|

市场调查报告书

商品编码

1692480

再生碳纤维:市场占有率分析、产业趋势与统计、成长预测(2025-2030)Recycled Carbon Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

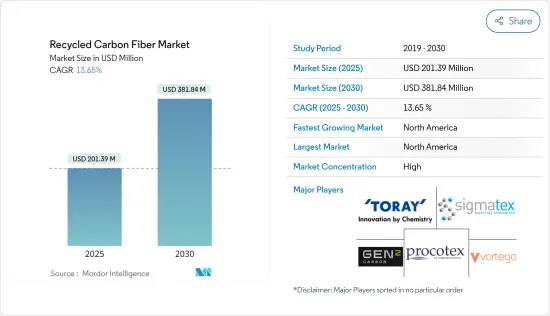

2025 年再生碳纤维市场规模估计为 2.0139 亿美元,预计到 2030 年将达到 3.8184 亿美元,预测期内(2025-2030 年)的复合年增长率为 13.65%。

主要亮点

- 2020 年,由于供应链中断,市场受到 COVID-19 的不利影响。随着疫情蔓延,全球许多涉及碳纤维回收的製造厂被迫关闭。然而,自限制解除以来,由于风力发电等各个终端用户行业的需求增加,该行业已经復苏。

- 短期内,轻型车辆需求的增加、碳纤维废料回收的增加、风力发电领域的再利用增加以及回收碳纤维的成本效益是推动市场需求的一些因素。

- 再生碳纤维的各种替代品的可用性和供应链安全是阻碍市场成长的因素。

- 更加重视永续性、回收技术研发的进步以及积层製造和 3D 列印领域不断增长的潜在需求可能会在未来几年为市场创造机会。

- 预计北美将主导市场,并在预测期内以最高的复合年增长率成长。

再生碳纤维的市场趋势

在航太和国防工业的应用日益增多

- 回收的碳纤维具有与用于生产航太和国防工业所用复合材料的原始碳纤维相似的特性。这些碳纤维为航太和国防工业中使用的零件提供了独特的优势,例如在恶劣条件和高温下的耐用性、耐磨损和腐蚀性。

- 飞机正在使用回收的碳纤维来取代铝,以提高燃油效率。更轻的材料和结构使得军用飞机可以携带更多的燃料和有效载荷,而民航机可以携带更少的燃料和有效载荷。

- 使用轻质材料可以减少温室气体排放和送往垃圾垃圾掩埋场的废弃物量。例如,波音787重量减轻20%,燃油效率更高,燃油经济性提高近10%至12%。

- 此外,为了解决严重的飞机废弃物问题,航太业越来越倾向于使用再生碳纤维。全球航太业估计,到2030年,约有6,000至8,000架飞机将达到使用寿命。

- 空中巴士的目标是在 2020 年至 2025 年期间回收 95% 的碳纤维废弃物,并将 5% 重新用于航太领域。空中巴士 2021 年的飞机订单总数为 771 架,而 2020 年为 383 架。

- 随着乘客数量的增加和飞机退役数量的增加,预计未来 20 年将需要 44,040 架新喷射机,价值 6.8 兆美元。预计到 2038 年,全球民航机队数量将达到 50,660 架,其中包括所有新飞机和潜在的剩余喷射机。

- 根据国际航空运输协会(IATA)的数据,2020年全球商业航空公司的销售额价值为3,730亿美元,预计2021年将达到4,720亿美元,比与前一年同期比较增长26.7%。预计到 2022 年底将达到 6,580 亿美元。

- 波音公司预计,到2040年,全球民航机持有超过4.9万架,其中中国、欧洲、北美和亚太国家各占新飞机交付的20%左右,其余20%则流向其他新兴市场。

- 由于这些因素,预计预测期内全球再生碳纤维市场将成长。

北美占据市场主导地位

- 预计北美地区将占据市场主导地位。以国内生产毛额计算,美国是该地区最大的经济体。美国和加拿大是世界上成长最快的新兴经济体之一。

- 快速发展的汽车和航太工业正在推动北美地区所研究市场的成长。策略发展、成熟的汽车製造商、领先的再生碳纤维製造商的存在以及与再生碳纤维产品相关的技术进步都促进了该地区市场的成长。

