|

市场调查报告书

商品编码

1432945

CMOS影像感测器:市场占有率分析、产业趋势、成长预测(2024-2029)CMOS Image Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

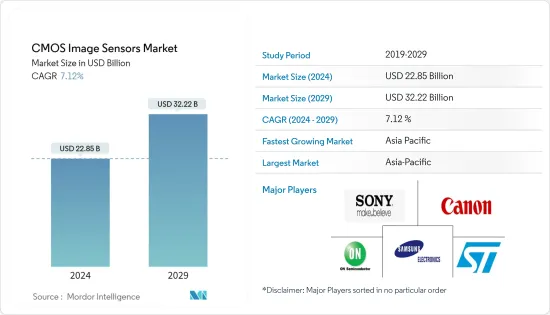

预计 2024 年 CMOS 影像感测器市场规模为 228.5 亿美元,预计到 2029 年将达到 322.2 亿美元,预测期内(2024-2029 年)复合年增长率为 7.12%。

主要亮点

- 各行业对高解析度影像撷取设备的需求不断增长,推动了 CMOS(互补型金属氧化物半导体)技术的广泛采用。该技术不仅可以实现百叶窗速度,还可以确保高品质的影像。

- 全球CMOS影像感测器市场正在经历显着成长,这主要是由于智慧型手机需求的不断增长。智慧型手机中带有影像感测器的相机的普及尤其有利于消费性电子产业。智慧型手机製造商正在透过在单一设备中整合多达五个摄影机来应对行动电话摄影的日益普及。这些 CMOS 影像感测器无所不在,不仅存在于智慧型手机中,还存在于笔记型电脑和数位单镜反光 (DSLR) 相机中。

- 随着智慧型手机普及的提高,相机与智慧型手机的整合大大增强了影像捕捉能力。这些因素将推动影像感测器市场向前发展。

- 同时,创新正在呈指数级增长对智慧型手机相机产生最高品质影像和 CMOS 技术的需求。此外,机器视觉系统的采用、自动驾驶汽车和高级驾驶辅助系统 (ADAS) 的出现进一步增加了对 CMOS 感测器的需求。

- 儘管 CCD(电荷耦合元件)感测器因其成熟度和高品质而在许多工业应用中变得普及,但对 CMOS 感测器的需求仍然存在。 CCD感测器以其高影像品质、高解析度影像和出色的感光度与CMOS感测器竞争。这种竞争预计将限制市场成长。

- 由于全球供应链停工和中断,电子和半导体产业在 COVID-19 大感染疾病期间面临重大挫折。儘管如此,由于消费性电器产品和汽车产业的需求不断增长,预计全球 CMOS 影像感测器市场仍将出现强劲成长。

CMOS影像感测器市场趋势

汽车和交通运输行业将成为成长最快的最终用户

- 各类车辆越来越多地采用先进驾驶辅助系统 (ADAS),这使得汽车和交通运输领域对 CMOS 影像感测器的需求迅速增加。将高性能保护功能整合到汽车系统中正在影响摄影机感测器系统的广泛采用,特别是在全球即将推出的无人驾驶和自动驾驶汽车的背景下。自动驾驶和联网汽车的持续发展正在为新的市场机会铺平道路。

- 例如,联邦运输管理局(FTA)最近宣布了示范计划的重大机会。这将提供高达 650 万美元的资金,其中包括 500 万美元用于公车 ADAS 以及另外 150 万美元用于自动化公车维护的初始阶段。和堆场作业。此外,2023 年 4 月,英国宣布核准福特先进驾驶辅助系统 (ADAS) BlueCruise 的免持驾驶技术,该技术将在该国高速公路上发挥引领作用。

- 此外,根据 IEA资料,电动车已成为道路交通脱碳的关键技术,因为该产业占全球能源相关排放的 15% 以上。近年来,由于续航里程的进步、车型的广泛可用性和性能的提高,电动车销量迅速增长。搭乘用电动车发展势头强劲,IEA 预测 2023 年售出的新车中 18% 将是电动车,其中欧洲、中国和美国将引领电动车市场。

