|

市场调查报告书

商品编码

1408746

资料中心网路:市场占有率分析、产业趋势/统计、成长预测,2024-2030 年Data Center Networking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2030 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

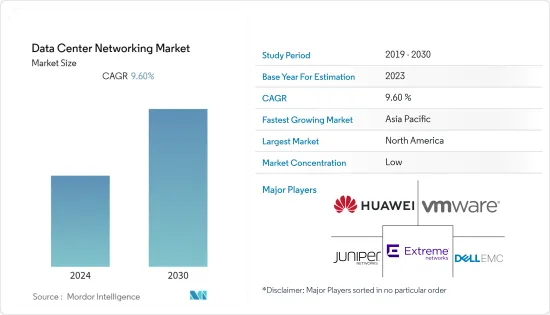

上年度全球资料中心网路市场规模达到 245 亿美元,预计在预测期内复合年增长率为 9.6%。

主要亮点

- 网路解决方案在过去几年中获得了广泛的欢迎,这主要是由于对负载平衡、效能改进以及对更高级需求的支援的需求不断增加。频宽需求的成长速度远远超过企业预算,分散式阻断服务 (DDoS) 等网路攻击不断增加。企业面临的挑战是以用户期望的速度安全、有效率地交付应用程式。这导致了巨大的市场需求。

- 数位化的进步预计将增加对资料中心的需求,并相应地推动网路市场的发展。全产业对边缘运算的投资将在未来四年内显着改变资料中心生态系统的面貌,到 2026 年,边缘元件在总运算中的份额将增加 29%,从 21% 增加到 27%。 Vertiv 对资料中心行业专家进行的新的全球调查的主要发现之一是该行业正在向边缘转移的程度。

资料中心网路市场趋势

应用程式交付控制器占很大份额

- 应用程式交付控制器主要在尖峰时段提供安全性和对应用程式的存取。随着运算转移到云端,软体应用程式交付控制器 (ADC) 正在承担传统上由自订硬体执行的任务。 ADC 也为应用程式部署提供附加功能和弹性。

- 在当今的数位商业环境中,公司专注于保持敏捷性和创新性,以实现竞争、成长和繁荣。因此,随着企业寻求简单、精简的方法来开发、部署、修改和管理应用程序,DevOps 处于数位商务策略的前沿和中心。 ADC 对于实现 DevOps 所实现的全速和敏捷性至关重要。

- 随着企业专注于从不断成长的资料中获得更多价值,市场供应商正在推出可扩展、安全且经济高效的最新 ADC 解决方案。例如,2021年5月,Array Networks发布了其APV系列应用效能控制器的软体版本(版本10.2.x)和创新硬体平台(x800系列)。 APV x800 系列实体家电(APV1800、2800、5800 等)提供多种指标、40 个 Gig-E 介面和改进的 SSL 效能。

- 与产生大量资料的笔记型电脑和桌上型电脑相比,越来越多的用户使用智慧型手机和平板电脑等行动装置上网。根据 GSM 协会的数据,预计到 2025 年,美国将成为全球智慧型手机普及最高的国家。

- 该供应商不断投资于研发活动并提供创新产品,以扩大其市场占有率和基本客群。例如,2022 年 8 月,F5 宣布推出新的流量管理和安全解决方案,旨在让客户更好地控制其 NGINX 实例伫列。新发布的 F5 NGINX 管理套件 1.0 具有集中式仪表板,可提供对 NGINX 实例、应用程式介面 (API) 管理工作流程、应用传输服务和安全解决方案的更大可见性和控制。

亚太地区将推动市场显着成长

- 在亚太地区,超互联环境正在提高通讯业者的重要性,营运商在支援消费者和企业的连接和协作需求方面发挥基础性作用。在整个亚太地区,75% 的通讯业者收益实现正成长。在通讯市场成熟度排名中,韩国排名全球第二,仅次于香港。

- 资料中心的需求显着增加,并且注重效率和低延迟。中国和印度在资料中心建置上着力追赶全球竞争对手,大型企业纷纷扩大资料中心规模,以确保资讯服务的稳定性和可靠性,对处理能力的需求快速成长。

- 韩国政府采用云端运算技术来增强该国的超高速网路连线、电子政府服务和稳定的长期演进 (LTE) 可用性。预计这将对预测期内的市场成长产生积极影响。

- 由于技术进步,受访市场中连网设备的数量正在增加。此外,中国云端运算产业的成长得到了政府的大力支持和私营部门的大量投资的支持。此外,5G和支援5G的设备将显着提高设备的互连性。其结果是连接设备的增加,这直接增加了控制资料流量和云端基础的应用程式的安全性的需求。

