|

市场调查报告书

商品编码

1408575

汽车作业系统:市场占有率分析、产业趋势与统计、2024-2029 年成长预测Automotive Operating Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

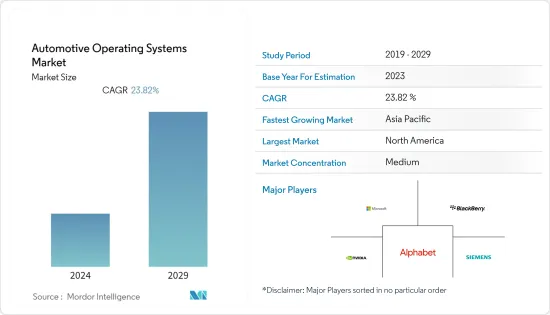

汽车作业系统市场目前的市场规模为154.2亿美元,预计未来五年将达到448.9亿美元,预测期内复合年增长率为23.82%。

主要亮点

- 电动和自动驾驶汽车的普及、车辆中 ADAS(高级驾驶辅助系统)功能的日益采用以及用户介面 (UI) 增强的先进技术的介入预计将显着推动市场成长。

- 许多与连接相关的解决方案都得到了很好的集成,特别是在现代车辆中,它们主要需要互联网服务来执行各自的功能。透过这种方式,车辆可以透过整合或嵌入式连接服务提供连接。透过智慧型手机和现代连接设备,您可以创建一个具有整体影响力的旅行目的地,为车内的每个设备提供网路存取。未来,连接解决方案领域的成长预计将推动连网型汽车市场的成长,并显着增加汽车作业系统市场的成长机会。

- 此外,汽车产业在汽车连接、机器学习和 ADAS 方面取得了重大进展,使车辆能够与其他车辆和外部设备通讯。这种连接提供了高效的流量管理、增强的安全功能以及改进的整体用户体验,从而导致对支援这些功能的作业系统的需求。

- 例如,2022 年 9 月,Qualcomm Technologies, Inc. 与领先的开放原始码解决方案提供商红帽建立了业务伙伴关係,该解决方案主要用于汽车连接和远端资讯处理、数位驾驶座和ADAS(高级驾驶员辅助)。它将为搭载 Snapdragon 数位底盘平台的下一代汽车提供功能安全认证 (ASIL-B)、基于 Linux 的作业系统,该平台是 Snapdragon 开发的一组可扩展、开放和云端连接的平台。

- 此外,重要的公司也在投资、与其他业务合併、投资新计画,以扩大消费群并满足各种应用的需求。例如,2023 年 2 月,梅赛德斯-奔驰宣布推出新作业系统 MB.OS,该作业系统将开始安装在该公司新 MMA 平台支援的新车中。新作业系统将让车主检查一系列重要的安全功能,包括扫描道路的雷射雷达等,并允许在机舱主画面上玩《愤怒的小鸟》等游戏和《TikTok》等社群媒体。

- 然而,隐私和安全相关问题等因素是全球汽车作业系统市场面临的重大挑战,并可能限制整个预测期内的市场成长机会。

- COVID-19 的爆发已成为对汽车操作系统市场产生重大影响的关键因素。 COVID-19 大流行给製造商的稳定性和财务弹性带来了巨大压力,对市场成长产生了负面影响。然而,近年来,随着许多公司转向远端工作环境并寻求汽车相关服务的进步,对汽车作业系统的需求不断增加。

汽车作业系统市场趋势

对联网汽车和自动驾驶汽车的需求增加以及各种安全功能预计将推动市场发展

- 随着车辆越来越多地配备先进的安全和舒适功能,例如车辆资讯娱乐和 ADAS(高级驾驶员辅助系统),该市场正在快速成长。由于乘客安全性和舒适性意识的增强,整合 ADAS(高级驾驶辅助系统)功能的自动驾驶汽车的产量不断增加,以及强制要求安全功能的各种政府法规正在推动市场需求。

- 全球汽车产业的整体动态也在快速变化。此外,自动驾驶和自动驾驶车辆的接受度不断提高也对整体市场成长做出了重大贡献。预计这将在预测期内提供广泛的利润丰厚的成长机会。

