|

市场调查报告书

商品编码

1431451

HVAC 感测器:市场占有率分析、行业趋势和统计、成长预测(2024-2029 年)HVAC Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

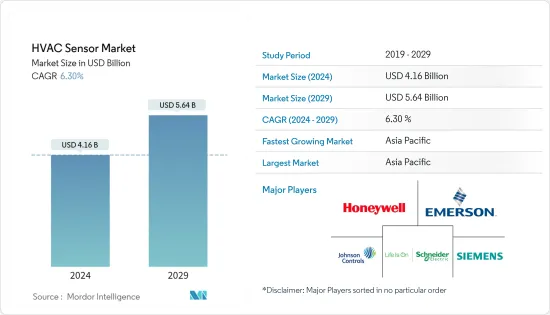

HVAC感测器市场规模预计到2024年将达到41.6亿美元,预计到2029年将达到56.4亿美元,在市场估计和预测期间(2024-2029年)复合年增长率为6.30%。曾经。

HVAC 感测器可调节和监控商业建筑和住宅等最终用户建筑中的各种活动,例如空气温度、压力和品质。因此,由于降低能耗和提高能源效率的需求不断增加,HVAC 感测器得到普遍使用。

主要亮点

- 全球工业化和都市化的快速发展是推动市场成长的主要因素之一。由于世界各地各种商业建筑和住宅的建设大幅增加,作为空间供暖和製冷系统、通风控制、湿度控制和空气过滤,对 HVAC 感测器的需求大幅增加。例如,根据IEA的数据,全球建筑施工产业金额超过6.3兆美元,与前一年同期比较成长5%。

- 提高感测器与物联网 (IoT) 平台的兼容性正在成为促进远端监控和控制的先决条件。物联网连接设备为感测器在工业、医疗、消费性电子和汽车等各种应用中提供了巨大的可能性。根据思科年度网际网路报告,到2023年,连网设备数量预计将从2018年的184亿增加到约300亿。到 2023 年,物联网设备预计将占所有连网装置的 50%(147 亿),高于 2018 年的 33%(61 亿)。物联网设备的增加可能会推动所研究市场的成长。

- 商业建筑中的暖气、通风和空调通常比建筑内的任何其他活动消耗更多的能源。根据美国能源局研究,暖通空调设备通常占建筑物能源使用的 40% 以上。由于能源量庞大,HVAC系统可以利用感测器来提高设备效率,从而显着降低建筑运营成本。

- 例如,暖通空调监控系统包括物联网感测器,用于监控温度、运转率、新鲜空气摄入量和其他室内气候条件。控制器和致动器将从这些感测器收集的资料转化为行动。有些操作是立即执行的,并且已预先编程到系统中。具有机器学习功能的智慧建筑管理平台可以提供详细的见解并不断完善调整,以执行更复杂的分析。

- 此外,能源规范和建筑规范在过去十年也大大支持了节能建筑的设计。例如,主导美国绿建筑委员会(USGBC)主导的能源与环境设计(LEED)绿建筑评级体系提高了人们对建筑设计有效利用能源的必要性的认识。因此,该国多个州要求政府建筑使用 LEED 评级系统。

- 诸如此类的措施显示了建筑节能的重要性。因此,降低能耗的需求日益增长,HVAC 感测器越来越普遍用于提高能源效率。因此,政府和监管机构正在关注暖通空调控制如何减少建筑能耗。

- 这种流行病对暖通空调产业产生了重大影响,由于封锁限制和公司避免投资新设备,感测器需求在前几个月大幅下降。疫情导致世界各地许多建设计划暂停。商业、住宅和工业领域建设活动的减少暂时减少了对 HVAC 感测器(包括空气调节机)的需求。

- 此外,2020年2月至3月,由于中国等国家停产,多个产业出现供不应求。供应链中断导致原物料价格上涨,影响感测器的整体定价。

HVAC感测器市场趋势

建筑和维修活动的增加推动了市场成长

- 根据JRAIA统计,近年来全球室内空调需求量已增加至9,516万台。此外,根据联合国的数据,预计到 2022 年 11 月 15 日,世界人口将达到 80 亿。该组织的最新预测表明,2030年世界人口将达到约85亿,2050年约97亿,2100年约104亿。死亡率下降也影响着人口成长。

