领域的使用不断增加,以及人们对自主移动机器人优势的认识不断增强,都推动了对自主移动机器人的需求。然而,高昂的安装成本和网路覆盖范围不足可能会限制自主移动机器人的采用。

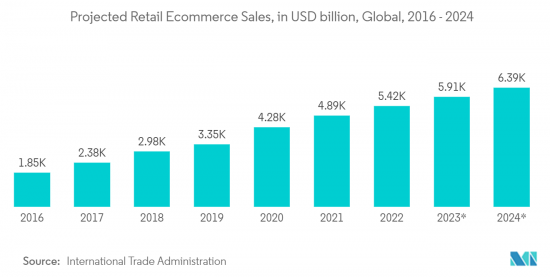

- 电子商务现已成为消费者首选的购物方式。电子商务提供的选择、人性化的体验以及随时随地购物和支付的便利性是推动电子商务产业成长的因素。根据国际贸易局预测,到2024年,全球零售电商销售额预计将达到63,880亿美元。

- 由于需要保证向经常期望即时满足的客户及时交货,以及由此产生的持续跟踪和补充产品库存的需求,电子商务公司现在使用 AMR 来提高大型仓库和配送中心的运营效率他们运作。因此,电子商务业务的快速成长对AMR市场的成长做出了巨大贡献。

- 此外,AMR能够适应不同的工作流程,回应工厂流程变化,并能够与多个顶级模组整合以满足有效负载要求。这可以实现智慧、可靠的交付并优化整个流程。因此,AMR 在投资收益和生产力优化方面优于 AGV。

中国正在经历快速成长

- 中国拥有全球最大的製造业,产生很大份额的市场需求。此外,根据工业和资讯化部 (MIIT) 的数据,儘管因 COVID-19 限制措施导致生产和物流中断,但 2022 年中国工业产值仍与前一年同期比较增长 3.6%。根据工信部预测,2022年製造业产值预估成长3.1%,占中国国内生产总值(GDP)的28%。

- 此外,中国政府的「中国製造2025」主导是一项国家主导的产业政策,旨在让中国在全球高科技製造业中占据优势,为市场带来显着的成长动力。 「中国製造2025」是一个透过快速发展10个高新技术产业来更新中国製造基础的十年计画。主要领域包括电动车等新能源车、新一代资讯科技(IT)和通讯、尖端机器人和人工智慧等。这些领域也是第四次工业革命的核心。

- 市场的另一个重要趋势是,许多企业正在加大投资,扩大国内产能。例如,2022年12月,ABB在中国上海正式开设了一家最先进的、全自动化、灵活的机器人工厂。该生产研发基地占地67,000平方米,公司投资1.5亿美元,将在下一代机器人生产中引入公司的数位化和自动化技术,巩固ABB在中国机器人和自动化领域的领先地位。加强.此外,该工厂没有传统的固定组装;取而代之的是智慧型、自主和移动机器人,以数位方式连接、网路和服务灵活的模组化生产单元。

- 随着移动机器人不断进入各种商业和工业环境以及新的参与者进入该领域,这个市场正在吸引许多中国投资者的投资。国内机器人企业近年来受惠于资金大幅增加。

- 此外,人口高龄化和人事费用上升也影响了中国对移动机器人的需求。例如,根据中国国家统计局的数据,目前中国约有14个地区,包括北京、江苏、河北、浙江、广东和四川,最低月薪超过2,000元人民币(308美元)。

移动机器人产业概况

移动机器人市场竞争激烈,已进入分散化阶段,多家企业在竞争相当激烈的市场空间中争夺注意力。此外,公司的策略决策,例如新产品发布、投资和联盟,预计将改变竞争形势。主要市场参与者包括 Teledyne Inc.、Fetch Robotics、Aethon Inc. 和 KION Group AG。

2023 年 4 月,创新仓库管理和自动化解决方案供应商 JASCI Software 与 Tompkins Robotics 合作,推出大量拣选和机器人单元分类技术。该公司还投资于研发,为客户提供增强和创新的产品。

2023 年 3 月,ClearPath 旗下公司 OTTO Motors 推出了 OTTO 600,这是同类产品中最具挑战性和敏捷性的 AMR。从 OTTO 600 简介来看,OTTO Motors 目前持有市场上最大的自动物料搬运车辆车队。 OTTO 600 是一款 AMR,专为在最严苛的工厂环境中运作而设计,采用全金属结构和 IP54 防护等级。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 产业价值链分析

