|

市场调查报告书

商品编码

1433010

小袋包装:市场占有率分析、产业趋势、资料、成长预测(2024-2029)Pouch Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

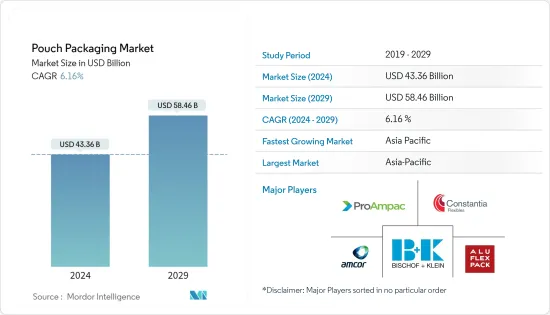

预计2024年小袋包装市场规模为433.6亿美元,预计2029年将达到584.6亿美元,在预测期内(2024-2029年)复合年增长率为6.16%。

主要亮点

- 袋是食品和饮料行业中使用最广泛的包装产品之一,包括宠物食品、婴儿食品和液体包装(茶、咖啡、果汁)。这是因为它们具有多种特性,包括易于打开(例如撕裂凹口和雷射穿孔)、易于使用(拉炼和形状)和可重新密封性。此外,它具有化学惰性,使其广泛应用于多种行业,包括药物、宠物食品和化妆品。

- 西方国家冷冻包装产业的成长预计将对市场产生积极影响。例如,根据欧洲冷冻食品的数据,德国、法国和英国占了欧洲冷冻食品市场50%以上的份额。政府因 COVID-19 大流行而实施的封锁对市场产生了积极影响,有助于许多地区的冷冻食品销售。

- 市场扩张的关键因素包括对包装食品和食品和饮料的需求不断增长、对即食 (RTE)食品日益增长的兴趣、袋装食品的易用性和可负担性。此外,对随身携带零食的需求不断增加,也增加了对为消费者提供便利的可重新封闭的自立袋的需求。消费者生活方式和食品偏好的变化以及食品技术的变化也在推动市场需求。

- 然而,消费者对环境问题意识的增强、不断变化的监管标准、对永续性的持续推动(包括用生物分解性材料取代塑胶包装产品)以及缺乏先进的回收设施导致回收率提高。这些都是阻碍回收率提高的因素。市场成长。

- 袋包装比硬质运输包装便宜得多,重量也轻。据软包装协会 (FPA) 称,製造方法的进步和材料创新使一些软包装的重量减轻了近 50%。此外,袋包装可以节省空间,这意味着可以使用更少的燃料和能源来运输更多的产品。

- COVID-19 大流行对小袋包装销售产生了多种影响。疫情导致全球许多地区的袋包装製造商面临供应链中断和产量减少的情况。然而,对医疗和保健用品的需求不断增长预计将对袋包装市场产生积极影响。

自立袋包装市场趋势

对方便食品和已调理食品的需求增加

- 满足消费者对便利性的需求是现有和新型包装技术的关键驱动力。包装产业正在经历一场根本性的转变,开始注重品牌体验。舒适性的需求也是改变的关键驱动力。软包装,尤其是袋包装,由于其对消费者和製造商的便利性而得到大力推广。因此,软包装形式被认为是建立品牌忠诚度的资产。消费者喜欢将产品从软质包装中挤压出来以节省空间并重新密封产品以按照自己的步调调整产品消费的能力。

- 从刚性包装转向软质包装以利用便利包装并适应不断变化的生活方式的总体趋势是由越来越多的小家庭和日益增长的单一服务选择推动的。随着单身家庭数量的增加,大多数消费者(尤其是年轻人)倾向于频繁购买少量食品杂货,以便随身携带自己喜欢的产品。派对大小的食品袋现在已成为过去。

- 美洲和欧洲地区消费者生活方式的变化也增加了对已调理食品的需求。已调理食品的需求从未如此强烈。全天候工作的新时代劳动力和寻找方便食品的一代已经成为已调理食品的最佳解决方案。

- 世界日益都市化强调了包装的便利性和永续性。需要便利包装的最终用户(例如生鲜食品、已调理食品、即食食品、咖啡等)的健康成长预计将推动袋包装的製造需求。据印度经济顾问办公室称,2022财年,印度加工和已调理食品批发价格指数突破137。过去十年,印度的物价指数普遍上涨。

- 零嘴零食、肉品、泡麵、米等方便食品的需求量大。食品和饮料支出的增加、对健康食品的认识提高、用餐模式和饮食习惯的变化以及社会和经济变量的变化都导致了对快餐的渴望增加。据韩国产业通商资源部称,2023年1月韩国便利商店即时加工食品月销售额与去年同月相比成长了14.6%。

