|

市场调查报告书

商品编码

1432524

饱和聚酯树脂:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Saturated Polyester Resins - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

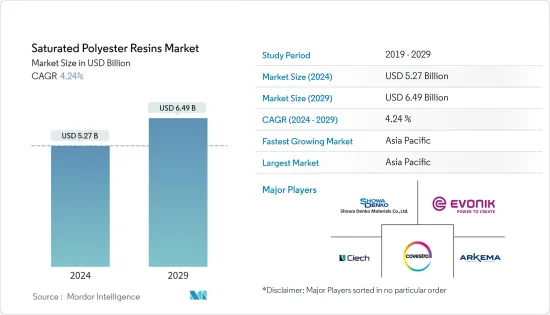

饱和聚酯树脂市场规模预计到2024年为52.7亿美元,预计到2029年将达到64.9亿美元,在预测期内(2024-2029年)复合年增长率为4.24%。

在 COVID-19 大流行期间,由于全球营运和供应链限制,饱和聚酯树脂市场出现低迷。这些因素对油漆和涂料行业等主要最终用户的需求产生了负面影响。然而,一旦2021年限制放鬆,聚酯树脂的需求就会上升到疫情前的水平。

主要亮点

- 中期推动市场成长的主要因素是由于卓越的机械性能,与替代品相比具有卓越的性能。

- 另一方面,饱和聚酯树脂的高加工和製造成本预计将阻碍市场成长。

- 非 BPA 罐头涂料的趋势正在为饱和聚酯树脂创造新的成长机会。

- 亚太地区在市场中占据主导地位,预计在预测期内仍将保持最高的复合年增长率。

饱和聚酯树脂市场趋势

粉末涂料需求增加

- 饱和聚酯树脂主要用于生产无溶剂粉末油漆和被覆剂。饱和聚酯树脂具有良好的耐候性、良好的衝击强度和对金属的黏合(即使在潮湿条件下)等优异性能,用于室外和室内建筑应用、机械、电器产品、钢铁、家具和花园的涂漆首选工具。

- 在全球范围内,电子产业的技术进步和研发活动的快速创新正在推动对更新、更快、更可靠的电子产品的需求,从而增加了对涂层元件的需求。

- 根据日本电子情报技术产业协会(JEITA)预测,全球电子资讯科技产业产值将从2021年的3.36兆美元成长到2022年,与前一年同期比较成长1%。4,400亿。此外,2023年预计与前一年同期比较增长3%。根据消费者科技协会的数据,2022 年美国消费性电子产品或科技的零售额预计将达到 5,050 亿美元,而 2021 年为 4,610 亿美元。

- 在欧洲,德国的电子工业是该地区最大的。根据 ZVEI 的数据,2022 年 11 月德国电子和数位产业销售额达 211 亿欧元(217 亿美元),较 2021 年 11 月成长 14.4%。

- 同样,不断增长的建筑业预计将推动使用饱和聚酯树脂生产的无溶剂粉末涂料的使用。这将推动预测期内受调查市场的成长。

- 亚太地区、中东和非洲的建筑业正在经历强劲成长。在中东和非洲地区,各国政府正努力发展非石油部门。例如,沙乌地阿拉伯政府根据其经济转型计画「2030 年愿景」启动了一系列基础设施计划。这些计划主要涉及电力、水利、碳氢化合物、建筑、公路、铁路、港口和机场领域。

- 因此,各终端用户产业对粉末涂料的需求正在稳步增长,预计将带动对饱和聚酯树脂的需求。

亚太地区主导市场

- 由于中国、印度和日本等经济体的需求不断增长,亚太地区在全球市场份额中占据主导地位。

- 预计在预测期内,亚太地区对饱和聚酯树脂的需求将健康成长。这是由于该地区建筑、汽车和电子行业的油漆和涂料应用预计将显着增长。

- 据国家发展委员会 (NDC) 称,2022 年 2 月,中国政府机构提案了1,800 亿元新台币(64.7 亿美元)的基础设施发展计画。该计划包括前瞻性基础设施发展计划第四阶段的预算提案,将于 2023 年至 2024 年使用。

- 在中国,2021年住宅在已竣工开发案中所占比例最大。住宅建筑面积占竣工占地面积的67%以上。随着经济成长,越来越多的人从农村地区迁移到都市区,增加了对住宅的需求。此外,中国拥有全球最大的建筑市场,占全球整体建筑投资的20%。预计到2030年,中国将在建筑方面花费约13兆美元,使得全球饱和聚酯树脂市场前景乐观。

- 亚太地区是世界上一些最有价值的汽车製造商的所在地。它的总部位于中国、印度、日本和韩国等新兴国家。基于饱和聚酯树脂的油漆和被覆剂由于其对金属表面的高黏合而越来越多地用于汽车工业。

- 根据中国工业协会统计,中国是全球最大的汽车生产基地,预计2022年汽车产量将达到2,700万辆,比去年的2,600万辆成长3.4%。此外,2022年前7个月,中国生产汽车1,457万辆,与前一年同期比较成长31.5%。此外,2022年7月电池式电动车保有量较2021年1-7月成长117.2%。预计 2022 年 7 月该国电动车销量约为 61.7 万辆。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 包装产业需求增加

