|

市场调查报告书

商品编码

1432803

风险分析:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Risk Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

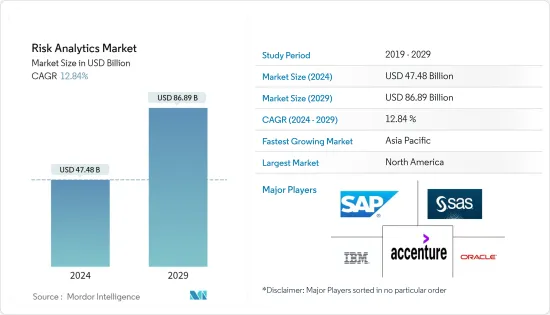

风险分析市场规模预计到 2024 年为 474.8 亿美元,预计到 2029 年将达到 868.9 亿美元,在市场估计和预测期间(2024-2029 年)复合年增长率为 12.84%。

风险分析解决方案有助于解决和防范人为错误、系统故障(可能与软体、硬体、网路等相关)和诈欺网路犯罪等内部因素所引起的营运风险。

主要亮点

- 风险分析技术现在使风险管理者能够比以往更可靠地衡量和预测风险。企业使用风险分析从各种安全资料来源收集支援讯息,以量化网路风险、自动化保全行动并主导情报驱动的决策。此外,从网路角度来看,透过 PCI-DSS 和 NIST 网路安全框架等强制要求和指导,组织面临越来越大的监管压力。

- 各个最终用户产业越来越多地使用大量结构化和非结构化资料,增加了对风险资料来管理和保护资料免受威胁的需求。例如,根据 Seagate Technology PLC 的数据,全球资料量预计将在 2020 年增加到 47 Zetta位元组,到 2025 年将增加到 163 Zetta位元组。

- 此外,云端处理正在推动一场软体革命,其规模比过去 40 年来任何其他运算革命都更加令人震惊。随着基于位置的风险分析的进步,使用云端基础的技术而不是传统的基于伺服器的系统来建立和交付它是有意义的。目前有多种可透过云端进行风险评估和储存的平台。基于规则的安全方法,无论是应用于威胁侦测、调查或回应,都无法再应对进阶网路威胁,包括受损帐号和恶意相关人员。我不能。

- 行动银行业务服务使用的增加和资料量的增加也推动了银行、金融服务和保险 (BFSI) 领域对风险分析的需求。透过应用风险分析,您可以将资料整合到一个全面的观点中,收集基本资料并产生可行的见解。此外,风险分析对于世界各地的物流公司有效应对冠状病毒国际感染疾病造成的业务中断和供应链问题至关重要。

- 此外,一些公司正在提供新的分析解决方案(主要是在医疗保健领域)来对抗 COVID-19。实验室测试推动了很大一部分临床决策,并在改善常见和高风险疾病的患者护理方面发挥重要作用。例如,LabCorp 发布 Insight Analytics 报告,帮助提供者组织在个人和人群层面为各种高风险健康状况提供更好的照护。

风险分析市场的趋势

BFSI 预计将大量采用风险分析解决方案

- 世界各地的银行都了解风险分析的重要性,并意识到需要更简化的方法来解决银行和金融业日益增加的风险。

- 风险分析使银行和金融机构能够摆脱「筒仓」风险管理方法,并全面了解整个企业的风险。例如,在操作风险管理(ORM)中,需要监控的交易数量呈指数级增长,这增加了当前银行基础设施的压力,并为风险分析市场注入了活力。

- 金融机构在发展业务的同时面临着减少诈欺并满足严格的监管合规要求的巨大压力。此外,新帐户诈骗和帐户接管是金融机构目前面临的最主要的两种诈骗类型。风险分析解决方案使用基于机器学习的风险分析(一种人工智慧)来防范线上和行动管道上的这些和诈欺诈欺。