亚太地区将经历最快的成长

- 该市场是由越来越多的中国客户推动的,他们主要喜欢蒸馏包装的产品以保持货架稳定性,例如鱼、肉和蔬菜。此外,中国消费者也越来越习惯家常小菜。

- 由于食品、药品/医疗、个人护理和家庭护理等最终用户行业的需求快速增长,中国在预测期内可能会对软包装产品产生巨大需求。儘管该国拥有庞大的包装基地,但由于其低成本和众多的产品优势,软包装在所有型态的包装中经历了最快和最显着的增长。

- 此外,印度对乳製品产业也做出了巨大贡献。由于一次性塑胶受到严格限制,市场相关人员在开发生物分解性和可重复使用的袋子方面具有巨大潜力。永续包装还包括可重复使用的材料,例如由生质乙醇製成的聚乙烯、聚乳酸、微纤化纤维素和生物分解性材料。

- 软包装袋,特别自立袋,是在该国不断扩大的食品行业中迅速发展的包装类型。客户和供应商都立即喜欢这种类型的包装。现今忙碌的消费者正在寻找简单、轻巧、便于携带的零食包装。因此,从食品包装的趋势来看,更紧凑、更小的包装尺寸很快就变得流行,尤其是那些具有可重新闭合功能(如拉炼)的包装。

- 越来越多使用袋包装的替代包装选项限制了产品在市场上的扩张。由于包装食品需求激增、可支配收入增加以及职业女性数量增加,预计印度将在亚太地区包装行业中占据重要份额。

- 2022 年 8 月,致力于提高人们对塑胶废弃物危险性认识的印度青年协会 (IYFS) 发起了一项收集奶袋的新措施。 VS Krishna 学院特别重视收集奶袋。该组织表示,该组织收集并回收了这些袋子。 IYFS 与大剪切机市政公司合作,在垃圾场建立了回收站。 IYFS 办公室可以轻鬆处理不需要的奶袋和塑胶。

自袋包装产业概况

由于全球存在多个市场参与者,小袋包装市场呈现零碎化。主要参与者包括 Bischof+Klein SE &Co.KG、Amcor Limited、Aluflexpack Group、ProAmpac Intermediate 和 Constantia Flexibles Group GmbH。市场参与者预计将采取创新措施,利用多个最终用户垂直领域成长所带来的机会,并扩大其在市场中的影响力。

2022年9月,Amcor对基于数位化的ePacFlexible Packaging(自称在印刷技术方面具有优势的自立袋、平铺袋和捲材製造商)进行了4500万美元的战略投资,并收购了ePacHoldings LLC的少数股权.宣布增持持股比率.

2022 年 7 月,Mondi 宣布投资扩大其永续宠物食品包装解决方案。 Mondi 宣布计划投资约 6,500 万欧元(7,142 万美元)在欧洲建造三个消费性软包装工厂,以提高产能并满足客户对永续宠物食品包装解决方案的需求。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 对具有成本效益的包装解决方案和品牌提升的需求不断增长

- 对方便即食食品的需求不断增长

- 市场限制因素

- 日益严重的环境问题与回收

第六章市场区隔

- 按类型

- 标准

- 无菌的

- 蒸馏

- 热填充

- 按闭合类型

- 拉炼

- 喷口

- 撕裂缺口

- 按最终用户产业

- 食品和饮料

- 个人护理

- 卫生保健

- 其他最终用户产业

- 按地区

- 北美洲

- 美国

- 法国

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 其他亚太地区

- 拉丁美洲

- 巴西

- 阿根廷

- 其他拉丁美洲

- 中东/非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲

- 北美洲

第七章 竞争形势

- 公司简介

- Amcor PLC

- Bischof+Klein SE & Co. KG

- Aluflexpack AG

- ProAmpac Intermediate Inc.

- Constantia Flexibles Group GmbH

- Coveris Management GmbH

- FLAIR Flexible Packaging Corporation

- Gualapack SpA

- Hood Packaging Corporation

- Mondi PLC

- Scholle IPN

- Sealed Air Corporation

- Sonoco Products Company

- Toppan Inc.

- TOYO SEIHAN CO LTD(Toyo Seikan Group Holdings Ltd.)

- Huhtamaki Flexible Packaging

- Glenroy Inc.

- Uflex Limited

- KM Packaging Services Ltd.

