|

市场调查报告书

商品编码

1408754

日本资料中心网路:市场占有率分析、产业趋势与统计、2024 年至 2030 年成长预测Japan Data Center Networking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2030 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

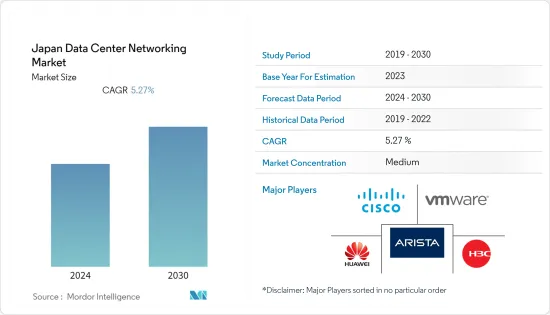

上年度日本资料中心网路市场规模达到 7.096 亿美元,预计在预测期内复合年增长率为 5.27%。

主要亮点

- 中小企业对云端运算的需求不断增长、政府有关资料安全的法规以及国内企业投资的增加是推动日本资料中心需求的主要因素。

- 日本资料中心网路市场未来IT负载能力预计到2029年将达到2000MW。到 2029 年,日本的占地面积预计将增加到 1,000 万平方英尺。

- 预计到2029年,安装的机架总数将达到50万个。到 2029 年,东京将安装最多数量的机架。连接日本的海底电缆系统有近30个,其中许多正在建造中。

- 其中一条海底电缆计划于 2023 年开通,即东南亚-日本 2 号电缆 (SJC2),该电缆全长超过 10,500 公里,登陆点位于千仓和志摩。

- 由于资料储存需求不断增长,全国资料中心的数量正在迅速增加。此外,能源约占资料中心营运成本的40%,这使得资料中心强调能源效率变得越来越重要。为了将提高能源效率作为削减成本的措施,主要企业正在专注于制定日本资料中心的绿色标准,从而增加了对基础设施管理的需求。因此,预计这些因素将在预测期内推动市场成长。

日本资料中心网路市场趋势

IT/通讯领域占有很大份额。

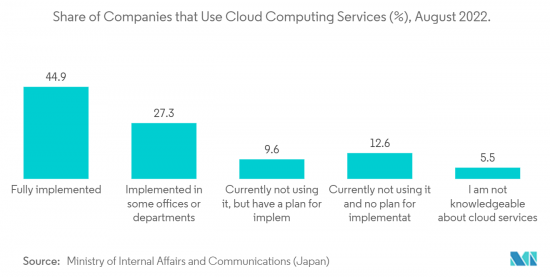

- 基于云端基础的服务的日益普及导致日本零售和超大规模主机代管服务的扩张,从而导致对资料中心空间的需求增加以及对资料中心内网路设备和服务的需求增加。

- 云端服务在日本越来越受欢迎。巨量资料整合的需求、更多远端工作的需求以及资料迁移到云端的需求正在推动国内云端资料中心的使用。

- 预计云端运算在所有最终用户中将显着成长。日本政府数位机构正在中央和地方政府办公室推广云端服务的使用。在日本,企业转向云端基础设施的商业案例得到了多个因素的支持。云端基础设施不需要大量的资本投资,云端处理可以轻鬆地随着每个公司的IT系统进行扩展。整体而言,云端成长率为13.51%。

- 此外,在电讯领域,随着LTE的长期演进,政府继续推动5G和其他能够比目前技术资料传输的最尖端科技的部署。 NTT Docomo、KDDI、Softbank Corporation和乐天移动均已获得内务部分配的 5G 频段。

- 此外,预测期内日本的行动资讯服务收入将以6.8%的速度成长,主要是由于行动网路订阅数量的增加和5G服务的采用增加,从而带来更高的ARPU(每位用户平均收入)。预计会增加。这些发展方面预计将进一步补充该地区资料中心的成长,并促进市场上网路设备和服务的成长。

乙太网路切换器市场占有率最大

- 资料中心乙太网路切换器是运作在资料中心环境中的网路设备。它在资料中心伺服器、储存设备和其他网路设备之间建立互连以促进高效、快速的资料传输方面发挥着至关重要的作用。交换器旨在支援Gigabit和多Gigabit以太网,包括 10GbE、25GbE、40GbE 和 100GbE,以实现高速资料传输。

