|

市场调查报告书

商品编码

1408172

卫星物联网通讯:市场占有率分析、产业趋势与统计、2024-2029 年成长预测Satellite IoT Communication - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

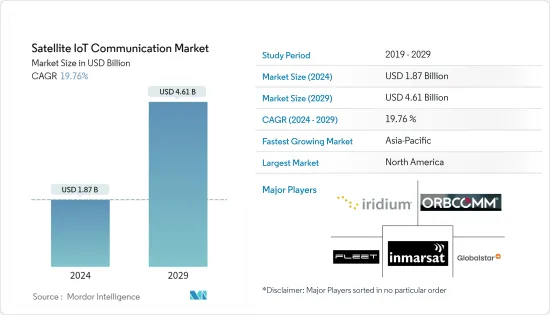

卫星物联网通讯市场规模预计到 2024 年为 18.7 亿美元,预计到 2029 年将达到 46.1 亿美元,在预测期内(2024-2029 年)复合年增长率为 19.76%。

卫星通讯补充了偏远地区的地面蜂巢式网路和非蜂巢式网路,并有利于各种工业应用。 5G生态系统将是卫星和地面网路无缝整合的关键趋势。

主要亮点

- 卫星通讯的动力源自于物联网(IoT)设备全球连结的迫切需求。该领域的几家公司正在投资扩大卫星通讯的应用,特别是推出 SmallSat卫星群。多家公司正在使用卫星物联网服务来监控和追踪设备以实现智慧型资料传输。

- 全球卫星物联网通讯市场是由5G无线连接的发展和成长所推动的。由于透过LEO卫星扩大5G连线的力度活性化,例如SAT 5G(欧盟支援的5GPPP计划)和城域乙太网路论坛(MEF),需要更多的互动。建构安全、异质的卫星和地面5G网路也将帮助通讯业者和LEO卫星供应商更好地整合服务。

- LEO卫星市场的大规模投资是推动卫星物联网通讯市场成长的关键方面。这项投资受到适应性、廉价成本、先进机械、易于组装和发射、大量生产和短生命週期的推动,这些可能会推动未来几年的市场成长。

- 此外,工业领域采用自主系统和连网型设备的成长趋势也对市场研究产生了正面影响。据爱立信称,到年终,预计近60%的蜂巢式物联网连接将是宽频物联网,其中4G占大多数。这可能会在整个预测期内为市场的成长和增强创造充足的机会。

- 外太空的极端气温是限制市场的重要因素。卫星暴露在恶劣的太空环境中,其内部的电子元件受到极端温度的威胁。因此,卫星必须保持工作温度,以避免系统故障且不影响通讯。

- COVID-19 大流行震惊了世界各地的每个行业。它也对卫星物联网通讯领域产生了重大影响。该行业在多个领域依赖政府合同,例如卫星通讯服务的高可靠性和耐用性,这对于灾难通讯和备份服务至关重要,这使得它们更容易受到全球流行病严重程度的影响。 。然而,大流行之后,地面连接服务的使用增加,为卫星物联网通讯留下了巨大的机会。

卫星物联网通讯市场趋势

低地球轨道 (LEO) 推动卫星物联网通讯的成长

- 围绕地球上方 160 至 2000 公里运行的低地球轨道 (LEO)卫星星系对于将 5G 连接扩展到没有地面覆盖的偏远、服务欠缺和偏远地区具有潜在的吸引力。它是一个目标。由于地球表面只有约 10% 的区域提供地面连接服务,因此使用 LEO 卫星进行卫星物联网通讯仍然存在巨大的机会。

- LEO卫星因其适应性强、价格实惠、机械先进以及易于组装和发射而吸引了各大公司的大量投资。卫星的生命週期短,且生产量大。政府机构和零售、银行、石油和天然气等商业部门对低成本、高速网路的需求很高。此外,新兴国家的个人消费者对农村地区网路存取的需求正在推动对低地球轨道卫星群的投资。