- Eagle Flexible Packaging

第八章投资分析

第9章市场的未来

The Pouch Packaging Market size is estimated at USD 43.36 billion in 2024, and is expected to reach USD 58.46 billion by 2029, growing at a CAGR of 6.16% during the forecast period (2024-2029).

Key Highlights

- Pouches are among the most widely used packaging products in the food and beverage industry, including pet food, baby food, and liquid packaging (tea, coffee, and juices) owing to their different features, including an easy opening (like a tear notch and laser perforation), easy to use (with zippers and shapes) and being reclosable. Moreover, as they are chemically inert, they are widely used in different industries, such as pharmaceuticals, pet food, and cosmetics.

- The growth of the frozen packaged industry across European and American countries is expected to impact the market positively. For instance, according to Frozen Food Europe, Germany, France, and the United Kingdom account for more than 50% of the frozen food market in Europe. The government-mandated lockdown due to the COVID-19 pandemic aided the sales of frozen foods in many regions and impacted the market positively.

- The key market expansion drivers include increased demand for packaged foods and beverages, expanding interest in ready-to-eat (RTE) food, ease of use, and affordability of pouches. In addition, the rise in the demand for on-the-go snacks led to the need for re-closable stand-up pouches as they offer convenience to consumers. The changing lifestyle and food preferences among consumers and changing food technology also boost the market demand.

- However, the growing consumer awareness about environmental concerns, dynamic regulatory standards, the ongoing drive for sustainability that includes replacing plastic-based packaging products with biodegradable materials, and poor recycling rate due to the lack of advanced recycling facilities are some factors challenging the market's growth.

- Pouch packing is significantly less expensive and lower in weight than rigid packaging for transportation. According to the Flexible Packaging Association (FPA), advancements in manufacturing methods and material innovation have reduced the weight of some flexible packaging by nearly 50%. Furthermore, pouch packaging allows for space savings, which implies that large quantities of products can be shipped with less fuel and energy.

- The COVID-19 pandemic had a mixed influence on pouch packaging sales. Due to the outbreak, pouch packaging manufacturers faced supply chain disruptions and decreased manufacturing in many parts of the world. However, the increasing demand for medical and healthcare supplies was expected to positively affect the pouch packaging market.

Pouch Packaging Market Trends

Increasing Demand for Convenience and Ready-to-eat Food

- Meeting consumer demands for convenience is a significant driver for existing and new packaging technologies. The packaging industry has been experiencing fundamental shifts focused on brand experience. Demand for comfort is also a key driver of change. There is a considerable push for flexible packaging, especially pouches, owing to its convenience for consumers and manufacturers. Therefore, flexible packaging formats are recognized as an asset in building brand loyalty. Consumers like the ability to squish or squeeze out products from a flexible package to save space and prefer resealing products to regulate product consumption at their own pace.

- The general trend of shifting from rigid to flexible packaging to avail the benefits of convenience packaging and fit the changing lifestyles, along with the growing number of smaller households, is increasing the need for single-serve options. In line with the growth in the number of single-person households, most consumers (especially the youth) are inclined to frequent shopping for groceries in smaller quantities as they can carry their favorite products with them wherever they move to convenience. Party-size bags of food items have been an old norm as smaller or individual-sized pouches allow consumers to feel more likely in control of portion sizes.

- The changing lifestyle of the consumer in the American and European regions also increased demand for ready-to-eat foods. The need for ready-to-eat food is at an all-time high. With the new age working population working round the clock and the gen-z looking for everything handy, ready-to-eat foods have emerged as the best solution.

- The increasing rate of urbanization worldwide has resulted in a higher focus on convenience and sustainability in packaging. The healthy growth of end users, such as fresh food, ready-to-eat food, ready-to-food, and coffee that require convenient packaging, is projected to drive the need for producing pouch packaging. According to the Office of Economic Adviser (India), during the fiscal year 2022, India's Wholesale Price Index of processed ready-to-eat meals exceeded 137. Since the past decade, the country has witnessed an overall increase in the price index.

- Convenience meals such as snacks, meat products, quick noodles, rice, and other items are in high demand. Higher food and beverage expenditure, more awareness of healthier foods, changes in meal patterns and eating habits, and shifting social and economic variables are all contributing causes to the increased desire for quick foods. According to the South Korean Ministry of Trade, Industry, and Energy, the year-on-year growth of processed instant food sales at convenience stores each month in South Korea increased by 14.6% in January 2023 compared to the previous month.

Asia-Pacific to Witness the Fastest Growth

- The market is being driven by Chinese customers' growing preference for mostly retort-packed goods to maintain their shelf stability, including fish, meat, and vegetables. Additionally, the nation's customers are becoming increasingly accustomed to ready-made meals.

