|

市场调查报告书

商品编码

1432786

控制阀:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Control Valve - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

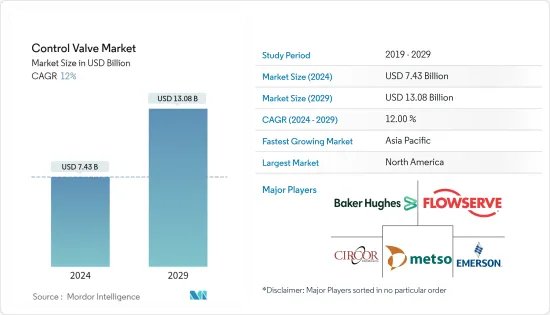

控制阀市场规模预计2024年为74.3亿美元,预计到2029年将达到130.8亿美元,在预测期内(2024-2029年)增长12%,预计将以复合年增长率增长。

在预测期内,由于近期管道投资和基础设施扩建的增加,控制阀的需求预计将增加。

主要亮点

- 技术进步形成了创新的解决方案,可以简化加工厂的运作并进一步提高效率。随着行业要求的发展和变化,控制阀和阀门自动化解决方案供应商预计将继续开发能够应对这些新挑战的产品和流程。

- 控制阀市场的成长是由诸如对无线基础设施监控各种工厂设备的需求不断增加、对自动化的日益关注以及製程工业中设施数量不断增加等因素所推动的。

- 具有嵌入式处理器和网路功能的阀门技术在石油、天然气和製药等重要行业中越来越普及。这些技术与先进的监控设备结合使用,并透过中央控制站进行协调。

- 为了响应市场需求,开发了具有高循环率和耐高温能力的控制阀。此外,对替代能源(尤其可再生能源)投资的日益关注,为控制阀带来了机会和新的潜在应用。例如,IEA预测全球能源投资的70%将投向可再生能源。

- 此外,随着製造自动化变得普及,控制阀供应商正在寻求透过併购来加强其市场地位。例如,2021年10月,阿姆斯壮国际完成了蒸气调节器、工业泵浦、热水器和控制系统製造商Leslie Controls的收购。莱斯利的各种控制阀和蒸气热水器都包含在交易中。

- COVID-19 的爆发在世界各地引发了经济危机。疫情对油气产业造成严重影响,原油价格大幅下跌。主要石油生产商耗尽了其开采的石油的储存空间,从而减少了需求。根据美国石油协会 2020 年 4 月月度统计报告,美国石油需求下降近 27%,至 1,420 万桶/日。

- 这种情况造成了供需之间的巨大差距。石油和天然气行业是使用控制阀的主要行业之一。新的石油和天然气探勘计划、运输管道计划和维护活动是全球市场控制阀的主要需求来源。

控制阀市场趋势

能源来源控制阀推动市场成长

- 关键的市场驱动因素之一是可再生能源计划的势头。由于太阳能热电厂数量的迅速增加,控制阀的应用领域正在不断扩大。然而,全球低效率的物流和供应系统预计将阻碍控制阀市场的发展。

- 感测器和阀门技术的进步使能源来源产业的製造商能够透过降低设备的整体拥有成本、最大限度地延长运作和降低维护成本来提高製造能力。

- 对可再生能源计划的日益关注导致太阳能热电厂数量迅速增加,在一些地区也扩大了控制阀的应用领域。此外,具有高水准能力和广泛资金筹措选择的劳动力正在推动对可再生能源计划的需求。

- 此外,由于区域需求不断增长,能源公司正在该地区探索石油和天然气生产机会。例如,2021年11月,海洋能源管理局(BOEM)举行了墨西哥湾石油和天然气租赁销售活动。此次租赁销售吸引了 308 个街区的超过 1.91 亿美元的竞标。关于租赁销售,我们共收到33家公司的317份提案。

- 各行业製造商引入新技术,使得控制阀行业能够开发出与无菌阀门相结合的新配件,以提供高水准的控制和完整准确的阀门状态。

北美占有很大的市场占有率

- 北美是世界上最重要的控制阀市场之一。美国和加拿大各行业都有庞大的需求,包括石油和天然气、电力、食品和包装以及化学品。随着工业自动化的快速发展,该地区预计将成为控制阀需求的前沿。

