|

市场调查报告书

商品编码

1431031

主资料管理:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Master Data Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

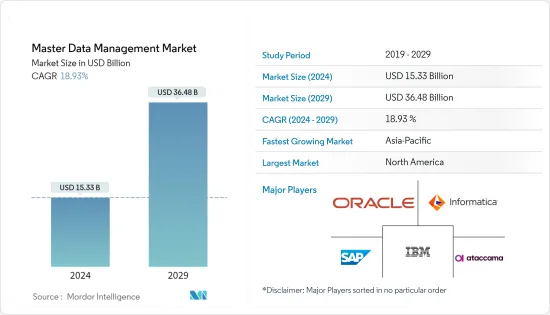

主资料(MDM)管理市场规模预计到2024年为153.3亿美元,预计到2029年将达到364.8亿美元,在预测期内(2024-2029年)复合年增长率为18.93%,预计将会增长。

对资料合规性的需求以及知名公司越来越多地使用主资料管理解决方案来改善业务可能会推动收益成长。

主要亮点

- 主资料管理和资料管治工具对于为决策和消费者参与提供可信任资讯至关重要。这是因为资料是由更广泛的系统、IT 专家以及企业和合作伙伴组织的资料创建和存取的。

- 近年来,组织越来越意识到决定其最重要业务活动成败的资料。物联网 (IoT)、互连连网型、云端处理、行动性和数数位化都在增加资料流量和资料量,再加上更便宜的储存空间。我们强烈建议您节省几乎所有的组织。不幸的是,这种策略会改变敏感、关键和关键任务资料点的参数,并通常造成暗资料沼泽。

- 目前许多公司正在探索和尝试从孤立的资料环境切换到统一的主资料。这种主资料计画(也称为主资料管理计划)的目的是产生和利用关键企业资料的黄金副本,以尽可能接近源头发现、检验和解决资料错误。成功的 MDM 计划可提供资料的一致性、完整性和准确性。然而,实施 MDM 计划只有伴随着业务支援的资料管理倡议才能保证成功。

- 机器学习 (ML)、巨量资料和人工智慧 (AI) 领域的最新创新正在扩大市场。该技术不仅提供了对大量资料集的访问,而且还为资料处理和储存开闢了新的技术可能性。随着新技术变得更有能力处理来自多个学科和观点的资料,客户开始有了不同的期望。最常见的要求是将主资料管理系统与巨量资料、分析和商业智慧技术结合。

- 然而,实施、资料安全和隐私问题正在限制市场收益。严格的立法和广泛的业务要求使 MDM 的实施成为一项挑战。此外,随着公司越来越多地整合技术,他们变得更容易受到安全漏洞和攻击。由于担心丢失重要的个人资料,用户抵制 MDM 解决方案。这些问题阻碍了 MDM 解决方案的采用并限制了市场的收益成长。

主资料管理市场趋势

云端MDM细分市场将占据很大份额

- 随着主资料管理 (MDM) 对企业成功变得至关重要,分析用于捕获、储存和利用主资料的新技术和方法变得至关重要。下一代 MDM 系统将由 AI/ML、云端、联合架构、跨公司共用、全球覆盖、资料平台解决方案和其他现代 MDM 功能提供支援。

- 随着供应商和客户遍布全球并进行虚拟通信,企业部门已转向云端中的 MDM 技术来提高速度和弹性。企业将客製化MDM云端服务,陆上将更加关注主资料与云端来源的整合与资料品质。

- 随着越来越多的应用程式和资料迁移到云端,资料专业人员将能够跨多个云端、云端内和本地源管理日益复杂的资料量。多重云端和跨云端资料管理对于实现这种多样化的拓扑至关重要。

- 云端基础的服务正在广泛用于 MDM(以及其他关键企业应用程式)。随着资料重心不断移出防火墙,在与众包资料和应用程式整合方面,云端 MDM 等云端原生解决方案可能会比本地解决方案更具优势。