- 银行可以透过多种方式使用资料分析来保护自己免受危险。例如,客户分析可用于根据信用风险管理的信用度对客户进行分类。此类客户预计将按时付款,从而使个人能够选择信贷产品的目标市场并降低违约风险。据世界风险专业人士协会称,资本市场、银行和保险业预计将在风险资讯技术和服务上花费 960 亿美元。

- 此外,根据 Grant Thornton 的一项研究,85% 的受访者认为他们银行的资料和风险资讯管理倡议需要进一步提高效率才能充分发挥潜力。此外,82% 的受访者对于银行的风险分析和衡量也持相同的看法。因此,此类趋势推动了 BFSI 产业对风险分析解决方案的需求。

北美预计将占据很大份额

- 预计北美将占据最高的市场占有率,其中美国领先市场。该地区的优势在于终端用户行业越来越多地采用风险分析解决方案、大公司的强大存在以及来自低成本地区其他公司的竞争,而这得益于技术引进的促进。

- 此外,跨产业采用云端运算也推动了市场成长。保护医疗资讯系统 (HIS) 免受紧迫网路安全风险的挑战与云端运算的采用交织在一起。 HIS资料和资源本质上与其他系统共用,用于远端存取、决策、紧急情况和其他医疗保健相关方面。

- 此外,在大流行期间,美国报告了 28 起资料外洩事件,包括电子邮件骇客事件、恶意软体攻击和未授权存取EHR(资料来源:美国卫生与公众服务部)。在医疗保健领域,云端处理被认为是一种快速解决方案,因为它具有可扩展性和经济性。

- 美国医疗保健基础设施在预测分析领域正在经历积极的趋势。研究发现,过去几年,超过 40% 的医疗保健主管报告资料量增加了 50%。随着资料集变得越来越大且越来越难以处理,医疗保健系统和付款人越来越多地采用预测分析。

- 此外,风险分析供应商在该地区拥有牢固的立足点,为市场成长做出了贡献。其中包括 IBM Corporation、Oracle Corporation、SAS Institute Inc.、AxiomSL Ltd. 等。

风险分析行业概况

风险分析市场相对整合,大型供应商占据主导地位,尤其是在企业级实施方面。大公司也主导了这个市场,因为他们能够为最终用户提供创新和高品质的服务。 IBM 公司、SAP SE、SAS Institute Inc.、Oracle 公司、埃森哲 PLC、Adenza Group Inc.

2023 年 11 月,软体即服务 (SaaS) 风险分析供应商 Renew Risk 与着名可再生能源计划保险公司 GCube Insurance 宣布建立策略合作伙伴关係。 GCube的离岸风力发电客户将从此次合作中受益匪浅,增强离岸风力发电风险分析和建模能力。 GCube 将利用 Renew Risk 为离岸风电投资组合量身定制的先进巨灾风险模型,从该协议中受益。

2023 年 9 月,企业风险解决方案、投资组合建构工具和因子风险模型的全球供应商 Axioma 宣布与 Jacobi Inc. 建立新的合作伙伴关係。总部位于旧金山的 Jacobi 的技术可实现动态客户参与、优化投资业务并简化多资产投资组合的建置和维护。这种工作流程整合解决方案使投资经理可以轻鬆存取时间序列和时间点风险资料,以基于因子资料股权和多资产类别投资组合。

2022年10月,世界一流的投资银行、证券和投资管理公司高盛集团与创新风险、分析和指数解决方案领先供应商Qontigo宣布扩大合作伙伴关係。 Qontigo 是高盛数据金融云,是模组化资料管理和分析解决方案的集合,也是该公司的数位平台,为机构投资者提供市场领先的资料、分析、市场洞察和交易解决方案。风险模型将透过高盛Marquee 提供,

2022 年 9 月,Camelot Management Consultants 与领先的供应链洞察和风险分析供应商 Everstream Analytics 建立了联合合作伙伴关係。此次合作将 Everstream 卓越的风险评估和人工智慧分析与 Camelot 无与伦比的策略流程设计和组织知识相结合,以创建高效能、合规且有弹性的价值链。这是值得建造的东西。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 市场定义和范围

