|

市场调查报告书

商品编码

1408219

Wi-Fi路由器:市场占有率分析、产业趋势/统计、2024年至2029年成长预测Wi-Fi Router - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

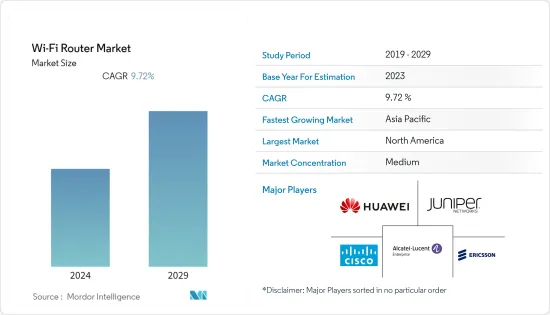

全球Wi-Fi路由器市场规模目前为125亿美元,预计五年内将达198.8亿美元,预测期内复合年增长率为9.72%。

越来越多的客户参与网页浏览、行动学习和其他线上相关活动,增加了对更快网路存取的需求。因此,经常用于笔记型电脑、个人电脑和平板电脑的无线路由器已成为人类生存的必需品。无线路由器正在为满足消费者对可靠网路连线不断增长的需求以及加强许多国家的网路连线做出重大贡献。

主要亮点

- 越来越多的客户参与电子商务交易、网页浏览、行动学习和其他线上相关活动,增加了对更快网路存取的需求。因此,经常用于笔记型电脑、个人电脑和平板电脑的无线路由器已成为人类生存的必需品。 Wi-Fi 路由器正在为许多国家/地区消费者对可靠网路连线不断增长的需求以及加强 Wi-Fi 连线做出重大贡献。医疗保健、教育、商业、金融服务和其他应用中互联设备的使用不断增加是全球无线路由器市场的关键驱动因素之一。此外,中小企业采用自备设备政策也对市场成长产生正面影响。此外,预计在预测期内,政府对智慧城市计划的措施将会增加,为市场扩张创造有利的机会。

- 此外,通讯(ITU) 预测,到 2022 年,将有 53 亿人(即世界人口的 66%)使用网路。这比 2019 年成长了 24%,预计届时将有 11 亿人加入网路。随着网路的日益普及,国内外无线路由器厂商将有机会推出新产品、提高频宽并占领重要的市场占有率。

- 此外,思科的年度网际网路报告预测,到 2023 年,连网装置和连线的数量将接近 300 亿,高于 2018 年的 184 亿。到 2023 年,物联网设备将占所有连网装置的 50%(147 亿),高于 2018 年的 33%(61 亿)。此外,根据思科的数据,固定网际网路 IP 流量已从 2016 年的 65,942 台装置增加到 2021 年的 1,87,386 台装置。网路流量的增加可能会推动受访市场的发展。此外,根据Statistics Counter的数据,2022年1月,行动流量占加拿大所有网站流量的38.04%以上,低于2020年的40.95%。桌上型电脑和笔记型电脑继续主导加拿大的网路使用。连网设备的增加可能会促进研究市场的成长。

- 同时,根据诺基亚 2022 年年度行动宽频指数 (MBiT) 报告,资料流量增加了 31%,每位用户每月平均行动资料使用量达到 17GB。印度快速扩张的4G和5G网路几乎承载了所有行动宽频流量。报告称,2021年将有超过4000万新增或升级的4G用户使用该服务。随着数位化的不断适应,这一数字预计将进一步增加。大都会地区的交通量明显高于以前。近年来,第四代长期演进(4G/LTE)行动宽频网路极大促进了辖区和部门之间的通讯互通性。

- 新冠疫情爆发后,在家工作已成为一大趋势。大规模远端工作的转变速度导致了行动电话、笔记型电脑和桌上型电脑等个人设备的使用。我们也看到员工使用个人或无线 Wi-Fi 路由器和网路连线来存取公司网路。欧盟统计局的数据显示,欧洲能够在家工作的员工比例显着增加,法国达29.4%,德国达到22.8%,西班牙为15.1%,义大利为13.6%。

Wi-Fi路由器市场趋势

零售和电子商务预计将占据主要市场份额

- 电子商务(电子商务)是透过互联网购买和销售产品和服务。它包括为线上买家和卖家提供的各种资料、系统和工具,包括行动购物和线上付款加密。大多数拥有线上业务的企业都使用线上商店和平台进行电子商务行销和销售活动,并监督物流和履约。这些电子商务趋势可能会推动对 Wi-Fi 路由器的需求,使消费者能够访问任何网路购物网站。