- China will likely experience a considerable demand for flexible packaging goods during the forecast period due to the rapid development in demand from end-user sectors like food, pharmaceutical and medical, personal care, and domestic care. Despite the country having a sizable basis for packaging, flexible packaging had the quickest and most significant growth among all forms of packaging due to its low cost and numerous product benefits.

- Moreover, India made a significant contribution to the dairy industry. Due to strict limits on single-use plastics, market players have considerable potential to develop biodegradable and reusable pouches. Reusable materials such as polyethylene made from bioethanol, polylactic acid, micro-fibrillated cellulose, and biodegradable materials are also included in sustainable packaging.

- Flexible pouches, particularly stand-up pouches, are the packaging types expanding rapidly in the expanding food business in the country. Customers and suppliers alike love this kind of packaging right away. Consumers nowadays who lead hectic lives seek simple, lightweight snack packaging that is portable. Because of this, trends in food packaging show that more compact, smaller package sizes are popular right away, especially when they have recloseable features like zippers.

- A rise in the use of alternative packaging options for pouch packaging is constraining the market's expansion of products. Due to the rapidly increasing demand for packaged food goods, an increase in disposable income, and the number of working women in the country, India is predicted to hold a significant share of the Asia-Pacific packing industry.

- In August 2022, the India Youth For Society (IYFS), a committed group raising awareness about plastic waste's dangers, launched a new initiative to collect milk pouches. At Dr. V.S. Krishna Degree College, a particular push to collect these pouches got underway. According to the organization, the group gathers pouch bags for recycling. In collaboration with the Greater Visakhapatnam Municipal Corporation, the IYFS set up a recycling operation at the dump. The IYFS office is convenient for disposing of unwanted milk pouches and plastic.

Pouch Packaging Industry Overview

The Pouch Packaging market is fragmented due to the presence of several market players globally. Some major players are Bischof + Klein SE & Co. KG, Amcor Limited, Aluflexpack Group, ProAmpac Intermediate, and Constantia Flexibles Group GmbH. The market players are expected to leverage the opportunity posed by the growth of several end-user verticals and are innovating to expand their market presence.

In September 2022, Amcor announced a strategic investment of USD 45 million in the digitally-based ePacFlexible Packaging (manufacturers of stand-up pouches, lay flat pouches, and roll stock, with a self-claimed advantage in print technology) to increase its minority shareholding in ePacHoldings LLC.

In July 2022, Mondi announced an investment to expand sustainable pet food packaging solutions. Mondi announced plans to invest nearly EUR 65 million (USD 71.42 million) in three consumer flexible packaging plants in Europe to increase production capacity and meet customer demand for sustainable pet food packaging solutions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Requirements for Cost-effective Packaging Solutions and Brand Enhancement

- 5.1.2 Increasing Demand for Convenience and Ready-to-eat Food

- 5.2 Market Restraints

- 5.2.1 Growing Environmental Concerns and Recycling

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Standard

- 6.1.2 Aseptic

- 6.1.3 Retort

- 6.1.4 Hot-fill

- 6.2 By Closure Type

- 6.2.1 Zipper

- 6.2.2 Spout

- 6.2.3 Tear Notch

- 6.3 By End-user Industry

- 6.3.1 Food and Beverage

- 6.3.2 Personal Care

- 6.3.3 Health Care

- 6.3.4 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Italy

- 6.4.2.5 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Japan

- 6.4.3.4 Australia

- 6.4.3.5 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.5.4 Rest of Middle East & Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor PLC

- 7.1.2 Bischof + Klein SE & Co. KG

- 7.1.3 Aluflexpack AG

- 7.1.4 ProAmpac Intermediate Inc.

- 7.1.5 Constantia Flexibles Group GmbH

- 7.1.6 Coveris Management GmbH

- 7.1.7 FLAIR Flexible Packaging Corporation

- 7.1.8 Gualapack SpA

- 7.1.9 Hood Packaging Corporation

- 7.1.10 Mondi PLC

- 7.1.11 Scholle IPN

- 7.1.12 Sealed Air Corporation

- 7.1.13 Sonoco Products Company

- 7.1.14 Toppan Inc.

- 7.1.15 TOYO SEIHAN CO LTD (Toyo Seikan Group Holdings Ltd.)

- 7.1.16 Huhtamaki Flexible Packaging

- 7.1.17 Glenroy Inc.

- 7.1.18 Uflex Limited

- 7.1.19 KM Packaging Services Ltd.

- 7.1.20 Eagle Flexible Packaging