|

市场调查报告书

商品编码

1432619

智慧製造 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029)Smart Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

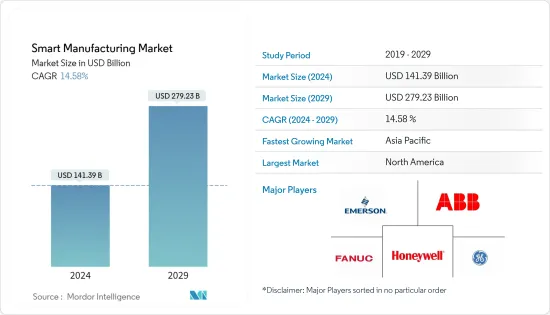

2024年智慧製造市场规模预估为1,413.9亿美元,预估至2029年将达2,792.3亿美元,预测期(2024-2029年)CAGR为14.58%。

采用智慧製造的措施不断增加将推动市场成长。智慧製造领导联盟 (SMLC) 是由美国工业组织、技术供应商、实验室和大学组成的联盟,致力于开发下一代智慧製造平台和智慧工厂连接。同样,另一个由产业主导的倡议——工业互联网联盟(IIC)的成立,旨在汇集加速工业自动化发展所需的先进技术和组织。

使用 SCADA、ERP、HMI、PLC、DCS、PLM 和 MES 等服务和软体,使各行业能够收集即时资料并做出决策。该软体对行业来说是有益的,因为它减少了产品错误,减少了停机时间,进行计划维护,从反应阶段转向预测和规定阶段,并支援决策。

对流程控制和系统的依赖,加上 IT 和作业系统技术系统的整合,使得製造业企业越来越容易遭受网路攻击。由于其专有和定制的网络,製造商的控制系统长期以来被认为是难以渗透的。物联网为窃取专有资讯开启了空间。随着这些设备的自动化和数位化程度越来越高,这些设备最初是在没有适当安全措施的情况下建构的,资料安全问题也将随之增加,阻碍市场成长。

此外,全球对工业 4.0 的投资正在增加。由于工业 4.0 智慧解决方案对其业务产生积极影响,包括提高生产力,组织已开始采用工业 4.0 智慧解决方案。例如,根据凯捷公司和全国软体与服务公司协会 (NASSCOM) 的报告,预计超过三分之二的印度製造业有意拥抱工业 4.0。到 2025 年

此外,市场上营运的公司注重创新并推出新产品,以在竞争中保持领先地位。例如,2023 年 2 月,该公司宣布推出可程式逻辑控制器 OTAC,以应对与工业物联网、智慧工厂和营运技术 (OT) 相关的关键未解决挑战。这透过利用动态「一次性身份验证代码」(OTAC) 技术解决典型的 ICS/OT 安全挑战,专门为 PLC 设备提供了高度最佳化且高度安全的身份验证解决方案。

COVID-19的爆发引发製造业重新评估其传统生产流程,主要推动整个生产线的数位转型和智慧製造实践。製造商也被迫实施和设计多种敏捷的新方法来监控产品和品质控制。

智慧製造市场趋势

汽车产业预计将推动市场成长

汽车製造预计将获得智慧技术、工业4.0、物联网等的强劲推动。离散製造是指生产或製造可以单独计数和触摸的不同零件。这些部件主要与装配线有关。离散製造包括汽车、汽车零件等日益互联的产品。

智慧製造有望帮助平衡供需、增强产品设计、优化製造效率并显着减少浪费。机器人、感测器等现场设备和 ICS 为汽车行业提供了更快地响应市场需求、减少製造停机时间、提高供应链效率和扩大生产力的机会。

智慧製造解决了汽车产业最关心的问题,即专案週期。快速投资回报项目与低成本自动化和成本创新相结合,正在帮助製造商透过提高生产力来提高竞争力。

此外,根据瑞银的数据,预计2025年欧洲电动车销量将达到633万辆,其次是中国,为484万辆。由于欧洲和亚太地区引领电动车需求,预计这些地区智慧汽车工厂的实施将会增加。

