|

市场调查报告书

商品编码

1432581

软包装:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Flexible Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

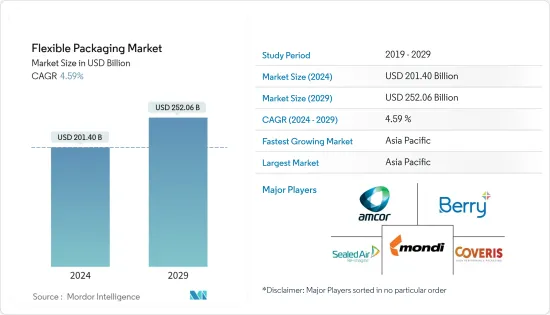

软包装市场规模预计到2024年为2014亿美元,预计到2029年将达到2520.6亿美元,在预测期内(2024-2029年)复合年增长率为4.59%。

由于显着的能源和环境效益,包装产业正在转向采用软包装解决方案。

主要亮点

- 此外,人们对软包装中生物分解性聚合物的使用及其对环境的影响越来越关注,这促使製造商提供安全、可靠和环保的包装。製造商在生产过程中使用更少的资源和能源,匹配最终用户的产品和品牌名称,更少的运输支出,更长的产品保质期,减轻成本压力,并改进产品包装。我们继续专注于提供永续的包装选择,以保护正直。

- 多种最终用途对软包装的需求不断增长。这包括电子商务、数位印刷和永续性趋势,这些趋势正在推动市场的开拓和成长。客户越来越愿意为软包装增强的某些产品属性支付额外费用。消费者愿意为采用永续包装的产品支付更多费用,这将有助于产业吸收因转向永续包装而增加的成本。

- 食品企业对肉类、家禽和鱼贝类的软包装的选择受到便利性以外的因素的影响,例如永续性、透明度、食品安全和减少食品废弃物。永续性是企业对使用可回收和再生材料的软包装解决方案越来越感兴趣的原因之一。这方面的解决方案不断涌现,其中包括可塑纸,它具有优异的阻隔性,适用于份量包装和午餐肉,并且根据行业估计,可以减少高达 80% 的塑胶使用量。

- 世界上许多公司都倾向于借助单一材料来製造基于 PE 的包装。例如,2022 年 8 月,Mondi 和汉高透过开发全新的可重复使用包装概念,帮助消费者更环保地洗碗。两家公司合作开发了适用于汉高手洗餐具解决方案的包装解决方案,实现从软袋到宝特瓶的再填充。此次合作将有助于汉高实现其永续发展目标,即在 2025 年实现 100% 可回收或可重复使用包装以及将由石化燃料製成的原生塑胶减少 50%。替代硬质宝特瓶时,柔性立式袋可减少 70% 的塑胶用量,而且在拥有成熟回收基础设施的地区也易于回收。

- 此外,AR Packaging 于 2021 年 7 月推出了 Ecoflex,这是一种热成型单聚乙烯薄膜,100% 可回收,提供比 PA 材料更环保的选择,同时完全符合 OPRL 标准。推出 Ecoflex,零售商现在可以选择永续材料。 Ecoflex 提供可比较的机械强度和衝击强度,可作为柔性热成型应用中 PA/PE 材料的替代品。例如,在英国,回收设施可以在商店回收柔性聚烯包装。

- 大多数回收设施都已经过时,因此效率低下,无法跟上不断变化的废弃物流。例如,目前的设备不足以跟上包装废弃物的变化趋势,即使纸张废物量减少且塑胶废物量增加。

- 软包装製造商越来越担心通膨。人事费用、能源和运输成本造就了一个营运成本高且竞争激烈的产业。原物料价格进一步上涨受到俄乌危机、俄罗斯制裁以及东西方地缘政治领域重新布局的影响。

- 最近的 COVID-19 疫情为软包装製造商带来了许多问题,包括非製药应用的需求下降,而且这些问题可能会持续一段时间。供应链中断、製造原材料短缺、劳动力短缺、可能推高生产成本并超出预算的价格波动以及出货问题只是封锁造成的一些后果。随着封锁放鬆和解除,市场开始復苏,COVID-19 的影响现已开始消退。

