|

市场调查报告书

商品编码

1907344

日本电动车充电设备市场占有率分析、产业趋势及统计、成长预测(2026-2031)Japan Electric Vehicle Charging Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

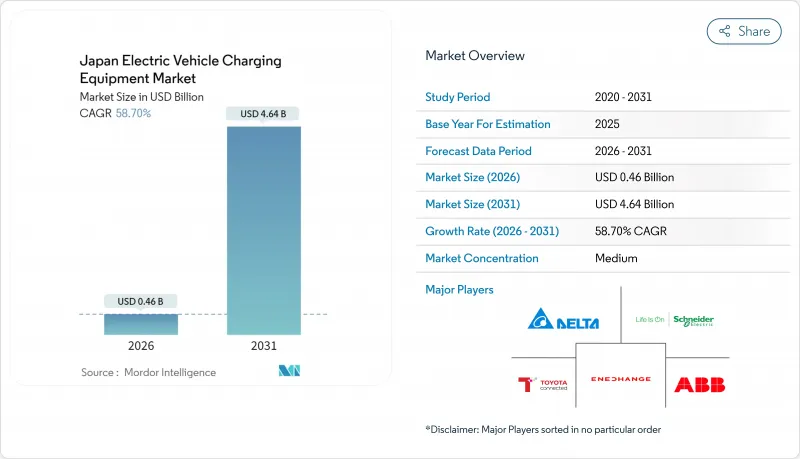

日本电动车充电设备市场预计到 2025 年将价值 2.9 亿美元,从 2026 年的 4.6 亿美元成长到 2031 年的 46.4 亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 58.70%。

日本电动车充电设备市场的发展主要得益于2035年禁止销售汽油动力车的政策、大规模的绿色成长投资以及双向充电桩在全国电力系统中的普及。大型企业集团推行的强制性电气化政策为日本电动车充电设备市场创造了高度可预测的需求基础,使得网路建设速度更快,规模经济效益也比消费者主导型模式更早实现。技术创新(特别是液冷充电线、复合电缆和新一代CHAdeMO/ChaoJi通讯协定)正将充电设备定位为电网资产,而不仅仅是硬体的「燃料补给」。各部会和都道府县之间的政策协调维持了补贴制度并缩短了投资回收期,而零件技术的创新则降低了总体拥有成本。儘管日本电动车充电设备市场仍处于一定程度的分散状态,但电力公司正开始在整个生态系统中扮演关键的协调者角色,并透过需量反应计画开发新的收入来源。

日本电动车充电设备市场趋势及洞察

由于2035年禁止销售汽油车,因此需要推广向电动车转型。

这项禁令消除了政策上的不确定性,刺激了资本投资,因为日本充电设备市场的供应商可以更有信心地预测未来十年的现金流。日本政府已拨款数兆日圆用于扩大充电基础设施,并设定了2030年建成30万个公共充电桩的目标(增加八倍)。商用车辆也将受到限制,这将即时产生对充电桩的需求,从而支撑日本电动车充电设备市场的高复合年增长率。东京及其周边地区吸引了大部分初始资金,这反映了这些地区人口密度高,且企业总部集中。

凯雷茨集团主导的企业ESG和车队电气化倡议

日本独特的企业集团(keiretsu)体系已将电动车的普及从消费者的选择转变为统一的企业策略,从而形成了西方市场所不具备的独特基础设施需求模式。一些日本企业已承诺在2030年前实现其商用车辆的全面电气化,并为工厂和物流中心签订了长期充电桩合约。规模经济将降低每个港口的安装成本,并加快投资回报,尤其是在关东-关西经济特区。

根据《建筑物管理法》,公寓维修核准出现延误。

日本《建筑物管理法》规定,公寓大楼内任何重大电气设备改造都必须获得所有业主的同意。这项规定对住宅充电站的安装构成重大障碍,尤其是在公寓大楼普遍存在的都市区。该法的製定主要针对传统的建筑维修,未能充分考虑电动车基础建设所面临的独特挑战。业主个人的决定将对建筑物的电力容量和整体安全系统产生深远影响。随着电动车的普及,这些限制日益严格,造成了基础设施瓶颈。因此,许多新电动车车主被迫依赖公共充电设施,增加了营运成本,降低了电动车的吸引力。

细分市场分析

到2025年,乘用车将占日本电动车充电设备市场份额的93.48%,成为大多数公共电网的基础负载。同时,商用车的复合年增长率将达到64.30%,这将促使设备製造商转向大规模直流模组和先进的负载调度软体。车队电气化合约通常为期多年,使供应商能够确保持续的维护收入并更准确地预测零件需求。像大和运输和佐川急便这样的物流公司正在部署兆瓦级枢纽作为微电网,利用固定式电池来降低高峰需求,并向电力公司出售辅助服务。这些大型设施也对个人驾驶员产生了连锁反应,因为营运商会在夜间向公众开放剩余的电力容量。