为了适应不断变化的汽车製造格局,业内许多企业正在采用智慧製造解决方案。例如,2022 年 1 月,华域汽车系统有限公司(以 HASCO 名义开展业务)和 ABB 集团宣布,他们在现有关係的基础上创建了一家合资企业,「以推动下一代智慧製造」。两家公司声称,合资企业将使他们能够进一步巩固华域汽车的领先地位,透过自动化解决方案造福中国客户。

过去 50 年来,汽车产业在各种製造流程的组装线上使用了机器人。目前,汽车製造商正在探索在更多程式中使用机器人技术。对于这类生产线来说,机器人更有效率、灵活、准确和可靠。这项技术使汽车产业仍然是最重要的机器人用户之一,并拥有全球自动化程度最高的供应链之一。

例如,2022年4月,汽车製造公司Stellantis NV的子公司菲亚特在其Mirafiori工厂投资7亿欧元,打算使用协作机器人等最先进的技术生产500辆电动车。该公司的目标是实现复杂装配线操作和品质控制的自动化,安装了 11 台来自 Universal Robots A/S 的协作机器人。协作机器人是智慧工厂的重要组成部分,因为它们结构紧凑、重量轻,并且能够与人类安全地一起工作。

亚太地区将占据主要市场份额

中国生产了相当大一部分的市场需求,并拥有全世界最大的製造业。此外,根据工业和资讯化部 (MIIT) 的数据,儘管 COVID-19 限制措施导致生产和供应链受挫,但 2022 年中国工业产值仍比上年增长 3.6%。工信部预计,2022年製造业产出成长3.1%,占国内生产毛额的比重达28%。

传统上被视为世界製造工厂的中国,透过数位化和工业化,已从(廉价)劳动密集型製造业向高端製造业显着转型。据GSMA称,到2025年,中国可能占全球IIoT市场的三分之一。

製造业也已成为印度高成长产业之一。 「印度製造」计画使印度成为世界地图上的製造中心,并让印度经济得到全球认可。

政府在实施该地区工业物联网应用案例方面发挥着重要作用。数位印度和印度製造等政府措施正在为印度製造业增添动力。物联网透过提供创新方法来维持製造组织的永续发展,大大促进了印度製造活动。

此外,印度製药业在自动化方面也相对领先,该国主要製药公司如Zydus Cedilla、Torrent Pharma、Cipla等都专注于药品製造过程的自动化,特别是在机器与设备完全整合的领域。需要设备。

此外,印度政府的目标是到2025年经济规模达到5兆美元,其中製造业价值可能达到1兆美元。印度製造、技能印度和数位印度等旗舰项目的整合可能是实现这一目标的关键,从而推动该国市场的成长。

此外,一些领先的行业参与者正在印度投资智慧製造部门,以提高效率并获得市场竞争优势。例如,2023年3月,三星电子宣布投资其位于诺伊达的第二大手机工厂的智慧製造能力,以提高生产竞争力。

智慧製造产业概况

智慧製造市场竞争激烈,由多家主要参与者组成。市场上拥有明星份额的主要参与者专注于扩大海外客户群。两家公司利用策略合作计划来增加市场占有率和获利能力。市场上营运的公司还收购了从事自动送货机器人技术的新创企业,以增强其产品能力。

2023年5月,三菱电机公司宣布对Clearpath Robotics进行策略性投资,以支持製造自动化的发展。 Clearpath Robotics 专注于开发和销售自主移动机器人 (AMR)。透过这项投资,该公司将利用 AMR 系统加强对整个工厂优化和自动化的支援。

2023 年 3 月,霍尼韦尔国际公司宣布推出霍尼韦尔通用机器人控制器 (HURC),以控制不同的机器人和自动化系统,并促进资料和通讯的无缝交换。该公司将在芝加哥举行的 ProMat 2023 上展示机器人和自动化解决方案。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设和市场定义

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代产品的威胁

- 竞争激烈程度

- COVID-19 对智慧製造市场的影响

第 5 章:市场动态

- 市场驱动因素

- 为了提高效率和品质而对自动化的需求不断增加

- 数位化需要合规性和政府支持

- 物联网的普及

- 市场限制

- 对资料安全的担忧

- 高昂的初始安装成本和缺乏熟练的劳动力阻碍企业全面采用

第 6 章:市场细分

- 依技术

- 可程式逻辑控制器(PLC)

- 监控控制器和资料采集 (SCADA)

- 企业资源与规划 (ERP)