- 根据欧盟统计局2021年企业使用云端服务的统计数据,欧盟超过94%的企业已经实施了云端软体即服务,包括主资料管理解决方案。所有业务趋势都显示需要云端原生 MDM 平台。除了需要更少的精力来推出和运行这一众所周知的好处之外,灵活的微服务设计还提供了显着的好处,例如轻鬆更新、平滑的扩充性和快速可移植性。

北美占据主要市场占有率

- 据估计,主资料管理产业占据北美最大的市场占有率。该地区技术使用的不断增长是推动北美 MDM 市场成长的关键因素之一。 IBM、 Oracle和 Informatica Inc. 等 MDM 厂商在各地区的扩张预计将推动市场的进一步扩张。

- 同时,主要区域经济体研发支出的成长正在推动北美主资料管理市场新技术的开拓。

- 例如,2022 年 6 月,整合资料管理和管治解决方案提供商 Ataccama 在一轮成长资本投资中获得了 1.5 亿美元。

- 美国严格的资料保护和安全法规要求银行业和医疗保健等特定行业的组织实施 MDM。提高业务效率和减少资料冗余的日益增长的愿望也推动了市场的发展。

主资料管理产业概述

主资料管理市场高度分散,有几个重要的参与者。目前只有IBM、 Oracle、Informatica Inc.、SAP SE 和Atacma 等少数几家主要企业控制着大部分市场。市场参与者正在国际上扩大消费群,以增加市场占有率和盈利。

- 2022 年 10 月 - 统一资料管理平台领先供应商 Ataccama 宣布提前分发 Ataccama ONE 平台的下一个重大更新。在这个版本中,Ataccama 引入了新功能,支援公司为世界各地的企业提供端到端资料管理并实现资料民主化的目标。此次平台升级使 Ataccama 处于日益增长的行业共识的最前沿,即现代资料管治计划必须以单一用途技术无法实现的方式整合资料管治功能。我会做到的。

- 2022 年 2 月 - IBM 宣布收购 Neudesic,这是一家美国云端服务顾问公司,专门从事 Microsoft Azure 平台和多重云端专业知识。此次收购显着增加了 IBM 的混合多重云端服务组合,并进一步推进了公司的混合云和人工智慧策略。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究成果

- 研究场所

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 对检验和合规性的需求不断增长

- 扩大资料品质工具在资料管理中的使用

- 市场限制因素

- 昂贵的整合和维护工作

- 资料安全和隐私问题

- 各地区实施严格的资料规定

第六章市场区隔

- 按成分

- 软体

- 服务

- 按部署模型

- 本地

- 云

- 按公司规模

- 大公司

- 中小企业

- 按申请

- 供应商

- 副产品

- 客户

- 其他用途

- 按行业分类

- 资讯科技/通讯

- BFSI

- 卫生保健

- 政府机关

- 零售

- 製造业

- 教育

- 其他行业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 中东/非洲

- 世界其他地区

第七章 竞争形势

- 公司简介

- IBM

- Oracle

- Informatica Inc.

- SAP SE

- Ataccama

- SAS Institute Inc.

- TIBCO Software Inc.

- Teradata Corporation

- Syndigo LLC

- Profisee

第八章投资分析

第9章市场的未来

The Master Data Management Market size is estimated at USD 15.33 billion in 2024, and is expected to reach USD 36.48 billion by 2029, growing at a CAGR of 18.93% during the forecast period (2024-2029).

The demand for data compliance and the growing usage of master data management solutions in prominent companies to improve business operations would likely fuel revenue growth.

Key Highlights

- To deliver information that can be relied upon for decision-making and consumer outreach, tools for master data management and data governance are essential. This is because a broader range of systems, IT specialists, and users from businesses and partner organizations create and access data.

- In recent years, organizations have become more aware of their data, which is crucial to the success or failure of an organization's most important business activities. The Internet of Things (IoT), interconnected, connected devices, cloud computing, mobility, and digitalization have all boosted data flow and volume, combined with the availability of less expensive storage, pushing organizations to preserve practically everything. Unfortunately, this strategy has caused sensitive, critical, and mission-critical data points to have varying parameters, commonly creating dark data swamps.