- 越来越多的客户参与电子商务交易、网页浏览、行动学习和其他线上相关活动,增加了对更快网路存取的需求。因此,经常用于笔记型电脑、个人电脑和平板电脑设备的无线 LAN 路由器已成为人类生存的必需品。 Wi-Fi 路由器正在为满足消费者对可靠网路连线不断增长的需求以及加强许多国家的 Wi-Fi 连线做出重大贡献。

- 根据 GSMA(特种行动协会)情报资料,2022 年初,新加坡拥有 870 万活跃行动连线。此外,截至 2022 年 1 月,新加坡的行动连线人口占总人口的 147%。该地区的互联网普及可能会推动电子商务市场的发展。此外,根据新加坡统计局的数据,到2022年,电脑和通讯设备的线上销售将占总销售额的47.4%。相较之下,30%的家具和家电都是在网路上购买的。该地区线上购买量的增加将为新玩家进入市场以及国际玩家扩大在新加坡的业务创造重要机会。

- 根据通讯(MoTC) 的数据,卡达以 264 美元的平均交易额领先中东国家。此外,去年全国有350家电子商务公司在经营,未来六个月还将新增66家电子商务公司,到去年12月底达到416家。此外,卡达的电子商务普及为62.1%。此外,从网路购物来看,卡达人最受欢迎(22%),其次是欧美人(17%)、阿拉伯人(19%)、亚洲人(20%)和其他人(22%)。 )。) 。卡达是中东和北非 (MENA) 地区(与海湾合作委员会相比)中每用户平均年度电子商务支出最高的国家,每笔线上交易的平均支出高于海湾合作委员会的平均水平。

- Kibo Commerce 的数据显示,2022 年第二季度,美国电商网站的访问中有 2.3% 产生了购买行为。在英国,线上购物者的转换率已增至 4% 以上。行动商务在页面浏览量和收益方面正在迎头赶上,但透过 PC 进行的传统网路购物仍然处于领先地位。线上用户转换率的提高对学生市场产生了积极影响。

预计北美将占据很大的市场份额

- 美国是技术发展、商业数位化和互联网使用方面领先的国家之一。高速网路的需求已成为满足国家数位转型之旅的必要条件。根据Cisco的预测,北美地区的平均 Wi-Fi 网路连线速度将从 2020 年的 70.7 Mbps 增加到 2023 年的 109.5 Mbps。如此巨大的网路速度可能会促使玩家开发支援这种网路速度的新 Wi-Fi 路由器。

- 美国政府正在与美国私营部门合作支持泰国4.0。 2022 年,美国、泰国皇家政府和企业高管举办了研讨会,共用有关 6GHz 频率分配和下一代 Wi-Fi 技术重要性的知识。研讨会不仅将加速家庭Wi-Fi的速度,也将进一步巩固泰国作为先进製造和工业创新中心的地位。两国之间的这些合作关係可能会推动美国Wi-Fi 製造商市场的发展。

- 该地区的公司正在以经济的价格推出最新产品,以增加市场占有率。例如,美国路由器製造商Linksys计划于2022年5月推出Hydra 6和Atlas 6等双频Wi-Fi 6路由器。这些路由器专为速度和效能而设计,价格合理,预计将为混合工作、线上游戏、4K 超高清串流媒体等提供可靠的连接。

- 加拿大经济发达,人们有能力购买有用的智慧型设备。据思科称,人均设备和连接数量将从2016年的6.3个增加到2021年的10.7个。另外,到2023年,加拿大将有3,530万网路用户,网路用户的增加将对Wi-Fi路由器产生正面影响,因此该国Wi-Fi路由器将有巨大的成长潜力。那

- 该国对低延迟、高速网路服务的需求不断增长,许多全球参与者正在该国推出先进的 Wi-Fi 路由器和网状 Wi-Fi 路由器。例如,2022 年 10 月,Google在加拿大推出了具有 Wi-Fi 6E 的 Nest Wi-Fi Pro,这是其首款能够在三频网状网路上运行的路由器。在相容设备上,Wi-Fi 6E(E 表示扩展)使用新的、不太拥挤的 6GHz 无线电频宽,可提供高达 Wi-Fi 6 两倍的速度。

Wi-Fi路由器产业概况

Wi-Fi 路由器市场由多家公司适度整合,包括Cisco、爱立信公司、华为科技公司、Juniper Networks和阿尔卡特朗讯企业公司。公司持续投资于策略合作伙伴关係和产品开拓,以大幅提高市场占有率。