- 美国是该地区再生碳纤维消费的领导者,并被各大公司所使用。由于对减轻车辆重量的轻量材料的需求不断增长,该地区汽车和航太终端行业对再生碳纤维的使用正在增加。

- 此外,美国联邦航空管理局(FAA)表示,2020年美国商用飞机数量为5,882架,与前一年同期比较减少22.9%。然而,预计到 2041 年这一数量将增长至 8,756 架,复合年增长率为 2%。预计这将增加航太工业多种应用对碳纤维的需求。

- 在加拿大,魁北克复合材料开发中心(CDCQ)在包括碳纤维在内的各种复合材料的价值链中进行了一系列活动。该中心也积极参与碳纤维的回收利用。

- 在全球范围内,加拿大在民用飞行模拟领域排名第一,在民用引擎生产领域排名第三,在民航机生产领域排名第四。加拿大是唯一一个在所有主要类别中均排名前五名的国家。加拿大航太航太业70%以上的产品出口到六大洲190多个国家。

- 加拿大的风力发电占发电量的3.5%,是该地区第二大可再生能源发电来源。风力发电在实现全球净零碳排放发挥关键作用。加拿大拥有多种能源来源,包括水力、生质能、风能和太阳能,是世界可再生能源生产和使用的领导者之一。

- 由于这些因素,预计该地区的再生碳纤维市场在预测期内将稳定成长。

再生碳纤维产业概况

再生碳纤维市场部分整合。该市场的主要企业包括(不分先后顺序)东丽、Procotex、Vartega Inc.、Gen 2 Carbon Limited 和 Sigmatex。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 对轻型车辆的需求不断增加

- 提高风力发电领域碳纤维废弃物的回收再利用

- 回收碳纤维的成本效益

- 限制因素

- 有多种替代方案

- 再生碳纤维供应链的安全

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔

- 种类

- 短切再生碳纤维

- 再生碳纤维

- 酱

- 汽车废料

- 航太废料

- 其他的

- 最终用户产业

- 车

- 航太与国防

- 风力发电

- 体育用品

- 其他最终用户产业

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲国家

- 世界其他地区

- 南美洲

- 中东和非洲

- 亚太地区

第六章竞争格局

- 併购、合资、合作与协议

- 市场排名分析

- 主要企业策略

- 公司简介

- Alpha Recyclage Composites

- Carbon Conversions

- Carbon Fiber Recycling

- Carbon Fiber Remanufacturing

- Gen 2 Carbon Limited

- Karborek RCF

- Mitsubishi Chemical Holdings Corporation.

- Procotex

- Shocker Composites LLC

- Sigmatex

- Toray Industries Inc.

- Vartega Inc.

第七章 市场机会与未来趋势

- 朝向永续性转变

- 回收技术研发进展

- 积层製造和 3D 列印的需求潜力增加

简介目录

Product Code: 91476

The Recycled Carbon Fiber Market size is estimated at USD 201.39 million in 2025, and is expected to reach USD 381.84 million by 2030, at a CAGR of 13.65% during the forecast period (2025-2030).

Key Highlights

- The market was negatively impacted by COVID-19 in 2020 due to disruption in the supply chain. As the pandemic spread, many manufacturing plants involved in the recycling of carbon fiber globally were shut down due to the strict lockdowns. However, the sector has been recovering since restrictions were lifted owing to increased demand from various end-user industries, such as wind energy.

- Over the short term, the rising demand for lightweight vehicles, growing carbon fiber scrap recycling, its increasing reuse in the wind energy sector, and the cost-effectiveness of recycled carbon fiber are some of the factors driving the market demand.

- The availability of various substitutes and supply chain security for recycled carbon fiber are the factors hindering the market's growth.

- Shifting focus toward sustainability, advancement in research and development for recycling techniques, and increasing potential demand from additive manufacturing and 3D printing sectors are likely to create opportunities for the market in the coming years.

- The North American region is expected to dominate the market and is likely to witness the highest CAGR during the forecast period.

Recycled Carbon Fiber Market Trends

Increasing Usage in the Aerospace and Defense Industry

- Recycled carbon fiber possesses similar properties to new carbon fiber used for manufacturing composites that are used in the aerospace and defense industry. These carbon fibers offer specific advantages to components used for the aerospace and defense industry, such as durability in harsh conditions and at high temperatures, abrasion resistance, and corrosion resistance.