- 宏观趋势对市场的影响

第五章市场动态

- 市场驱动因素

- 电子商务的快速成长导致仓库自动化

- 已开发国家人事费用增加

- 市场抑制因素

- 高资本要求和连接问题

第六章市场区隔

- 副产品

- 自动导引运输车(AGV)

- 自主机器人(AMR)

- 按外形尺寸

- 堆高机

- 拖车/拖拉机/拖船

- 单位负荷

- 组装

- 透过导航感测器

- 反射镜

- QR 图码

- 雷射/光达

- 相机、混合(相机和 LiDAR)和其他导航感测器

- 按使用环境

- 製造业(汽车、电气/电子、食品和饮料、化学品/製药和其他商业环境)

- 非製造业(物流中心/配送中心/仓库)

- 按地区

- 美国

- 欧洲

- 亚太地区(不包括中国)

- 中国

- 世界其他地区

第七章竞争形势

- 公司简介

- Teradyne Inc(Mobile Industrial Robots ApS(MIR))

- Fetch Robotics

- JASCI LLC

- Aethon Inc.

- KION Group AG

- SCOTT TECHNOLOGY LIMITED

- Murata Machinery Ltd

- Toyota Material Handling US

- John Bean Technologies(JBT)Corporation

- 6 River Systems Inc

- inVia Robotics Inc.

- IAM Robotics LLC

- GreyOrange Pte Ltd

- Clearpath Robotics Inc.

- Geek+Inc

- Omron Corporation

- Daifuku Co. Ltd

第八章 厂商排名分析

第九章投资分析

第十章投资分析未来展望

The Mobile Robots Market size is estimated at USD 6.99 billion in 2024, and is expected to reach USD 23.56 billion by 2029, growing at a CAGR of 27.5% during the forecast period (2024-2029).

Due to increased e-commerce activity worldwide, demand for mobile robots is expanding. Due to their capacity to maneuver autonomously in challenging situations, factors such as growing warehouse automation and rising acceptance of these robots across various industries are further projected to drive market expansion. Furthermore, the rising adoption of automated material handling and trends like lights-out automation will likely drive market expansion throughout the projection period.

Key Highlights

- The growth in the e-commerce industry and the need for efficient warehousing and inventory management worldwide are driving the market growth. For instance, according to IBEF, the Indian e-commerce market is expected to flourish from USD 38.5 billion in 2017 to USD 200 billion by 2026.

- Factors such as decreasing costs, lower rates of transport, rising customer demand, and globalization of trade have caused a steady increase in the use of containers for sea-borne cargo. Consequently, container terminals have become an important component of logistic networks. It is paramount that ships are unloaded and loaded promptly at the port to satisfy customer demand.

- Mobile Robots are increasingly becoming the popular mode of container transport in seaport terminals. These unmanned vehicles transfer containers between ships and storage locations on land. The e?ciency of a container terminal is directly related to the amount of time each vessel spends in the port. Hence, to maintain competitive advantage and increase the efficiency of the container terminal, AGVs are being deployed that formulate good dispatching strategies and simultaneously enhance operational efficiencies.

- With social distancing becoming more common in the workplace, connected solutions and automation assist in continuing daily operations. The use of mobile robots guides work solutions, and computer-controlled equipment has been regarded as necessary by companies in Honeywell's Study. Moreover, warehouse execution software (48 percent ), order-picking technology (46 percent ), and robotic solutions (44 percent ) have been widely implemented solutions currently, which are also most expected to receive further investment soon.

- Wireless communication systems in industrial environments must guarantee that the information is sent and received within precise time bounds. However, the nature of the radio channels and the medium access control (MAC) generates random communication delays. These delays can cause severe performance problems in automated guided vehicles for networked control systems.

Mobile Robots Market Trends

Autonomous Mobile Robot (AMR) to Witness the Market Growth

- Until recently, traditional automated guided vehicles (AGVs) were the only option for automating internal transportation tasks. However, in the present day, autonomous mobile robots (AMRs) threaten AGVs with their more advanced, adaptable, and affordable technology.