- 日本各地的资料中心使用广泛的乙太网路交换器网路。日本拥有许多资料中心,为金融、科技和医疗保健等众多产业提供支援。为了确保基础设施的效率和可靠性,这些资料中心依赖乙太网路交换器等高效能网路设备。

- 在日本,5G 服务正在大力部署和采用,资料中心的成长也在扩大。内务部旨在继续推动日本的 5G 体验。我们的目标是到 2024 年 3 月底实现 98% 的 5G 人口覆盖率。资料中心营运商正在增加对先进技术的投资,以保持在全球市场的竞争力。为了满足您的网路需求,您可能会依赖不同製造商的乙太网路切换器,包括国内和国际品牌。

- 市场主要企业正在专注于更新网路设备以满足市场需求。 2023 年 6 月,Cisco Nexus 9800 系列模组化交换器透过新的底盘架构扩展了Cisco Nexus 9000 系列产品组合,该架构包括多个第一代线路卡和交换矩阵模组的组合,能够从57Tbps 扩展到115Tbps,如下图所示。底盘中的每个线路卡插槽可容纳提供 400GE 或 100GE 连接埠以及更高速度的线路卡。

- 超大规模资料中心比企业资料中心具有优势,例如规模经济和自订工程。日本此类设施的数量正在增加。此前,日本企业依赖当地的系统整合。然而,我们现在对全云采取更保守的方法。 Hyperscalar 继续在日本投资,并看到私人公司和政府的数位化带来了巨大的开拓成长。由于网路使用者数量的增加和整个国家的数位化,对资料中心的需求不断增加,预计该行业在预测期内将出现合理增长。

日本资料中心网路产业概况

日本计划未来建置资料中心计划,预计未来几年日本资料中心网路产业的需求将会增加。该市场适度整合,主要参与者包括思科系统公司、Arista Networks Inc.、H3C Technologies、VMware Inc.和华为技术有限公司。这些主要参与者拥有重要的市场占有率,并正在积极努力扩大基本客群。

2023年8月,H3C发布了下一代资料中心交换器S9827系列。此创新产品采用CPO硅光电技术打造,以其卓越的性能成为产业里程碑。单晶片提供高达51.2T的频宽,支援64个800G端口,吞吐量较400G产品提升8倍。该设计融合了液体冷却和智慧型无损操作等先进技术,将有助于创建高度普及、低延迟、节能的智慧网路。Masu。

2022 年 11 月,Equinix 和VMware发布了重要公告,以满足对新型数位基础设施和多重云端服务不断增长的需求。两家公司已宣布计划在全球扩大合作伙伴关係。此外,两家公司还宣布推出VMware Cloud on Equinix Metal,这是一项新的分散式云端服务,旨在支援企业应用程序,提高效能、安全性和成本效率。该服务将 VMware 管理和支援的云端基础设施与 Equinix 互连的全球即服务相结合,为企业提供增强的云端解决方案。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 市场驱动因素

- 更多采用云端基础的服务

- 5G网路的出现推动市场成长

- 市场抑制因素

- 网路安全威胁与勒索软体攻击

- 价值链/供应链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- COVID-19 影响评估

第五章市场区隔

- 按成分

- 副产品

- 乙太网路切换器

- 路由器

- 储存区域网路 (SAN)

- 应用交付控制器 (ADC)

- 其他网路设备

- 网路安全设备、广域网路优化家电和软体,包括:

- 按服务

- 安装与集成

- 培训与咨询

- 支援与维护

- 副产品

- 最终用户

- 资讯科技/通讯

- BFSI

- 政府机关

- 媒体与娱乐

- 其他最终用户

第六章 竞争形势

- 公司简介

- Cisco Systems Inc.

- Arista Networks Inc.

- H3C Technologies Co., Ltd.

- VMware Inc

- Huawei Technologies Co. Ltd.

- Extreme Networks Inc.

- NVIDIA Corporation(Cumulus Networks Inc.)

- Dell EMC

- NEC Corporation

- IBM Corporation

- HP Development Company, LP

- Intel Corporation

- Broadcom Corp

- Schneider Electric

第七章 投资分析

第八章 市场机会及未来趋势

The Japan data center networking market reached a value of USD 709.6 million in the previous year, and it is further projected to register a CAGR of 5.27% during the forecast period.

Key Highlights

- The increasing demand for cloud computing among SMEs, government regulations for local data security, and growing investment by domestic players are some of the major factors driving the demand for data centers in the country.