- 此外,在亚太地区,特别是中国和印度等新兴市场,大量人口从农村迁移到都市区,增加了政府和私人在住宅、商业建筑和基础设施方面的支出。我就是。新建筑的建设对安装暖气、通风和空调系统新设备产生了巨大的需求。因此,建设产业的成长可能会推动所研究的市场。

- 例如,2021年11月,印度政府核准在Pradhan Mantri Awas Yojana(都市区)下建造361万套住宅。新住宅单位的核准使该计划批准的住宅总数达到 11.4 亿套。这些趋势将对新安装的暖通空调系统中对暖通空调感测器的需求产生正面影响。

- 此外,政府为提高能源效率而进行的建筑维修计划数量不断增加,正在显着扩大全球暖通空调感测器市场。这是因为节能建筑有益于公众健康,因为它们可以减少温室气体排放,降低住宅和企业的能源费用,并改善室内空气品质。

- 此外,欧洲等国家也宣布了《欧洲绿色交易》,这是一项雄心勃勃的一揽子政策,旨在使欧洲在 2050 年之前成为第一个气候中和的大陆。欧洲绿色新政的目标是到 2050 年将建筑维修率提高一倍或三倍,加速建筑数位化,并使欧盟建筑存量实现脱碳。Masu。

- 因此,随着建筑和维修的增加,降低能耗的需求显着增加了对节能 HVAC 感测器的需求,以维持建筑物内舒适的室内温度和良好的空气质量,从而提高能源和效率。

亚太地区预计将录得最快成长

- 由于印度和中国的商业和住宅建设活动以及奢侈品消费者支出的增加,预计亚太地区暖通空调感测器市场将出现强劲成长。由于拥有率低和可支配收入增加,亚洲市场预计将成长。由于印度和中国的需求不断增长,住宅领域占据了亚太地区暖通空调感测器市场的很大一部分。

- 根据中国建设业协会的数据,2021年,住宅建筑在中国竣工建筑中占比最大。住宅建筑面积占竣工占地面积的67%以上。随着国家经济的成长,人们从农村地区迁移到大城市,增加了这些地区的住宅需求。此外,用作投资物业的公寓正在推动需求。如此大规模的住宅预计将推动受调查的市场。

- 而且,商业建筑的增加估计会对人们的能源消耗产生直接影响,因此中国政府正在认真考虑能源管理。两项法律为建筑能源系统以及 HVAC 和 R 行业提供了主要指导方针:《节能法案》和《可再生能源法案》。

- 该地区的公司正在开发新产品以赢得市场占有率。例如,2022年3月,Voltas推出了印度首款采用HEPA过滤技术的空调。 Voltas的PureAir 6级可调变频空调内建PM1.0空气品质感测器和AQI指示器(业界首创)可协助净化室内空气,并具有6级可调音调模式,您可以在多种音调之间切换取决于环境温度和房间内的人数。提供纯净、干净的空气,节省成本并优化能源。

- 此外,根据 RAP(监管援助计划)的数据,到 2021 年,在日本安装热泵将减少 8,100 万吨二氧化碳排放。 RAP 计算得出,中国建筑中热泵的部署每增加 1%,每年可减少 7.1 吨二氧化碳排放。目前,我国只有3.4%的建筑面积采用热泵供暖。

- 这些估计支持该地区采用高效的 HVAC 感测器。物联网 HVAC 监控系统使用感测器资料评估设备效能、识别低效率并根据各种变数提高效率,帮助建筑物更有效率地供热和冷却。制定您的自动化策略。

- 物联网设备还可以监控暖通空调系统内的元件,包括可变风量系统和风机盘管,以提高能源效率。例如,即使家中无人,运动启动空调系统也可以根据家中的运动情况打开和关闭感应器,从而节省金钱。

HVAC 感测器产业概述

HVAC 感测器市场中知名製造商的数量不断增加,而竞争公司之间的敌意预计在预测期内将会加剧。西门子股份公司、艾默生电气公司、霍尼韦尔国际公司和 TE Connectivity Ltd. 等市场老牌企业对整个市场有重大影响。市场上的公司正在采取联盟和收购等策略来加强其产品阵容并获得永续的竞争优势。