- Due to their unique operational characteristics and patterns, the demand for autonomous robots has recently increased significantly. Growth in the application of autonomous robots in different industrial sectors such as automotive and healthcare and raising awareness about the benefits of autonomous mobile robots fuel the demand for autonomous mobile robots. However, high costs associated with the setup and insufficient internet connectivity coverage might limit the adoption of autonomous mobile robots.

- E-commerce has now emerged as the preferred mode of shopping for customers. The choices it offers, the user-friendly experience it provides, and the convenience of shopping and paying for it from anywhere at any time are some of the factors driving the growth of the e-commerce industry. According to the International Trade Administration, global retail e-commerce sales are expected to reach USD 6,388 billion by 2024.

- Driven by the need to ensure timely delivery to their customers, who often expect instant gratification, and the resulting need to continually track and restock inventory of the goods, e-commerce companies are now using AMRs to improve the operational efficiencies of the big warehouses and distribution centers they operate. Thus, the rapid growth of the e-commerce business is contributing in a significant way to the growth of the AMR market.

- Further, AMRs can adapt to different workflows, accommodate factory process changes, and allow integration with several top modules to meet payload requirements. This enables smart, reliable deliveries and optimizes overall processes. Consequently, AMRs are superior to AGVs regarding return on investment and productivity optimization.

China to Witness Rapid Growth

- China has the world's largest manufacturing industry, generating a significant share of market demand. Moreover, the country's industrial output grew by 3.6% in 2022 from the previous year, as per the Ministry of Industry and Information Technology (MIIT), despite production and logistics disruptions from COVID-19 curbs. The manufacturing sector's output was estimated to have risen by 3.1% in 2022, accounting for 28% of China's gross domestic product (GDP), according to the MIIT.

- Moreover, the Chinese government's Made in China 2025 initiative, a state-led industrial policy that seeks to make China dominant in global high-tech manufacturing, provides significant growth momentum to the market. Made in China 2025 is a ten-year plan to update the country's manufacturing base by rapidly developing ten high-tech industries. Chief among these are electric cars and other new energy vehicles, next-generation information technology (IT) and telecommunications, and advanced robotics and artificial intelligence. These sectors are also central to the fourth industrial revolution.

- Increasing investments by many players in expanding their production capacities in the country is another important trend for the market. For instance, in December 2022, ABB officially opened its state-of-the-art, fully automated, and flexible robotics factory in Shanghai, China. The 67,000 m2 production and research facility represents a USD 150 million investment by the company and is likely to deploy the company's digital and automation technologies to manufacture next-generation robots, enhancing ABB's robotics and automation leadership in China. Moreover, there are no traditional, fixed assembly lines in the facility; instead, intelligent, autonomous mobile robots connect to, network, and service flexible, modular production cells digitally.

- As mobile robots continue to make their way into various commercial and industrial settings and new players enter the sector, the market has been drawing increasing investments from many Chinese investors. Domestic robotics companies have been benefiting from a significant increase in funds in recent years.

- Moreover, the aging population and increasing labor costs are also influencing the demand for mobile robots in China. For instance, according to the National Bureau of Statistics of China, about 14 regions in China currently have a minimum monthly wage of over RMB 2,000 (USD 308), including Beijing, Jiangsu, Hebei, Zhejiang, Guangdong, and Sichuan.

Mobile Robots Industry Overview

The mobile robots market is competitive, moving towards a fragmented stage owing to the growing interest of several companies vying for attention in a fairly contested market space. Further, companies' strategic decisions, such as new product launches, investments, and collaborations, are expected to change the competitive landscape. Some key market players include Teledyne Inc., Fetch Robotics, Aethon Inc., and KION Group AG, among others.

In April 2023, JASCI Software, a provider of innovative warehouse management and automation solutions, partnered with Tompkins Robotics to launch batch pick and robotic unit sortation technology that would revolutionize how goods are sorted and stored in warehouses. Further, the company also aims to invest in research and development initiatives with the aim of providing its customers with enhanced and innovative products on the market.