- The upcoming IT load capacity of the Japan data center market is expected to reach 2000 MW by 2029. The country's construction of raised floor area is expected to increase to 10 million sq. ft by 2029.

- The country's total number of racks to be installed is expected to reach 500 K units by 2029. Tokyo is expected to house the maximum number of racks by 2029. There are close to 30 submarine cable systems connecting Japan, and many are under construction.

- One such submarine cable that is estimated to start service in 2023 is Southeast Asia-Japan Cable 2 (SJC2), which stretches over 10,500 Kilometers with landing points from Chikura and Shima, Japan.

- An increasing need for data storage has resulted in an upsurge in the number of data centers nationwide. Additionally, energy represents around 40% of the operational costs of a data center; it is also becoming increasingly important for data centers to focus on energy efficiency. To improve energy efficiency as a cost-saving measure, key players focus on developing a green standard for data centers in Japan, which results in increasing the demand for Infrastructure management. Hence, such factors are expected to drive market growth during the forecast period.

Japan Data Center Networking Market Trends

IT & Telecommunication Segment Holds the Major Share.

- The increasing adoption of cloud-based services is driving the expansion of retail and hyperscale colocation services in Japan, resulting in increased demand for space in data centers and, consequently, the need for more network devices and services within data centers.

- Cloud services are growing in popularity in Japan. The need for big data integration and the demand for more remote work and data migration to the cloud are driving the use of domestic cloud data centers.

- Cloud is expected to showcase major growth among all the end users. The Government of Japan's Digital Agency promotes the utilization of cloud services for both central government and local government offices. In Japan, the business case for enterprises moving to cloud infrastructure is supported by several factors. Cloud infrastructure does not require a large capital investment, and cloud computing can easily be scaled to each company's IT system. Overall, the growth rate for the cloud is 13.51%.

- Further, in the Telecom sector, the Government is continuing its push to deploy 5G and other cutting-edge technologies that could transfer data faster than currently available with the long-term evolution of LTE. NTT DOCOMO, KDDI, Softbank, and Rakuten Mobile were each allocated a 5G spectrum by the Ministry of Internal Affairs and Communication (MIC).

- Additionally, Mobile data service revenue in Japan is expected to increase at a growth rate of 6.8% during the forecast period, primarily driven by growing mobile internet subscriptions and the increasing adoption of higher average revenue per user (ARPU)-yielding 5G services. Such developmental aspects are expected to further complement the growth of the data centers in the region and substantiate the growth of network devices and services in the market.

Ethernet Switches Holds Largest Market Share

- Data center ethernet switches are network devices that operate in a data center environment. In order to facilitate the efficiency and rapid transfer of data, they play an essential role in establishing interconnection between servers, storage devices, or other network equipment at a data center. Switches are designed for high-speed data transmission with support for gigabit and multigigabit Ethernet, including 10GbE, 25GbE, 40GbE, 100GbE, and beyond.

- Data centers throughout Japan use an extensive network of ethernet switches. Japan has many data centers to support a broad range of industries, including finance, technology, healthcare, and so on. To ensure efficiency and reliability in their infrastructure, these data centers rely on High-Performance Networking Equipment such as ethernet switches.

- Significant deployment and adoption of 5G services in Japan, resulting in increasing the growth of the data centers. The Ministry of International Affairs and Communications aims to continue moving the Japanese 5G experience forward. It set a target of 98% 5G population coverage by the end of March 2024. Data center operators are increasingly investing in advanced technology to maintain their competitiveness in a global market. To meet the network needs, they may rely on Ethernet switches from various manufacturers, including domestic and international brands.

- The key players in the market focus on updating the network devices to meet the market demand. In June 2023, Cisco's Nexus 9800 Series modular switches expand the Cisco Nexus 9000 Series portfolio with a new chassis architecture to include a combination of several first-generation line cards and fabrics modules, allowing it to scale from 57 Tbps up to 115 Tbps. Each line card slot on the chassis can support line cards that now offer 400GE or 100GE ports and higher speeds.

- Hyperscale data centers offer advantages such as economies of scale and custom engineering over enterprise data centers. These facilities are increasing in Japan. Previously, Japanese businesses relied on local systems integrators. However, now, they have a more conservative approach to going full cloud. Hyperscalers continue to invest in Japan and see a large, untapped growth coming from digitization in the private sector and the government. The demand for data centers is continuously rising along with a growing number of internet users and digitalization across the country, which is expected to experience decent growth in the segment during the forecast period.

