|

市场调查报告书

商品编码

1432850

农业收割机械:全球市场占有率分析、产业趋势与统计、成长预测(2024-2029)Global Agricultural Harvesting Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

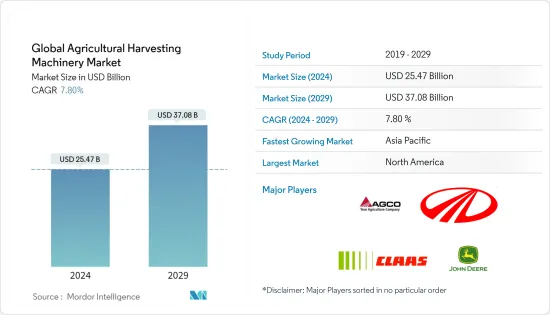

预计2024年全球农业收割机械市场规模为254.7亿美元,预计2029年将达370.8亿美元,在预测期内(2024-2029年)复合年增长率为7.80%,预计将成长。

主要亮点

- 在印度等新兴经济体,农业劳动力稀缺、农机技术进步以及政府支持农机购买的各种补贴政策正在推动收割机械市场的成长。

- 高昂的初始资本成本和农民对传统种植方法的偏好限制了市场的成长。

- Deere & Company(约翰迪尔)、AGCO Corporation、CNH Industrial NV、Mahindra & Mahindra Limited 是该市场的一些主要企业。

收割机械市场趋势

精密农业实现高品质收成

由于需要高品质收割以提高产量和生产率,收割机配备了多种先进功能,包括用于监控收割负载的增强型电子感测、云端基础的产量处理和品质地图。农业技术正在不断发展。据CEMA称,新销售的农业机械和收割机中有70%至80%配备了精密农业技术。对配备技术开发工具的收割机的需求不断增长进一步体现在欧洲等地区联合收割机的进口总额,从2016年的341万美元增加到2018年的4.1亿美元,增加到1000万美元。因此,持续的精密农业趋势预计将在预测期内增加对收割机的需求。

亚太地区是一个快速成长的市场

由于不断增长的工业部门的利润丰厚的机会,农业活动的劳动力资源严重短缺,这是推动该地区收割机等农业机械设备成长的主要因素。除此之外,各国政府也向农民提供补贴,以投资更好的设备,以有效满足更高的生产力需求。例如,印度政府透过 Rashtriya Krishi Vikas Yojna (RKVY) 等计画和国家粮食安全任务 (NFSM) 下的机械化计画在该国启动了各种农业机械化计画。透过这些计划,政府向农民提供补贴,鼓励他们购买收割机等农业机械。因此,随着更多国际公司在预测期内扩大在该地区的业务,推出收割机,收割机的需求预计将进一步增加。

收割机产业概况

全球收割机市场分散,国际参与者和众多区域参与者在该市场运作。 Deere & Company(约翰迪尔)、AGCO Corporation、CNH Industrial NV 和 Mahindra & Mahindra Limited 是该市场的一些主要企业。这些参与者将产品创新作为关键策略,推出具有针对不同地区顾客需求的功能的收割机。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究成果

- 研究场所

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 市场驱动因素

- 市场限制因素

- 波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔

- 透过机器

- 联合收割机

- 饲料收割机

- 甘蔗收割机

- 其他收割机

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 其他北美地区

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 西班牙

- 其他欧洲国家

- 亚太地区

- 印度

- 中国

- 日本

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 非洲

- 南非

- 其他非洲

- 北美洲

第六章 竞争形势

- 最采用的策略

- 併购

- 公司简介

- Deere & Company

- CNH Industrial

- AGCO Corporation

- CLAAS KGaA mbH

- Mahindra & Mahindra(Tractors)

- Krone NA, Inc.

- Yanmar Co., Ltd.

- KUBOTA Corporation

- Tractors and Farm Equipment Limited

- Bernard Krone Holding GmbH & Co. KG

第七章 市场机会及未来趋势

The Global Agricultural Harvesting Machinery Market size is estimated at USD 25.47 billion in 2024, and is expected to reach USD 37.08 billion by 2029, growing at a CAGR of 7.80% during the forecast period (2024-2029).

Key Highlights

- The acute shortage of farm labor, the technological advancements in agricultural machinery and various government backedsubsidy policies supporting the purchase of farming machinery in developing economies such as India is driving the market growth for harvestors.

- The high initial capital cost and more inclination of farmers towards traditinal plowing methods are some of the factors restraining the market growth.

- Deere & Company (John Deere), AGCO Corporation, CNH Industrial N.V and Mahindra & Mahindra Limited are some of the major players who have their presence in this market.