In March 2023, OTTO Motors, a Clearpath company, unveiled the OTTO 600, the most challenging and agile AMR in its class. With the introduction of the OTTO 600, OTTO Motors now has the market's largest fleet of autonomous material-handling vehicles. The OTTO 600 is an AMR built to perform in the most demanding factory environments, with an all-metal construction and an IP54 rating.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of Macro Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapid Growth of E-commerce Leading to Warehouse Automation

- 5.1.2 Increasing Labor Costs in the Developed Nations

- 5.2 Market Restraints

- 5.2.1 High Capital Requirements and Connectivity Issues

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Automated Guided Vehicle (AGV)

- 6.1.2 Autonomous Mobile Robot (AMR)

- 6.2 By Form Factor

- 6.2.1 Forklifts

- 6.2.2 Tow/Tractor/Tug

- 6.2.3 Unit Load

- 6.2.4 Assembly Line

- 6.3 By Navigation Sensor

- 6.3.1 Reflector

- 6.3.2 QR Code

- 6.3.3 Laser/LiDAR

- 6.3.4 Camera, Hybrid (Camera & LiDAR) and Other navigation sensors

- 6.4 By Environment of Operation

- 6.4.1 Manufacturing (Automotive, Electrical & Electronics, Food & Beverage, Chemical & Pharmaceuticals and Other Environments of Operation)

- 6.4.2 Non-Manufacting (Logistics Centers/Distribution Centers/Warehouses)

- 6.5 By Geography

- 6.5.1 United States

- 6.5.2 Europe

- 6.5.3 Asia-Pacific (Excluding China)

- 6.5.4 China

- 6.5.5 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Teradyne Inc (Mobile Industrial Robots ApS (MIR))

- 7.1.2 Fetch Robotics

- 7.1.3 JASCI LLC

- 7.1.4 Aethon Inc.

- 7.1.5 KION Group AG

- 7.1.6 SCOTT TECHNOLOGY LIMITED

- 7.1.7 Murata Machinery Ltd

- 7.1.8 Toyota Material Handling US

- 7.1.9 John Bean Technologies (JBT) Corporation

- 7.1.10 6 River Systems Inc

- 7.1.11 inVia Robotics Inc.

- 7.1.12 IAM Robotics LLC

- 7.1.13 GreyOrange Pte Ltd

- 7.1.14 Clearpath Robotics Inc.

- 7.1.15 Geek+ Inc

- 7.1.16 Omron Corporation

- 7.1.17 Daifuku Co. Ltd

8 VENDOR RANKING ANALYSIS

9 INVESTMENT ANALYSIS

10 FUTURE OUTLOOK

移动机器人市场规模、份额和成长分析(按机器人类型、有效载荷、最终用途和地区)- 产业预测 2025-2032

移动机器人市场规模、份额和成长分析(按机器人类型、有效载荷、最终用途和地区)- 产业预测 2025-2032 全球移动机器人市场:市场规模、份额、趋势分析(按组件、产品、应用和地区)、细分市场预测(2025-2030 年)

全球移动机器人市场:市场规模、份额、趋势分析(按组件、产品、应用和地区)、细分市场预测(2025-2030 年) 移动机器人市场:按类型、组件、移动性、有效负载能力、应用、最终用途 - 2025-2030 年全球预测

移动机器人市场:按类型、组件、移动性、有效负载能力、应用、最终用途 - 2025-2030 年全球预测 行动机器人充电站的全球市场:产业分析,规模,占有率,成长,趋势,预测(2024年~2031年)

行动机器人充电站的全球市场:产业分析,规模,占有率,成长,趋势,预测(2024年~2031年) 移动机器人市场:按组件、类型、操作条件和应用分类 - 2025-2030 年全球预测

移动机器人市场:按组件、类型、操作条件和应用分类 - 2025-2030 年全球预测 行动控制机器人市场 - 全球产业规模、份额、趋势、机会和预测,按类型、按产品、按应用、按地区和竞争,2019-2029F

行动控制机器人市场 - 全球产业规模、份额、趋势、机会和预测,按类型、按产品、按应用、按地区和竞争,2019-2029F 移动机器人

移动机器人 2030 年移动机器人市场预测:按类型、部署模式、技术、最终用户和地区进行的全球分析

2030 年移动机器人市场预测:按类型、部署模式、技术、最终用户和地区进行的全球分析 2024 年移动机器人世界市场报告

2024 年移动机器人世界市场报告 全球移动机器人市场:按机器人类型(自主自动导引车/自主移动机器人)、应用、最终用户产业和地区预测(~2032年)

全球移动机器人市场:按机器人类型(自主自动导引车/自主移动机器人)、应用、最终用户产业和地区预测(~2032年)