|

市场调查报告书

商品编码

1408146

软体定义网路 (SDN):市场占有率分析、产业趋势与统计、2024-2029 年成长预测Software Defined Networking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

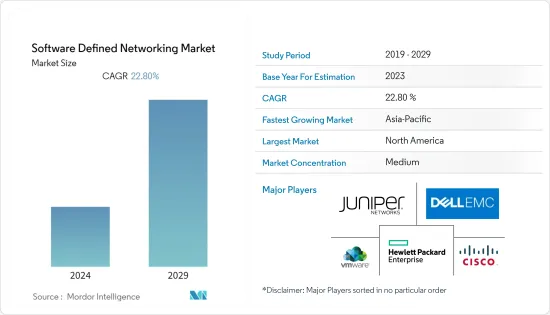

目前全球软体定义网路(SDN)市场规模为119.1亿美元,预计未来五年将达332.5亿美元,预测期内复合年增长率为22.8%。

透过资料以及区块链、物联网、认知和高级分析等网路技术不断进行的数位转型加强了各行业对连接进步的整体采用,这极大地推动了市场。我是。

主要亮点

- 全球软体定义网路(SDN)市场的开拓是由云端运算采用的快速成长、对软体定义网路(SDN)功能虚拟的投资不断增加(特别是为了最大限度地减少资本支出和营运费用以及各种移动服务)所推动的。受到需求成长等关键因素的推动; SDN 网路中云端运算解决方案的接受度迅速提高,将在提高先进资料中心的整体可操作性、安全性和网路可管理性方面发挥关键作用。

- 此外,各通讯服务供应商增加对5G基础设施的投资将有助于改善连接性并最大限度地部署SDN解决方案。此外,5G基础设施网路的发展预计将支持SDN市场的成长。根据 5G Americas 的数据,截至 2023 年,全球 5G 用户数约为 19 亿。预计到年终将增至约28亿,到2027年将增至约59亿,预计将成为市场的主要驱动力。

- 此外,企业的数位化趋势进一步推动了对强大网路服务的需求。随着许多公司寻求增强其整体网路能力,软体定义网路越来越受到关注。例如,2023 年 2 月,ETSI开放原始码组织 TeraFlowSDN 宣布推出第二版 TeraFlowSDN 控制器,这是一款强大且创新的 SDN 控制器和编排器。 TeraFlowSDN 第 2 版为各个网域上的端对端传输网路切片提供了启用和扩展的支援。

- 然而,经验丰富、技术熟练的网路工程师的短缺以及安全风险和攻击威胁的增加可能会限制整个预测期内的市场成长。

- 自 COVID-19 爆发以来,随着企业采用远距工作模式,对云端基础的解决方案的需求显着增加。随着远距工作模式的兴起,企业将最大限度地投资于云端基础的分析和保障、边缘运算和人工智慧驱动的网路技术,这有望推动所研究的市场。

软体定义网路 (SDN) 市场趋势

电信和云端基础服务供应商预计将实现强劲成长

- 软体定义网路因其资料流量受控、大规模网路易于管理等优点而广泛应用于IT和通讯业。通讯技术的进步、资料消耗的增加、智慧型手机的使用增加以及物联网/M2M 连接带来的互联网流量的增加正在推动软体定义网路 (SDN) 在通讯业的采用。

- 企业正在努力寻找有效运作IT基础设施以及高效管理和营运其网路的方法。特别是,企业正在对储存、运算和网路等商用硬体上的传统 IT 技术进行现代化改造,以采用云端技术,从而实现新网路服务的快速部署和开发。随着企业中云端基础的应用程式数量的增加,云端基础的服务变得越来越普及。

- 过去十年,云端处理总数有所增加,主要得益于中小企业投资的增加。由于组织中云端基础的应用程式数量不断增加,云端基础的服务越来越受到重视。在过去十年中,云端处理的总体使用量有所增加,这主要是由于中小型企业支出的增加。

- 此外,业内多家公司正在合作推出SDN解决方案。例如,2022年10月,5G无线基础设施供应商EdgeQ Inc.和开放无线接取网路全球通讯行动电话电信商沃达丰宣布,他们将共同建置下一代软体可程式5G ORAN系统.我们合作了。此次合作利用 ORAN 提供全球首款开放式可程式全内联 L1 加速卡,支援多载波、大规模 MIMO。为了支援 5G 宏蜂窝部署,此大规模整合架构将整个 4G/5G 实体层整合到单一卡片上。