2023年3月,Sensirion宣布推出SHT40I-类比湿度感测器。此感测器适用于噪音水平高且数位解决方案无效的恶劣工业应用和恶劣环境。这种新颖的传感器由于其简单的设计和客户特定的输出特性,可以大量生产。

2022 年4 月,特灵科技(Trane Technologies PLC) 宣布将继续建立战略合作伙伴关係,利用三菱电机的Air-Fi 无线感测器进行City Multi-VRF 和Intellipak 1 HVAC 屋顶机组改进,以实现更高的能源效率。此次升级提供技术、资料和控制,帮助建筑业主满足效率标准,实现脱碳目标,并使维修变得更容易、更具成本效益。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 科技趋势

- 产业吸引力-波特五力分析

- 买方议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 价值链分析

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 建筑业的成长

- 汽车领域对暖通空调感测器的需求不断增长

- 市场限制因素

- 与运动启动空调相关的挑战

第六章市场区隔

- 按类型

- 温度感应器

- 湿度感测器

- 压力/流量感测器

- 动作感测器

- 烟雾/气体感测器

- 其他类型

- 按最终用户

- 住宅

- 商业/工业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第七章 竞争形势

- 公司简介

- Siemens AG

- Emerson Electric Co.

- Honeywell International Inc.

- Schneider Electric

- TE Connectivity Ltd.

- Sensirion AG

- Senmatic A/S

- Sensata Technologies, Inc.

- Belimo Aircontrols(USA), Inc.

- Johnsons Controls Inc.

第八章投资分析

第9章市场的未来

The HVAC Sensor Market size is estimated at USD 4.16 billion in 2024, and is expected to reach USD 5.64 billion by 2029, growing at a CAGR of 6.30% during the forecast period (2024-2029).

The HVAC sensors regulate and monitor various activities like air temperature, pressure, and quality in end-user buildings like commercial and residential buildings. Hence, HVAC sensors are being commonly used owing to the increasing need to reduce energy consumption and enhance energy efficiency.

Key Highlights

- The rapid rise in industrialization and urbanization worldwide is one of the primary factors driving the market's growth. The significant increase in the construction of different commercial and residential buildings worldwide is creating considerable demand for HVAC sensors as a space heating and cooling system, ventilation control, humidity control, and air filtration. For instance, according to the IEA, the global building construction sector's value increased by 5% compared to the previous year, reaching over USD 6.3 trillion.

- Increasing sensor compatibility with the Internet of Things (IoT) platform is gradually becoming a prerequisite for facilitating remote monitoring and control. IoT-connected devices have opened massive opportunities for sensors in several applications like industrial, medical, consumer electronics, automotive, etc. According to Cisco's Annual Internet Report, by 2023, there is expected to be nearly 30 billion network-connected device connections, up from 18.4 billion in 2018. By 2023, IoT devices were expected to make up 50% (14.7 billion) of all networked devices, up from 33% (6.1 billion) in 2018. Such an increase in IoT devices would drive the growth of the studied market.

- Heating, ventilating, and air-conditioning in a commercial building usually consume more energy than any other activity in the building. According to U.S. Department of Energy studies of commercial buildings, HVAC equipment usually accounts for over 40% of a building's energy usage. Owing to the huge amount of energy, HVAC systems use sensors to improve equipment efficiency, which results in significant reductions in building operating costs.

- For instance, HVAC monitoring systems include IoT sensors for monitoring temperature, occupancy, fresh air intake, and other indoor climate conditions. Controllers and actuators turn the data collected from these sensors into action. Some actions are immediate and preprogrammed into the system. Smart building management platforms with machine learning capabilities that provide in-depth insights and continuously refine adjustments carry out more complex analyses.

- Furthermore, energy standards and building codes have also significantly driven the design of energy efficient buildings over the past decade. For instance, the US Green Building Council's (USGBC) leadership in the Energy and Environmental Design (LEED) Green Building Rating System has raised awareness of the need for building designs that use energy efficiently. As such, several states in the country have mandated the use of the LEED rating system for government buildings.

- Such initiatives indicate the importance of energy conservation in buildings. Hence, HVAC sensors are being commonly used because the need to reduce energy consumption is increasing, enhancing energy efficiency. As a result, the government and regulatory organizations are primarily focusing on how HVAC controls can reduce energy consumption in buildings.

