|

市场调查报告书

商品编码

1432868

氢气压缩机:市场占有率分析、产业趋势、成长预测(2024-2029)Hydrogen Compressor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

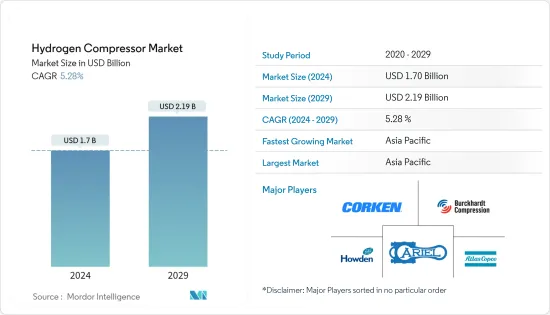

氢压缩机市场规模预计到 2024 年为 17 亿美元,预计到 2029 年将达到 21.9 亿美元,在预测期内(2024-2029 年)复合年增长率为 5.28%。

主要亮点

- 从中期来看,化肥和精製等终端用户产业对氢气的需求不断增加,以及全球运输用氢气管道基础设施的部署不断增加等因素预计将在预测期内推动氢气压缩机市场的发展。

- 另一方面,由于关税上升和贸易政策长期不确定性导致製造业活动急剧下降,以及全球贸易低迷导致工业和经济活动放缓,将减少使用资本货物的行业对资本财的需求。氢:预计这将减少所研究市场的成长。

- 然而,技术进步和透过电解生产氢气的新来源与太阳能和风能等清洁能源相结合,可能为市场成长提供充足的机会。

- 在预测期内,亚太地区预计将主导氢气压缩机市场,大部分需求来自中国、印度和日本。

氢气压缩机市场趋势

油基型细分市场占据主导地位

- 油基润滑压缩机比无油压缩机具有更低的成本和更长的使用寿命,对油污染非常敏感,不适合商业和工业应用,除非该行业需要无油压缩机,被认为是最佳选择。

- 油基压缩机比无油压缩机效率更高,因为油充当冷却介质,在压缩过程中带走压缩机约 80% 的热量,使其适用于需要高压缩比的工业应用。 。

- 就资本支出而言,润滑油压缩机被认为比无油压缩机便宜,价差通常在 30-40% 范围内。根据容量和特定产业要求等因素,甚至可以达到 50%,从而导致对油基氢气压缩机的需求增加。

- 油基压缩机比无油压缩机更实惠,但需要持续维护并更加註意更换过滤器和其他零件,以消除漏油的风险。持续的油污染可能会产生严重后果,包括产品污染、安全性降低、生产停顿和法律问题。

- 油基氢气压缩机主要首选製造业,如玻璃精製、钢铁工业、半导体製造、金属焊接、退火、热处理、发电厂(发电机冷却水)、航太应用、製药等。

- 根据美国地质调查局估计,2022年美国原钢产量预估为8,200万吨。随着工业化的发展,钢铁产量可能会继续增加,这也可能产生对油基氢气压缩机的需求。

- 由于缺乏润滑而导致氢气压缩机零件过早磨损的威胁仍然存在,这会增加维护成本并限制对油基氢气压缩机的需求。

- 因此,在预测期内,油基型预计将主导氢气压缩机市场。

亚太地区预计将主导市场

- 由于中国、日本和印度等国家的有利政府政策,预计亚太地区在未来几年将成为燃料电池的一个充满前景的市场。

- 中国是全球最大、成长最快的氢气压缩机市场之一。近年来,该国的化学、石油、天然气和製造业经历了显着成长。

- 氢气离心压缩机用于精製和石化行业,例如乙烯厂,用于裂解气压缩和冷冻服务。由于乙烯和苯产量短缺,国家正在投资增加乙烯和苯产能。

- 例如,2022 年 5 月,诺伊曼埃塞尔北京向中国内蒙古三修復材料公司 (CIMSNM) 供应了四套压缩机系统。该压缩机似乎在 1,4-丁二醇 (BDO) 生产过程中用于氢气增压和回收。 BDO 用作溶剂,用于生产某些聚合物、弹性纤维和聚氨酯。

- 日本开拓氢燃料电池汽车新兴市场和建造加氢站为氢燃料电池汽车充电的目标预计将推动氢压缩机市场的发展。

- 例如,在日本,包括汽车製造商和能源公司在内的11家国内企业已组成联盟,决定在2022年建造80座氢燃料电池汽车加氢站,以打造下一代燃料电池汽车市场。截至2021年9月,日本有154座加氢站,还有11座处于规划和建设阶段。预计这将在预测期内推动加氢站对氢气压缩机的需求。