- 亚太和中东欧快速工业化

- 其他司机

- 抑制因素

- 加工製造成本高

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(以金额为准的市场规模)

- 种类

- 液体饱和聚酯树脂

- 固态饱和树脂

- 目的

- 粉末涂料

- 卷材和罐头涂料

- 汽车漆

- 包装涂料

- 工业漆

- 其他用途

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲

- 亚太地区

第六章 竞争形势

- 併购、合资、联盟、协议

- 市场占有率(%)/排名分析

- 主要企业策略

- 公司简介

- ALLNEX GMBH

- Arkema Group

- CIECH SA

- Covestro AG

- DIC CORPORATION

- Eternal Materials Co. Ltd

- Evonik Industries AG

- Showa Denko Materials Co. Ltd

- Hitech Industries FZE

- Hexion

- Novaresine SRL

- DSM

- Sir Industriale

- Stepan Company

- Nippon Gohsei

第七章 市场机会及未来趋势

- 由于挥发性有机化合物排放低,饱和聚酯树脂的使用增加

- 其他机会

The Saturated Polyester Resins Market size is estimated at USD 5.27 billion in 2024, and is expected to reach USD 6.49 billion by 2029, growing at a CAGR of 4.24% during the forecast period (2024-2029).

During the COVID-19 pandemic, the saturated polyester resin market witnessed a downturn due to operational and supply chain restrictions in various countries across the globe. Factors like these negatively impacted the demand from key end users like Paints and Coatings industry, among others. However, as the restriction eased in 2021, the demand for polyester resin rose to pre-pandemic levels.

Key Highlights

- Over the medium term, the major factor driving the market's growth is their better performance compared to their alternatives because of their superior mechanical properties.

- On the flip side, the high processing and manufacturing cost of saturated polyester resins is expected to hinder the studied market's growth.

- The growing trend of non-BPA can coatings creates new growth opportunities for saturated polyester resins.

- The Asia-Pacific region is expected to dominate the market and will likely witness the highest CAGR during the forecast period.

Saturated Polyester Resins Market Trends

Increasing Demand for Powder Coatings

- Saturated polyester resins are primarily used to manufacture solvent-free powder paints and coatings. Its superior properties, such as good weather resistivity, excellent impact strength, and adhesion to metals (even under humid conditions), saturated polyester resins are favored for exterior and interior architectural applications, coating machinery, domestic appliances, steel furniture, and garden tools.

- Globally the rapid pace of innovation in terms of the advancement of technologies and R&D activities in the electronics industry is driving the demand for newer, faster, and more reliable electronic products, thus increasing the need for coated components.

- According to the Japan Electronics and Information Technology Industries Association (JEITA), the production by the global electronics and IT industry was estimated at USD 3.44 trillion in 2022, registering a growth rate of 1% year on year, compared to USD 3.36 trillion in 2021. Moreover, the industry is expected to grow by 3% year on year by 2023. According to the Consumer Technology Association, the retail revenue from consumer electronics or technology sales in the United States was estimated at USD 505 billion in 2022, compared to USD 461 billion in 2021.

- In Europe, the German electronics industry is the largest in the region. According to the ZVEI, Germany's electro and digital industry turnover accounted for EUR 21.1 billion (USD 21.7 billion) in November 2022, witnessing a growth rate of 14.4% compared to November 2021.

- Similarly, the growing construction sector is expected to drive the usage of solvent-free powder coatings manufactured using saturated polyester resins. It is thereby boosting the growth of the market studied during the forecast period.

- The construction sector is witnessing robust growth in Asia-Pacific, Middle East & Africa. In the Middle East & Africa region, governments are trying to develop the non-oil sectors. For Instance, Under the Vision 2030 economic transformation plan, the Saudi Arabian government initiated numerous infrastructure projects. These projects majorly cover projects related to the power, water, hydrocarbons, construction, road, rail, seaport, and airport sectors.

- Hence, the robust growth in the demand for powder coatings from various end-user industries is expected to drive the demand for saturated polyester resins.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the global market in terms of share, owing to the growing demand from economies like China, India, and Japan.

- Asia-Pacific is expected to witness healthy growth in the demand for saturated polyester resins during the forecast period. It is due to the expected noticeable growth of paints and coatings applications in industries like construction, automotive, and electronics industries, among others in the region.

- In February 2022, the Chinese government agencies proposed a TWD 180 billion (USD 6.47 billion) infrastructure development plan, according to the National Development Council (NDC). It includes the proposed budget for the fourth stage of the Forward-looking Infrastructure Development Program would be used from 2023-2024.

- In China, residential buildings comprised the largest portion of finished development in 2021. Construction intended for housing accounted for over 67% of the completed floor space. As the economy grows, more people move from rural to urban regions, increasing the need for residential accommodation. In addition, the country includes the largest construction market in the world, encompassing 20% of all construction investments globally. China is expected to spend nearly USD 13 trillion on buildings by 2030, creating a positive market outlook for the global saturated polyester resins market.