- The pandemic significantly influenced the HVAC industry, as demand for the sensors observed a significant drop during the initial months, owing to lockdown restrictions and businesses refraining from investing in new equipment. Due to the pandemic, many construction projects were halted across the world. The reduction in construction activities across the commercial, residential, and industrial sectors temporarily dampened the demand for HVAC sensors, including those for air handling units.

- Moreover, due to the production shutdown in countries such as China, multiple industries observed a shortage of supply of various products during February and March 2020. Due to supply chain disruption, the price of raw materials increased, impacting the overall pricing of the sensors.

HVAC Sensor Market Trends

Increased Construction and Retrofit Activity to Aid the Market's Growth

- According to JRAIA, the global demand for room air conditioners has increased to 95.16 million in recent years. Furthermore, according to the United Nations, the world's population was projected to reach 8 billion on November 15, 2022. The latest projections by the organization suggested that the global population could reach around 8.5 billion in 2030, 9.7 billion in 2050, and 10.4 billion in 2100. Declining levels of mortality partly influence population growth.

- Furthermore, in emerging markets like the Asia Pacific region, especially China and India, many people have been migrating from rural areas to cities, raising government and private spending on housing, commercial construction, and infrastructure. New building construction is creating significant demand for new equipment installations for heating, ventilation, and air conditioning systems. Hence, the growing construction industry would likely drive the studied market.

- For instance, in November 2021, the Indian government approved the construction of 3.61 lakh houses under the Pradhan Mantri Awas Yojana (Urban). The approval of the new housing units takes the total number of sanctioned houses under the scheme to 1.14 crore. Such trends positively contribute to the demand for HVAC sensors, in newly installed HVAC systems.

- Moreover, increasing building renovation projects by the government to make them more energy-efficient are significantly increasing the global HVAC sensor market. This is because energy-efficient buildings can help reduce greenhouse gas emissions, lower energy bills for homeowners and businesses, and improve indoor air quality, thus making them suitable for public health.

- Moreover, a country like Europe has presented the European Green Deal, an ambitious package of policy measures to make Europe the first climate-neutral continent by 2050. The European Green Deal aims to double or even triple building renovation rates and speed up building digitization to ensure the EU's building stock is on track to decarbonize by 2050.

- Therefore, with the growing construction and retrofit activities, there will be a significant rise in the demand for energy-efficient HVAC sensors for maintaining comfortable indoor temperatures and good air quality in buildings, owing to the need to reduce energy consumed, increasing and leading to the enhancement of energy and its efficiency.

Asia-Pacific Expected to Register Fastest Growth

- The Asia-Pacific HVAC sensor market is predicted to rise steadily due to commercial and residential construction activity in India and China and rising consumer expenditure on luxury products. Low ownership rates and increased disposable income in Asia will likely boost the market's growth. Due to rising demand from India and China, the residential sector accounted for a significant portion of the Asia-Pacific HVAC sensor market.

- According to the China Construction Industry Association, in 2021, residential structures accounted for the largest share of finished construction in China. Buildings intended for housing accounted for over 67 percent of the completed floor space. As the country's economy grows, people migrate from rural areas to major cities, increasing demand for residential accommodation in these locations. Furthermore, apartments utilized as investment properties drive up demand. Such huge residential construction is expected to drive the studied market.

- Besides, the increase in commercial buildings is estimated to affect national energy consumption directly, so the Chinese government has seriously considered energy management. Two laws, the Energy Saving Law and the Renewable Energy Law, provide the main guidelines for building energy systems and the HVAC and R industries.

- The players in the region are developing new products to capture market share. For instance, in March 2022, Voltas unveiled India's first AC with HEPA filter technology. Voltas' PureAir 6 Stage Adjustable Inverter AC is embedded with a PM 1.0 air quality sensor and AQI indicator (an industry first) that helps to purify the indoor air and is also loaded with 6 Stage Adjustable Tonnage Mode, which allows the user to switch between multiple tonnages depending on the ambient heat or number of people in the room. It provides pure and clean air, cost savings, and energy optimization.

- Further, according to RAP (Regulatory Assistance Project), heat pump installations in the country reduced CO2 emissions by 81 million metric tons in 2021. RAP calculated that with every 1% increase in heat pump uptake in China's buildings, an additional 7.1 Mt of CO2 may be avoided each year. Presently, just 3.4% of building area in China uses heat pumps for space heating, indicating a considerable possibility to grow deployment and reduce CO2 emissions countrywide.