- 此外,印度、中国和美国有关 ADAS 要求的法规不断增加,要求所有车辆配备各种系统,包括停车系统辅助,这导致汽车製造商正在采取各种重要措施来装备汽车和具有这些功能的车辆。 ADAS 功能曾经仅适用于高檔汽车,现在已包含在其他车辆领域。这些系统也可作为非豪华汽车的选配设备。如今,这些重要功能也适用于商用车。

- 2023年7月,oToBrite推出了oToGuard,这是世界上第一个用于重型商用车的一体式ADAS系统。只需一个德州仪器(TI) TDA4 汽车处理器即可实现AVM、MOIS (UN R159)、BSIS (UN R151)、BSD、FCW/HWM/PCW、LDW (UN R130)、DMS 以及ACC、LKA 等10多种ADAS 功能可实现包括L2+ADAS感知功能。一套系统可以满足多项联合国法规,同时提高重型商用车的整体安全性。

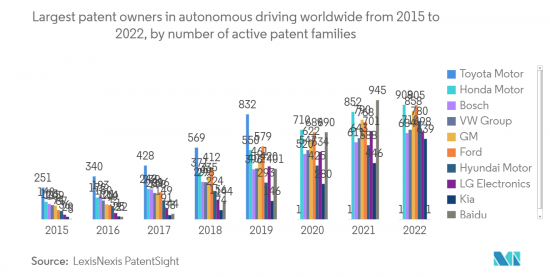

- 根据LexisNexis PatentSight统计,截至2022年12月31日,丰田汽车的专利组合包括1,823个活跃专利系列,使该公司成为全球自动驾驶专利持有者,而百度和本田汽车的专利组合分别包括1,209个和908个活跃专利系列。这些活跃专利系列总数的增加预计将倍增市场成长机会。

北美获得主要市场占有率

- 预计北美将在预测期内主导市场。这主要是由于强大而成熟的汽车公司丛集以及微软和谷歌等全球重要科技公司的所在地等因素,使该地区成为自动驾驶汽车的先驱。特别是在美国,自动驾驶汽车已经在德克萨斯州、加利福尼亚州、华盛顿州、亚利桑那州和密西根州等多个州进行测试和使用。

- 近年来,中国推出的自动驾驶汽车车型总数大幅增加,汽车参与企业的自动驾驶系统开发也不断取得进展。此外,预计在整个预测期内将继续保持整体成长率。

- 2022 年 5 月,通用汽车与全球开放原始码解决方案供应商红帽公司合作,协助推进边缘软体定义汽车。两家公司期待主要透过红帽汽车作业系统来扩展其创新生态系统,该系统为通用汽车 Ultifi 软体平台的持续发展提供功能安全认证的 Linux 作业系统基础。我是。红帽公司与通用汽车之间的合作是技术与交通行业融合的一个重要时刻,因为红帽的云原生、企业级、开放原始码操作系统继 Ultifi 的首次推出之后,推动了通用汽车软体的整体发展-定义的车辆程序。这将使两家公司能够在典型开发时间的一小部分时间内可靠、负责任地向客户提供更有价值的功能。

- 此外,2023年9月,Google云端与科技公司大陆集团建立策略合作伙伴关係,为汽车产业提供灵活、创新、面向未来的数位解决方案。此次合作将把大陆集团的汽车技术专业知识与Google的资料和人工智慧技术相结合,打造新一代高效、安全和以用户为中心的汽车解决方案。此外,两家公司期待未来将策略伙伴关係拓展到更多合作领域,旨在进一步打造汽车互联和客户体验。

汽车作业系统产业概况

汽车作业系统产业包括各种主要企业,包括微软公司、黑莓有限公司、Nvidia公司、Alphabet公司和西门子公司。这些公司为汽车技术和作业系统的发展做出了重大贡献。

2023 年 7 月,领先的汽车安全软体供应商 TTTech Auto 与发布/订阅/查询协议创新者 ZettaScale Technology 合作,宣布推出突破性的 Zetta Auto 平台。两家公司利用各自的技术优势,成为汽车产业整合通讯解决方案的先驱。最初,这些公司的重点是提高服务导向的架构(SOA)通讯的安全性、效能和可预测性。此外,Zetta Auto 旨在弥合云端和微控制器系统之间的通讯差距,满足产业的关键需求。

