|

市场调查报告书

商品编码

1432826

化学喷射泵和阀门:市场占有率分析、行业趋势和成长预测(2024-2029)Chemical Injection Metering Pumps And Valves - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

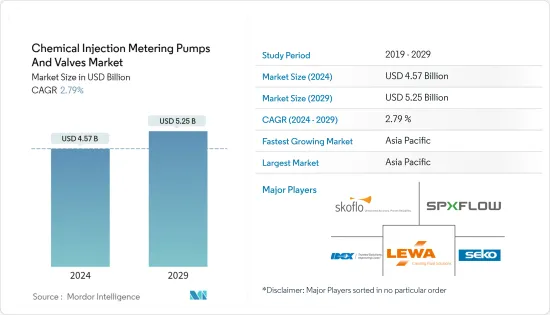

化学计量帮浦和阀门市场规模预计到2024年为45.7亿美元,预计到2029年将达到52.5亿美元,复合年增长率预计为2.79%。

2020 年,COVID-19 爆发导致全国封锁、製造活动和供应链中断以及全球生产停顿,对市场产生了负面影响。然而,到了2021年,情况开始好转,市场恢復了成长轨迹。

主要亮点

- 市场研究的主要驱动力之一是污水处理应用需求的不断增长。

- 然而,某些应用的高维护和更换成本预计将阻碍市场成长。

- 能源、电力和化学产业在市场中占据主导地位,预计在预测期内将成长。用水和污水处理产业预计在未来几年仍将保持最高的复合年增长率。

- 亚太地区占市场主导地位,其次是北美和欧洲,中国、日本和印度等国家的消费量最高。

- 製药业不断增长的需求可能会提供未来的机会。

化工计量帮浦和阀门市场趋势

能源、电力和化学品主导市场

- 能源、电力和化学是喷射计量泵和阀门市场的主要最终用户领域。纸浆和造纸工业也包含在该细分市场中。

- 化学工业包括最终产品的合成。计量泵和阀门可用于在不同温度和化学处理压力下处理各种有毒化学物质。

- 化学注入系统也用于发电。硫酸铁和硫酸等化学物质需要精确测量,才能将水转化为锅炉用超纯水。

- 在法国,从美国和中东国家的进口满足了大部分石油产品的需求。在法国,大约有60%的能源被用作化石资源。能源来源主要是石油产品、天然气和煤炭。因此,能源产出依赖从沙乌地阿拉伯、俄罗斯、哈萨克、阿尔及利亚和奈及利亚进口原油,以及从俄罗斯、挪威、奈及利亚和荷兰进口天然气。

- 法国消耗的石油95%以上是从其他国家进口的。大部分石油是从俄罗斯进口以满足法国的需求。然而,自从俄罗斯和乌克兰战争爆发以来,欧盟一直在寻找将俄罗斯石油赶出欧洲市场的方法。由于法国是欧盟最大的石油进口国之一,法国政府已经在加紧与阿联酋的谈判,以取代购买俄罗斯石油。

- 大多数石化设施利用产生的热量来运作锅炉并满足现场电力需求。

- 根据美国人口普查局的数据,2022 年采矿和采石业收益达到 143.9 亿美元,而 2021 年为 136.8 亿美元。预计 2023 年该产业收益将达到 152.5 亿美元。

- 采矿和冶金是加拿大的主要工业。加拿大向世界各国供应 60 多种金属和矿物。采矿业正在投资创新和新技术,迅速重塑这个产业。采矿业也出现了整合,引发了对该行业未来几年成长前景的猜测。

- 在电力工业中,例如火力发电厂和核能发电厂,通常需要化学物质来向锅炉系统供水。

- 能源、电力和化学产业的成长以及投资的增加可能会推动预测期内对调查市场的需求。

中国在亚太地区市场占据主导地位

- 预计亚太地区将主导化学计量泵和阀门的需求。光是中国就占了亚太市场的约35%。

- 石油和天然气计量泵和阀门消耗量较高,国家正在增加下游生产和石化产能。

- 中国其他突出的最终用户产业是化工厂,市场上许多大公司在中国设有化工厂,它们进一步增加了所生产的化学品喷射计量泵和阀门的消耗量和产能。其他主要行业是生活水处理设施,用于各个行业。