- 国家安全委员会预测,到2026年,约71%的註册车辆将配备后置摄像头,60%将配备后停车感应器。 ADAS 的广泛采用预计将显着推动市场成长。

- 根据世界经济论坛预测,到2035年,预计每年将售出1,200万辆全自动驾驶汽车,占全球汽车市场的25%。联网汽车和电动车的需求激增推动了 CMOS 影像感测器市场的创新和产品开发。主要市场供应商都专注于产品创新,以满足不断增长的消费者需求。

美洲预计将出现显着成长

- 由于行动相机模组和其他行动装置使用率较高的消费性电器产品市场的存在,CMOS 影像感测器在美国得到越来越多的采用。在消费性电器产品,智慧型手机已成为主要的拍照设备,压倒了相机和数位单眼相机。智慧型手机领域的激烈竞争促使製造商提供更好的相机来击败竞争对手,从而导致该领域的技术创新投入大量资金。

- 美国人口普查局估计 2022 年至 2023 年智慧型手机销售额为 747 亿美元。成长放缓是美国智慧型手机出货下降的结果。在经济挑战、高通膨和季节性需求疲软的背景下,低阶智慧型手机销量下降是导致经济下滑的最大因素。然而,这种情况预计将在未来几年内结束。这些销售趋势预计将对消费电子领域 CMOS 影像感测器的成长产生重大影响,该领域不仅包括智慧型手机,还包括个人电脑、笔记型电脑、平板电脑等。

- 除此之外,机器人摄影机已成为各行业的革命力量,改变了我们拍摄、监控以及与周围环境互动的方式。这些先进的设备配备了尖端技术,具有许多优点,使其成为从监控和安全到製造和娱乐等应用的宝贵资产。因此,CMOS 感测器在产生数位影像方面更有效率,并且比 CCD 消耗更少的功率。它们可以比 CCD 更大,从而可以提供更高解析度的图像,并且与 CCD 相比製造起来更经济,从而增加了区域市场的需求。

- 由于车辆驾驶员辅助系统越来越多地使用生物识别、医疗和胶片相机等影像感测器设备,安全和监控设备预计将在未来成为一个巨大的市场。此外,在美国等国家,无人机被广泛用于进行勘察,製造商一直在寻找能够从高空捕捉影像的相机。具有高百万像素解析度和小感测器尺寸的相机可能会受到影像衍射效应的影响。

- 这影响了对 CMOS 影像感测器的需求,该感测器越来越多地用于汽车应用。例如,根据 OICA 的数据,到 2022 年,墨西哥将以 3,509,800 辆的销量成为拉丁美洲地区领先的汽车製造商,其次是巴西(2,369.77 辆)、阿根廷(536.9 辆)和哥伦比亚(51.46 辆)。

CMOS影像感测器产业概况

CMOS 影像感测器市场高度分散,主要企业包括意法半导体、索尼集团公司、三星电子、安森美半导体公司和佳能公司。这些公司利用合作伙伴关係和收购等策略来加强产品系列建立持久的竞争优势。边缘。

2023年9月,Sony Semiconductor Solutions Corporation发表了IMX735,这是一款汽车摄影机的尖端CMOS影像感测器,有效像素数达到业界领先,达到1,742万像素。这项创新产品将加强具有先进感测和识别能力的汽车摄影机系统的开发,并将为促进安全可靠的自动驾驶做出巨大贡献。

此外,2023 年 1 月,三星电子发布了最新的 2000 万像素 (MP) 影像感测器 ISOCELL HP2。该感测器采用增强的像素技术和增强的全井容量,可为高阶智慧型手机提供令人惊嘆的行动影像。 ISOCELL HP2 具有 2 亿个 1/1.3 吋光学格式的 0.6微米(μm) 像素,这种感光元件尺寸广泛用于领先的 108MP 智慧型手机相机,让消费者可以轻鬆使用他们最新的高阶智慧型手机。体验更高的分辨率。相机的突出部分变大了。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 评估 COVID-19 对产业的影响