BlackBerry Limited 于 2023 年 5 月发布了 QNX 软体开发平台 (SDP) 8.0。 QNX 软体开发平台(SDP) 8.0 是一个基于镜像的软体开发平台,旨在帮助汽车製造商和物联网系统开发人员以更低的成本开发更强大的产品,同时不牺牲安全性、安全性或可靠性。这是一个临时版本。 SDP 8.0 由先进的新世代作业系统 QNX 提供支持,是 QNX 嵌入式作业系统产品的巅峰之作。此版本充分利用了物联网系统开发商和汽车製造商青睐的越来越多的多核心处理器。此版本反映了利用 BlackBerry QNX 领先的知识产权和高效能 EDGE 运算方面的丰富经验进行的广泛研究和开发工作。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究成果

- 研究场所

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 市场驱动因素

- 对联网汽车和自动驾驶汽车的需求增加

- 人工智慧和机器学习技术在汽车系统中的集成

- 市场抑制因素

- 对资料隐私和网路安全的担忧

- 价值链/供应链分析

- 波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔

- 作业系统类型

- QNX

- Linux

- Android

- Windows

- 其他作业系统类型

- 汽车模型

- 小客车

- 商用车

- 应用程式类型

- 资讯娱乐系统

- ADAS 与安全系统

- 连网型服务

- 车身控制与舒适系统

- 引擎控制和动力传动系统

- 其他使用类型

- 地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第六章 竞争形势

- 公司简介

- BlackBerry Ltd

- Green Hills Software

- Wind River Systems

- Luxoft

- DXC Technology

- Microsoft Corporation

- Alphabet Inc.

- Nvidia Corporation

- Renesas Electronics Corporation

- Siemens AG

第七章 市场机会及未来趋势

The automotive operating systems market is valued at USD 15.42 billion in the current year and is expected to register a CAGR of 23.82% during the forecast period to become USD 44.89 billion by the next five years.

Key Highlights

- The surge in the penetration of electric and autonomous vehicles, the rise in the adoption of advanced driver assistance systems (ADAS) features in cars, and the interference of advanced technologies for enhanced user interface (UI)are anticipated to drive the market's growth significantly.

- Many connectivity-related solutions are well integrated into modern cars that primarily require Internet service, especially to perform their respective functions. Thus, a car can provide connectivity through integrated and embedded connectivity services. With the help of a smartphone or a modern connectivity device, an overall impact travel spot can be created to present Internet access to all the devices within the car. Henceforth, the increase in the field of connectivity solutions will enhance the growth of the connected cars market, which will considerably augment the automotive operating systems market's growth opportunities.

- Moreover, the automotive industry has witnessed significant advancement in-vehicle connectivity, machine learning, and ADAS, allowing vehicles to communicate with other vehicles and external devices. This connectivity offers efficient traffic management, enhances safety features, and improves the overall user experience, leading to this demand for operating systems supporting these features.

- For instance, in September 2022, Qualcomm Technologies, Inc. declared that it is operational with Red Hat, a leading provider of open-source solutions, to bring functional-safety certified (ASIL-B) Linux-based operating systems to next-generation vehicles that mainly utilize Snapdragon Digital Chassis platforms, a set of scalable and open cloud-connected platforms primarily built for automotive connectivity and telematics, digital cockpit, and advanced driver assistance.

- Furthermore, to increase their consumer base and better meet their demands across various applications, significant companies are also investing, merging with other businesses, and investing in new projects. For instance, in February 2023, Mercedes-Benz declared it's got a new operating system, MB.OS that would start appearing on new vehicles underpinned by the company's new MMA platform. Owners would witness various crucial safety features such as road-scanning lidar, especially due to the new operating system, and games like Angry Birds and social media such as TikTok would be available on the cabin-dominating screens.

- However, factors like privacy and security-related concerns are the significant challenges the global automotive operating systems market faces, which could restrict the market's growth opportunities throughout the forecast period.