- 污水处理主要是因为煤炭、钢铁和钢铁业的日常活动需要淡水。中国北方地区拥有全国约90%的煤炭相关产业。

- 中国政府颁布了用水和排放法规,以改善该地区宝贵的水资源。最近,政府加强了对华北地区煤炭和化工厂的监管,要求实现零液体排放(ZLD)。

- 中国食品和饮料产业规模庞大,在国家经济中扮演重要角色。由于具有购买力的中产阶级人口不断增长以及对食品安全和品质的日益关注,食品和饮料行业预计将继续增长。

- 在上游石油和天然气行业,製造商不断寻求提高产能、整体流程效率和机器停机时间。石油和天然气公司使用化学注入计量泵和阀门来提高产量、减少腐蚀、分离石油、天然气和水,并提高所有探勘和采收活动的盈利。

- 儘管中国是世界第二大石油和天然气消费国,但仅是第六大生产国。中国作为石油消费量大国,石油消费量逐年增加,成长速度不一。但由于石油供应仍无法满足需求,中国主要依赖进口。

- 在预测期内,上述各种最终用户产业的成长预计将推动该国对化学喷射计量帮浦和阀门的需求。

化学品注入泵和阀门行业概述

全球化学品计量泵和阀门市场高度分散,五家主要企业的市场占有率非常小。主要公司包括 Idex Corporation、SPX Flow、Lewa GmbH、SkoFlo Industries Inc. 和 Seco SpA。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 污水处理应用的需求不断增加

- 健全的环境监管操作程序

- 其他司机

- 抑制因素

- 维护和更换成本很高,取决于应用

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(金额:市场规模)

- 泵浦类型

- 隔膜

- 活塞/柱塞

- 其他泵浦类型

- 最终用户产业

- 能源、动力、化学

- 油和气

- 水和污水处理

- 食品和饮料

- 製药

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 澳洲和纽西兰

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 俄罗斯

- 西班牙

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲

- 亚太地区

第六章 竞争形势

- 併购、合资、联盟、协议

- Market Ranking/Share(%)Analysis

- 主要企业策略

- 公司简介

- Cameron(Schlumberger)

- Hunting PLC

- Idex Corporation

- ITC Dosing Pumps

- Lewa GmbH

- McFarland-Tritan LLC

- Milton Roy

- ProMinent

- Seepex GmbH

- Seko SpA

- SkoFlo Industries Inc.

- SPX FLOW Inc.

- Swelore Engineering Pvt Ltd.

第七章 市场机会及未来趋势

- 製药业需求不断成长

- 开发技术先进的化学注入系统

The Chemical Injection Metering Pumps And Valves Market size is estimated at USD 4.57 billion in 2024, and is expected to reach USD 5.25 billion by 2029, growing at a CAGR of 2.79% during the forecast period (2024-2029).

Due to the COVID-19 outbreak, nationwide lockdowns worldwide, disruption in manufacturing activities and supply chains, and production halts negatively impacted the market in 2020. However, the conditions started recovering in 2021, restoring the market's growth trajectory.

Key Highlights

- One of the major factors driving the market study is the accelerating demand for wastewater treatment applications.

- However, high maintenance and replacement costs in some applications are expected to hinder the market's growth.

- The energy, power, and chemicals industry dominated the market and is expected to grow during the forecast period. The water and wastewater treatment industry is expected to register the highest CAGR in the coming years.

- Asia-Pacific dominated the market, followed by North America and Europe, with the largest consumption from countries such as China, Japan, and India.

- Growing demand from the pharmaceutical industry will likely act as an opportunity in the future.