软包装市场趋势

乳製品预计将在食品领域占据较大市场占有率

- 当前的市场状况表明,随着乳製品消费的健康成长,乳製品的需求激增。例如,根据美国农业部 (USDA) 的数据,欧洲的人均起司消费量最高。 2021年欧盟(EU)平均起司消费量为20.44公斤。美国和加拿大同年分居第二和第三位,人均起司消费量分别约为17.9公斤和15公斤。 2021年,欧盟(EU)27个国家生产了1,035万吨乳酪,大约是第二大生产国的两倍。

- 牛奶是主要的乳製品食品,是均衡饮食的重要组成部分,富含钙和其他重要营养素。根据联合国粮食及农业组织及美国农业部统计,印度2021年的牛奶消费量量约8,300万吨,是全球最大的消费国。第二大国家是欧盟 (EU),拥有 2,390 万吨。软包装袋是迄今为止最受欢迎的牛奶包装类型,其次是无菌包装,且使用量正在上升。软包装袋已成为快速、廉价且安全的包装选择。由于国内分销网络广泛,这种包装类型易于包装和处理。消费者对奶袋的正面反应鼓励了新技术的采用。

- 液体盒包装传统上与牛奶联繫在一起,因为它可以保护食品并且有利于环境。纸板是一种经常用于製作牛奶包装液体盒的材料。牛奶纸盒,也称为山形盖顶纸盒,是一种由聚乙烯涂层纸製成的型态。以重量计算,牛奶盒的材质为 80% 纸张和 20% 聚乙烯。 20 世纪 50 年代,纸盒牛奶取代了可再填充的玻璃瓶,为消费者提供了方便、轻巧的替代品。

- 许多起司品牌和生产商已经采用软包装来提供价值和便利。软包装透过紧密的供应链为产品提供强度和保护,但可能会损坏其他包装类型并导致不良结果。

- 例如,GOOD PLANeT Foods 于 2022 年 4 月重新设计了其全系列植物性乳酪,预计 2022 年将大幅成长,并且近期扩大了在超级市场的分销,Sprouts 也增加了全国范围内的分销。 GOOD PLANeT 为该产品选择了 Bellmark 的可回收软包装袋,以增强配方和包装。

- 具有中等阻隔性(PA/PE)或阻隔性(PA/EVOH/PE)的真空袋被广泛接受。这些以薄膜为基础的真空袋被纳入调气包装(MAP) 应用中,主要用于乳製品和蛋白质包装。

亚太地区预计将出现显着成长

- 在食品业,不仅是便利性,永续性、透明度、食品安全和减少食品废弃物等其他特性也在影响肉类、家禽和鱼贝类软包装的选择。根据中国工业与资讯化部、国家统计局统计,2021年,中国食品工业获利约6,187亿元。

- 根据厚生劳动省的数据,截至 2021 年 9 月,学名药在日本伦理药品市场的销售份额约为 79%。根据联合国COMTRADE国际贸易资料库,2021年日本将进口372.9亿美元的药品。随着日本人口迅速老化,需要治疗相关疾病的新药,这项需求预计将会增加。因此,这些趋势预计将对市场成长产生正面影响。

- 根据美国农业部对外农业局统计,2021年印度包装食品市场乳製品销售达2,381万吨。这比 2017 年的约 1,974 万吨大幅增加。印度食品零售的扩张和多元化预计将成为乳製品包装食品的催化剂,其中都市区占销售额的75%以上。

- 印度品牌股权基金会的报告显示,印度政府最近在FMCG(快速消费品)领域进行了良好的投资和支持。 2000年4月至2022年3月,快消品产业吸收FDI健康流入201.1亿美元。此外,2022-23 年联邦预算向消费者事务局拨款 2.2219 亿美元,向食品和公共分配部拨款 278.2 亿美元。增加对分销的投资可以提高全部区域进出口中永续包装的采用。

软包装产业概况

由于少数占据重要市场占有率的供应商,软包装市场得到适度整合。市场似乎有些集中,主要企业采取产品创新、併购等策略来保持竞争力。该行业的主要企业包括 Amcor PLC、Mondi Group、Berry Global Inc 和 Sealed Air Corporation。