- 此外,2022年3月,诺基亚宣布将与沃达丰独家合作,为沃达丰的多接入固定网路技术建置SDN-M&C(软体定义网路管理器和控制器)解决方案。根据这项合作关係,两家公司正在欧洲进行概念验证研究。

北美市场占有率最高

- 北美地区在促进软体定义网路服务市场的成长方面发挥着至关重要的作用。其主要原因是先进技术的接受与采用、网路自动化的发展、云端基础的服务数量的增加等诸多因素。在未来五年中,我们预计大多数 IT 团队将越来越多地采用 NaaS,因为供应商提供包括软体、云端智慧和本地硬体设备管理替代方案的混合服务。

- 此外,连网行动装置的显着增加推动了对增强网路服务的需求的整体成长。由于美国始终处于技术采用的前沿,该地区的连网型设备采用率最高,为市场带来了巨大的成长机会。

- 该地区的主要企业正在联合推出各种解决方案,以保持市场竞争力。例如,2022 年 6 月,全球领先的IT基础设施服务供应商之一 Kyndryl 与思科宣布建立合作伙伴关係,主要利用思科解决方案和 Kyndryl 託管服务,帮助企业客户加速向资料主导型业务转型。技术伙伴关係Kindril 和思科也宣布了新的私有云服务和网路、边缘运算解决方案、软体定义网路 (SDN) 解决方案以及在具有各种进阶安全功能的环境中提供的多网路广泛解决方案。・我们也将开发区域网路。

- 此外,全部区域的5G 部署和电信业者数量的增加在显着推动市场成长方面发挥着重要作用。此外,该地区各种重要 SDN 供应商的存在以及向 5G 网路的快速迁移正在对 SDN 市场的采用产生积极影响。此外,5G技术公司之间的合作在5G技术市场中变得越来越普遍。这主要是由于公司专注于透过汇集资源、专业知识、技术和成本来建立坚实的 5G 基础设施并支援创造性平台。

- 此外,2022年6月,美国半导体公司高通收购了Cellwize Wireless Technologies Pte. Ltd。此次收购旨在改善Qualcomm Technologies的5G网路基础设施,将为互联和智慧型边缘提供动力,加速跨产业的数位转型,并支持云端经济的崛起,市场成长将呈指数级扩张。

软体定义网路 (SDN) 产业概述

全球软体定义网路市场竞争温和,并由主要企业组成。从市场占有率来看,目前该市场由几家主要企业占据。然而,云端运算和区块链的大规模采用正在推动整个市场的需求。许多公司正在透过赢得新契约和开拓新市场来最大限度地扩大其市场占有率。

2023 年 4 月,美国铁塔公司子公司、领先的混合IT 解决方案供应商 Coresight 在其软体定义网路 (SDN) 平台 Open Cloud Exchange 中新增了新的扩充网路。・我们已宣布将推出此服务。这项新服务可自动执行Oracle云端基础架构内的额外设定功能,并在核心站点的完全託管虚拟路由器上实现云端到云端通讯功能。

2022 年 7 月,沃达丰升级了其软体定义网路 (SDN),整合了多个供应商元素并实现了其全球传输网路的现代化。该网路为四大洲 28 个国家的通讯业者协调所有行动、固定和语音流量,为数亿消费者以及独立网路业者和内容供应商提供服务。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- COVID-19 市场影响评估

- 产业生态系统分析

- 主要使用范例

- 技术分析

- 物联网和边缘运算

- 安全

- 云端运算

- 市场驱动因素

- 增加网路基础设施自动化投资

- 物联网和云端服务的采用率不断提高

- 市场挑战

- 缺乏技术纯熟劳工

- 安全风险和攻击威胁

- 邻近市场分析

- SD-WAN

- 市场估计/预测

- 成长机会与挑战

- 主要厂商发展情形

- 安全存取服务边际(SASE)

- 市场估计/预测

- 成长机会与挑战

- 主要厂商发展情形

- SD-WAN

第五章市场区隔

- 按组织规模

- 中小企业

- 大公司

- 按最终用户

- BFSI

- 卫生保健

- 零售

- 电信和云端服务供应商

- 製造业

- 教育机构

- 其他最终用户

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第六章竞争形势

- 公司简介

- Cisco Systems

- VMware

- Dell EMC

- HPE

- Juniper Networks

- Fortinet

- Huawei Technologies

- Barracuda Networks

- Versa Networks

- Arista Networks

第七章 市场机会及未来趋势

The Global Software Defined Networking Market is valued at USD 11.91 billion in the current year and is expected to register a CAGR of 22.8% during the forecast period to become USD 33.25 billion by the next five years. The rising digital transformation through data as well as networking technologies, such as blockchain, IoT, cognitive, and advanced analytics, strengthens the overall adoption of connectivity advances in various industries, which in turn is driving the market significantly.