- 因此,由于这些因素,预计亚太地区在预测期内将主导氢气压缩机市场。

氢气压缩机产业概况

氢气压缩机市场较为分散。着名公司包括(排名不分先后)Corken Inc.、Ariel Corporation、Burckhardt Compression AG、Howden Group Ltd 和 Atlas Copco Group。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 2028年之前的市场规模和需求预测(金额)

- 最新趋势和发展

- 政府法规政策

- 市场动态

- 促进因素

- 最终用户产业对氢气的需求增加

- 增加交通运输氢气管道基础设施的部署

- 抑制因素

- 由于製造业活动和世界贸易急剧下降,工业和经济活动放缓

- 促进因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔

- 科技

- 单级

- 多级

- 类型

- 油腻的

- 不含油

- 最终用户产业

- 化学

- 油和气

- 其他最终用户产业

- 按地区分類的市场分析(到 2028 年的市场规模和需求预测(仅按地区))

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 亚太地区

- 印度

- 中国

- 日本

- 其他亚太地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章 竞争形势

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- Corken Inc.

- Ariel Corporation

- Burckhardt Compression AG

- Hydro-Pac Inc.

- Haug Kompressoren AG

- Sundyne Corp.

- Howden Group Ltd

- Indian Compressors Ltd

- Atlas Copco Group

- Ingersoll Rand Inc.

第七章 市场机会及未来趋势

- 技术进步与氢气产生新来源

简介目录

Product Code: 54577

The Hydrogen Compressor Market size is estimated at USD 1.7 billion in 2024, and is expected to reach USD 2.19 billion by 2029, growing at a CAGR of 5.28% during the forecast period (2024-2029).

Key Highlights

- Over the medium term, factors such as the increase in demand for hydrogen from end-user industries, such as fertilizers and oil refineries, and increasing deployment of hydrogen pipeline infrastructure globally for transportation are likely to drive the hydrogen compressor market during the forecast period.

- On the other hand, the slowdown in industrial and economic activities due to a sharp decline in manufacturing activity and global trade, with higher tariffs and prolonged trade policy uncertainty, is expected to decrease the demand for capital goods from industries using hydrogen, thereby restraining the growth of the market studied.

- Nevertheless, the technological advancements and emerging sources for hydrogen production using electrolysis in combination with cleaner sources, such as solar and wind, are likely to provide ample opportunities for the market's growth.

- Asia-Pacific is expected to dominate the hydrogen compressor market during the forecast period, with the majority of the demand coming from China, India, and Japan.

Hydrogen Compressor Market Trends

Oil-based Type Segment Expected to Dominate the Market

- Oil-based lubricated compressors cost less, provide a longer service life compared to oil-free compressors, and are considered ideal for commercial and industrial applications until and unless in industries where consequences of oil contamination are considered very high and having an oil-free compressor is a must.

- Oil-based compressors are considered more efficient than the oil-free type compressors, as oil acts as a cooling medium, taking out approximately 80% of the compressor's heat during the compression process, and considered more suitable for industrial usage with requirements of a high compression ratio.

- In terms of capital outlay, lubricated oil-based compressors are often considered less expensive than oil-free compressors, with price differences often varying in the range of 30-40%. It may even reach 50%, depending upon factors such as capacity and industry-specific requirements, resulting in increased demand for oil-based hydrogen compressors.

- Although oil-based compressors are more affordable than oil-free, these compressors require continuous maintenance and greater attention in replacing filters and other components used to eliminate the risk of oil leakage. Ongoing oil contamination may result in severe consequences, such as spoiled or unsafe products, production downtime, and legal issues.

- Oil-based hydrogen compressors are mostly preferred in the manufacturing industry for glass purification, iron and steel industry, semiconductor manufacturing, etc., for welding, annealing and heat-treating of metals, in power plants (coolant for generators), aerospace applications, pharmaceuticals, etc.

- According to the United States Geological Survey, in 2022, the United States' raw steel production was estimated to be 82 million metric tons. With the increasing industrialization, steel production may continue to increase, which, in turn, may create demand for oil-based hydrogen compressors.

- There is a persistent threat of premature wear of hydrogen compressor components due to insufficient lubrication, which may add to the maintenance cost of oil-based hydrogen compressors and limit their demand.

- Therefore, based on such factors, the oil-based type segment is expected to dominate the hydrogen compressor market during the forecast period.

Asia-Pacific Expected to Dominate the Market

- Asia-Pacific is expected to be a promising market for fuel cells in the coming years because of the favorable government policies in countries such as China, Japan, and India.

- China is one of the world's largest and fastest-growing hydrogen compressor markets. The country has witnessed significant growth in its chemical, oil, gas, and manufacturing sectors in recent years.