- 集散控制系统(DCS)

- 人机介面 (HMI)

- 产品生命週期管理 (PLM)

- 製造执行系统(MES)

- 其他技术

- 按组件

- 机器视觉系统

- 控制装置

- 机器人技术

- 通讯板块

- 感应器

- 其他组件

- 按最终用户产业

- 汽车

- 半导体

- 油和气

- 化学与石化

- 製药

- 航太和国防

- 食品与饮品

- 金属和采矿

- 其他最终用户产业

- 按地理

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 亚太地区其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地区

- 中东和非洲

- 北美洲

第 7 章:竞争格局

- 公司简介

- ABB Ltd

- Emerson Electric Company

- Fanuc Corporation

- General Electric Company

- Honeywell International Inc.

- Mitsubishi Electric Corporation

- Robert Bosch GmbH

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Texas Instruments Incorporated

- Yokogawa Electric Corporation

第 8 章:投资分析

第 9 章:市场的未来

The Smart Manufacturing Market size is estimated at USD 141.39 billion in 2024, and is expected to reach USD 279.23 billion by 2029, growing at a CAGR of 14.58% during the forecast period (2024-2029).

The increasing initiatives to adopt smart manufacturing will drive market growth. Smart Manufacturing Leadership Coalition (SMLC), a combination of US-based industrial organizations, technology suppliers, laboratories, and universities, is working on a next-generation Smart Manufacturing Platform and Smart Factory connectivity. Similarly, another industry-led initiative, the Industrial Internet Consortium (IIC), was formed to bring together the advanced technologies and organizations needed to accelerate the growth of industrial automation.

Using services and software, such as SCADA, ERP, HMI, PLC, DCS, PLM, and MES, has enabled industries to collect real-time data and make decisions. The software has been beneficial to the industry as it reduces product errors, reduces downtime, conducts planned maintenance, moves from the reactive phase to the predictive and prescribing phases, and enables decision-making.

The dependence on process control and systems combined with the convergence of IT and operating technologies systems has increasingly exposed manufacturing firms to cyber attacks. Manufacturers' control systems have long been deemed impenetrable due to their proprietary and customized networks. IoT has opened the scope for the theft of proprietary information. With more automation and digitization of these devices, which were originally built without the proper security measures, the data security concern will also grow, hindering the market growth.

Furthermore, investments in Industry 4.0 are rising globally. Organizations have started adopting Industry 4.0 smart solutions owing to their positive impact on their businesses, including increased productivity. For instance, as per a report by Capgemini and the National Association of Software and Services Companies (NASSCOM), it is expected that more than two-thirds of the Indian manufacturing sector intention embrace Industry 4.0. by 2025

Moreover, the companies operating in the market focus on innovations and launch new products to stay ahead of the competition. For instance, in February 2023, which announced the launch of Programmable Logic Controller OTAC to combat key unresolved challenges related to industrial IoT, smart factories, and operational technology (OT). This provides a highly optimized and highly secure authentication solution specifically for PLC devices by utilizing their dynamic 'one-time authentication code' (OTAC) technology to resolve typical ICS/OT security challenges.

The outbreak of COVID-19 triggered the manufacturing sector to re-evaluate its traditional production processes, primarily driving digital transformation and smart manufacturing practices across the production lines. The manufacturers also forced to implement and devise multiple agile and new approaches to monitor product and quality control.

Smart Manufacturing Market Trends

Automotive Industry is Expected to Drive the Market Growth

Automotive manufacturing is expected to gain strong impetus from smart technologies, Industry 4.0, IoT, etc. Discrete manufacturing is producing or manufacturing distinct parts that can be individually counted and touched. The pieces are mainly related to assembly lines. Discrete manufacturing includes products, such as cars, automotive parts, etc., that are increasingly connected.

Smart manufacturing is expected to help balance supply and demand, enhance product design, optimize manufacturing efficiency, and significantly reduce waste. Field devices, like robotics, sensors, etc., and ICS offer opportunities to the automotive sector to react faster to market requirements, reduce manufacturing downtimes, enhance supply chain efficiency, and expand productivity.

Smart manufacturing addresses the prime concern of the automotive industry, i.e., the length of a project. Quick return-on-investment projects combined with low-cost automation and cost innovation are helping manufacturers improve competitiveness through productivity improvement.