- 此外,中国、印度和印尼等国家的网路用户和资料流量正在增加,进一步推动了该地区 ADC 解决方案的成长。随着数位时代的进步,市场供应商透过为最终用户提供更多创新的网路解决方案和产品并确保最佳的技术体验来引领细分市场。

- 例如,2022 年 6 月,网路安全和应用程式交付解决方案供应商Radware 和託管保全服务供应商 OneSecure 宣布扩大合作协议。为了增强OneSecure 为东协企业提供的Webyith 篡改和网域网路钓鱼监控服务,MSSP 透过Radware 的应用程式保护即服务服务和云端分散式拒绝服务(DDoS) 保护服务扩展了其网路安全套件,并宣布将纳入其中。

资料中心网路产业概述

全球资料中心网路市场呈现明显的分散化,近年来竞争形势日益激烈。 Extreme Networks、Dell EMC 和 VMware 等行业主要企业已经巩固了自己的地位并占领了重要的市场占有率。这些主要企业正积极致力于扩大各地区的基本客群。为了实现这一目标,我们正在采取策略合作倡议,旨在加强市场占有率并提高整体盈利。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 市场驱动因素

- 对云端储存的需求不断增长以及对可靠应用程式效能的需求不断增长

- 公司网路攻击增加

- 市场抑制因素

- 网路复杂度

- 价值链/供应链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- COVID-19 影响评估

第五章市场区隔

- 按成分

- 副产品

- 乙太网路交换器

- 路由器

- 储存区域网路(SAN)

- 应用交付控制器 (ADC)

- 其他的

- 按服务

- 安装/集成

- 培训/咨询

- 支援/维护

- 副产品

- 按最终用户

- 资讯科技/通讯

- BFSI

- 政府

- 媒体娱乐

- 其他的

- 地区

- 北美洲

- 欧洲

- 亚太地区

- 南美洲

- 中东

- 非洲

第六章 竞争形势

- 公司简介

- Extreme Networks Inc.

- Dell EMC

- Vmware, Inc.

- Huawei Technologies Co. Ltd.

- Juniper Networks Inc.

- Arista Networks Inc.

- NEC Corporation

- HP Development Company, LP

- Fortinet, Inc.

- Array Networks, Inc.

- Radware Corporation

- A10 Networks, Inc.

- Moxa Inc.

- Lenovo Group Limited

- Broadcom Corporation

- H3C Holding Limited

- NVIDIA(Cumulus Networks Inc.)

- Cisco Systems Inc.

- F5 Networks Inc.

第七章 投资分析

第八章 市场机会及未来趋势

The global data center networking market reached a value of USD 24.5 billion in the previous year, and it is further projected to register a CAGR of 9.6% during the forecast period.

Key Highlights

- Networking solutions have gained significant traction in the past few years, primarily owing to the rising need for load balancing, improving performance, as well as to handle much more advanced requirements. Bandwidth demand is growing much faster than the company budgets, and cyber attacks such as distributed denial-of-service (DDoS) are constantly on the rise. It has become a challenge for companies to securely and efficiently deliver their applications at the speed the users expect. This factor leads to major market demand.

- The rise in digitalization will likely increase the demand for data centers, proportionately driving the networking market. Significantly, industry-wide investment in edge computing will transform the profile of the data center ecosystem over the next four years, raising the edge component of total computing by 29%, from 21% of total computing to 27% in 2026. The extent of the industry's ongoing shift to the edge is among the significant findings from a new global survey of data center industry specialists from Vertiv.

- The upcoming IT load capacity of the global data center server market is expected to reach 71K MW by 2029. The region's construction of raised floor area is expected to increase 273.9 million sq. ft by 2029. The region's total number of racks to be installed is expected to reach 14.2 million units by 2029. North America is expected to house the maximum number of racks by 2029.

- There are close to 500 submarine cable systems connecting the regions globally, and many are under construction. One such submarine cable that is estimated to start service in 2025 is CAP-1, which stretches over 12,000 km with a landing point in Grover Beach, United States.