- Hydrogen centrifugal compressors are used in refining and petrochemical industries such as ethylene plants for cracked-gas compression and refrigeration services. Due to ethylene and benzene production shortages, the country has been investing to increase its ethylene and benzene production capacity.

- For instance, in May 2022, Neuman & Esser Beijing supplied four compressor systems to China Inner Mongolia Sanwei New Material Co. Ltd (CIMSNM). The compressors were likely used for hydrogen boosting and recycling while manufacturing 1,4-Butanediol (BDO). BDO is used in industry as a solvent and in producing specific polymers, elastic fibers, and polyurethanes.

- The development of hydrogen fuel cell vehicles and Japan's aim to build hydrogen fuel stations for recharging the vehicles are expected to drive the hydrogen compressor market.

- For instance, in Japan, 11 domestic firms, including automakers and energy firms, made a consortium to build 80 fueling stations for hydrogen fuel cell vehicles by 2022 to create a market for the next-gen fuel cell vehicle. As of September 2021, Japan has 154 hydrogen fueling stations and another 11 in the planning or construction stage. This, in turn, is expected to drive the hydrogen compressor demand for hydrogen fuel stations during the forecast period.

- Therefore, based on such factors, Asia-Pacific is expected to dominate the hydrogen compressor market during the forecast period.

Hydrogen Compressor Industry Overview

The hydrogen compressor market is semi fragmented. Some of the major companies include (in no particular order) Corken Inc., Ariel Corporation, Burckhardt Compression AG, Howden Group Ltd, and Atlas Copco Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increase in Demand for Hydrogen from End-user Industries

- 4.5.1.2 Increasing Deployment of Hydrogen Pipeline Infrastructure for Transportation

- 4.5.2 Restraints

- 4.5.2.1 The Slowdown in Industrial and Economic Activities Due to a Sharp Decline in Manufacturing Activity and Global Trade

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Single-stage

- 5.1.2 Multistage

- 5.2 Type

- 5.2.1 Oil-based

- 5.2.2 Oil-free

- 5.3 End-user Industry

- 5.3.1 Chemical

- 5.3.2 Oil and Gas

- 5.3.3 Other End-user Industries

- 5.4 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 Saudi Arabia

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Corken Inc.

- 6.3.2 Ariel Corporation

- 6.3.3 Burckhardt Compression AG

- 6.3.4 Hydro-Pac Inc.

- 6.3.5 Haug Kompressoren AG

- 6.3.6 Sundyne Corp.

- 6.3.7 Howden Group Ltd

- 6.3.8 Indian Compressors Ltd

- 6.3.9 Atlas Copco Group

- 6.3.10 Ingersoll Rand Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements and Emerging Sources for Hydrogen Production

02-2729-4219

+886-2-2729-4219

全球氢气压缩机市场:按技术类型、润滑类型和应用分类 - 预测 2025-2030

全球氢气压缩机市场:按技术类型、润滑类型和应用分类 - 预测 2025-2030 氢气压缩机市场规模和预测、全球和地区份额、趋势和成长机会分析报告范围:按类型、技术、最终用户和地理位置

氢气压缩机市场规模和预测、全球和地区份额、趋势和成长机会分析报告范围:按类型、技术、最终用户和地理位置 全球氢气压缩机市场

全球氢气压缩机市场 氢气压缩机市场规模、份额和趋势分析报告:按润滑类型、最终用途、地区、细分市场预测,2024-2030年

氢气压缩机市场规模、份额和趋势分析报告:按润滑类型、最终用途、地区、细分市场预测,2024-2030年 到 2030 年亚太地区氢气压缩机市场预测 - 区域分析 - 按类型、阶段和最终用户

到 2030 年亚太地区氢气压缩机市场预测 - 区域分析 - 按类型、阶段和最终用户 到 2030 年北美氢气压缩机市场预测 - 区域分析 - 按类型、阶段和最终用户

到 2030 年北美氢气压缩机市场预测 - 区域分析 - 按类型、阶段和最终用户 欧洲氢气压缩机市场预测至 2030 年 - 区域分析 - 按类型、阶段和最终用户

欧洲氢气压缩机市场预测至 2030 年 - 区域分析 - 按类型、阶段和最终用户 全球氢气压缩机市场:市场规模与占有率分析 - 趋势、驱动因素、竞争格局、预测(2024-2030)

全球氢气压缩机市场:市场规模与占有率分析 - 趋势、驱动因素、竞争格局、预测(2024-2030) 往復式氢气压缩机2024年全球市场报告

往復式氢气压缩机2024年全球市场报告 全球氢气压缩机市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测

全球氢气压缩机市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测

▼