- 2022 年 4 月 - Mondi 与法国机械製造商 Thimonnier 合作开发可回收包装,以减少塑胶废弃物。两家公司开发了一种可以完全清空的新型液体填充用包装。共挤聚乙烯是一种单一可回收材料,用于生产 Barlingo小袋。与硬质塑胶瓶相比,该产品重量更轻,塑胶用量减少 75% 以上。此再填充解决方案可取代目前业界标准但不可回收的多层 PVC 再填充容器。

- 2021 年 10 月 - Berry World 和利安德巴塞尔联手推进到 2026 年 100%永续采购客户包装的目标。此次合作将帮助更多消费者从可回收的塑胶内衬基板中选择可回收的透明塑胶饮水杯。

- 2021 年 6 月 - Coveris 凭藉其技术力开发了一种新的串行班轮解决方案。 Cereal+ 内衬的开发旨在提高包装机性能并延长保质期。 Coveris 的 Cereal+ 内衬由完全可回收的聚乙烯製成,为盒中袋薄膜包装的谷物和干食品提供产品保护、新鲜度和保质期。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 产业吸引力-波特五力分析

- 买方议价能力

- 供应商的议价能力

- 替代品的威胁

- 新进入者的威胁

- 竞争公司之间的敌对关係

- 产业价值链分析

- 评估 COVID-19 对产业的影响

- 市场驱动因素

- 对便捷包装的需求不断增长

- 长期储存的需求和生活方式的改变

- 市场限制因素

- 环境和回收问题

第五章市场区隔

- 材料种类

- 塑胶

- 聚乙烯(PE)

- 双轴延伸聚丙烯(BOPP)

- 流延聚丙烯 (CPP)

- 聚氯乙烯(PVC)

- 乙烯 - 乙烯醇(EVOH)

- 纸

- 铝箔

- 塑胶

- 产品类别

- 小袋

- 包包

- 薄膜和包装

- 其他产品类型

- 最终用户产业

- 食品

- 冷冻食品

- 乳製品

- 水果和蔬菜

- 肉类、家禽、鱼贝类

- 烘焙点心/零嘴零食

- 糖果/糖果零食

- 其他食品

- 饮料

- 药品和医疗用品

- 家居用品/个人护理

- 其他最终用户产业

- 食品

- 地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 土耳其

- 波兰

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 其他亚太地区

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 其他拉丁美洲

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 埃及

- 伊朗

- 奈及利亚

- 其他中东和非洲

- 北美洲

第六章 竞争形势

- 公司简介

- Amcor Plc

- Berry Global Inc.

- Mondi Group

- Sealed Air Corporation

- Coveris Holdings SA

- UFlex Limited

- Huhtamaki Group

- Proampac LLC

- WIPF Doypak(Wipf AG)

- FlexPak Services LLC

- Laser Packaging Manufacturing PTE Limited

- KM Packaging Services Ltd

- Sonoco Products Company

第七章 投资分析

第八章 市场机会及未来趋势

The Flexible Packaging Market size is estimated at USD 201.40 billion in 2024, and is expected to reach USD 252.06 billion by 2029, growing at a CAGR of 4.59% during the forecast period (2024-2029).

The packaging industry has been shifting toward adopting flexible packaging solutions owing to its considerable energy and environmental benefits.

Key Highlights

- Additionally, manufacturers have been prompted to provide environmentally friendly packaging choices that are safe and secure, owing to growing worries about the usage of biodegradable polymers for flexible packaging and its effects on the environment. Manufacturers continue to look toward providing sustainable packaging options that use fewer resources and energy during production, fit with the product and brand name of the end-user, need less money for transportation, and provide products with a longer shelf life to ease cost pressure and preserve the integrity of product packages.

- The demand for flexible packaging is growing across multiple end-use applications. It includes e-commerce, digital printing, and sustainability trends, which can drive market development and growth. Customers are increasingly eager to pay extra for specific product attributes boosted by flexible packaging. Consumers' willingness to pay more for products with sustainable packaging could help the industry absorb the increased costs of switching to sustainable packaging.