2023 年 3 月,NETGEAR 发布了 Nighthawk RS700,这是首款支援 Wi-Fi 7 的路由器。 NETGEAR 表示,该三频单元专为低延迟 AR(扩增实境)/VR(虚拟实境)游戏、UHD Zoom 通话、8K 同步串流等而设计。 RS700 具有新的塔状形状,不会让人想起以前的 Nighthawk 夜鹰路由器,并设计有内建天线,可实现 360 度覆盖范围达 3,500 平方英尺。

2022 年 11 月,全球消费者和企业网路产品供应商 TP-Link 宣布推出整个适用于家庭和企业用途的 Wi-Fi 7 产品线。 TP-Link针对ISP市场推出新款Wi-Fi 7路由器、Omada EAP、Deco产品、Aginet产品,涵盖所有使用情境。 TP-Link的全新HomeShield 3.0也提供了更可靠、更智慧的网路解决方案。 Wi-Fi 7 路由器仍然是表现最佳的 Archer 系列之一,为您的家庭带来前所未有的体验。在本次活动中,发布了三款 Wi-Fi 7 路由器。其中,Archer BE900拥有四频24Gbps Wi-Fi 7速度以及相比传统路由器的全新设计。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 生态系分析

- 产业吸引力-波特五力分析

- 买方议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- COVID-19 市场影响评估

- 使用案例

第五章市场动态

- 市场驱动因素

- 网路流量增加以及消费者对网路设备的需求增加

- 数位化导致企业频宽需求快速成长

- 市场抑制因素

- 网路安全和网路管理的复杂性

- 行动宽频使用情况

第六章市场区隔

- 按类型

- 边缘路由器

- 核心路由器

- 按组织规模

- 中小企业

- 大公司

- 按最终用户产业

- 卫生保健

- 运输/物流

- 零售/电子商务

- 製造业

- 政府机关

- BFSI

- 其他的

- 按地区

- 北美洲

- 欧洲

- APAC

- 中东/非洲

- 拉丁美洲

第七章 竞争形势

- 公司简介

- Cisco Systems Inc

- Ericsson Inc.

- Huawei Technologies Co.ltd

- Juniper Networks Inc.

- Alcatel Lucent Enterprise SAS

- ARUBA SPA

- Fortinet Inc.

- Panasonic Corporation

- Broadcom Inc

- Extreme Networks Inc.

第八章投资分析

第9章 未来趋势

The global Wi-Fi router market is valued at USD 12.50 billion in the current year and is expected to reach USD 19.88 billion over five years, achieving a CAGR of 9.72% during the forecast period. A growing number of customers are engaging in web browsing, mobile learning, and other online-related activities, driving the demand for faster Internet access. As a result, the wireless router, frequently utilized in laptops, PCs, and tablets, has become essential for human existence. Wireless routers are primarily responsible for the rising need among consumers to stay linked to dependable Internet and for enhancing internet connections in numerous nations.

Key Highlights

- A growing number of customers are engaging in e-commerce transactions, web browsing, mobile learning, and other online-related activities, driving the demand for faster Internet access. As a result, the wireless router, frequently utilized in laptops, PCs, and tablets, has become essential for human existence. Wi-Fi routers are mostly responsible for the rising need among consumers to stay linked to dependable Internet and for enhancing Wi-Fi connections in numerous nations. The increasing use of connected devices in healthcare, education, business, financial services, and other applications is one of the critical drivers of the worldwide wireless router market. Additionally, the market growth is positively impacted by small and medium businesses adopting a bring your device policy. Further, during the projected period, a rise in government initiatives for smart city projects is anticipated to create lucrative opportunities for market expansion.

- Further, in 2022, the International Telecommunication Union (ITU) estimates that 5,300 Million people, or 66% of the world's population, will use the Internet. This marks a 24% growth from 2019, with an expected 1.1 billion individuals joining the Internet throughout that time. The advancement in Internet penetration will create opportunities for international and local Wireless router vendors to introduce new products and improve the bandwidth to capture a significant market share.

- Moreover, By 2023, there will be close to 30 billion network-connected devices and connections, up from 18.4 billion in 2018, predicts Cisco's Annual Internet Report. By 2023, IoT devices will drive up 50% (14.7 billion) of all networked devices, up from 33% (6.1 billion) in 2018. Further, according to Cisco, the fixed internet IP traffic has increased from 65,942 units in 2016 to 1,87,386 units in 2021. Such a rise in internet traffic will drive the studied market. Further, according to the stats counter, in Canada, mobile traffic accounted for more than 38.04 % of all website traffic in January 2022, down from 40.95% in 2020. In Canada, desktops and laptops continue to dominate web usage. Such a rise in Internet-connected devices would allow the studied market to grow.