第五章市场动态

- 市场驱动因素

- 扩大CMOS影像感测器在消费性电子领域的引入

- 4K像素技术在安防监控领域的出现

- 市场限制因素

- 与CCD感测器的竞争

第 6 章 技术概览

- 依通讯类型

- 有线

- 无线的

第七章市场区隔

- 按最终用户产业

- 消费性电子产品

- 卫生保健

- 产业

- 安全/监控

- 汽车与运输

- 航太/国防

- 计算

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第八章 竞争形势

- 公司简介

- STMicroelectronics NV

- Sony Corporation

- Samsung Electronics Co. Ltd

- ON Semiconductor Corporation

- Canon Inc.

- SK Hynix Inc.

- Omnivision Technologies Inc.

- Hamamatsu Photonics KK

- Panasonic Corporation

- Teledyne Technologies Inc.

- GalaxyCore Shanghai Limited Corporation

- 供应商市场占有率分析

第九章投资分析

第十章市场机会与未来趋势

The CMOS Image Sensors Market size is estimated at USD 22.85 billion in 2024, and is expected to reach USD 32.22 billion by 2029, growing at a CAGR of 7.12% during the forecast period (2024-2029).

Key Highlights

- The rising demand for high-definition image-capturing devices in various industries has spurred a significant adoption of CMOS (Complementary Metal-Oxide-Semiconductor) technology. This technology not only provides faster shutter speeds but also ensures high-quality images.

- Primarily driven by the increasing demand for smartphones, the global CMOS image sensors market has seen substantial growth. The widespread use of cameras with image sensors in smartphones has particularly benefited the consumer electronics industry. Smartphone producers are responding to the surge in popularity of cell phone photography by incorporating up to five cameras into a single device. These CMOS image sensors are omnipresent, found not only in smartphones but also in laptops and digital single-lens reflex (DSLR) cameras.

- Integration of cameras into smartphones has significantly augmented image capturing, aligning with the expanding smartphone penetration rate. These factors are poised to propel the image sensor market forward.

- Simultaneously, the demand for producing top-quality images in smartphone cameras and for CMOS technology is exponentially increasing due to innovations. Moreover, the adoption of machine vision systems and the emergence of self-driving cars and advanced driver assistance systems (ADAS) further drive the demand for CMOS sensors.

- Despite the prevalence of CCD (Charge-Coupled Device) sensors in many industrial applications due to their maturity and higher quality, the demand for CMOS sensors persists. CCD sensors excel in high-quality, high-resolution images and excellent light sensitivity, providing competition to CMOS sensors. This competition is expected to limit the market's growth.

- The electronics and semiconductor industries faced significant setbacks during the COVID-19 pandemic due to closures and disruptions in the global supply chain. Despite this, the anticipated growth of the global CMOS image sensors market remains strong, driven by increased demand from the consumer electronics and automotive sectors.

CMOS Image Sensors Market Trends

Automotive and Transportation Industry to be the Fastest Growing End User

- The demand for CMOS image sensors in the automotive and transportation sectors is rapidly expanding due to the increasing adoption of advanced driver-assistance systems (ADAS) across various categories of vehicles. The integration of high-performance protective functions into automotive systems has influenced the widespread adoption of camera sensor systems, particularly in the context of upcoming driverless autonomous vehicles worldwide. The ongoing development of autonomous and connected vehicles is paving the way for new market opportunities.

- For instance, the Federal Transit Administration (FTA) recently announced a substantial opportunity for demonstration projects, offering up to USD 6.5 million, including USD 5 million for ADAS in Transit Buses and an additional USD 1.5 million for the initial phase of Automated Transit Bus Maintenance and Yard Operations. Additionally, in April 2023, the UK announced the approval of hands-free driving technology through Ford's advanced driver-assistance system (ADAS), BlueCruise, set to lead the way on the country's motorways.