- The switch from segregated data environments to a consolidated master data set is now being investigated and tried by many businesses. The purpose of such master data initiatives, also known as master data management (MDM) projects, is to generate a golden copy of crucial company data for consumption and to discover, validate, and address data errors near the source as feasible. A successful MDM program enables data consistency, completeness, and correctness. However, installing an MDM program can only guarantee success if business-supported data management initiatives are implemented concurrently.

- The market is growing due to recent innovations in machine learning (ML), big data, and artificial intelligence (AI). In addition to offering access to enormous datasets, this technology offers new technological possibilities for data processing and storage. As new technologies' capacity for handling data from several domains and perspectives has increased, customers have a wide range of expectations. The most frequent request has been to combine master data management systems with big data, analytics, and business intelligence technologies.

- However, implementation, data security, and privacy issues constrain market revenue. Due to strict laws and extensive business requirements, MDM implementation might be challenging. Furthermore, firms are progressively integrating technologies, which makes them prone to security flaws and assaults. Users resist MDM solutions because they are concerned about losing critical personal data. These issues are inhibiting MDM solution adoption and limiting the market's revenue growth.

Master Data Management Market Trends

Cloud MDM Segment to Hold a Significant Share

- Analyzing new technologies and approaches for acquiring, storing, and utilizing master data is becoming vital as master data management (MDM) becomes essential for fostering company success. The next generation of MDM systems is driven by AI/ML, cloud, federated architectures, inter-enterprise sharing, global deployment, data platform solutions, and other contemporary MDM features.

- Enterprise sectors have used MDM technologies on the cloud for speed and flexibility since vendors and customers are dispersed worldwide and communicate virtually. Businesses will customize their MDM cloud services, while those onshore will result in a stronger focus on master data integration and data quality to and from cloud sources.

- As more apps and data migrate to the cloud, data professionals can manage more complicated amounts of data across several clouds, inside one cloud, and on-premises sources. To enable these various topologies, multi-cloud and inter-cloud data management is essential.

- Cloud-based services are becoming more widely used for MDM (as well as other essential corporate applications). A cloud-native solution, such as cloud MDM, will probably offer advantages over on-premise solutions concerning integration with cloud-sourced data and apps as the center of gravity for data continues to move beyond the firewall.

- According to Eurostat statistics on enterprise use of cloud services in 2021, over 94% of all businesses in the European Union have implemented cloud software-as-a-service, which includes master data management solutions. Every business trend indicates that a cloud-native MDM platform is required. In addition to the well-known benefit of requiring less work to get up and running, the flexible microservice design offers greater advantages for simple updates, smooth scalability, and rapid portability.

North America to Hold Major Market Share

- The master data management industry is estimated to have the largest market share in North America. The expanding use of technology in the area is one of the main reasons promoting the growth of the MDM market in North America. The expansion of MDM players across regions, such as IBM, Oracle, and Informatica Inc., is anticipated to drive market expansion further.

- On the other hand, the growth of R&D spending by significant regional economies is helping the development of new technologies in the North American master data management market.

- For instance, in June 2022, Ataccama, a unified data management and governance solutions provider, secured USD 150 million in a growth capital investment round, money that will be used to finance the company's efforts to develop new products and expand its market presence.

- Organizations working in specific industries, including banking and healthcare, are required to adopt MDM because of the strict data protection and security rules in the United States. The increasing desire to enhance operational effectiveness and lessen data redundancy also drives the market.

Master Data Management Industry Overview

The master data management market is highly fragmented and has several significant players. Only some key companies currently hold a large portion of the market, such as IBM, Oracle, Informatica Inc., SAP SE, and Ataccama. The players in the market are growing their consumer bases internationally to raise their market share and profitability.