Japan Data Center Networking Industry Overview

The upcoming DC construction projects in Japan are expected to drive increased demand in the Japan Data Center Networking Market over the coming years. This market is moderately consolidated, featuring key players such as Cisco Systems Inc., Arista Networks Inc., H3C Technologies Co., Ltd., VMware Inc., and Huawei Technologies Co. Ltd. These major players, holding significant market shares, are actively engaged in expanding their customer base in the region.

In August 2023, H3C introduced the S9827 series, a next-generation data center switch. This innovative product, built on CPO silicon photonics technology, marks a milestone in the industry with its remarkable capabilities. It offers a single-chip bandwidth of up to 51.2T and supports 64 800G ports, resulting in an eightfold increase in throughput compared to 400G products. The design incorporates advanced technologies such as liquid cooling and intelligent lossless operations, which collectively contribute to the creation of a highly widespread, low-latency, and energy-efficient smart network.

In November 2022, Equinix, Inc. and VMware, Inc. made a significant announcement in response to the growing demand for new digital infrastructure and Multicloud services. The two companies revealed their plans for a worldwide expansion of their partnership. Additionally, they introduced VMware Cloud on Equinix Metal as a new distributed cloud service aimed at supporting enterprise applications with improved performance, security, and cost-effectiveness. This service is set to combine VMware's managed and supported cloud infrastructure with Equinix's interconnected global bare-metal-as-a-service offering, providing an enhanced cloud solution for businesses.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Adoption of Cloud-Based Services

- 4.2.2 Advent of 5G Networks Drives Market Growth

- 4.3 Market Restraints

- 4.3.1 Cybersecurity Threats and Ransomware Attacks

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 By Product

- 5.1.1.1 Ethernet Switches

- 5.1.1.2 Router

- 5.1.1.3 Storage Area Network (SAN)

- 5.1.1.4 Application Delivery Controller (ADC)

- 5.1.1.5 Other Networking Equipment

- 5.1.1.5.1 Including: Network security equipment, WAN optimization appliance, Softwares)

- 5.1.2 By Services

- 5.1.2.1 Installation & Integration

- 5.1.2.2 Training & Consulting

- 5.1.2.3 Support & Maintenance

- 5.1.1 By Product

- 5.2 End-User

- 5.2.1 IT & Telecommunication

- 5.2.2 BFSI

- 5.2.3 Government

- 5.2.4 Media & Entertainment

- 5.2.5 Other End-Users

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Cisco Systems Inc.

- 6.1.2 Arista Networks Inc.

- 6.1.3 H3C Technologies Co., Ltd.

- 6.1.4 VMware Inc

- 6.1.5 Huawei Technologies Co. Ltd.

- 6.1.6 Extreme Networks Inc.

- 6.1.7 NVIDIA Corporation (Cumulus Networks Inc.)

- 6.1.8 Dell EMC

- 6.1.9 NEC Corporation

- 6.1.10 IBM Corporation

- 6.1.11 HP Development Company, L.P.

- 6.1.12 Intel Corporation

- 6.1.13 Broadcom Corp

- 6.1.14 Schneider Electric

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

资料中心网路技术:全球市场

资料中心网路技术:全球市场 资料中心网路市场按组件类型、垂直行业和地区划分

资料中心网路市场按组件类型、垂直行业和地区划分 资料中心网路市场按产品类型、部署模式、连接埠速度、应用程式和最终用户划分 - 全球预测 2025-2032

资料中心网路市场按产品类型、部署模式、连接埠速度、应用程式和最终用户划分 - 全球预测 2025-2032 资料中心网路市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

资料中心网路市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 2025年全球云端资料中心市场报告2025年全球自癒网路市场报告

2025年全球云端资料中心市场报告2025年全球自癒网路市场报告 资料中心路由器市场 - 全球及区域分析:按路由器类型、资料中心类型、最终用户垂直领域及区域 - 分析与预测(2025-2034)

资料中心路由器市场 - 全球及区域分析:按路由器类型、资料中心类型、最终用户垂直领域及区域 - 分析与预测(2025-2034) 全球云端资料中心市场

全球云端资料中心市场 资料中心网路市场规模、份额和趋势分析报告:按组件、最终用途、地区和细分市场预测,2025 年至 2033 年

资料中心网路市场规模、份额和趋势分析报告:按组件、最终用途、地区和细分市场预测,2025 年至 2033 年 全球资料中心网路市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测

全球资料中心网路市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测