- Moreover, electric vehicles have emerged as a pivotal technology for decarbonizing road transport, given that this sector contributes over 15% of global energy-related emissions, as per IEA data. Recent years have witnessed exponential growth in EV sales, with advancements in range, broader model availability, and enhanced performance. Passenger electric cars are gaining traction, and the IEA estimates that 18% of new cars sold in 2023 will be electric, with Europe, China, and the US leading the electric vehicle markets.

- The National Safety Council projects that by 2026, approximately 71% of registered vehicles will feature rear cameras, while 60% will be equipped with rear parking sensors. This widespread adoption of ADAS is expected to fuel the market's growth significantly.

- According to the World Economic Forum, an estimated 12 million fully autonomous cars are projected to be sold annually by 2035, encompassing 25% of the global automotive market. This surge in demand for connected and electric vehicles has spurred innovation and product development in the CMOS image sensor market. Key market vendors are concentrating on product innovation to meet the escalating consumer demand.

Americas is Expected to Witness Significant Growth

- The growing adoption of CMOS image sensors across the United States is due to the strong presence of the consumer electronics market, which is fueling the usage of mobile camera modules and other portable devices at a high rate. In consumer electronics, the smartphone has become the primary camera device, dominating cameras and DSLRs. Heavy competition in the smartphone segment has driven manufacturers to provide better cameras to have the edge over the competition, resulting in high investments in technology innovations in this field.

- The US Census Bureau estimated the smartphone sales value at USD 74.7 Billion in 2022-2023. This sluggish growth is an outcome of declined shipments of smartphones in the US. Low-end smartphone sale declines were the biggest contributing factor to the downturn amid economic challenges, high inflation, and poor seasonal demand; however, this is expected to end in the upcoming years. These sales trends are expected to have a significant impact on the growth of CMOS image sensors in the consumer electronics segment, which not only includes smartphones but also PCs, laptops, and tablets.

- In addition to this, robotic cameras have become a revolutionary force in various industries, transforming the way of capturing, monitoring, and interacting with surroundings. These sophisticated devices, equipped with cutting-edge technology, offer a plethora of advantages, making them invaluable assets in applications ranging from surveillance and security to manufacturing and entertainment. Thus, CMOS sensors are more efficient in generating a digital image and consume less power than a CCD. They can be larger than a CCD, enabling high-resolution images, and their manufacture is more economical when compared to a CCD, thus driving the demand in the regional market.

- With the increase in the use of image sensor devices in biometrics, medical, and film cameras by vehicle driver assistance systems, security, and surveillance devices are expected to have a substantial market in the future. Moreover, drones are widely used in countries such as the United States to conduct surveys, and manufacturers are constantly looking for cameras that can capture images from altitude. Cameras with high megapixel resolution and small sensor sizes can be subject to image diffraction effects.

- This is impacting the demand for CMOS image sensors as they are increasingly being used in automotive applications. For instance, according to OICA, in 2022, Mexico was the leading motor vehicle manufacturer in the Latin American region, with 3,509.8 thousand vehicles, followed by Brazil (2,369.77), Argentina (536.9), and Colombia (51.46).

CMOS Image Sensors Industry Overview

The CMOS image sensor market exhibits high fragmentation, with major players such as STMicroelectronics NV, Sony Group Corporation, Samsung Electronics Co. Ltd, ON Semiconductor Corporation, and Canon Inc. These entities are leveraging strategies like partnerships and acquisitions to enrich their product portfolios and establish enduring competitive edges.

In September 2023, Sony Semiconductor Solutions Corporation unveiled the IMX735, a cutting-edge CMOS image sensor designed for automotive cameras, boasting an industry-leading pixel count of 17.42 effective megapixels. This innovative product is poised to bolster the development of automotive camera systems capable of sophisticated sensing and recognition, contributing significantly to the advancement of safe and secure automated driving.