Key Highlights

- The development of the global software-defined networking market is fuelled by key factors like a surge in the adoption of cloud computing, an increase in investments in software-defined networking function virtualization, especially to minimize the capital expenditure & operating expenses, and a rise in the need for various mobility services. The surge in the acceptance of cloud computing solutions in the SDN network plays a crucial role in improving the overall operability, security, and network manageability in advanced data centers.

- Moreover, the rising investments by various telecom service providers in 5G infrastructure would help to improve connectivity and maximize the deployment of SDN solutions. Also, the evolution of the 5G infrastructure network would help boost the SDN market's growth. According to 5G Americas, as of 2023, there are around 1.9 billion 5G subscriptions worldwide. It is anticipated to increase to about 2.8 billion by the end of the year 2024 and 5.9 billion by 2027, which in turn is expected to drive the market considerably.

- Also, the enterprise's propensity toward digitalization further propels the demand for robust network services. Many companies are looking to enhance their overall network capabilities, which is where Software Defined Network is gaining traction. For instance, in February 2023, ETSI Open Source Group TeraFlowSDN declared the 2nd launch of TeraFlowSDN controller, a robust and innovative SDN controller and orchestrator. TeraFlowSDN Release 2 delivers validated and extended support for slicing end-to-end transport networks over various domains.

- However, the lack of experienced and skilled network engineers and the rise in security risks and attack threats can restrict market growth throughout the forecast period.

- Since the outbreak of COVID-19, the demand for cloud-based solutions significantly grew owing to remote working models being adopted by enterprises. With the rising remote working model, companies maximized investments in cloud-based analytics and assurance, edge computing, and AI-powered networking technologies, which were expected to boost the studied market.

Software Defined Networking Market Trends

Telecom and Cloud-Based Service Provider is expected to witness a significant growth

- Software-defined networking is widely used in the IT and telecommunication industry due to advantages such as data traffic control and easily manageable large networks. The advancement of communication technologies, increased data consumption, the expansion of smartphone use, and the rise of internet traffic as a result of IoT/M2M connectivity together drive the adoption of software-defined networking in the telecommunications industry.

- Enterprises are striving to run their IT infrastructure efficiently and find ways to manage and operate their networks effectively. Enterprises are modernizing traditional IT techniques on commodity hardware, such as storage, computing, and networking, especially to incorporate cloud technologies that allow rapid deployment and development of new network services. With an increasing number of cloud-based applications across enterprises, cloud-based services are becoming significantly popular.

- Over the past decade, the total adoption of cloud computing has been rising mainly due to the increasing investments from small and medium enterprises. The cloud-based services are becoming prominent as the number of cloud-based apps in organizations grows. The overall usage of cloud computing has increased over the last decade, which is primarily due to the increased expenditures from small and medium-sized businesses.

- Moreover, various companies in the industry are parting to launch SDN solutions. For instance, in October 2022, EdgeQ Inc., a provider of 5G wireless infrastructure, and Vodafone, a global telecoms mobile operator in Open Radio Access Networks, collaborated to create the next-generation, software-programmable 5G ORAN systems. The partnership would utilize ORAN to provide the world's first open programmable, completely in-line L1 accelerator card to support multi-carrier, massive MIMO. To handle the 5G macro cell deployments, this massively integrated architecture converges the whole 4G/5G Physical layer into a single card.

- Additionally, In March 2022, Nokia declared that it was chosen exclusively to collaborate with Vodafone on creating software-defined network manager and controller (SDN-M&C) solutions for the multi-access fixed network technology of the company. Both companies are performing proof-of-concept studies in Europe under the terms of the partnership.

North America to Hold the Highest Market Share

- The North American region plays a very crucial role in terms of enhancing the growth of the software-defined network service market. It is mainly because of factors like the Inclining toward acceptance and implementation of advanced technology, development in network automation, the rise in the number of cloud-based services, and many others. Over the next five years, most IT teams are expected to increasingly adopt NaaS as suppliers provide hybrid offerings that involve software, cloud intelligence, and the alternative for the management of on-premises hardware devices.