企业级应用的兴起也推动了连接器耐用性和支付整合的创新,因为车队应用场景需要数千次的连接循环和集中收费。处理能力的提升加快了硬体更换週期,扩大了电缆、密封件和开关设备的售后市场。将硬体与SaaS车队管理仪錶板捆绑销售的供应商,由于整合到物流工作流程中的软体客户解约率较低,可以稳定利润率。随着企业级应用的普及,即使乘用车仍保持销售优势,商用车在日本电动车充电设备市场的份额预计也将成长。

预计到2025年,其他类别(例如接线端子、电能表、安全装置等)将占日本电动车充电设备市场份额的33.62%,而线缆预计将以63.90%的复合年增长率成长。轻量复合复合材料鞘套将电缆重量减轻40%,从而减轻工作量并减少因连接器脱落而导致的维修次数。日本国内企业正与树脂供应商合作开发这些设计,并签订独家供应协议以提高利润率。零件的规模经济显着降低了单位成本,从而提高了小规模独立营运商的采用率。

传统的桿式充电桩在都市区面临面积限制,促使供应商推出纤薄的壁挂式充电桩,可直接安装在现有的停车场灯桿上。电源和控制面板的更新换代与日本电动车充电设备市场的整体成长趋势相符,碳化硅MOSFET的采用显着提高了转换效率,并带来了额外的成长潜力。 CHAdeMO的「超快」蓝图推动了互通性的改进,确保新硬体能够向下相容旧款车辆。提供端到端硬体套件的供应商透过捆绑销售策略简化采购审核,从而赢得市政竞标。这场组件之争表明,在快速扩张的市场中,技术的渐进式改进如何能显着影响收入来源。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 日本计划于2035年禁止销售汽油动力汽车,这将促进向电动车的转型。

- 企业环境、社会及治理(ESG)及集团公司强制要求车队电气化

- 经济产业省绿色成长基金提供的高功率充电器补贴

- 电力公司对车辆到家庭(V2H)的附加费

- 太阳能资源丰富的地区对併网双向充电器的需求

- 配合2025年大阪世博会试行引进道路充电桩

- 市场限制

- 根据《建筑物管理法》,公寓维修核准出现延误。

- 高速公路沿线公共快速充电设施的土地租金高昂

- CHAdeMO/CCS/NACS 标准的持续划分

- 本地充电站利用率低(低于8%)

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模和成长预测(价值和数量)

- 按车辆类型

- 搭乘用车

- 商用车辆

- 透过充电设备

- 支柱

- 电线和电缆

- 基板

- 充电控制器

- 电源

- 其他的

- 透过充电方法

- 交流充电站

- 直流充电站

- NACS(北美充电系统)

- 透过使用

- 家用充电

- 公共充电

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Panasonic Corporation

- Denso Corporation

- Mitsubishi Electric Corporation

- Hitachi, Ltd.

- Delta Electronics

- Nichicon Corporation

- Fujikura Ltd.

- Toshiba Corporation

- NEC Corporation

- Sumitomo Electric Industries, Ltd.

- Tokyo Electric Power Company Holdings(TEPCO)

- ENECHANGE Ltd.

- Terra Motors Corporation

- Envision AESC Group

第七章 市场机会与未来展望

The Japan EV charging equipment market was valued at USD 0.29 billion in 2025 and estimated to grow from USD 0.46 billion in 2026 to reach USD 4.64 billion by 2031, at a CAGR of 58.70% during the forecast period (2026-2031).

The Japan EV charging equipment market is propelled by the 2035 gasoline-vehicle sales ban, heavy green-growth spending, and nationwide integration of bidirectional chargers into the power system. Corporate electrification mandates issued by major keiretsu groups give the Japan EV charging equipment market an unusually predictable demand base, allowing faster network build-outs and earlier scale economies than consumer-led models. Technology advances-especially liquid-cooled cords, composite cables, and next-generation CHAdeMO/ChaoJi protocols-position equipment as grid assets rather than simple refueling hardware. Policy coherence between ministries and prefectures sustains subsidy pipelines that narrow payback periods, while component innovation drives total cost of ownership down. Although the Japan EV charging equipment market remains moderately fragmented, utilities have emerged as pivotal ecosystem orchestrators that unlock new revenue through demand-response programs

Japan Electric Vehicle Charging Equipment Market Trends and Insights

EV-Shift Stimulus From Japan's 2035 Gasoline-Car Sales Ban

The ban removes policy ambiguity and accelerates equipment investment because Japanese EV charging equipment market suppliers can confidently model ten-year cash flows. The Japanese government has earmarked trillions for charging build-outs and set a 300,000-public-port target by 2030, an almost eight-fold expansion. Commercial fleets must also comply, triggering immediate depot-charging demand that underpins the Japan EV charging equipment market's significant CAGR. Tokyo and adjacent prefectures attract the bulk of early funding, reflecting population density and corporate head-office concentration.