Data Center Networking Market Trends

Application Delivery Controller to Hold Significant Share

- The application delivery controllers primarily provide security and access to the applications at peak times. As computing is moving toward the cloud, software application delivery controllers (ADCs) have been performing tasks that have been traditionally performed by custom-built hardware. They also offer additional functionalities and flexibility for application deployment.

- In today's digital business environment, businesses focus on staying agile and innovative to compete, grow, and thrive. That puts DevOps front and center in digital business strategy as companies seek simple, streamlined ways to develop, deploy, change, and manage applications. The ADC is critical in enabling the full speed and agility that DevOps makes possible.

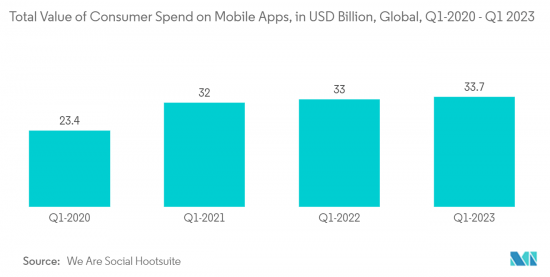

- Moreover, We Are Social and Hootsuite data indicates that consumer spending on mobile applications grew over the past few years, starting at USD 3.7 billion till quarter-one 2023, which is accelerating the demand for the ADC with features that enhance the performance of applications.

- With organizations focusing on extracting greater value from their growing data volumes, market vendors are introducing scalable, secure, and cost-effective modern ADC solutions. For instance, in May 2021, Array Network announced a software version (version 10.2.x) and innovative hardware platforms (the x800 Series) for its APV Series application performance controllers. APV x800 Series physical appliances (APV1800, 2800, 5800, etc.) offer production across multiple metrics, 40 Gig-E interfaces, and improved SSL performance.

- More users are surfing the web on smartphones, tablets, and other mobile devices compared to a laptop or desktops, resulting in the generation of large amounts of data. According to the GSM Association, by 2025, the United States is expected to have the highest smartphone adoption globally.

- Market vendors continuously invest in R&D activities to introduce innovative product offerings to gain more market presence and customer base. For instance, in August 2022, F5 announced the launch of a new traffic management and security solution designed to offer better control over its customers' fleets of NGINX instances. The newly launched F5 NGINX Management Suite 1.0 comes with a centralized dashboard to provide high visibility and control of NGINX instances, application programming interface (API) management workflows, application delivery services, and security solutions.

Asia-Pacific To Hold Significant Market Growth

- In Asia-Pacific, the hyper-connectivity environment has reinforced the importance of telcos, which play a foundational role in supporting consumers' and enterprises' connectivity and collaboration needs. Across Asia-Pacific, 75% of the operators registered positive revenue growth. South Korea is second only to Hong Kong in the world rankings of telecom market maturity.

- The need for data centers is increasing significantly and placing a greater emphasis on effectiveness and low latency. China and India are putting much effort into overtaking their competitors globally in constructing data centers, which is generating a booming demand for processing capacity as larger organizations attempt to scale up their data centers to assure the stability and reliability of data services.

- The South Korean government employed cloud computing technologies to enhance its banking on the country's super-fast internet connectivity, e-government services, and stable long-term evolution (LTE) availability. This is expected to contribute to the market's growth positively over the forecast period.

- Owing to technological advancements, there is an increase in the number of connected devices in the studied market. Moreover, strong government backing and substantial private sector investment are behind the growth of China's cloud computing industry. Furthermore, 5G and 5 G-enabled devices will exponentially increase the devices' interconnectivity. As a result, it increases connected devices, thereby directly augmenting the need for controlling the data traffic and security of the cloud-based applications.

- As financial organizations are increasingly adopting hybrid cloud, public cloud, and multi-cloud strategies to meet the need for compliance, competition, and modernization, the demand for networking solutions is anticipated to grow in the coming years. According to F5's State of Application Strategy Report- Financial Services Edition for 2022, 69% of financial services organizations in the Asia Pacific region have deployed multi-cloud strategies.

- In addition, the increasing internet users and data traffic in countries like China, India, and Indonesia are further augmenting the growth of ADC solutions in the region. With the evolving digital era, market vendors are offering more innovative network solutions and products for end-users, ensuring they have the best technology experience driving the market segment.

- For instance, in June 2022, Cyber security and application delivery solutions provider Radware and managed security service provider OneSecure announced the expansion of their collaboration agreement. In order to enhance OneSecure's Webyith defacement and domain phishing monitoring service for the ASEAN enterprises, the MSSP announced to expand of the cyber security suite to include Radware's Application Protection-as-a-service offering and cloud-distributed denial-of-service (DDoS) protection service.