Further, according to UBS, Europe's projected electric vehicle sales are expected to reach 6.33 million units by 2025, followed by China, with 4.84 million units. As Europe and Asia-Pacific are leading the electric vehicles demand, the regions are anticipated to see an increase in smart automotive factories' implementation.

To cater to the changing landscape of automotive manufacturing, many players in the industry are adopting smart manufacturing solutions. For instance, in January 2022, Huayu Automotive Systems Co., which does business as HASCO, and ABB Group announced that they have created a joint venture building on their existing relationship "to drive the next generation of smart manufacturing." The companies claimed that the joint venture would enable them to further develop HASCO's leading position with automated solutions that benefit customers in China.

For the past 50 years, the automotive industry has used robots in its assembly lines for various manufacturing processes. Currently, automakers are exploring the use of robotics in more procedures. Robots are more efficient, flexible, accurate, and dependable for such production lines. This technology enables the automotive industry to remain one of the most significant robot users and possess one of the most automated supply chains globally.

For instance, in April 2022, an automotive manufacturing company, Fiat, a subsidiary of Stellantis NV, invested EUR 700 million at its Mirafiori factory, intending to produce 500 electric vehicles using state-of-the-art technology, such as collaborative robots. The company aims to automate its complex assembly line operations and quality controls, installing 11 cobots from Universal Robots A/S. Cobots are an essential part of the smart factory since they are compact, light, and built to work alongside humans safely.

Asia Pacific Region to Occupy a Major Market Share

China produces a sizeable portion of the market's demand and has the largest manufacturing sector in the entire world. In addition, despite production and supply chain setbacks brought on by COVID-19 curbs, the nation's industrial output increased by 3.6% in 2022 compared to the previous year, according to the Ministry of Industry and Information Technology (MIIT). The MIIT predicted that the manufacturing sector's output would have increased by 3.1% in 2022, making up 28% of China's GDP.

Traditionally seen as the world's manufacturing factory, China has significantly transformed from (cheap) labor-intensive manufacturing to high-end manufacturing through digitalization and industrialization. According to GSMA, China may account for one-third of the global IIoT market by 2025.

Manufacturing has also emerged as one of the high-growth sectors in India. The 'Make in India' program places India on the world map as a manufacturing hub and globally recognizes the Indian economy.

Government plays an important role in implementing the use of cases of IIoT in the region. Government initiatives, like Digital India and Make in India, are adding impetus to the Indian manufacturing industry. IoT immensely benefits the Make in India campaign by providing innovative ways to sustain manufacturing organizations' sustainable development.

Moreover, India's pharmaceutical sector is comparatively ahead in automation, with the major pharmaceutical companies in the country, such as Zydus Cedilla, Torrent Pharma, and Cipla, focusing on automating their manufacturing processes of drugs, especially in areas where the complete integration of machines and equipment is required.

Additionally, India's government aims for a USD 5 trillion economy by 2025, of which manufacturing may be worth USD 1 trillion. The convergence of flagship programs, such as Make in India with Skill India and Digital India, may be key to achieving this goal, thereby driving the country's market growth.

Furthermore, several leading industry players are investing in smart manufacturing units in India to improve efficiency and gain a competitive edge in the market. For instance, in March 2023, Samsung Electronics announced investing in smart manufacturing capabilities at its second-largest mobile phone plant in Noida to make production more competitive.

Smart Manufacturing Industry Overview

The smart manufacturing market is highly competitive and consists of several major players. The major players with star shares in the market focus on expanding their customer base across foreign countries. The companies leverage strategic collaborative initiatives to increase their market share and profitability. The companies operating in the market are also acquiring start-ups working on autonomous delivery robot technologies to strengthen their product capabilities.

In May 2023, Mitsubishi Electric Corporation announced to make a strategic investment in Clearpath Robotics to support the development of manufacturing automation. Clearpath Robotics specializes in developing and selling autonomous mobile robots (AMR). Through this investment, the company will strengthen its support for complete factory optimization and automation by utilizing AMR systems.