Chemical Injection Metering Pumps & Valves Market Trends

Energy, Power, and Chemicals to Dominate the Market

- Energy, power, and chemicals are major end-user segments in the injection metering pumps and valves market. Even the pulp and paper industry is considered in this segment.

- The chemical industry consists of the synthesis of finished or intermediate products. Metering pumps and valves help handle various toxic chemicals at different temperatures and chemical processing pressures.

- Chemical injection systems also find major use in power generation. Chemicals, such as ferric sulfate and sulphuric acid, are needed in precise measurements to transform water into ultra-pure water for boilers.

- In France, imports from the United States and Middle Eastern countries meet most of the demand for petroleum products. Around 60% of the energy is utilized in the form of fossil resources in France. Energy is primarily derived from petroleum products, natural gas, and coal. Hence energy generation depends on imports from Saudi Arabia, Russia, Kazakhstan, Algeria, and Nigeria for crude oil while upon Russia, Norway, Nigeria, and the Netherlands for gas.

- Over 95% of the oil consumed in France is imported from other nations. A large share of oil is imported from Russia to fulfill the country's demand. However, since the onset of the Russia-Ukraine war, European Union has been finding ways to push out Russian oil from the European market. Since France is one of the largest oil importers in the European Union, the French government has already strengthened talks with United Arab Emirates (UAE) to replace Russian oil purchases.

- Most petrochemical facilities use generated heat to run boilers to meet site power requirements.

- As per the United States Census Bureau, revenue in mining and quarrying amounted to USD 14.39 billion in 2022, compared to USD 13.68 billion in 2021. The revenue from this sector is projected to amount to USD 15.25 billion in 2023.

- Mining and metallurgy are key industries in the country. Canada supplies over 60 metals and minerals to different countries worldwide. The mining industry invests in innovation and new technologies, rapidly reshaping the sector. The mining industry also witnessed consolidations, which led to speculations regarding the growth prospects for the industry in the coming years.

- Power industries, such as thermal and nuclear plants, often require chemicals to inject the feed water into the boiler system.

- The growth in the energy, power, and chemicals sectors with increasing investments is likely to drive the demand in the market studied during the forecast period.

China to Dominate the Market in Asia-Pacific Region

- Asia-Pacific region is expected to dominate the demand for chemical injection metering pumps and valves. China alone accounts for about 35% of the market in the Asia-Pacific region.

- The consumption of metering pumps and valves is high in oil and gas; the downstream production has increased in the country, which has also increased the production capacities of petrochemicals; therefore, it will augment the consumption of chemical injection metering pumps and valves in the country.

- The other end-user industry prominent in China is the chemical plants, many big companies in the market have their chemical plants in China, and they have even increased their production capacities, which will increase the consumption of chemical injection metering pumps and valves. The other major industry is a water treatment facility in the country, used in different industries.

- Wastewater treatment is mainly because the coal, steel, and iron industries require fresh water for daily activities. North China has approximately 90% of the country's coal-based industries.

- The Chinese government has enacted water use and discharge regulations to improve the region's precious water resources. Recently, the government has tightened the rules for coal and chemical plants in North China, which require zero-liquid discharge (ZLD).

- China's food and beverage industry is enormous and plays an important role in the country's economy. The food and beverages industry is expected to continue growing because of the increasing middle-class population with more purchase power and growing attention to food safety and quality.

- In the upstream Oil & Gas industry, manufacturers constantly seek to improve their production capacities, overall process efficiency, and machinery downtime. Oil and gas companies use chemical Injection metering pumps and valves to increase production, reduce corrosion, separate oil/gas/water, and improve the profitability of all exploration and recovery efforts.

- China is the world's second-largest consumer of oil and gas but only the sixth-largest producer of the same. As a big oil consumer, China's oil consumption is increasing yearly with fluctuating growth rates. However, China mainly relies on imports because the oil supply still cannot meet the demand.