- On the flip side, According to Nokia's 2022 Annual Mobile Broadband Index (MBiT) Report, data traffic grew by 31%, and the monthly average for mobile data use reached 17GB per user. India's rapidly expanding 4G and 5G networks carried practically all mobile broadband traffic. More than 40 million new or upgraded 4G subscribers will be using services in 2021, according to the report. As digitization adaptation increases, this amount will increase even more. Traffic in metro areas has significantly increased as compared to prior years. In recent years, inter-jurisdictional and inter-disciplinary communications interoperability was greatly aided by the fourth generation Long Term Evolution (4G/LTE) mobile broadband networks.

- Working from home has become a megatrend post COVID pandemic. The speed of the shift to large-scale distant work has resulted in the use of personal devices, including portable phones, laptops, desktops, etc. Employees are also observed using individual or wireless Wi-Fi routers and internet connections to access the corporate network. According to Eurostat, a considerable increase in the proportion of employed people in Europe who could work from home was observed, reaching 29.4% in France, 22.8% in Germany, 15.1 percentage in Spain, and 13.6% in Italy.

Wi-Fi Router Market Trends

Retail and E-commerce are Expected to Hold Significant Share of the Market

- E-commerce (or electronic commerce) is the buying and selling of goods or services on the Internet. It encompasses various data, systems, and tools for online buyers and sellers, including mobile shopping and online payment encryption. Most businesses with an online presence use an online store and/or platform to conduct ecommerce marketing and sales activities and to oversee logistics and fulfillment. Such trends in E-commerce would drive the demand for Wi-Fi routers so that consumers can have access to any online shopping site.

- A growing number of customers are engaging in e-commerce transactions, web browsing, mobile learning, and other online-related activities, driving the demand for faster internet access. As a result, the wireless router, frequently utilized in laptops, PCs, and tablets, has become essential for human existence. Wi-Fi routers are mostly responsible for the rising need among consumers to stay linked to dependable Internet and for enhancing Wi-Fi connections in numerous nations.

- At the beginning of 2022, Singapore had 8.70 million active mobile connections, according to data from Groupe Speciale Mobile Association (GSMA) Intelligence. Furthermore, mobile connections in Singapore were equivalent to 147% of the total population in January 2022. Such internet penetration in the region will drive the e-commerce market. Furthermore, According to the Singapore Department of Statistics, in 2022, online computer and telecommunications equipment sales accounted for 47.4% of total sales. In comparison, 30% of furniture and household equipment were acquired online. Such a rise in online purchases in the region will significantly create an opportunity for new players to enter the market and for international players to expand their presence in Singapore.

- According to the Ministry of Transport and Communications (MoTC), Qatar leads the Middle Eastern countries in terms of the average value of a single transaction at USD 264 per transaction. Moreover, 350 e-commerce companies were operating in the country last year, and 66 more e-commerce companies opened in the next six months, bringing the total to 416 by the end of December last year. Further, in Qatar, e-commerce penetration is 62.1%. Also, online shoppers by demographics, Qataris (22%), are the most likely to shop online, followed by Westerners (17%), Arabs (19%), Asians (20%), and others (22%). Qatar has the most significant average yearly e-commerce spend per user in the Middle East and Northern Africa (MENA) area (relative to the GCC), and the average value per online transaction is greater than the GCC average.

- According to Kibo Commerce, During the second quarter of 2022, 2.3% of visits to e-commerce websites in the United States converted to purchases. In Great Britain, online shopper conversion rates rose to over four percent. Although mobile commerce is catching up regarding page views and revenue, traditional online shopping via PC still holds the top. Such a rise number of online users' conversion rates positively impact the student market.

North America is Expected to Hold Significant Share of the Market

- The United States is one of the leading countries in terms of technological development, digitalization of businesses, and internet usage. The requirement of high-speed internet is becoming essential to match the requirement for the country's digital transformation journey. According to Cisco Systems, the average Wi-Fi network connection speed in North America was 109.5 Mbps in 2023, an increase from 70.7 Mbps in 2020. Such huge speed internet would push the players to develop new Wi-Fi routers to support such internet speeds.