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 市场驱动因素

- 业务流程复杂性

- 全球监管框架与政府政策

- 市场限制因素

- 实施和营运成本高

- 复杂的监管合规可能会阻碍市场成长

- COVID-19 对整个市场的影响

第五章市场区隔

- 按成分分类

- 解决方案

- 按服务

- 按发展

- 本地

- 云

- 按行业分类

- BFSI

- 卫生保健

- 零售

- 製造业

- 其他最终用户(IT 和电信)

- 地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 其他亚太地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲

- 中东/非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 其他多边环境协定

- 北美洲

第六章 竞争形势

- 公司简介

- IBM Corporation

- Oracle Corporation

- SAP SE

- SAS Institute Inc.

- Moody's Analytics Inc.

- OneSpan Inc.

- Capgemini SE

- Accenture PLC

- Risk Edge Solutions

- Adenza Group Inc.(AxiomSL Ltd.)

- Provenir Inc.

第七章 投资分析

第八章 市场机会及未来趋势

The Risk Analytics Market size is estimated at USD 47.48 billion in 2024, and is expected to reach USD 86.89 billion by 2029, growing at a CAGR of 12.84% during the forecast period (2024-2029).

Risk analytics solutions help organizations deal with and protect against operational risks, which can arise due to internal factors, such as human errors, failures of systems (which can be related to software, hardware, network, etc.), and fraud cybercrime.

Key Highlights

- Currently, risk analytics techniques are enabling risk managers to measure and predict risk with more certainty than ever before. Organizations are leveraging risk analytics to gather supporting information through various security data sources to quantify their cyber risks, automate their security operations, and make intelligence-driven decisions. Additionally, organizations are witnessing increased regulatory pressure from the cyber perspective with mandates and guidance, such as the PCI-DSS and NIST Cybersecurity Framework.

- The increased usage of large amounts of structured and unstructured data in the various end-user industries boosts the demand for risk analytics to manage and save data from threats. For instance, According to Seagate Technology PLC, the global volume of data is expected to increase to 47 zettabytes and 163 zettabytes in 2020 and 2025.

- Moreover, cloud computing is driving a software revolution astonishingly as any other computing revolution of the past 40 years. As analytics for location-based risk advance, it is only sensible that they can be built and delivered using cloud-based technology rather than older server-based systems. There are several risk assessment and accumulation platforms available now through the cloud. Rules-based approaches to security, whether they are applied to threat detection, investigation, or response, can no longer keep pace with advanced cyber threats, including account compromise and malicious insiders.

- The demand for risk analytics in the banking, financial services, and insurance (BFSI) sector is also fueled by the increased use of mobile banking services and the rising volume of data. Risk analytics can be applied to combine the data into a single, comprehensive perspective, collect essential data, and produce insights that can be put to use. In addition, risk analytics are critical for logistics firms worldwide to efficiently address business disruptions and supply chain issues brought on by the spread of the coronavirus disease internationally.

- Furthermore, players cater to provide new analytics solutions, majorly in the healthcare sector, to combat COVID-19. Laboratory testing influences a significant percentage of clinical decisions and plays an essential role in improving care for patients with common, high-risk conditions. For example, LabCorp launched Insight Analytics reports that support provider organizations are delivering improved care, both individually and on a population level, for a range of high-risk health conditions.

Risk Analytics Market Trends

BFSI is Expected to Witness Huge Adoption of Risk Analytics Solutions

- Banks across the world are realizing that they need a more rational approach to managing a growing plethora of risks enveloping the banking and financial industries' landscape, and they have now understood the significance of risk analytics.

- Risk analytics enables banks and financial institutions to move away from the 'silo' approach to risk management and move toward the comprehensive view of enterprise-wide risks. For instance, in operational risk management (ORM), the number of transactions that need to be monitored is growing exponentially, thus implying pressure on the current banking infrastructure and enabling the market for risk analytics.