- October 2022 - Ataccama, a top provider of unified data management platforms, announced the early distribution of the upcoming significant update to its Ataccama ONE platform. With this version, Ataccama will introduce new features that support its objective of giving businesses worldwide end-to-end data management and allowing data democratization. The platform upgrade places Ataccama at the forefront of a growing industry agreement that contemporary data governance programs must converge data governance capabilities in ways that single-purpose technologies cannot.

- February 2022 - IBM announced that it had acquired Neudesic, a US cloud services consultant focused on the Microsoft Azure platform and multi-cloud expertise. The portfolio of hybrid multi-cloud services offered by IBM will be significantly increased due to this purchase, further advancing the company's hybrid cloud and AI strategy.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Verification and Compliance

- 5.1.2 Growing Usage of Data Quality Tools for Data Management

- 5.2 Market Restraints

- 5.2.1 Expensive Integration and Maintenance activities

- 5.2.2 Concerns on Data Security and Privacy

- 5.2.3 Stringent Data Regulations Imposed in Various Regions

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Software

- 6.1.2 Service

- 6.2 By Deployment Model

- 6.2.1 On-premise

- 6.2.2 Cloud

- 6.3 By Enterprise Size

- 6.3.1 Large Enterprises

- 6.3.2 Small and Medium Enterprises

- 6.4 By Application

- 6.4.1 Supplier

- 6.4.2 Product

- 6.4.3 Customer

- 6.4.4 Other Applications

- 6.5 By Industry Vertical

- 6.5.1 IT and Telecommunication

- 6.5.2 BFSI

- 6.5.3 Healthcare

- 6.5.4 Government

- 6.5.5 Retail

- 6.5.6 Manufacturing

- 6.5.7 Education

- 6.5.8 Other Industry Verticals

- 6.6 By Geography

- 6.6.1 North America

- 6.6.2 Europe

- 6.6.3 Asia-Pacific

- 6.6.4 Middle East and Africa

- 6.6.5 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM

- 7.1.2 Oracle

- 7.1.3 Informatica Inc.

- 7.1.4 SAP SE

- 7.1.5 Ataccama

- 7.1.6 SAS Institute Inc.

- 7.1.7 TIBCO Software Inc.

- 7.1.8 Teradata Corporation

- 7.1.9 Syndigo LLC

- 7.1.10 Profisee

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

主资料管理市场 - 全球产业规模、份额、趋势、机会和预测,细分、按组件、按部署类型、按组织规模、按垂直行业、按地区、按竞争,2019-2029F

主资料管理市场 - 全球产业规模、份额、趋势、机会和预测,细分、按组件、按部署类型、按组织规模、按垂直行业、按地区、按竞争,2019-2029F 主资料管理市场:按元件、按资料类型、按部署、按产业 - 2025-2030 年全球预测

主资料管理市场:按元件、按资料类型、按部署、按产业 - 2025-2030 年全球预测 主资料管理市场规模、份额、趋势分析报告:按组件、部署模式、最终用途、地区和细分市场预测,2024-2030 年

主资料管理市场规模、份额、趋势分析报告:按组件、部署模式、最终用途、地区和细分市场预测,2024-2030 年 主资料管理市场规模:按组件、按部署模型、按企业规模、按最终用户 - 区域展望、竞争策略、细分市场预测(~2033)

主资料管理市场规模:按组件、按部署模型、按企业规模、按最终用户 - 区域展望、竞争策略、细分市场预测(~2033) 主资料管理的全球市场:2024 年

主资料管理的全球市场:2024 年 主资料管理 (MDM) 解决方案的全球市场 2024-2028

主资料管理 (MDM) 解决方案的全球市场 2024-2028 主资料管理市场:按组件、部署模型、公司规模和最终用户:2023-2032 年全球市场机会分析和产业预测

主资料管理市场:按组件、部署模型、公司规模和最终用户:2023-2032 年全球市场机会分析和产业预测 主资料管理的全球市场

主资料管理的全球市场