Harvesting Machinery Market Trends

Precision Farming for Quality Harvest

The need for quality harvest with an increased yield and productivity has led to the evolution of several advanced farming technologies in harvesters, such as increased electronic sensing to monitor harvest load, cloud-based processing for yield, and quality maps, among others. According to CEMA, 70%-80% of the new agricultural machinery and harvesters sold have been found to be equipped with precision farming technology. The increasing demand for harvesters equipped with technologically developed tools is further reflected through the total import value of combine harvesters in the region such as Europe, where imports rose from USD 3.41 million in 2016 to USD 4.10 million in 2018. As such, the ongoing trend of precision farming is projected to increase the demand for harvesters duing the forecast period.

Asia Pacific is the Fastest growing market

The acute shortage of labor resources for agricultural activities, owing to the lucrative opportunities in the growing industrial sector, is the major factor driving the growth of agricultural machinery equipment, such as harvesters in the region. In additin to this various governments are providing subsidies to farmers for investing in better equipment to efficiently meet the needs for higher productivity. For instance, Government of India inititated various farm mechanization programs in the country through the schemes, such Rashtriya Krishi Vikas Yojna (RKVY) and Mechanisation, under the National Food Security Mission (NFSM). Through these schemes, the government is encouraging farmers to purchase farm machinery, such as harvesters, by providing a subsidy. Thus, the demand for harvestor machines is projected to increase further with number of international companies launching their harvesting machinery by expanding their business in the region during the forecast period.

Harvesting Machinery Industry Overview

The global harvesting machinery market is fragmented with the presence of international players and numerous regional players operating in this market. Deere & Company (John Deere), AGCO Corporation, CNH Industrial N.V and Mahindra & Mahindra Limited are some of the major players who have their presence in this market. These players are using product innovation as their key strategy by launching harvestors with tailored featurescatering the needs of customers across various regions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porters five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Machinery

- 5.1.1 Combine Harvester

- 5.1.2 Forage Harvester

- 5.1.3 Sugar cane Harvester

- 5.1.4 Other Harvestors

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 US

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.1.4 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 UK

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia Pacific

- 5.2.3.1 India

- 5.2.3.2 China

- 5.2.3.3 Japan

- 5.2.3.4 Rest of Asia Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Africa

- 5.2.5.1 South Africa

- 5.2.5.2 Rest of Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Mergers & Acquisitions

- 6.3 Company Profiles

- 6.3.1 Deere & Company

- 6.3.2 CNH Industrial

- 6.3.3 AGCO Corporation

- 6.3.4 CLAAS KGaA mbH

- 6.3.5 Mahindra & Mahindra (Tractors)

- 6.3.6 Krone NA, Inc.

- 6.3.7 Yanmar Co., Ltd.

- 6.3.8 KUBOTA Corporation

- 6.3.9 Tractors and Farm Equipment Limited

- 6.3.10 Bernard Krone Holding GmbH & Co. KG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

收割机械市场规模、份额、成长分析、2025-2032 年产业预测(按产品类型、形式、种类、应用和地区)

收割机械市场规模、份额、成长分析、2025-2032 年产业预测(按产品类型、形式、种类、应用和地区) 甘蔗收割机市场(按产品类型、动力来源、最终用户和分销管道)—2025-2032 年全球预测

甘蔗收割机市场(按产品类型、动力来源、最终用户和分销管道)—2025-2032 年全球预测 2025年全球甘蔗收割机市场报告2025年全球自动收割系统市场报告

2025年全球甘蔗收割机市场报告2025年全球自动收割系统市场报告 收割设备市场-全球产业规模、份额、趋势、机会和预测(按产品、应用、地区和竞争细分,2020-2030 年)

收割设备市场-全球产业规模、份额、趋势、机会和预测(按产品、应用、地区和竞争细分,2020-2030 年) 全球自动收割机市场

全球自动收割机市场 全球自动收割机市场:预测至 2032 年-按产品类型、自动化程度、推进方式、运作地点、作物类型、技术、最终使用者和地区进行分析收割机市场-全球产业规模、份额、趋势、机会和预测,按类型、按自动化程度、按推进类型、按地区和竞争细分,2020-2030 年全球农业收割机市场

全球自动收割机市场:预测至 2032 年-按产品类型、自动化程度、推进方式、运作地点、作物类型、技术、最终使用者和地区进行分析收割机市场-全球产业规模、份额、趋势、机会和预测,按类型、按自动化程度、按推进类型、按地区和竞争细分,2020-2030 年全球农业收割机市场 收割机市场规模、份额及成长分析(按机制、功率、等级、类型、自动化程度和地区)-2025-2032 年产业预测

收割机市场规模、份额及成长分析(按机制、功率、等级、类型、自动化程度和地区)-2025-2032 年产业预测