- Financial Organizations are under intense pressure to reduce fraud and meet strict regulatory compliance requirements while growing their business. Moreover, New Account Fraud and Account Takeover are the top two types of fraud challenging financial institutions today. Risk analytics solutions protect against these and other fraudulent activities across online and mobile channels, using machine learning-based risk analysis, a form of AI.

- Data analytics can be used in a variety of ways by banks to protect themselves from danger. Customer analytics, for instance, can be used to categorize customers according to their creditworthiness for credit risk management. Because one can rely on those customers to make payments on time, doing so lets individuals choose a target market for credit products and lowers exposure to default risk. According to the Global Association of Risk Professionals, it is estimated that capital markets, banking, and insurance sectors are likely to spend USD 96 billion on risk information technologies and services.

- Additionally, the Grant Thornton survey study identified that 85% of respondents believed that their bank's data and risk information management initiatives need additional efficiencies to realize their full potential. Furthermore, 82% had indicated the same for their institution's risk analytics and measurements. Hence, such trends drive the need for risk analytics solutions in the BFSI industry.

North America is Expected to Hold a Significant Share

- North America is expected to hold the highest market share, with the United States leading the market. The dominance of the region is due to its increasing adoption of risk analytics solutions among end-user industries, a significant presence of large enterprises, and drive for early technological adoption owing to competition from other businesses operating in low-cost regions.

- Moreover, adopting cloud computing across industries is driving market growth. The task of protecting Healthcare Information Systems (HIS) from immediate cyber security risks has been intertwined with cloud computing adoption. The data and resources of HISs are inherently shared with other systems for remote access, decision-making, emergency, and other healthcare-related perspectives.

- Additionally, there have been 28 data breach incidents reported during the pandemic year in the United States, including email hacking incidents, malware attacks, and unauthorized access to EHRs (source the US Department of Health & Human Services). In the medical healthcare sector, cloud computing is considered to be an immediate remedy because it is scalable as well as economical.

- The healthcare infrastructure in the United States is experiencing positive trends in the predictive analytics domain. Studies have shown that in the last few years, more than 40% of healthcare executives reported a 50% increase in data volume. As the data sets become bigger and more difficult to handle, health systems and payers increasingly adopt predictive analytics.

- Moreover, the region has a strong foothold of risk analytics vendors, which contributes to the growth of the market. Some of them include IBM Corporation, Oracle Corporation, SAS Institute Inc., and AxiomSL Ltd, among others.

Risk Analytics Industry Overview

The risk analytics market is a relatively consolidated market as the major vendors account for a significant share of the market, especially in the enterprise-level adoption. Additionally, large companies dominate this market owing to their ability to offer innovative and high-quality services to end-users on a different scale and with customization that suits their specific needs. IBM Corporation, SAP SE, SAS Institute Inc., Oracle Corporation, Accenture PLC and Adenza Group Inc. (previosuly AxiomSL Ltd.) are a few prominent players operating in the market.

In November 2023, Renew Risk, a Software-as-a-Service (SaaS) risk analytics supplier, and GCube Insurance, a prominent insurance company for renewable energy projects, announced a strategic partnership. GCube's offshore wind clients will significantly benefit from this partnership, strengthening the company's capacity for offshore wind risk analytics and modeling. GCube will benefit from this agreement by utilizing Renew Risk's advanced catastrophe risk models, which are tailored for offshore wind portfolios.

In September 2023, Axioma, a global supplier of corporate risk solutions, portfolio construction tools, and factor risk models, announced a new partnership with Jacobi Inc. The San Francisco-based company Jacobi's technology enables dynamic client engagement, optimizes investing operations, and simplifies multi-asset portfolio building and maintenance. With this single workflow-integrated solution, investment managers can readily access time series and point-in-time risk data for factor-based decomposition across equity and multi-asset class portfolios.

In October 2022, Goldman Sachs Group, Inc., a top global investment banking, securities, and investment management organization, and Qontigo, a leading innovative risk, analytics, and index solutions provider, announced an expanded partnership. Through Goldman Sachs Financial Cloud for Data, a collection of modular data management and analytics solutions, as well as Goldman Sachs Marquee, the company's digital platform that offers market-leading data, analytics, market insights, and trading solutions to institutional investors, Qontigo would now make the Axioma Portfolio Optimize and Axioma Equity Factor Risk Models available.