- LEO适合低功耗通讯,讯号传播损耗低,降低了用户设备的功耗要求,非常适合接触低功耗物联网设备。目前,大多数用于物联网的LEO卫星主要利用CubeSat技术建造,该技术允许公司批量生产组件并提供现成的组件,从而可以显着减少设计和开发卫星所需的成本和时间。这已成为老牌卫星通讯业者和推出卫星物联网通讯服务的新兴企业的首选。

- 此外,重要的公司也在投资、与其他企业合併以及投资新计画,以扩大消费群并更好地满足各种应用的需求。例如,2023年4月,第一家营运5G-IoT标准低地球轨道(LEO)卫星星系的公司Sateliot发射了有史以来第一颗5G标准LEO卫星Sateliot_0「The GroundBreaker」。

- 2023 年 2 月,美国Rivada Networks, Inc.的完全子公司Rivada Space Networks GmbH (RSN) 宣布,Rivada 的创新型「我们已委託为 Sky Network 生产 300 颗低地球轨道 (LEO) 卫星。 RSN 的天基资料网路提供类似光纤的低延迟和每秒Gigabit的资料传输,并且具有超安全性和高弹性。

预计北美将占据最大份额

- 北美在卫星物联网通讯市场中占有很大份额。这一增长是由于政府在军事和通讯网路方面的支出增加。霍尼韦尔国际公司、通用动力公司和 L3Harris 技术公司等主要参与企业的存在极大地推动了该地区的市场成长。

- 5G网路将在帮助政策制定者和政府将城市转变为智慧城市、使居民获得社会经济效益、参与先进的数位化和资料密集型经济方面发挥关键作用,我将实现这一目标。因此,当局将需要建置和升级光纤网路和资料中心等被动资产,以满足卫星物联网通讯市场的需求。

- 此外,政府、农业、采矿、能源、海事和航空等最终用户行业不断增长的需求正在加强该地区的市场成长。此外,该地区还改善了网路连接并拥有强大的技术基础设施立足点。例如,2022 年 8 月,Inmarsat 和 hiSky 建立了一个新的可扩展物联网解决方案,为物联网采用者提供经济高效的服务,同时增强连接性。

- 2023年6月,高通技术公司宣布推出两款具有卫星通讯功能的调变解调器晶片组(高通9205S调变解调器和高通212S调变解调器)。高通的新型调变解调器晶片组将主要支援需要独立非地面网路(NTN)连接或与地面网路混合连接的离网工业用例,并将由物联网开发商、企业、 OEM使用,并且使ODM能够利用关键技术即时资讯和见解,特别适合管理各种业务计划。

- 此外,铱星通讯公司也宣布于2022年12月推出铱星资讯传输SM(Iridium Messaging TransportSM)服务。它是一种双向云端原生网路资料,主要针对 Iridium Certus 上的使用进行了最佳化,旨在轻鬆地将卫星连接整合到现有或新的物联网解决方案中。 IMT 提供铱星网路独特的 IP资料传输服务,专为中小型讯息而构建,以支援卫星物联网应用。这项新服务与 Iridium CloudConnect 和 Amazon Web Services 集成,可最大限度地降低各种新型 Iridium Connected IoT 设备的开发成本并缩短上市时间。

卫星物联网通讯业概况

卫星物联网通讯市场竞争激烈,由几家主要参与者组成,包括 Astrocast、Inmarsat Technologies、Kepler Communications、Ligado Networks、Galaxy Space 和吉利。目前,只有少数大公司在市场占有率方面占据主导地位。这些拥有重要市场占有率的领先公司致力于扩大海外基本客群。这些公司利用策略合作计划来增加市场占有率和盈利。主要进展包括:

2023年3月,全球物联网解决方案供应商移远无线推出了物联网产业的CC200A-LB卫星模组,采用全球物联网通讯与解决方案供应商ORBCOMM提供的卫星物联网连线。该模组主要旨在以经济高效的价格分布和超低延迟提供可靠的全球连接和覆盖。该模组是运输、海事、重型设备、采矿、农业以及石油和天然气监测等广泛应用的理想解决方案。