In March 2023, Honeywell International, Inc. announced introducing Honeywell Universal Robotics Controller (HURC) to control disparate robotics and automation systems and facilitate the seamless exchange of data and communications. The company will demo robotic and automation solutions at ProMat 2023 in Chicago.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the Smart Manufacturing Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Automation to Achieve Efficiency and Quality

- 5.1.2 Need for Compliance and Government Support for Digitization

- 5.1.3 Proliferation of Internet of Things

- 5.2 Market Restraints

- 5.2.1 Concerns Regarding Data Security

- 5.2.2 High Initial Installation Costs and Lack of Skilled Workforce Preventing Enterprises from Full-scale Adoption

6 MARKET SEGMENTATION

- 6.1 By Technology

- 6.1.1 Programmable Logic Controller (PLC)

- 6.1.2 Supervisory Controller and Data Acquisition (SCADA)

- 6.1.3 Enterprise Resource and Planning (ERP)

- 6.1.4 Distributed Control System (DCS)

- 6.1.5 Human Machine Interface (HMI)

- 6.1.6 Product Lifecycle Management (PLM)

- 6.1.7 Manufacturing Execution System (MES)

- 6.1.8 Other Technologies

- 6.2 By Component

- 6.2.1 Machine Vision Systems

- 6.2.2 Control Device

- 6.2.3 Robotics

- 6.2.4 Communication Segment

- 6.2.5 Sensor

- 6.2.6 Other Components

- 6.3 By End-user Industry

- 6.3.1 Automotive

- 6.3.2 Semiconductors

- 6.3.3 Oil and Gas

- 6.3.4 Chemical and Petrochemical

- 6.3.5 Pharmaceutical

- 6.3.6 Aerospace and Defense

- 6.3.7 Food and Beverage

- 6.3.8 Metals and Mining

- 6.3.9 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia Pacific

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Japan

- 6.4.3.4 Rest of Asia Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Mexico

- 6.4.4.3 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Ltd

- 7.1.2 Emerson Electric Company

- 7.1.3 Fanuc Corporation

- 7.1.4 General Electric Company

- 7.1.5 Honeywell International Inc.

- 7.1.6 Mitsubishi Electric Corporation

- 7.1.7 Robert Bosch GmbH

- 7.1.8 Rockwell Automation Inc.

- 7.1.9 Schneider Electric SE

- 7.1.10 Siemens AG

- 7.1.11 Texas Instruments Incorporated

- 7.1.12 Yokogawa Electric Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

智慧型弹性生产系统(FMS)的全球市场,实际成果与预测(2018年~2029年)

智慧型弹性生产系统(FMS)的全球市场,实际成果与预测(2018年~2029年) 2024年智慧製造全球市场报告

2024年智慧製造全球市场报告 智慧製造的传播—全球趋势

智慧製造的传播—全球趋势 智慧製造市场 - 全球产业规模、份额、趋势、机会和预测,按组件、技术、最终用途行业、地区、竞争细分,2018-2028 年

智慧製造市场 - 全球产业规模、份额、趋势、机会和预测,按组件、技术、最终用途行业、地区、竞争细分,2018-2028 年 智慧製造市场:2023-2028 年全球产业趋势、份额、规模、成长、机会与预测

智慧製造市场:2023-2028 年全球产业趋势、份额、规模、成长、机会与预测 智慧製造市场报告:2030 年趋势、预测与竞争分析

智慧製造市场报告:2030 年趋势、预测与竞争分析 全球智慧製造市场规模研究与预测,按组件、技术、最终用途和区域分析,2023-2030 年

全球智慧製造市场规模研究与预测,按组件、技术、最终用途和区域分析,2023-2030 年 2030 年智慧製造平台市场预测 - 按类型、组织规模、部署类型、产业、用途和地区的全球分析

2030 年智慧製造平台市场预测 - 按类型、组织规模、部署类型、产业、用途和地区的全球分析 全球智能製造市场:按技术(3D 打印、铝製造、自动导引运输车、状态监测、网络安全、数字孪生、HMI、机器视觉、MES、PAM、机器人、传感器)、按行业、按地区- 预测至2028 年

全球智能製造市场:按技术(3D 打印、铝製造、自动导引运输车、状态监测、网络安全、数字孪生、HMI、机器视觉、MES、PAM、机器人、传感器)、按行业、按地区- 预测至2028 年 智慧製造业的全球市场 2023-2027

智慧製造业的全球市场 2023-2027