- The choice of flexible packaging for meat, poultry, and seafood in the food business is influenced by factors beyond convenience, such as sustainability, transparency, food safety, and a reduction in food waste. Companies are becoming increaslngly interested in flexible packaging solutions that uses recyclable and recycled content for obvious reasons, one of which is sustainability. Solutions, including formable paper, which offers good barrier qualities, is suited for portion packs and lunchmeat, and according to some industry estimates it reduces plastic use by up to 80%, are gaining ground in this regard.

- Many companies worldwide are following a trend of building PE-based packages with the help of mono materials. For instance, in August 2022, Mondi and Henkel assisted consumers in more environmentally friendly dishwashing by developing an entirely new reusable packaging idea. The two businesses collaborated on a packaging solution for Henkel's hand dishwashing solutions in allowing the refilling of plastic bottles from flexible pouches. The collaboration helps Henkel achieve its sustainability goals of 100% recyclable or reusable packaging by 2025 and a 50% decrease in virgin plastic made from fossil fuels. When rigid plastic bottles are replaced, the flexible stand-up pouch eliminates plastic by 70% and is simple to recycle in areas with established recycling infrastructure.

- Furthermore, in July 2021, Ecoflex, a thermoforming mono polyethylene film that is 100% recyclable and offers a greener option to PA-based materials while completely adhering to OPRL criteria, was launched by the AR Packaging. Retailers now have a sustainable material of choice with the introduction of Ecoflex. Ecoflex provides comparable mechanical and impact strength for its flexible thermoformed applications instead of PA/PE material. For instance, recycling facilities can recycle flexible polyolefin packaging at the front-of-store in the United Kingdom.

- Most recycling facilities are inefficient in handling changes in waste streams because they are outdated. The current device, for instance, is inadequate to address such shifts in packaging waste trends, even while the amount of paper trash has declined and the amount of plastic waste has increased.

- Manufacturers of flexible packaging are getting increasingly concerned about inflation. Labor, energy and transportation costs have created a competitive industry with high operational expenses. Additional raw material price hikes are influenced by the crisis between Russia and Ukraine, Russian sanctions, and the realignment of western and eastern countries in the geopolitical arena.

- The recent COVID-19 outbreak has caused many problems for flexible packaging makers, including demand decline in the sectors that were not relted to pharmaceutical applications, although these are only likely to last for a short while. Supply chain interruptions, a lack of raw materials for manufacture, workforce shortages, pricing fluctuations that could drive up production costs and push them beyond budget, and shipping issues are just a few consequences of a lockdown. The COVID-19 impact has now started to wear-off with market recovering post easing and lifting of lockdown.

Flexible Packaging Market Trends

Dairy Products are Expected to Hold a Significant Market Share in the Food Segment

- The current market scenario indicates an upsurge in demand for dairy products, as the consumption of dairy products is increasing at a healthy rate. For instance, according to the United States Department of Agriculture (USDA), cheese consumption per capita is the highest in Europe. The average cheese consumed in the European Union in 2021 was 20.44 kilos. With around 17.9 and 15 kg of cheese per person, the United States and Canada placed second and third in the year. In 2021, the 27 countries that make up the European Union produced 10.35 million metric tonnes of cheese, nearly twice as much as the second-largest producer.

- Among all dairy products, milk is a primary staple food and an essential part of a balanced diet containing a high percentage of calcium and other vital nutrients. According to the FAO (Food and Agriculture Organization of the United Nations) and the US department of agriculture, India consumed roughly 83 million metric tonnes of cow milk in 2021, the world's largest. With 23.9 million metric tons, the European Union utilized the next-highest amount of milk. Flexible pouches, which predominate in total milk packaging, are followed by aseptic packaging, whose use is on the rise. Flexible pouches have established themselves as a rapid, inexpensive, and secure packing option. The packaging type is also simple to package and handle due to the nation's vast distribution network. The positive consumer reaction to milk pouches made the adoption of new technology.

- Liquidbox packaging has conventionally been associated with milk, as it protects food and is also good for the environment. Paperboard is a frequently used material for making liquidbox for milk packaging. Also known as gable-top cartons, milk cartons is a common form of poly-coated paper packaging. By weight, milk cartons are 80% paper and 20% polyethylene. Paper milk cartons substituted refillable glass bottles in the 1950s, offering consumers a convenient, lightweight alternative.