Additionally, in January 2023, Samsung Electronics introduced its latest 200-megapixel (MP) image sensor, the ISOCELL HP2. This sensor incorporates enhanced pixel technology and increased full-well capacity, delivering stunning mobile images for premium smartphones. Packed with 200 million 0.6-micrometer (μm) pixels within a 1/1.3" optical format, a sensor size widely used in 108MP primary smartphone cameras, the ISOCELL HP2 enables consumers to experience even higher resolutions in the latest high-end smartphones without larger camera protrusions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Implementation of CMOS Image Sensors in the Consumer Electronics Segment

- 5.1.2 Emergence of 4K Pixel Technology in the Security and Surveillance Sector

- 5.2 Market Restraints

- 5.2.1 Competition from CCD Sensor

6 TECHNOLOGY SNAPSHOT

- 6.1 By Communication Type

- 6.1.1 Wired

- 6.1.2 Wireless

7 MARKET SEGMENTATION

- 7.1 By End-user Industry

- 7.1.1 Consumer Electronics

- 7.1.2 Healthcare

- 7.1.3 Industrial

- 7.1.4 Security and Surveillance

- 7.1.5 Automotive and Transportation

- 7.1.6 Aerospace and Defense

- 7.1.7 Computing

- 7.2 By Geography

- 7.2.1 North America

- 7.2.2 Europe

- 7.2.3 Asia-Pacific

- 7.2.4 Latin America

- 7.2.5 Middle East and Africa

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 STMicroelectronics NV

- 8.1.2 Sony Corporation

- 8.1.3 Samsung Electronics Co. Ltd

- 8.1.4 ON Semiconductor Corporation

- 8.1.5 Canon Inc.

- 8.1.6 SK Hynix Inc.

- 8.1.7 Omnivision Technologies Inc.

- 8.1.8 Hamamatsu Photonics KK

- 8.1.9 Panasonic Corporation

- 8.1.10 Teledyne Technologies Inc.

- 8.1.11 GalaxyCore Shanghai Limited Corporation

- 8.2 Vendor Market Share Analysis

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球有机 CMOS 影像感测器市场规模、份额、成长分析,按应用(3D 成像、视讯)、按技术(有机光电探测器、有机光电二极体)- 2024-2031 年行业预测

全球有机 CMOS 影像感测器市场规模、份额、成长分析,按应用(3D 成像、视讯)、按技术(有机光电探测器、有机光电二极体)- 2024-2031 年行业预测 合约药物开发与受託製造厂商(CDMO) 2024 年全球市场报告

合约药物开发与受託製造厂商(CDMO) 2024 年全球市场报告 全球 CMOS 影像感测器市场:按类型、应用和最终用户产业划分 - 预测 2024-2030 年

全球 CMOS 影像感测器市场:按类型、应用和最终用户产业划分 - 预测 2024-2030 年 CMOS相机模块市场:按类型(5MP至13MP、13MP或以上、小于5MP)、按用途(汽车、家用电器) - 2023-2030年全球预测

CMOS相机模块市场:按类型(5MP至13MP、13MP或以上、小于5MP)、按用途(汽车、家用电器) - 2023-2030年全球预测 CMOS影像感测器市场:高度保全监视相机的需求剧增创造新的商机

CMOS影像感测器市场:高度保全监视相机的需求剧增创造新的商机 CMOS相机模组的全球市场

CMOS相机模组的全球市场 CMOS相机模组的全球市场 2023-2027

CMOS相机模组的全球市场 2023-2027 CMOS影像感测器的全球市场

CMOS影像感测器的全球市场 CMOS图像传感器的技术进步

CMOS图像传感器的技术进步 CMOS影像感测器的全球市场:2022-2028年

CMOS影像感测器的全球市场:2022-2028年