- The United States government is engaged in assisting Thailand 4.0., as they were collaborating with America's private sectors. In 2022, the United States, the Royal Thai government, and business executives started a workshop to share knowledge on the significance of 6 GHz spectrum allocation and next-generation Wi-Fi technology, which will not only make home Wi-Fi faster but also further solidify Thailand's position as a hub of advanced manufacturing and industry innovation. These partnerships between the country will drive the market for Wi-Fi manufacturers in the USA.

- Companies in the region are launching updated products with economical prices to increase their market shares. For example, in May 2022, American router maker Linksys intends to introduce dual-band Wi-Fi 6 routers, including the Hydra 6 and Atlas 6. These routers would offer reliable connectivity for hybrid work, online gaming, 4K UHD streaming, and more because they are designed for speed and performance at a reasonable price.

- Canada is an economically developed country for which people can afford smart devices for their convenience, and the number of connected devices has been increasing in the country, fueled by internet penetration. According to Cisco, Devices and connection per capita increased to 10.7 in 2021, which was 6.3 in 2016. In addition, by 2023, there will be 35.3 million Internet users in Canada, which shows huge growth potential for the Wi-Fi routers in the country because the growth of Internet users will positively impact the Wi-Fi routers.

- The country's need for Internet services with low latency and increasing speed is increasing, and many global players are launching advanced Wi-Fi routers or meshed Wi-Fi routers in the country. For example, in October 2022, Google launched its Nest Wi-Fi Pro with Wi-Fi 6E support in Canada, the company's first router capable of operating in a triband mesh network. On compatible devices, Wi-Fi 6E (E for Extended), which uses the new, less-congested 6 GHz radio band, provides speeds up to two times quicker than Wi-Fi 6.

Wi-Fi Router Industry Overview

The Wi-Fi router market is moderately consolidated with the presence of several players like Cisco Systems Inc, Ericsson Inc., Huawei Technologies Co. Ltd., Juniper Networks Inc., Alcatel Lucent Enterprise, etc. The companies continuously invest in strategic partnerships and product developments to gain substantial market share.

In March 2023, NETGEAR introduced its first Wi-Fi 7-capable router, the Nighthawk RS700 - possibly one of the fastest consumer-grade networking devices capable of a 19 Gbps peak data rate. NETGEAR stated the tri-band unit is designed for low-latency AR(Augmented Reality)/VR (Virtual reality) gaming, UHD Zoom calls, 8k simultaneous streaming, and many more. The RS700 has a new tower-like shape not reminiscent of the last Nighthawk routers, which is designed to house antennas for 360-degree coverage of up to 3,500 square feet.

In November 2022, TP-Link, a global consumer and business networking product provider, released an entire home and business Wi-Fi 7 product line. TP-Link launched new Wi-Fi 7 routers, Omada EAPs, Deco products, and Aginet products for ISP markets to cover all usage scenarios. TP-Link's new HomeShield 3.0 also provides more reliable and smarter network solutions. Continuing as one of the top performances of the Archer series, Wi-Fi 7 routers bring unprecedented experiences to homes. Three Wi-Fi 7 routers were unveiled at the event. Among them, Archer BE900 has quad-band 24 Gbps Wi-Fi 7 speeds and has a brand new design reimagined from previous routers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Ecosystem Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Buyers

- 4.3.2 Bargaining Power of Suppliers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

- 4.5 Use Cases

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth in Internet Traffic and Increasing Consumer Demand for Internet-enabled Devices

- 5.1.2 Exponential Increase in the Bandwidth Requirements across Enterprises owing to Digitization

- 5.2 Market Restraints

- 5.2.1 Network Security and Complexities Related to Network Management

- 5.2.2 Usage of Mobile Broadband

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Edge Router

- 6.1.2 Core Router

- 6.2 By Organization Size

- 6.2.1 SMEs

- 6.2.2 Large Enterprises

- 6.3 By End-User Industry

- 6.3.1 Healthcare

- 6.3.2 Transportation & Logistics

- 6.3.3 Retail & eCommerce

- 6.3.4 Manufacturing

- 6.3.5 Government

- 6.3.6 BFSI

- 6.3.7 Others

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 APAC

- 6.4.4 Middle East and Africa

- 6.4.5 Latin America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems Inc

- 7.1.2 Ericsson Inc.

- 7.1.3 Huawei Technologies Co.ltd

- 7.1.4 Juniper Networks Inc.

- 7.1.5 Alcatel Lucent Enterprise SAS

- 7.1.6 ARUBA S.P.A

- 7.1.7 Fortinet Inc.

- 7.1.8 Panasonic Corporation

- 7.1.9 Broadcom Inc

- 7.1.10 Extreme Networks Inc.