全球卫星和地面网路解决方案供应商 Marlink 与低地球轨道(LEO) 5G 物联网卫星电信业者OQ Technology 就相容现有蜂巢式网路、3GPP 5G 非地面网路蜂窝签署了标准全球销售合作伙伴关係谅解备忘录基于卫星的5G连线和硬体销售。

T-Mobile US 和 Starlink 宣布建立技术合作伙伴关係,开发卫星到设备的直接连接。同样,美国的 Omnispace 正在与菲律宾行动电话Smart(PLDT 的子公司)合作,利用符合 3GPP 的 5G NTN 标准探索 Smart 的 5G 网路与 Omnispace 的 LEO 卫星之间的互通性。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 市场驱动因素

- 5G 无线连线的发展与成长

- LEO卫星星系的重大投资

- 市场挑战

- 极端的宇宙温度

- 产业吸引力模型—波特五力分析

- 消费者议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 产业价值链分析

- COVID-19 对文件管理市场的影响

第五章市场区隔

- 按轨道类型

- 低地球轨道(LEO)

- 中轨道(MEO)

- 地球静止轨道(GEO)

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 其他的

第六章 竞争形势

- 公司简介

- Iridium Communications Inc.

- Orbcomm

- Inmarsat Global Limited

- Globalstar Inc

- Fleet Space Technologies Private Limited

- Viasat, Inc

- Cobham Limited

- Boeing

- L3Harris Technologies

第七章 投资分析

第八章 市场机会及未来趋势

The Satellite IoT Communication Market size is estimated at USD 1.87 billion in 2024, and is expected to reach USD 4.61 billion by 2029, growing at a CAGR of 19.76% during the forecast period (2024-2029).

Satellite communication complements terrestrial cellular and non-cellular networks in remote locations, which benefits various industrial applications. 5G ecosystems would be a key trend in seamlessly integrating satellite and terrestrial networks.

Key Highlights

- The drive for satellite communications stems from the pressing need for global connectivity for the Internet of Things (IoT) devices. Several businesses in this sector are investing in broadening the applications for satellite communication, most notably with the introduction of SmallSat constellations. Several businesses use satellite IoT services to monitor and track equipment for intelligent data transfers.

- The Global satellite Internet of Things communication market is driven by the development and growth of 5G wireless connectivity. The demand for more interaction between open and standardized ecosystems on both sides is emerging as a result of the growing number of efforts to expand 5G connection via LEO satellites, such as SAT 5G (a 5GPPP project supported by the European Union) and Metro Ethernet Forum (MEF). Building a safe, heterogeneous satellite and terrestrial 5G network would also aid telecom operators and LEO satellite providers better integrate their services.

- Considerable Investments in the LEO Satellite Market are a significant aspect boosting the growth of the satellite IoT Communication Market. The investments have been fueled by adaptability, cheap cost, advanced mechanics, simplicity of assembly and launch, mass production, and short life cycles, which would drive market growth in the coming years.

- Moreover, the growing trend of adopting autonomous systems and connected devices in the industrial sectors positively influences the market studied. According to Ericsson, by the end of 2028, almost 60 percent of cellular IoT connections are forecast to be broadband IoT, with 4G connecting the majority. This would create ample opportunities for the market to grow and enhance throughout the forecast period.

- Extreme Space temperature is a critical factor that could restrain the market. Satellites are exposed to the harsh environment of space, which makes the electronic components housed inside the satellites threatened by extreme temperatures. Hence satellites must maintain operational temperatures to avoid system failures so that communication is not affected.

- The COVID-19 pandemic caused shockwaves across every industry worldwide. It had a significant effect on the satellite IoT communication sector. The sector may be protected from the more severe effects of the global pandemic due to its reliance on government contracts in several areas, including the highly dependable and durable nature of satellite communications services, which are essential for disaster communications and backup services. However, there has been an increasing rise in access to terrestrial connectivity services after the pandemic, which left a significant opportunity for satellite IoT communications.