- The growth in those mentioned above various end-user industries in the forecast period is expected to boost the demand for chemical injection metering pumps and valves in the country.

Chemical Injection Metering Pumps & Valves Industry Overview

The global chemical injection metering pumps and valves market is highly fragmented, with the top 5 players accounting for a very small market share. The major companies include Idex Corporation, SPX Flow, Lewa GmbH, SkoFlo Industries Inc., and Seko SpA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Accelerating Demand from Wastewater Treatment Applications

- 4.1.2 Robust Operational Procedures for Regulating Environmental Concerns

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Maintenance and Replacement Costs in Some Applications

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Pump Type

- 5.1.1 Diaphragm

- 5.1.2 Piston/Plunger

- 5.1.3 Other Pump Types

- 5.2 End-user Industry

- 5.2.1 Energy, Power, and Chemicals

- 5.2.2 Oil and Gas

- 5.2.3 Water and Wastewater Treatment

- 5.2.4 Food and Beverage

- 5.2.5 Pharmaceutical

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Australia and New Zealand

- 5.3.1.7 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Spain

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking/Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Cameron (Schlumberger)

- 6.4.2 Hunting PLC

- 6.4.3 Idex Corporation

- 6.4.4 ITC Dosing Pumps

- 6.4.5 Lewa GmbH

- 6.4.6 McFarland-Tritan LLC

- 6.4.7 Milton Roy

- 6.4.8 ProMinent

- 6.4.9 Seepex GmbH

- 6.4.10 Seko SpA

- 6.4.11 SkoFlo Industries Inc.

- 6.4.12 SPX FLOW Inc.

- 6.4.13 Swelore Engineering Pvt Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand in the Pharmaceutical Industry

- 7.2 Development of Technologically Advanced Chemical Injection Systems

计量泵市场报告(按类型(隔膜泵、活塞泵等)、应用(水和废水处理、石油和天然气、化学製程、製药、食品和饮料、造纸和纸浆等)和地区 2024-2032

计量泵市场报告(按类型(隔膜泵、活塞泵等)、应用(水和废水处理、石油和天然气、化学製程、製药、食品和饮料、造纸和纸浆等)和地区 2024-2032 2024 年计量帮浦全球市场报告

2024 年计量帮浦全球市场报告 计量帮浦市场规模、份额、趋势分析报告:按类型、最终用途、地区、细分市场预测,2024-2030 年

计量帮浦市场规模、份额、趋势分析报告:按类型、最终用途、地区、细分市场预测,2024-2030 年 全球计量帮浦市场:按类型、最终用途产业、泵浦驱动器、地区 - 预测(至 2028 年)

全球计量帮浦市场:按类型、最终用途产业、泵浦驱动器、地区 - 预测(至 2028 年) 到 2030 年计量帮浦市场预测:按细分市场和地区分類的全球分析

到 2030 年计量帮浦市场预测:按细分市场和地区分類的全球分析 2023-2027年全球计量帮浦市场

2023-2027年全球计量帮浦市场 2023-2030年全球计量泵市场规模研究与预测,按类型(隔膜、活塞/柱塞、其他、终端用户行业、泵驱动和区域分析)划分

2023-2030年全球计量泵市场规模研究与预测,按类型(隔膜、活塞/柱塞、其他、终端用户行业、泵驱动和区域分析)划分 计量泵市场:按泵驱动装置、类型和最终用途行业 - COVID-19、俄罗斯-乌克兰衝突和高累积的累积影响 - 2023-2030 年全球预测

计量泵市场:按泵驱动装置、类型和最终用途行业 - COVID-19、俄罗斯-乌克兰衝突和高累积的累积影响 - 2023-2030 年全球预测 计量泵市场:2023-2028 年全球行业趋势、份额、规模、增长、机遇和预测

计量泵市场:2023-2028 年全球行业趋势、份额、规模、增长、机遇和预测 定量帮浦的全球市场

定量帮浦的全球市场