Data Center Networking Industry Overview

The global data center networking market exhibits a notable degree of fragmentation, characterized by a competitive landscape that has intensified in recent years. Key industry players, including Extreme Networks Inc., Dell EMC, and VMware, Inc., among others, have solidified their positions and demonstrated substantial market shares. These major players are actively concentrating on expanding their customer base across various regions. To achieve this goal, they employ strategic collaborative initiatives designed to bolster their market share and enhance overall profitability.

In November 2022, VMware, Inc. introduced its cutting-edge SD-WAN solution, which encompasses a novel SD-WAN Client. This innovation aims to assist enterprises in delivering applications, data, and services securely, reliably, and efficiently across diverse networks to any device.

In September 2022, AppViewX, a prominent player specializing in automated machine identity management (MIM) and application infrastructure security, made a significant announcement. The company joined F5's Technology Alliance Program (TAP), ushering in a partnership that is expected to jointly promote enterprise application security and delivery solutions. This collaboration focuses on the management of applications and the enhancement of cybersecurity measures across on-premises, cloud, and edge locations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Need of Cloud Storage and Rsing Demand for Reliable Application Performance

- 4.2.2 Increasing Cyberattacks Among Enterprises

- 4.3 Market Restraints

- 4.3.1 Increasing Network Complexity

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 By Product

- 5.1.1.1 Ethernet Switches

- 5.1.1.2 Router

- 5.1.1.3 Storage Area Network (SAN)

- 5.1.1.4 Application Delivery Controller (ADC)

- 5.1.1.5 Other Networking Equipment

- 5.1.2 By Services

- 5.1.2.1 Installation & Integration

- 5.1.2.2 Training & Consulting

- 5.1.2.3 Support & Maintenance

- 5.1.1 By Product

- 5.2 End-User

- 5.2.1 IT & Telecommunication

- 5.2.2 BFSI

- 5.2.3 Government

- 5.2.4 Media & Entertainment

- 5.2.5 Other End-Users

- 5.3 Region

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 South America

- 5.3.5 Middle East

- 5.3.6 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Extreme Networks Inc.

- 6.1.2 Dell EMC

- 6.1.3 Vmware, Inc.

- 6.1.4 Huawei Technologies Co. Ltd.

- 6.1.5 Juniper Networks Inc.

- 6.1.6 Arista Networks Inc.

- 6.1.7 NEC Corporation

- 6.1.8 HP Development Company, L.P.

- 6.1.9 Fortinet, Inc.

- 6.1.10 Array Networks, Inc.

- 6.1.11 Radware Corporation

- 6.1.12 A10 Networks, Inc.

- 6.1.13 Moxa Inc.

- 6.1.14 Lenovo Group Limited

- 6.1.15 Broadcom Corporation

- 6.1.16 H3C Holding Limited

- 6.1.17 NVIDIA (Cumulus Networks Inc.)

- 6.1.18 Cisco Systems Inc.

- 6.1.19 F5 Networks Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

资料中心网路技术:全球市场

资料中心网路技术:全球市场 资料中心网路市场按组件类型、垂直行业和地区划分

资料中心网路市场按组件类型、垂直行业和地区划分 资料中心网路市场按产品类型、部署模式、连接埠速度、应用程式和最终用户划分 - 全球预测 2025-2032

资料中心网路市场按产品类型、部署模式、连接埠速度、应用程式和最终用户划分 - 全球预测 2025-2032 资料中心网路市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

资料中心网路市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 2025年全球云端资料中心市场报告2025年全球自癒网路市场报告

2025年全球云端资料中心市场报告2025年全球自癒网路市场报告 资料中心路由器市场 - 全球及区域分析:按路由器类型、资料中心类型、最终用户垂直领域及区域 - 分析与预测(2025-2034)

资料中心路由器市场 - 全球及区域分析:按路由器类型、资料中心类型、最终用户垂直领域及区域 - 分析与预测(2025-2034) 全球云端资料中心市场

全球云端资料中心市场 资料中心网路市场规模、份额和趋势分析报告:按组件、最终用途、地区和细分市场预测,2025 年至 2033 年

资料中心网路市场规模、份额和趋势分析报告:按组件、最终用途、地区和细分市场预测,2025 年至 2033 年 全球资料中心网路市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测

全球资料中心网路市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测