Satellite IoT Communication Market Trends

Low Earth Orbit (LEO) drives the Growth of the Satellite IoT Communication

- Low-Earth Orbit (LEO) satellite constellations, which orbit between 160 and 2000 kilometers above the Earth, are potentially attractive for expanding 5G connectivity to isolated, underserved, and remote geographies where terrestrial coverage is absent. Only about 10 % of the Earth's surface has access to terrestrial connectivity services, which leaves a significant opportunity for satellite IoT communications on the LEO constellations.

- LEO satellites attract significant investment from major players due to their adaptability, affordability, advanced mechanics, and ease of assembly and launch. The satellites have a short lifecycle and are mass-produced. There is a significant demand for low-cost, high-speed internet in the government and commercial sectors like retail, banking, oil, and gas. Also, the need for internet access in rural areas among individual consumers in emerging countries is driving investments in LEO constellations.

- LEO are better suited to low-power communications and lower signal propagation losses, reducing the user equipment's power requirements and making it ideal for contact with low-power IoT devices. Today, most of the LEO satellites for IoT are built mainly for leveraging CubeSat technology, allowing companies to mass-produce components and provide commercial off-the-shelf parts, drastically reducing the cost and time to design and develop satellites. It has become the desired option for incumbent satellite operators and NewSpace start-ups launching satellite IoT communication services.

- Moreover, to increase their consumer base and better meet their demands across various applications, significant companies are also investing, merging with other businesses, and investing in new projects. For instance, in April 2023, Sateliot, the first company to operate a low-Earth orbit (LEO) nanosatellite constellation with 5G-IoT standard, introduced Sateliot_0 "The GroundBreaker," the first-ever 5G standard LEO satellite, to democratize access to the Internet of Things.

- In February 2023, Rivada Space Networks GmbH (RSN), an entirely owned subsidiary of U.S.-based Rivada Networks, Inc., engaged Terran Orbital's wholly owned subsidiary Tyvak Nanosatellite Systems, Inc. to manufacture 300 low-earth-orbit (LEO) satellites for Rivada's innovative "network in the sky." RSN's space-based data network will provide fiber-like low latency and gigabit-per-second data delivery which is ultra-secure and extremely resilient.

North America is Expected to Hold Largest Share

- North America holds a significant share of the Satellite IoT Communication market. The growth is attributed to the growing government spending on military and communication networks. The presence of key significant players, such as Honeywell International, Inc., General Dynamics Corporation, L3Harris Technologies Corporation, and many others, drive the market growth significantly across the region.

- 5G networks play a vital role in assisting policymakers and governments in transforming cities into smart cities, allowing inhabitants to participate and realize socioeconomic benefits from an advanced, digital, data-intensive economy. As a result, authorities would be required to build and upgrade passive assets, such as fiber networks and data centers, which strive to meet the demand for the satellite IoT Communication Market.

- Moreover, the rise in the demand from end-user industries, such as government, agriculture, mining, energy, maritime, and aviation, is enhancing the market growth in the region. Moreover, the region has improved network connectivity and advanced foothold technological infrastructure. For instance, In August 2022, Inmarsat and hiSky created a new scalable IoT solution to provide a cost-efficient offering to IoT adopters while improving connectivity.

- In June 2023, Qualcomm Technologies, Inc. declared two modem chipsets with satellite capability: the Qualcomm 9205S Modem and the Qualcomm 212S Modem. The new Qualcomm modem chipsets primarily power off-grid industrial use cases that need a standalone non-terrestrial network (NTN) connectivity or hybrid connectivity alongside terrestrial networks and enable IoT developers, enterprises, OEMs, and ODMs to harness the key real-time information and insights especially to manage various business projects.

- Also, in December 2022, Iridium Communications Inc. declared the service launch of Iridium Messaging TransportSM, a two-way cloud-native networked data service primarily optimized for use over Iridium Certus and built to make it easier to combine satellite connections to the existing or new IoT solutions. IMT delivers an IP data transport service unique to the Iridium network, built for small-to-moderate messages assisting satellite IoT applications. Integrated with Iridium CloudConnect and Amazon Web Services, the new service can minimize the development costs and the speed time to market for various new Iridium Connected® IoT devices.