- Recycled carbon fiber has replaced aluminum in aircraft to improve fuel economy. Lightweight materials and structures allow military aircraft to carry more fuel and payload while in commercial aircraft.

- Lightweight materials are used to reduce greenhouse gas emissions and the amount of waste sent to landfills. For instance, the Boeing 787 was made 20% lighter, which helped in increasing the fuel economy by nearly 10% to 12%.

- Moreover, the preference for recycled carbon fiber is also increasing in the aerospace industry to manage the significant problem of aircraft waste. It is estimated that, in the global aerospace industry, about 6000-8000 aircraft will reach the end of their service life by 2030, which may create a potential source for carbon recycling in the industry.

- Airbus has set a target of recycling 95% of its carbon fiber waste by 2020-2025, with 5% recycled back into the aerospace sector. The gross orders of aircraft for airbus were 771 units in 2021, as compared to 383 units in 2020.

- The growing passenger volumes and increasing retirements of aircraft are expected to drive the need for 44,040 new jets (valued at USD 6.8 trillion) over the next two decades. The global commercial fleet is expected to reach 50,660 aircraft by 2038, considering all the new aircraft and jets that may remain in service.

- According to the International Air Transport Association (IATA), the global revenue for commercial airlines was valued at USD 373 billion in 2020 and was estimated at USD 472 billion in 2021, registering a growth rate of 26.7% Y-o-Y. Furthermore, the revenue was expected to reach USD 658 billion by the end of 2022.

- According to Boeing, by 2040, the worldwide commercial fleet will exceed 49,000 planes, with China, Europe, North America, and the Asia-Pacific countries each accounting for around 20% of new plane deliveries and the remaining 20% going to other rising markets.

- Owing to all these factors, the market for recycled carbon fiber is likely to grow globally during the forecast period.

The North American Region to Dominate the Market

- The North American region is expected to dominate the market. In the region, the United States is the largest economy in terms of GDP. The United States and Canada are among the fastest emerging economies in the world.

- The fast-growing automotive and aerospace industries are driving the growth of the market studied in the North American region. Strategic developments, the presence of established car manufacturers, leading recycled carbon fiber manufacturers, and technological advancements related to recycled carbon fiber products all contribute to the market's growth in this region.

- The United States is the region's leader in the consumption of recycled carbon fiber, which is used by major corporations. Due to the growing demand for lightweight materials to reduce vehicle weight, the use of recycled carbon fiber in the automotive and aerospace end-use industries has increased in the region.

- Moreover, in the United States, according to the Federal Aviation Administration (FAA), the number of aircraft in the country's commercial fleet accounted for 5,882 in 2020, witnessing a decline rate of 22.9% compared to the previous year. However, the commercial fleet is projected to increase to 8,756 in 2041, with an average annual growth rate of 2% per year. This is expected to increase the demand for carbon fiber from multiple applications in the aerospace industry.

- In Canada, the country has a Centre de developpement des composites du Quebec (Composite Development Centre of Quebec) (CDCQ) engaged in various activities related to the value chain of various composite materials, including carbon fibers. The center is also actively involved in the recycling of carbon fiber as one of its major activities.

- Globally, Canada ranks first in civil flight simulation, third in civil engine production, and fourth in civil aircraft production. It is the only nationally ranked in the top five of all the key categories. The Canadian aerospace industry exports over 70% of its products to over 190 countries across six continents.

- Wind energy in Canada accounts for 3.5% of electricity generation, being the region's second most important renewable energy source. Wind energy plays a crucial role in reaching global net-zero carbon emissions. Canada is one of the world leaders in producing and using renewable power due to its diversified geography with hydro, biomass, wind, and solar energy sources.

- Due to all such factors, the market for recycled carbon fiber in the region is expected to have steady growth during the forecast period.