- 这些国家的快速工业化和交通运输业的成长预计将增加对石油和天然气的需求。为不断增长的人口提供饮用水的需要还需要安装海水淡化厂,这反过来又产生了对控制阀的需求。废弃物和污水管理也是预计推动未来需求的关键领域。

- 与加拿大相比,美国在该地区需求成长方面发挥着重要作用。该国几乎所有最终用户产业的需求都在成长,特别是石油和天然气、精製和发电产业。

- 石油和天然气、可再生能源、水和废水处理等国内主要产业正转向采用嵌入式处理器和网路功能的阀门技术,并透过中央控制站协调先进的监控技术。

- 美国石油产量持续快速扩张。例如,美国最大的石油生产商之一埃克森美孚计画最早在 2024 年扩大在德克萨斯州西部二迭纪盆地的业务,每日产量超过 100 万桶石油当量 (bpd)。生产活动。与目前的产能相比,这意味着增加了近80%。同样,雪佛龙预计将增加其净石油当量产量,到2020年达到每天60万桶,到2023年达到每天90万桶。

- 随着该地区可再生能源计划的势头不断增强,控制阀的应用领域也不断扩大,导致太阳能热电厂数量迅速增加。该地区拥有风能、太阳能、地热能、水能和生质能资源。丰富的资金筹措机会和高技能的劳动力也是推动可再生能源计划需求的因素。

控制阀产业概况

控制阀市场竞争适度,由几个主要参与者组成。随着控制阀需求的不断增加,许多新兴企业正在扩大其市场份额并在新兴国家开拓客户。

- 2022 年 5 月 - Flowserve 宣布改进了 Valtek FlowTop 控制阀的设计,以满足一般服务和中等要求服务应用的要求。新型FlowTop 通用阀以经过验证的FlowTop GS 和Valtek GS 控制阀为基础,提供一种标准化、多功能控制阀、精确控制、多种阀内件和填料选项以及简单性。透过提供标准化维护,我们满足了广泛的需求的要求。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 评估 COVID-19 对产业的影响

第五章市场动态

- 产业供应链分析

- 市场驱动因素

- 新兴市场越来越重视电力、水和用水和污水

- 最终用户关注环境问题和老化基础设施维修以保持竞争力

- 市场挑战

- 最终用户关注环境问题并维修老化基础设施以保持竞争力

- 油价的动态变化预计将影响整体计划支出

- 市场机会

第六章市场区隔

- 按类型

- 手套

- 球

- 蝴蝶

- 插头

- 隔膜

- 其他阀门

- 按最终用户

- 油和气

- 化工、石化、化肥

- 能源/电力

- 水处理/污水处理

- 金属/矿业

- 其他最终用户(食品和饮料、药品、纸浆/造纸製造等)

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

- 世界其他地区

- 北美洲

第七章 竞争形势

- 公司简介

- Emerson Electric Co.

- Flowserve Corporation

- Baker Hughes Company

- Metso Corporation

- CIRCOR International Inc.

- IMI PLC

- Christian Burkert GmbH & Co. KG

- GEA Group Aktiengesellschaft

- Neway Valve(Suzhou)Co. Ltd

第八章投资分析

第9章 未来趋势

The Control Valve Market size is estimated at USD 7.43 billion in 2024, and is expected to reach USD 13.08 billion by 2029, growing at a CAGR of 12% during the forecast period (2024-2029).

Over the projection period, it is expected that increasing recent investments in pipeline and infrastructure expansion will boost demand for control valves.

Key Highlights

- Advancements in technology have shaped innovative solutions that can improve process plants to become increasingly efficient by streamlining their operations. As industry requirements evolve and change, control valves and valve automation solutions suppliers are expected to continue developing products and processes that address these new challenges.

- The control valve market growth is driven by factors such as the increasing need for wireless infrastructure to monitor equipment in various plants, augmented focus on automation, and expanding number of process industry establishments.

- Valve technology with embedded processors and networking capabilities is becoming more popular in essential industries like oil and gas and pharmaceuticals. These technologies will function with sophisticated monitoring equipment and will be coordinated through a central control station.