In September 2022, A collaborative alliance was launched between CAMELOT Management Consultants and Everstream Analytics, a prominent provider of supply chain insights and risk analytics. This partnership combines Everstream's superior risk ratings and AI-powered analytics with CAMELOT's unrivaled strategic process design and organizational knowledge to create high-performing, compliant, resilient value chains.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Scope

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Market Drivers

- 4.4.1 Growing Complexities across Business Processes

- 4.4.2 Global Regulatory Frameworks and Government Policies

- 4.5 Market Restraints

- 4.5.1 High Installation and Operational Costs

- 4.5.2 Complicated Regulatory Compliance might hinder the Market Growth

- 4.6 Impact of COVID-19 on Overall Market

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 Solution

- 5.1.2 Service

- 5.2 By Deployment

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.3 By End-user Vertical

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 Retail

- 5.3.4 Manufacturing

- 5.3.5 Other End-user Verticals (IT and Telecom)

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 UK

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Mexico

- 5.4.4.3 Argentina

- 5.4.4.4 Rest of Latin America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 UAE

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of MEA

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles*

- 6.1.1 IBM Corporation

- 6.1.2 Oracle Corporation

- 6.1.3 SAP SE

- 6.1.4 SAS Institute Inc.

- 6.1.5 Moody's Analytics Inc.

- 6.1.6 OneSpan Inc.

- 6.1.7 Capgemini SE

- 6.1.8 Accenture PLC

- 6.1.9 Risk Edge Solutions

- 6.1.10 Adenza Group Inc. (AxiomSL Ltd.)

- 6.1.11 Provenir Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

风险分析市场规模、份额和成长分析:按风险类型、按产品、按风险阶段、按行业、按地区 - 行业预测,2024-2031 年

风险分析市场规模、份额和成长分析:按风险类型、按产品、按风险阶段、按行业、按地区 - 行业预测,2024-2031 年 2024-2032 年按组件、部署模式、组织规模、应用程式、垂直产业和区域分類的风险分析市场报告

2024-2032 年按组件、部署模式、组织规模、应用程式、垂直产业和区域分類的风险分析市场报告 2024-2028 年全球风险分析市场

2024-2028 年全球风险分析市场 风险分析市场 - 2019-2029 年按组件、部署、最终用户、地区和竞争细分的全球行业规模、份额、趋势、机会和预测

风险分析市场 - 2019-2029 年按组件、部署、最终用户、地区和竞争细分的全球行业规模、份额、趋势、机会和预测 风险分析市场规模、份额、趋势分析报告:按组件、按风险类型、按应用、按部署类型、按行业、按地区和按细分市场预测,2024-2030 年

风险分析市场规模、份额、趋势分析报告:按组件、按风险类型、按应用、按部署类型、按行业、按地区和按细分市场预测,2024-2030 年 风险分析市场规模 - 按组件、部署模式、组织规模、垂直领域和预测,2024 年 - 2032 年

风险分析市场规模 - 按组件、部署模式、组织规模、垂直领域和预测,2024 年 - 2032 年 全球风险分析市场:按产品、按风险类型、按风险阶段、按行业、按地区 - 预测(至 2029 年)

全球风险分析市场:按产品、按风险类型、按风险阶段、按行业、按地区 - 预测(至 2029 年) 风险分析市场:按组成部分、按风险类型、按部署、按行业 - 2024-2030 年全球预测

风险分析市场:按组成部分、按风险类型、按部署、按行业 - 2024-2030 年全球预测 2024 年风险分析世界市场报告

2024 年风险分析世界市场报告 全球风险分析市场研究报告 - 2023 年至 2030 年产业分析、规模、份额、成长、趋势与预测

全球风险分析市场研究报告 - 2023 年至 2030 年产业分析、规模、份额、成长、趋势与预测