Corporate ESG-Fleet Electrification Mandates By Keiretsu Groups

In Japan, the distinctive keiretsu system shifts electric vehicle (EV) adoption from mere consumer choices to unified corporate strategies, leading to unique infrastructure demand patterns not seen in Western markets. Some Japanese companies have pledged to have fully electrified commercial fleets by 2030, locking in long-term charger contracts at factories and logistics hubs. Scale advantages lower per-port installation costs and accelerate return on investment, especially in the Kanto and Kansai economic belts.

Slow Condominium Retrofit Approvals Under the Building Management Act

Japan's Building Management Act mandates unanimous consent from all condominium owners for major electrical modifications. This requirement poses significant hurdles for installing residential charging stations, especially in urban areas dominated by condominium living. While the Act was crafted for traditional building modifications, it fails to address the nuances of EV infrastructure deployment. Here, decisions made by individual owners can have far-reaching implications on the building's overall electrical capacity and safety systems. As EV adoption surges, these constraints intensify, leading to infrastructure bottlenecks. Consequently, many new EV owners are pushed towards public charging solutions, which inflate operational costs and dampen the appeal of EV adoption.

Other drivers and restraints analyzed in the detailed report include:

- Subsidized High-Power Charger Grants Under METI's Green Growth Fund

- V2H Tariff Premiums from Power Utilities

- High Land-Lease Costs for Public Fast-Charging Sites Near Expressways

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars held a 93.48% Japan EV charging equipment market share in 2025, furnishing the baseline load for most public networks. Commercial vehicles, however, post a 64.30% CAGR that pulls equipment makers toward depot-grade DC blocks and advanced load-scheduling software. Fleet electrification contracts are typically multi-year, letting suppliers lock in recurring maintenance revenue and forecast parts demand more accurately. Logistics firms like Yamato and Sagawa deploy megawatt hubs that double as micro-grids, using stationary batteries to shave peak demand and sell ancillary services to utilities. These large installations create spillover benefits for retail drivers when operators open excess nighttime capacity to the public.

The corporate pivot also drives connector durability and payment integration innovation because fleet use cases require thousands of mating cycles and centralized billing. Higher throughput accelerates hardware replacement cycles, expanding the aftermarket for cables, seals, and switchgear. Suppliers that bundle hardware with SaaS fleet dashboards gain margin insulation because software churn remains low once integrated into logistics workflows. As corporate adoption scales, the commercial share of the Japan EV charging equipment market size is expected to rise, even if passenger cars remain numerically dominant.

The Others (terminal blocks, energy meters, safety mechanisms, etc.) category held 33.62% of the Japan EV charging equipment market share in 2025, but cords and cables are forecast to grow at a 63.90% CAGR. Lightweight composite sheathing cuts cable mass by 40%, mitigating ergonomic strain and reducing maintenance calls linked to dropped connectors. Domestic firms co-develop these designs with resin suppliers, securing exclusive supply contracts that shore up margins. Component scale economies lower per-unit cost significantly, widening adoption among small independent operators.

Traditional pedestal pillars face urban footprint constraints, prompting vendors to roll out slimline wall-mounts that bolt onto existing parking-lot lighting poles. Power supplies and control boards track the overall growth of Japan's EV charging equipment market size but gain an incremental bump from silicon-carbide MOSFET adoption, significantly improving conversion efficiency. Interoperability upgrades follow CHAdeMO's ChaoJi roadmap, ensuring new hardware remains backward-compatible with earlier vehicles. Suppliers that offer end-to-end hardware suites win municipal tenders because bundling simplifies procurement audits. The component race thus underscores how incremental engineering tweaks can swing large revenue pools in a fast-scaling market.

The Japan Electric Vehicle Charging Equipment Market Report is Segmented by Vehicle Type (Passenger Cars and Commercial Vehicles), Charging Equipment (Pillar, Cord and Cable, Control Boards, Charging Controllers, and Others), Charging Type (AC Charging Station, DC Charging Station, and NACS), and Application Type (Home Charging and Public Charging). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Panasonic Corporation

- Denso Corporation

- Mitsubishi Electric Corporation

- Hitachi, Ltd.

- Delta Electronics

- Nichicon Corporation

- Fujikura Ltd.