Recycled Carbon Fiber Industry Overview

The recycled carbon fiber market is partially consolidated in nature. Some of the major players in the market include Toray Industries Inc., Procotex, Vartega Inc., Gen 2 Carbon Limited, and Sigmatex, among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand For Lightweight Vehicles

- 4.1.2 Growing Carbon Fiber Scrap Recycling and its Reuse in the Wind Energy Sector

- 4.1.3 Cost Effectiveness of Recycled Carbon Fiber

- 4.2 Restraints

- 4.2.1 Availability of Various Substitutes

- 4.2.2 Supply Chain Security for Recycled Carbon Fiber

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Revenue)

- 5.1 Type

- 5.1.1 Chopped Recycled Carbon Fiber

- 5.1.2 Milled Recycled Carbon Fiber

- 5.2 Source

- 5.2.1 Automotive Scrap

- 5.2.2 Aerospace Scrap

- 5.2.3 Other Sources

- 5.3 End-user Industry

- 5.3.1 Automotive

- 5.3.2 Aerospace and Defense

- 5.3.3 Wind Energy

- 5.3.4 Sporting Goods

- 5.3.5 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 Rest of the World

- 5.4.4.1 South America

- 5.4.4.2 Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Alpha Recyclage Composites

- 6.4.2 Carbon Conversions

- 6.4.3 Carbon Fiber Recycling

- 6.4.4 Carbon Fiber Remanufacturing

- 6.4.5 Gen 2 Carbon Limited

- 6.4.6 Karborek RCF

- 6.4.7 Mitsubishi Chemical Holdings Corporation.

- 6.4.8 Procotex

- 6.4.9 Shocker Composites LLC

- 6.4.10 Sigmatex

- 6.4.11 Toray Industries Inc.

- 6.4.12 Vartega Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Shifting Focus Toward Sustainability

- 7.2 Advancement in Research and Development for Recycling Techniques

- 7.3 Increasing Potential Demand from Additive Manufacturing and 3D Printing Sectors

02-2729-4219

+886-2-2729-4219

再生碳纤维市场分析及预测(至2035年):类型、产品、应用、技术、製程、终端用户、形式、材料类型、组件、解决方案

再生碳纤维市场分析及预测(至2035年):类型、产品、应用、技术、製程、终端用户、形式、材料类型、组件、解决方案 再生碳纤维市场规模、份额及成长分析(按产品、来源、回收方法、最终用途产业及地区划分)-2026-2033年产业预测

再生碳纤维市场规模、份额及成长分析(按产品、来源、回收方法、最终用途产业及地区划分)-2026-2033年产业预测 再生碳纤维市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

再生碳纤维市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 按应用、製程、纤维类型、最终用户和树脂相容性分類的再生碳纤维市场—全球预测,2025-2032年

按应用、製程、纤维类型、最终用户和树脂相容性分類的再生碳纤维市场—全球预测,2025-2032年 全球再生碳纤维市场按类型、原料、製造流程、最终用途产业和地区分類的预测(至 2030 年)

全球再生碳纤维市场按类型、原料、製造流程、最终用途产业和地区分類的预测(至 2030 年) 再生二氧化碳市场-全球产业规模、份额、趋势、机会和预测,按回收技术、来源、应用、地区和竞争细分,2020-2030 年

再生二氧化碳市场-全球产业规模、份额、趋势、机会和预测,按回收技术、来源、应用、地区和竞争细分,2020-2030 年 美国再生纤维市场规模、份额、趋势分析报告:按类型、最终用途和细分市场预测,2025-2030 年再生纤维市场规模、份额、趋势分析报告:按材料、最终用途、地区和细分市场预测,2025-2030 年再生碳纤维市场规模、份额、趋势分析报告(按来源、类型、最终用途、地区、细分市场预测),2025 年至 2030 年

美国再生纤维市场规模、份额、趋势分析报告:按类型、最终用途和细分市场预测,2025-2030 年再生纤维市场规模、份额、趋势分析报告:按材料、最终用途、地区和细分市场预测,2025-2030 年再生碳纤维市场规模、份额、趋势分析报告(按来源、类型、最终用途、地区、细分市场预测),2025 年至 2030 年 再生纤维的全球市场:市场规模·占有率·趋势,产业分析 (各材料·各最终用途·各地区),未来预测 (2025年~2034年)

再生纤维的全球市场:市场规模·占有率·趋势,产业分析 (各材料·各最终用途·各地区),未来预测 (2025年~2034年)

▼