- Control valves with a high number of cycles and the ability to withstand high temperatures have been developed in response to market demand. Furthermore, opportunities and new potential uses for control valves have been made possible by the growing emphasis on investing in alternative energy sources, especially renewable energy. For instance, the IEA predicts that 70% of all global energy investment will go toward renewable energy.

- Besides, because manufacturing automation is proliferating, control valve suppliers are attempting to enhance their market positions through mergers and acquisitions. For instance, in October 2021, Armstrong International finalized the acquisition of Leslie Controls, a producer of steam regulators, industrial pumps, water heaters, and control systems. Various control valves and steam water heaters from Leslie were included in the deal.

- The outbreak of COVID-19 has resulted in an economic crisis across the world. The pandemic has severely affected the oil and gas industry, with oil prices slashing down. Significant oil producers ran out of storage space for extracted oil, and the demand declined. According to the American Petroleum Institute's April 2020 Monthly Statistical Report, the petroleum demand in the United States declined nearly by 27% to 14.2 million barrels per day (b/d).

- This scenario has resulted in a massive gap between supply and demand. The oil and gas sector is one of the key industries using control valves. New oil and gas exploration projects, transportation pipeline projects, and maintenance activities are some of the major sources of demand for control valves in the global market.

Control Valve Market Trends

Control valves in Energy Sources to Drive the Market Growth

- One of the crucial market drivers is the thrust on renewable energy projects. A rapidly growing number of solar thermal energy plants have increased the application areas of control valves. However, inefficient logistics and supply systems worldwide are expected to hinder the control valve market.

- Advancements in sensor and valve technology have enabled manufacturers in the Energy sources industry to up their manufacturing capabilities by reducing the overall cost of equipment ownership, maximizing uptime, and lowering maintenance costs.

- With the increased emphasis on renewable energy projects, which sparked a sharp rise in the number of solar thermal energy plants, several regions have also seen raised application areas for control valves. A workforce is also driving the demand for renewable energy projects with a high level of competence and a force with plenty of financing options.

- Moreover, energy companies are looking for oil and gas production opportunities in the region, owing to the growing regional demand. For instance, in November 2021, the Bureau of Ocean Energy Management (BOEM) held an oil and gas lease sale for the Gulf of Mexico. This lease sale attracted over USD 191 million in bids for 308 blocks. In the lease sale, a total of 33 companies submitted 317 proposals.

- The implementation of new technologies by manufacturers across industries has aided the control valve industry in creating new accessories that, in conjunction with aseptic valves, offer high levels of control and complete and accurate status of a valve.

North America to Hold Significant Market Share

- North America is one of the world's most significant markets t for control valves. In both the United States and Canada, there is immense demand from various industries, including oil and gas, electricity, food and packaging, and chemicals. With rapid industrial automation, the region is expected to spearhead the need for control valves.

- Rapid industrialization and the growing transportation sector in these nations are expected to increase the demand for oil and gas. The need to provide potable water to the ever-increasing population also leads to the setting up of desalination plants, further resulting in the demand for control valves. Waste and wastewater management is also a considerable segment expected to drive future demand.

- The United States plays a critical role in increasing the demand from the region when compared to Canada. The country has an increasing demand from almost all the end-user segments, especially from the oil and gas, refining, and power generation segments.

- Major industries in the country, such as oil and gas, renewable energy, and water and wastewater treatment, are moving toward valve technology with embedded processors and networking capability to work alongside sophisticated monitoring technology coordinated through a central control station.

- Oil production in the United States continues to expand rapidly. For instance, ExxonMobil, one of the leading oil producers in the country, announced its plans to increase the production activity in the Permian Basin of West Texas by producing more than 1 million barrels per day (bpd) of oil equivalent by as early as 2024. This is equivalent to an increase of nearly 80% compared to the present production capacity. Similarly, Chevron is expected to increase its net oil-equivalent production to reach 600,000 bpd by 2020 and 900,000 bpd by 2023.

- The region has also witnessed increased application areas of control valves with the increased thrust on renewable energy projects, which led to the rapid increase in the number of solar thermal energy plants. The region features wind, solar, geothermal, hydro, and biomass resources. Ample financing opportunities and a highly skilled workforce are the other factors driving the demand for renewable energy projects.