- Numerous cheese brands and producers have already adopted flexible packaging to provide value and convenience. Flexible packaging delivers strength and protection for the product throughout the demanding supply chain, which can damage other packaging types and lead to poor outcomes.

- For instance, GOOD PLANeT Foods redesigned its whole range of plant-based cheeses in April 2022 in anticipation of a significant growth prediction in 2022, with recent distribution gains at supermarkets like Giant Martin, Giant Eagle, and Hy-Vee, as well as increasing distribution nationally in Sprouts. GOOD PLANeT chose Belmark's recyclable flexible pouches for the product to enhance formulation and packaging.

- Vacuum pouches with moderate (PA/PE) or high barrier (PA/EVOH/PE) properties have gained widespread acceptance. These film-based vacuum pouches are incorporated in Modified Atmosphere Packaging (MAP) applications and utilized mainly for dairy and protein packaging.

Asia Pacific is Expected to Witness Significant Growth

- In the food industry, beyond convenience, other characteristics, such as sustainability, transparency, food safety, and reduction in food waste, influence the flexible packaging choice for meat, poultry, and seafood. According to the Ministry of Industry and Information Technology and the National Bureau of Statistics of China, in 2021, the food industry in the country generated total profits of around CNY 618.7 billion.

- According to the Ministry of Health, Labor and Welfare (MHLW Japan), the volume share of generics in the Japanese prescription drugs market stood at around 79% as of September 2021. According to the United Nations COMTRADE database on international trade, Japan imported pharmaceutical products worth USD 37.29 billion in 2021. This demand is anticipated to increase as the country's rapidly aging population demands new medicines for associated conditions. Hence, such trends are expected to positively contribute to the market's growth.

- According to the USDA Foreign Agricultural Service, the sales volume of dairy food in the Indian packaged foods market amounted to 23.81 million metric tons in 2021. A significant increase from about 19.74 million metric tons in 2017 was recorded. India's food retail expansion and diversification are expected to act as catalysts for dairy packaged foods, with urban areas accounting for more than 75% of the sales.

- The government of India has recently provided the Fast Moving Consumer Goods (FMCG) sector with good investments and support, according to India Brand Equity Foundation reports. From April 2000 to March 2022, the industry saw healthy FDI inflows of USD 20.11 billion. Additionally, the Department of Consumer Affairs has been allocated USD 222.19 million, while the Department of Food and Public Distribution has been allocated USD 27.82 billion under the Union Budget 2022-23. The increased investments in distribution could improve sustainable packaging adoption for imports and exports across the region.

Flexible Packaging Industry Overview

The Flexible Packaging Market is moderately consolidated owing to the presence of a few vendors in the market with significant market share. The market appears to be slightly concentrated, with the major players adopting strategies such as product innovation, mergers, and acquisitions to stay competitive. Some of the major players in the industry are Amcor PLC, Mondi Group, Berry Global Inc, and Sealed Air Corporation, among others.

- April 2022 - Mondi teamed up with French machine producer Thimonnier to create a recyclable package that cuts down on plastic waste. The businesses have developed new liquid refill packaging that can be completely emptied. Coextruded polyethylene, a recyclable mono-material, is used to make the berlingot sachet. Compared to rigid plastic bottles, the product weighs less and employs more than 75% less plastic. The refill solution can replace the multilayer PVC refill containers, which are currently the industry standard but aren't recyclable.

- October 2021 - Berry Global and LyondellBasell collaborated to advance the goal of sourcing 100% of its customer-facing packaging sustainably by 2026. The collaboration supports the selection of plastic-lined paper cups with limited recyclability to single-substrate, clear plastic drink cups that more consumers will be able to recycle.