- Moreover, substantial growth in connected and mobile devices is spiking the rise in the overall demand for enhanced network services. Since the United States has always stayed at the forefront of technology adoption, the region has witnessed the maximum adoption of connected devices, driving the market's growth opportunities significantly.

- Major companies in the region are collaborating and launching various solutions to remain competitive in the market. For instance, in June 2022, Kyndryl, the world's significant IT infrastructure services provider, and Cisco declared a technology partnership to help and assist enterprise customers boost their transformation into data-driven businesses mainly powered by Cisco solutions and Kyndryl managed services. Kyndryl and Cisco would also develop new private cloud services and networks, as well as edge computing solutions, software-defined networking solutions, and multi-network wide area network offerings delivered in an environment with various advanced security capabilities.

- Moreover, the increase in 5G rollouts and telecom companies across the region is playing a significant role in terms of driving market growth significantly. Also, the presence of various crucial SDN providers and the quick shift to 5G networks in this region positively impact the SDN market adoption. Further, the surge in the collaborations between 5G tech firms is becoming more common in the market for 5G technologies. This is mainly due to the firm's focus on building a solid 5G infrastructure and supporting creative platforms by pooling their resources, expertise, technology, and costs.

- Further, in June 2022, Qualcomm, a semiconductor firm located in the United States, acquired Cellwize Wireless Technologies Pte. Ltd. This acquisition is intended to improve Qualcomm Technologies' 5G network infrastructure, which would power the connected, intelligent edge, fuel the digital transformation of the sectors, and assist the rise of the cloud economy which in turn will augment the market growth drastically.

Software Defined Networking Industry Overview

The Global Software Defined Networking market is moderately competitive and comprises major players. In terms of market share, few key market players currently dominate the market. However, the massive adoption of cloud computing and blockchain is increasing the market's overall demand. Many companies are maximizing their market presence by securing new contracts and tapping new markets.

In April 2023, CoreSite, a significant hybrid IT solutions provider and subsidiary of American Tower Corporation, declared the introduction of new enhanced network services to its software-defined networking platform, the Open Cloud Exchange. The new services would automate the additional provisioning functionality within the Oracle Cloud Infrastructure and direct its cloud-to-cloud communication capabilities on CoreSite's fully managed virtual routers.

In July 2022, Vodafone upgraded its software-defined networking (SDN) to integrate several supplier elements and modernize its worldwide transport network. Hundreds of millions of consumers, as well as independent internet and content providers, were served by this network, which coordinated all of the telco's mobile, fixed, and voice traffic across 28 nations on four continents.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness-Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of COVID-19 Impact on the market

- 4.4 Industry Ecosystem Analysis

- 4.5 Key Usecases

- 4.6 Technology Analysis

- 4.6.1 IoT and Edge Computing

- 4.6.2 Security

- 4.6.3 Cloud Computing

- 4.7 Market Drivers

- 4.7.1 Rising investment toward automation of network infrastructure

- 4.7.2 Increasing adoption of IoT and cloud services

- 4.8 Market Challenges

- 4.8.1 Lack of skilled workforce

- 4.8.2 Security risks and attack threats

- 4.9 Adjacent Market Analysis

- 4.9.1 SD-WAN

- 4.9.1.1 Market estimation and forecast

- 4.9.1.2 Growth opportunities and challenges

- 4.9.1.3 Key vendor developments

- 4.9.2 Secure Access Service Edge (SASE)

- 4.9.2.1 Market estimation and forecast

- 4.9.2.2 Growth opportunities and challenges

- 4.9.2.3 Key vendor developments

- 4.9.1 SD-WAN

5 MARKET SEGMENTATION

- 5.1 By Organization size

- 5.1.1 SMEs

- 5.1.2 Large Enterprises

- 5.2 By End User

- 5.2.1 BFSI

- 5.2.2 Healthcare

- 5.2.3 Retail

- 5.2.4 Telecom and Cloud Service Providers

- 5.2.5 Manufacturing

- 5.2.6 Education

- 5.2.7 Other End Users

- 5.3 By Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Latin America

- 5.3.5 Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Cisco Systems

- 6.1.2 VMware

- 6.1.3 Dell EMC

- 6.1.4 HPE

- 6.1.5 Juniper Networks

- 6.1.6 Fortinet

- 6.1.7 Huawei Technologies

- 6.1.8 Barracuda Networks

- 6.1.9 Versa Networks

- 6.1.10 Arista Networks