Control Valve Industry Overview

The control valve market is moderately competitive and consists of several significant players. With the growing demand for control valves, many new companies are increasing their market presence, tapping customers across emerging economies.

- May 2022 - Flowserve announced that it had improved the design of the Valtek FlowTop control valve to meet the global requirements for general service and moderately severe service applications. The new FlowTop General Service valve builds on the proven FlowTop GS and Valtek GS control valves to meet a broad range of requirements by providing: One standardized, versatile control valve, Precision control, A variety of trim and packing options, and Simplified maintenance.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of COVID-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Industry Supply Chain Analysis

- 5.2 Market Drivers

- 5.2.1 Growing emphasis on Power and Water & Wastewater in Emerging Markets

- 5.2.2 Focus of End Users on Environmental Issues and Refurbishment of Aging Infrastructure to Stay Competitive

- 5.3 Market Challenges

- 5.3.1 Focus of End Users on Environmental Issues and Refurbishment of Aging Infrastructure to Stay Competitive

- 5.3.2 Dynamic Change in Oil Prices is Expected to Influence the Overall Spending on the Projects

- 5.4 Market Opportunities

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Globe

- 6.1.2 Ball

- 6.1.3 Butterfly

- 6.1.4 Plug

- 6.1.5 Diaphragm

- 6.1.6 Other Types of Valves

- 6.2 By End User

- 6.2.1 Oil and Gas

- 6.2.2 Chemical, Petrochemical, and Fertilizer

- 6.2.3 Energy and Power

- 6.2.4 Water and Wastewater Treatment

- 6.2.5 Metal and Mining

- 6.2.6 Other End User (Food and Beverage, Pharmaceutical, Pulp and Paper, etc.)

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 South Korea

- 6.3.3.5 Rest of Asia-Pacific

- 6.3.4 Rest of the World

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Emerson Electric Co.

- 7.1.2 Flowserve Corporation

- 7.1.3 Baker Hughes Company

- 7.1.4 Metso Corporation

- 7.1.5 CIRCOR International Inc.

- 7.1.6 IMI PLC

- 7.1.7 Christian Burkert GmbH & Co. KG

- 7.1.8 GEA Group Aktiengesellschaft

- 7.1.9 Neway Valve (Suzhou) Co. Ltd

8 INVESTMENT ANALYSIS

9 FUTURE TRENDS

控制阀市场规模、份额、成长分析,按组件、按材料、按类型、按尺寸、按最终用途行业、按地区 - 行业预测,2024-2031 年

控制阀市场规模、份额、成长分析,按组件、按材料、按类型、按尺寸、按最终用途行业、按地区 - 行业预测,2024-2031 年 控制阀市场:按类型、组件、材料、技术、行业划分 - 2025-2030 年全球预测

控制阀市场:按类型、组件、材料、技术、行业划分 - 2025-2030 年全球预测 飞机气动阀市场 - 全球产业规模、份额、趋势、机会和预测,按应用、阀门类型、机构、地区和竞争细分,2019-2029F

飞机气动阀市场 - 全球产业规模、份额、趋势、机会和预测,按应用、阀门类型、机构、地区和竞争细分,2019-2029F 多孔流量控制阀市场:2024-2031年全球产业分析、规模、占有率、成长、趋势与预测

多孔流量控制阀市场:2024-2031年全球产业分析、规模、占有率、成长、趋势与预测 不銹钢控制阀市场报告:2030 年趋势、预测与竞争分析

不銹钢控制阀市场报告:2030 年趋势、预测与竞争分析 夹管阀的世界市场

夹管阀的世界市场 固体流量阀市场报告:2030 年趋势、预测与竞争分析

固体流量阀市场报告:2030 年趋势、预测与竞争分析 控制阀市场 - 全球和区域分析:按最终用途行业、类型、材料、组件、地区 - 分析和预测(2024-2034)

控制阀市场 - 全球和区域分析:按最终用途行业、类型、材料、组件、地区 - 分析和预测(2024-2034) 2024-2032 年按类型、技术、组件、材料、最终用途产业和地区分類的控制阀市场报告

2024-2032 年按类型、技术、组件、材料、最终用途产业和地区分類的控制阀市场报告 全球控制阀市场 2024-2031

全球控制阀市场 2024-2031