- Such estimates encourage the adoption of efficient HVAC sensors in the region. Since IoT HVAC monitoring systems help buildings heat and cool spaces more efficiently, Sensor data can be used to evaluate equipment performance, identify inefficiencies, and create efficiency-focused automation strategies based on a range of variables.

- IoT devices can also monitor elements within an HVAC system, including variable air volume systems and fan coils, to promote energy efficiency. For instance, motion-activated air conditioning systems use sensors that turn themselves off and on based on movement in the home, saving money in the absence of anyone in the home.

HVAC Sensor Industry Overview

The increasing presence of prominent manufacturers in the HVAC sensors market is expected to intensify competitive rivalry during the forecast period. Market incumbents like Siemens AG, Emerson Electric Co., Honeywell International Inc., and TE Connectivity Ltd. considerably influence the overall market. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain a sustainable competitive advantage.

In March 2023, Sensirion announced the release of the SHT40I-Analog humidity sensor, which is intended for demanding industrial applications and severe settings where high noise levels may make digital solutions ineffective. The novel sensor allows for simple design and customer-specific output characteristics for high-volume applications.

In April 2022, Trane Technologies PLC announced a strategic continuing collaboration to achieve higher energy efficiency using Air-Fi wireless sensors for Trane and Mitsubishi Electric City multi VRF and improvements to the IntelliPak 1 HVAC Rooftop Unit. The upgrades give building owners technology, data, and controls to help them satisfy efficiency standards, achieve decarbonization targets, and make retrofits easier and more cost-effective.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technology Trends

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Buyers

- 4.3.2 Bargaining Power of Suppliers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Value Chain Analysis

- 4.5 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth in Construction Sector

- 5.1.2 Growing Demand for HVAC Sensors in the Automotive Sector

- 5.2 Market Restraints

- 5.2.1 Issues Related to Motion-Activated Air Conditioners

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Temperature Sensors

- 6.1.2 Humidity Sensors

- 6.1.3 Pressure & Flow Sensors

- 6.1.4 Motion Sensors

- 6.1.5 Smoke & Gas Sensors

- 6.1.6 Other Types

- 6.2 By End-user

- 6.2.1 Residential

- 6.2.2 Commercial & Industrial

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle-East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Siemens AG

- 7.1.2 Emerson Electric Co.

- 7.1.3 Honeywell International Inc.

- 7.1.4 Schneider Electric

- 7.1.5 TE Connectivity Ltd.

- 7.1.6 Sensirion AG

- 7.1.7 Senmatic A/S

- 7.1.8 Sensata Technologies, Inc.

- 7.1.9 Belimo Aircontrols (USA), Inc.

- 7.1.10 Johnsons Controls Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

全球智慧暖通空调系统市场:市场规模、份额、趋势分析(按技术、应用、分销管道和地区划分)、细分市场预测(2025-2033年)

全球智慧暖通空调系统市场:市场规模、份额、趋势分析(按技术、应用、分销管道和地区划分)、细分市场预测(2025-2033年) HVAC 控制市场(按产品类型、连接性、安装、最终用户和分销管道)- 全球预测 2025-2032

HVAC 控制市场(按产品类型、连接性、安装、最终用户和分销管道)- 全球预测 2025-2032 美国的HVAC控制市场:2025年

美国的HVAC控制市场:2025年 2025年暖气、通风和空调 (HVAC) 控制全球市场报告HVAC 感测器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测全球智慧家庭暖通空调控制市场

2025年暖气、通风和空调 (HVAC) 控制全球市场报告HVAC 感测器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测全球智慧家庭暖通空调控制市场 HVAC控制系统市场:2025年至2030年的预测2025年暖气、通风和空调 (HVAC) 控制系统全球市场报告直接数位控制系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

HVAC控制系统市场:2025年至2030年的预测2025年暖气、通风和空调 (HVAC) 控制系统全球市场报告直接数位控制系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 2025 年至 2033 年 HVAC 控制市场报告(按组件、实施类型、系统、最终用户和地区)

2025 年至 2033 年 HVAC 控制市场报告(按组件、实施类型、系统、最终用户和地区)