- The COVID-19 pandemic emerged as a significant factor that had a profound impact on the automotive operating systems market. It exerted enormous pressure on manufacturers' stability and financial resilience, leading to adverse effects on the market's growth. However, as most companies transitioned to remote working environments and explored advancements in automotive-related services, the demand for automotive operating systems grew in recent times.

Automotive Operating Systems Market Trends

Increase in demand for connected and autonomous vehicles along with various safety features is expected to drive the market

- The surge in the integration of advanced safety and comfort features in the vehicle, like vehicle infotainment, advanced driver assistance systems, and many others, is witnessing major growth in the market. Growing production of autonomous vehicles with integrated advanced driver assistance systems (ADAS) features in the wake of increasing awareness toward the safety and comfort of passengers, as well as various government regulations mandating safety features, are expected to drive demand in the market.

- The overall dynamics of the global automotive industry are also changing at a rapid pace. Moreover, the increasing acceptance of self-driving and automated vehicles further contributes to the total growth of the market significantly. This is anticipated to bring a broad range of lucrative growth opportunities throughout the forecast period.

- Also, due to a rise in the regulations on ADAS requirements, like mandatory installation of various systems, including parking system assistance in all cars in India, China, the United States, etc., the automakers are making various significant efforts to include these features in most of their vehicles and cars. The ADAS features, which were only available in the premium cars, are now being brought to other car segments as well. These systems are being provided as optional equipment in cars other than high-end vehicles. In recent days, these crucial features are also being provided in commercial vehicles as well.

- In July 2023, oToBrite introduced its product, oToGuard, the world's first all-in-one ADAS system for heavy commercial vehicles. With only one Texas Instruments TDA4 automotive processor, it can allow more than 10 ADAS features such as AVM, MOIS (UN R159), BSIS (UN R151), BSD, FCW/HWM/PCW, LDW (UN R130), DMS, as well as L2+ADAS perception features like ACC, LKA, and more. While augmenting the overall safety of heavy commercial vehicles, it can also comply with multiple UN regulations in just one system.

- As per LexisNexis PatentSight, as of December 31, 2022, Toyota Motor's patent portfolio included 1,823 active patent families, which made the company the world's significant owner of autonomous driving patents, whereas Baidu and Honda Motor's patent portfolio included 1,209 and 908 active patent families respectively. A rise in the total count of these active patent families is thus expected to create significant growth opportunities for the market exponentially.

North America Captured a Major Market Share

- North America is expected to dominate the market in the forecast period. It is mainly due to factors like strong and established automotive company clusters and also being the home for the world's significant technology companies like Microsoft, Google, etc., the region has been a pioneer in regard to autonomous vehicles. Particularly in the United States, self-driving cars have already been tested and used in Texas, California, Washington, Arizona, Michigan, and various other states of the United States.

- The country has been significantly maximizing the total number of launches of autonomous car models, as well as the development of vehicle autonomous systems among the players in the entire automotive industry, over the past few years. Furthermore, it is expected to continue its overall growth rate throughout the forecast period.

- In May 2022, General Motors and Red Hat Inc., the global provider of open-source solutions, collaborated to assist advance software-defined vehicles at the edge. The companies primarily expect to extend an ecosystem of innovation throughout the Red Hat In-Vehicle Operating System, which delivers a functional-safety certified Linux operating system foundation that is intended for the ongoing evolution of GM's Ultifi software platform. This collaboration between Red Hat and GM is a noteworthy moment in the convergence of the technology and transportation industries, with Red Hat's cloud-native, enterprise-grade open-source operating system boosting the overall development of GM's software-defined vehicle programs following Ultifi's initial launch. This would allow both companies to provide customers with more valuable features reliably and responsibly in a fraction of the typical development time.

- Also, in September 2023, Google Cloud and technology company Continental entered into a strategic partnership to provide flexible, innovative, and future-oriented digital solutions for the automotive industry. The partnership would combine Continental's expertise in automotive technology with Google's data and AI technologies to build a new generation of efficient, safe, and user-focused automotive solutions. Furthermore, the two parties expect to extend their strategic partnership into additional fields of collaboration in the future, with the aim of building greater in-car connectivity and experiences for the customers.