- Toshiba Corporation

- NEC Corporation

- Sumitomo Electric Industries, Ltd.

- Tokyo Electric Power Company Holdings (TEPCO)

- ENECHANGE Ltd.

- Terra Motors Corporation

- Envision AESC Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV-Shift Stimulus from Japan's 2035 Gasoline-Car Sales Ban

- 4.2.2 Corporate ESG-Fleet Electrification Mandates by Keiretsu Groups

- 4.2.3 Subsidized High-Power Charger Grants Under METI's Green Growth Fund

- 4.2.4 V2H (Vehicle-To-Home) Tariff Premiums From Power Utilities

- 4.2.5 Grid-Balancing Demand for Bidirectional Chargers at Solar-Rich Prefectures

- 4.2.6 On-Street Charger Pilots Tied to 2025 World Expo Osaka

- 4.3 Market Restraints

- 4.3.1 Slow Condominium Retrofit Approvals Under Japan's Building Management Act

- 4.3.2 High Land-Lease Costs for Public Fast-Charging Sites Near Expressways

- 4.3.3 Persistent CHAdeMO / CCS / NACS Standards Fragmentation

- 4.3.4 Low Utilisation Rates (Below 8%) at Rural Charging Stations

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Commercial Vehicles

- 5.2 By Charging Equipment

- 5.2.1 Pillar

- 5.2.2 Cord and Cable

- 5.2.3 Control Boards

- 5.2.4 Charging Controllers

- 5.2.5 Power Supplies

- 5.2.6 Others

- 5.3 By Charging Type

- 5.3.1 AC Charging Station

- 5.3.2 DC Charging Station

- 5.3.3 NACS (North American Charging System)

- 5.4 By Application Type

- 5.4.1 Home Charging

- 5.4.2 Public Charging

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Panasonic Corporation

- 6.4.2 Denso Corporation

- 6.4.3 Mitsubishi Electric Corporation

- 6.4.4 Hitachi, Ltd.

- 6.4.5 Delta Electronics

- 6.4.6 Nichicon Corporation

- 6.4.7 Fujikura Ltd.

- 6.4.8 Toshiba Corporation

- 6.4.9 NEC Corporation

- 6.4.10 Sumitomo Electric Industries, Ltd.

- 6.4.11 Tokyo Electric Power Company Holdings (TEPCO)

- 6.4.12 ENECHANGE Ltd.

- 6.4.13 Terra Motors Corporation

- 6.4.14 Envision AESC Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

电动车充电主动滤波器按充电站类型、滤波器配置、额定输出功率和最终用户划分,全球预测,2026-2032年电动车充电滤波器市场按滤波器类型、滤波器拓扑结构、额定电流、应用和最终用户划分-全球预测,2026-2032年电动车智慧充电控制器市场:按充电等级、模式、通讯技术、交付方式、车辆类型、应用和最终用户划分-2026-2032年全球预测

电动车充电主动滤波器按充电站类型、滤波器配置、额定输出功率和最终用户划分,全球预测,2026-2032年电动车充电滤波器市场按滤波器类型、滤波器拓扑结构、额定电流、应用和最终用户划分-全球预测,2026-2032年电动车智慧充电控制器市场:按充电等级、模式、通讯技术、交付方式、车辆类型、应用和最终用户划分-2026-2032年全球预测 日本电动车充电设备市场规模、份额、趋势及预测(按充电站、最终用途和地区划分,2026-2034年)

日本电动车充电设备市场规模、份额、趋势及预测(按充电站、最终用途和地区划分,2026-2034年) 电动汽车家用充电套件市场预测至2032年:按充电器类型、连接器类型、车辆类型、安装类型、分销管道、应用和地区分類的全球分析

电动汽车家用充电套件市场预测至2032年:按充电器类型、连接器类型、车辆类型、安装类型、分销管道、应用和地区分類的全球分析 智慧电动汽车充电网路市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)超快速电动车充电(350kW+)系统市场机会、成长驱动因素、产业趋势分析及2025-2034年预测

智慧电动汽车充电网路市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)超快速电动车充电(350kW+)系统市场机会、成长驱动因素、产业趋势分析及2025-2034年预测 美国电动车 (EV) 充电:市场占有率分析、行业趋势和成长预测(2025-2030 年)欧洲电动车(EV)充电设备 -市场占有率分析、产业趋势/统计、成长预测(2025-2030)西欧电动车 (EV) 充电设备 -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

美国电动车 (EV) 充电:市场占有率分析、行业趋势和成长预测(2025-2030 年)欧洲电动车(EV)充电设备 -市场占有率分析、产业趋势/统计、成长预测(2025-2030)西欧电动车 (EV) 充电设备 -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)