- The Asia-Pacific region is home to some of the world's most valuable vehicle manufacturers. Developing countries such as China, India, Japan, South Korea. As paints and coatings based on saturated polyester resins offer high adhesion to metallic surfaces, These are increasingly used in the automotive industry.

- According to the China Association of Automobile Manufacturers (CAAM), China contains the largest automotive production base in the world, with a total vehicle production of 27 million units in 2022, registering an increase of 3.4 % compared to 26 million units produced last year. Further, in the first 7 months of 2022, the country produced 14.57 million units of cars, registering a growth rate of 31.5% Year on Year. Furthermore, in July 2022, the number of battery-powered electric vehicles increased by 117.2% compared to January-July in 2021. In July 2022, the country's electric vehicle sales were estimated at around 617 thousand units.

- Moreover, in India, during FY 2021-22 (April 2021 to March 2022), according to the Society of Indian Automobile Manufacturers (SIAM), the country's automotive industry produced a total of 22.03 million vehicles compared to 22.66 million units during April 2020 to March 2021. Further, according to the Centre for Monitoring Indian Economy (CMIE), car production increased to 193.63 thousand units in July 2022 from 169.52 thousand units in June 2022. Such factors are likely to increase the demand for the studied market

- The factors above are expected to drive the demand for saturated polyester resins in the region during the forecast period.

Saturated Polyester Resins Industry Overview

The saturated polyester resins market is partially fragmented, with the top players accounting for a small chunk of the market. These major players include Arkema Group, Covestro AG, Showa Denko Materials Co. Ltd, Evonik Industries AG, and CIECH SA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Packaging Industry

- 4.1.2 Rapid Industrialization in Asia-Pacific and Central and Eastern Europe

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Processing and Manufacturing Cost

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Liquid Saturated Polyester Resin

- 5.1.2 Solid Saturated Resin

- 5.2 Application

- 5.2.1 Powder Coatings

- 5.2.2 Coil and Can Coatings

- 5.2.3 Automotive Paints

- 5.2.4 Packaging

- 5.2.5 Industrial Paints

- 5.2.6 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ALLNEX GMBH

- 6.4.2 Arkema Group

- 6.4.3 CIECH SA

- 6.4.4 Covestro AG

- 6.4.5 DIC CORPORATION

- 6.4.6 Eternal Materials Co. Ltd

- 6.4.7 Evonik Industries AG

- 6.4.8 Showa Denko Materials Co. Ltd

- 6.4.9 Hitech Industries FZE

- 6.4.10 Hexion

- 6.4.11 Novaresine SRL

- 6.4.12 DSM

- 6.4.13 Sir Industriale

- 6.4.14 Stepan Company

- 6.4.15 Nippon Gohsei

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Usage of Saturated Polyester Resins Due to Low VOC Emissions

- 7.2 Other Opportunities

不饱和聚酯树脂市场规模、份额、成长分析、类型、最终用途产业、地区 - 产业预测,2024-2031

不饱和聚酯树脂市场规模、份额、成长分析、类型、最终用途产业、地区 - 产业预测,2024-2031 饱和聚酯树脂市场:2025-2030 年预测

饱和聚酯树脂市场:2025-2030 年预测 不饱和聚酯树脂市场:按类型、最终用途划分 - 2025-2030 年全球预测

不饱和聚酯树脂市场:按类型、最终用途划分 - 2025-2030 年全球预测 按类型、应用、国家和地区分類的粉末聚酯树脂市场:2024 年至 2032 年行业分析、市场规模、市场份额和预测

按类型、应用、国家和地区分類的粉末聚酯树脂市场:2024 年至 2032 年行业分析、市场规模、市场份额和预测 不饱和聚酯树脂市场:按类型、最终用途产业、地区划分 - 2029 年预测

不饱和聚酯树脂市场:按类型、最终用途产业、地区划分 - 2029 年预测 饱和聚酯树脂市场规模、份额、趋势分析报告:依材料、最终用途、地区、细分市场预测,2024-2030年

饱和聚酯树脂市场规模、份额、趋势分析报告:依材料、最终用途、地区、细分市场预测,2024-2030年 不饱和聚酯树脂市场:依产品类型、最终用途产业、地区

不饱和聚酯树脂市场:依产品类型、最终用途产业、地区 2024-2032 年不饱和聚酯树脂市场报告(按类型(邻苯二甲酸树脂、间苯二甲酸树脂、双环戊二烯树脂等)、最终用途、形式和地区)

2024-2032 年不饱和聚酯树脂市场报告(按类型(邻苯二甲酸树脂、间苯二甲酸树脂、双环戊二烯树脂等)、最终用途、形式和地区) 2024-2028年全球不饱和聚酯树脂市场

2024-2028年全球不饱和聚酯树脂市场 不饱和聚酯树脂(UPR)的全球市场(2016年~2032年)

不饱和聚酯树脂(UPR)的全球市场(2016年~2032年)