Automotive Operating Systems Industry Overview

The automotive operating systems industry features a diverse array of key players, including Microsoft Corporation, BlackBerry Ltd, Nvidia Corporation, Alphabet Inc., and Siemens AG. These companies contribute significantly to the evolution of automotive technology and operating systems.

In July 2023, TTTech Auto, a leading provider of automotive safety software, joined forces with ZettaScale Technology, an innovator in pub/sub/query protocols, to introduce the groundbreaking Zetta Auto platform. Leveraging their respective technological strengths, these two firms are pioneering a unified communication solution for the automotive sector. Initially, their focus was on enhancing the safety, performance, and predictability of Serviced-Oriented Architecture (SOA) communication. Furthermore, Zetta Auto aims to bridge the gap in communication between cloud and microcontroller systems, addressing a critical need in the industry.

In May 2023, BlackBerry Limited unveiled the QNX Software Development Platform (SDP) 8.0, a game-changing release designed to empower automakers and IoT systems developers to create more potent products at reduced costs without compromising on security, safety, or reliability. Powered by the advanced next-generation QNX operating system, SDP 8.0 represents the pinnacle of the company's embedded OS offerings. This release maximizes the performance capabilities of the growing number of multi-core processors preferred by IoT systems developers and automakers. It reflects extensive research and development efforts that leverage BlackBerry QNX's top-notch intellectual property and extensive experience in high-performance EDGE computing.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in demand for connected and autonomous vehicles

- 4.2.2 Integration of AI and machine learning technologies in automotive systems

- 4.3 Market Restraints

- 4.3.1 Concerns about data privacy and cyber security

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Operating System Type

- 5.1.1 QNX

- 5.1.2 Linux

- 5.1.3 Android

- 5.1.4 Windows

- 5.1.5 Other Operating System Types

- 5.2 Vehicle Type

- 5.2.1 Passengers Cars

- 5.2.2 Commercial Vehicles

- 5.3 Application Type

- 5.3.1 Infotainment System

- 5.3.2 ADAS and Safety System

- 5.3.3 Connected Service

- 5.3.4 Body Control and Comfort Systems

- 5.3.5 Engine Management and Powertrain

- 5.3.6 Other Application Types

- 5.4 Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia Pacific

- 5.4.4 Latin America

- 5.4.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 BlackBerry Ltd

- 6.1.2 Green Hills Software

- 6.1.3 Wind River Systems

- 6.1.4 Luxoft

- 6.1.5 DXC Technology

- 6.1.6 Microsoft Corporation

- 6.1.7 Alphabet Inc.

- 6.1.8 Nvidia Corporation

- 6.1.9 Renesas Electronics Corporation

- 6.1.10 Siemens AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

汽车作业系统市场-全球产业规模、份额、趋势、机会和预测(按作业系统类型、内燃机车辆类型、应用、地区和竞争格局划分,2020-2030 年预测)

汽车作业系统市场-全球产业规模、份额、趋势、机会和预测(按作业系统类型、内燃机车辆类型、应用、地区和竞争格局划分,2020-2030 年预测) 汽车作业系统市场规模、份额和趋势分析报告:按类型、车辆类型、应用程式、地区和细分市场预测(2025-2033 年)

汽车作业系统市场规模、份额和趋势分析报告:按类型、车辆类型、应用程式、地区和细分市场预测(2025-2033 年) 汽车作业系统市场按类型、产品、技术、车辆类型和应用划分-2025-2030 年全球预测

汽车作业系统市场按类型、产品、技术、车辆类型和应用划分-2025-2030 年全球预测 2025年全球汽车作业系统市场报告

2025年全球汽车作业系统市场报告 汽车作业系统市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测

汽车作业系统市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测 到 2030 年汽车作业系统市场预测:按类型、车型、应用、最终用户和地区分類的全球分析

到 2030 年汽车作业系统市场预测:按类型、车型、应用、最终用户和地区分類的全球分析 全球及中国汽车作业系统(OS)产业(2023-2024)

全球及中国汽车作业系统(OS)产业(2023-2024)