Satellite IoT Communication Industry Overview

The satellite IoT communication market is highly competitive and consists of several major players, such as Astrocast, Inmarsat Technologies, Kepler Communications, Ligado Networks, Galaxy Space, and Geely. Only some significant players currently dominate the market in terms of market share. With a prominent market share, these major players focus on expanding their customer base across foreign countries. These companies leverage strategic collaborative initiatives to increase their market share and profitability. Some of the key developments are:-

In March 2023, Quectel Wireless Solutions, a worldwide IoT solutions provider, launched the CC200A-LB satellite module for IoT industries that uses satellite IoT connectivity offered by ORBCOMM, a worldwide provider of IoT communications and solutions. The module is mainly built to deliver reliable global connectivity and coverage at a cost-effective price point and with ultra-low latency. It is a perfect solution for a vast spectrum of applications, including transportation, maritime, heavy equipment, mining, agriculture, and oil and gas monitoring.

Marlink, a global satellite and terrestrial network solution provider, and OQ Technology, the low Earth orbit (LEO) 5G IoT satellite communications company, signed an MoU for a global distribution partnership towards the distribution of Satellite 5G connectivity and hardware that is compatible with an existing cellular network and based on the 3gpp 5g non-terrestrial network cellular standard.

T-Mobile US and Starlink announced a technology partnership to develop a direct satellite-to-device proposition, which was expected to launch by 2024. Similarly, US-based Omnispace collaborated with the Philippines' mobile operator Smart, a subsidiary of PLDT, to explore interoperability between Smart's 5G network and Omnispace's LEO satellites, using 3GPP-compliant 5G NTN standards.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Development and Growth of 5G Wireless Connectivity

- 4.2.2 Considerable Investments in the LEO Satellite Constellations

- 4.3 Market Challenges

- 4.3.1 Extreme Space Temperature

- 4.4 Industry Attractiveness Model - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Industry Value Chain Analysis

- 4.6 Impact of COVID-19 on the Document Management Market

5 MARKET SEGMENTATION

- 5.1 By Type of Orbit

- 5.1.1 Low Earth Orbit (LEO)

- 5.1.2 Medium Earth Orbit (MEO)

- 5.1.3 Geostationary Orbit (GEO)

- 5.2 By Geography

- 5.2.1 North America

- 5.2.2 Europe

- 5.2.3 Asia-Pacific

- 5.2.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Iridium Communications Inc.

- 6.1.2 Orbcomm

- 6.1.3 Inmarsat Global Limited

- 6.1.4 Globalstar Inc

- 6.1.5 Fleet Space Technologies Private Limited

- 6.1.6 Viasat, Inc

- 6.1.7 Cobham Limited

- 6.1.8 Boeing

- 6.1.9 L3Harris Technologies

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

卫星基频晶片市场(按技术、卫星类型、频宽、功能、资料速率和应用)—2025-2030 年全球预测

卫星基频晶片市场(按技术、卫星类型、频宽、功能、资料速率和应用)—2025-2030 年全球预测 全球5G卫星市场全球国防卫星通讯市场全球天空通讯市场

全球5G卫星市场全球国防卫星通讯市场全球天空通讯市场 卫星通讯:D2C (Direct-to-Cellular) 及NTN的发展与契约卫星通讯:D2C (Direct-to-Cellular) 及NTN的发展与契约:市场资料概要 (2025年第3季)全球天基网路市场基于半导体的卫星通讯系统市场分析及预测(至2034年):类型、产品、服务、技术、组件、应用、最终用户、部署、功能和安装类型

卫星通讯:D2C (Direct-to-Cellular) 及NTN的发展与契约卫星通讯:D2C (Direct-to-Cellular) 及NTN的发展与契约:市场资料概要 (2025年第3季)全球天基网路市场基于半导体的卫星通讯系统市场分析及预测(至2034年):类型、产品、服务、技术、组件、应用、最终用户、部署、功能和安装类型 全球 5G 卫星市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测卫星通讯:宽频部署与订阅市场数据概览(2025 年第三季)

全球 5G 卫星市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测卫星通讯:宽频部署与订阅市场数据概览(2025 年第三季)