- June 2021 -Coveris, with its technical capabilities, developed a new cereal liner solution. The Cereal+ liner has been created to deliver packer performance and improved shelf life. Coveris Cereal+ liner is made from fully recyclable polyethylene and provides product protection, freshness, and shelf life for cereals and dry foods packed in bag-in-box films.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of Substitutes

- 4.2.4 Threat of New Entrants

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Industry

- 4.5 Market Drivers

- 4.5.1 Increased Demand for Convenient Packaging

- 4.5.2 Demand for Longer Shelf Life and Changing Lifestyles

- 4.6 Market Restraints

- 4.6.1 Concerns Regarding the Environment and Recycling

5 MARKET SEGMENTATION

- 5.1 Material Type

- 5.1.1 Plastic

- 5.1.1.1 Polyethene (PE)

- 5.1.1.2 Bi-orientated Polypropylene (BOPP)

- 5.1.1.3 Cast polypropylene (CPP)

- 5.1.1.4 Polyvinyl Chloride (PVC)

- 5.1.1.5 Ethylene Vinyl Alcohol (EVOH)

- 5.1.2 Paper

- 5.1.3 Aluminum Foil

- 5.1.1 Plastic

- 5.2 Product Type

- 5.2.1 Pouches

- 5.2.2 Bags

- 5.2.3 Films & Wraps

- 5.2.4 Other Product Types

- 5.3 End-User Industry

- 5.3.1 Food

- 5.3.1.1 Frozen Food

- 5.3.1.2 Dairy Products

- 5.3.1.3 Fruits and Vegetables

- 5.3.1.4 Meat, Poultry, and Seafood

- 5.3.1.5 Baked Goods and Snack Foods

- 5.3.1.6 Candy and Confections

- 5.3.1.7 Other Food Products

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Medical

- 5.3.4 Household and Personal Care

- 5.3.5 Other End-User Industries

- 5.3.1 Food

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Turkey

- 5.4.2.7 Poland

- 5.4.2.8 Russia

- 5.4.2.9 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Mexico

- 5.4.4.4 Rest of Latin America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Egypt

- 5.4.5.4 Iran

- 5.4.5.5 Nigeria

- 5.4.5.6 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Amcor Plc

- 6.1.2 Berry Global Inc.

- 6.1.3 Mondi Group

- 6.1.4 Sealed Air Corporation

- 6.1.5 Coveris Holdings SA

- 6.1.6 UFlex Limited

- 6.1.7 Huhtamaki Group

- 6.1.8 Proampac LLC

- 6.1.9 WIPF Doypak (Wipf AG)

- 6.1.10 FlexPak Services LLC

- 6.1.11 Laser Packaging Manufacturing PTE Limited

- 6.1.12 KM Packaging Services Ltd

- 6.1.13 Sonoco Products Company

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

软包装市场:按产品、材料和最终用户划分 - 2024-2030 年全球预测

软包装市场:按产品、材料和最终用户划分 - 2024-2030 年全球预测 2024-2032 年按材料类型、包装类型、应用、最终用途产业和地区分類的金属化软包装市场

2024-2032 年按材料类型、包装类型、应用、最终用途产业和地区分類的金属化软包装市场 全球软包装市场规模、份额、成长分析(按类型、最终用户)- 产业预测,2024-2031 年

全球软包装市场规模、份额、成长分析(按类型、最终用户)- 产业预测,2024-2031 年 2024-2032 年按产品类型、原料、印刷技术、应用和地区分類的软包装市场报告

2024-2032 年按产品类型、原料、印刷技术、应用和地区分類的软包装市场报告 2024 年金属软质包装全球市场报告

2024 年金属软质包装全球市场报告 到 2030 年金属化软包装市场预测:按产品类型、材料类型、技术、最终用户和地区进行的全球分析

到 2030 年金属化软包装市场预测:按产品类型、材料类型、技术、最终用户和地区进行的全球分析 软包装市场:按包装类型、材料、最终用途产业:2023-2032 年全球机会分析与产业预测

软包装市场:按包装类型、材料、最终用途产业:2023-2032 年全球机会分析与产业预测 金属化软包装市场:材料类型、结构、产品、最终用途产业划分 - 2024-2030 年全球预测

金属化软包装市场:材料类型、结构、产品、最终用途产业划分 - 2024-2030 年全球预测 2023年至2028年加工软包装市场预测

2023年至2028年加工软包装市场预测 全球金属化软包装市场:按材料类型、按结构、按包装类型、按最终用途行业、按地区 - 到 2028 年的全球预测

全球金属化软包装市场:按材料类型、按结构、按包装类型、按最终用途行业、按地区 - 到 2028 年的全球预测