|

市场调查报告书

商品编码

1433019

类比混合讯号 IP:市场占有率分析、产业趋势与统计、成长预测(2024-2029 年)Analog and Mixed Signal IP - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

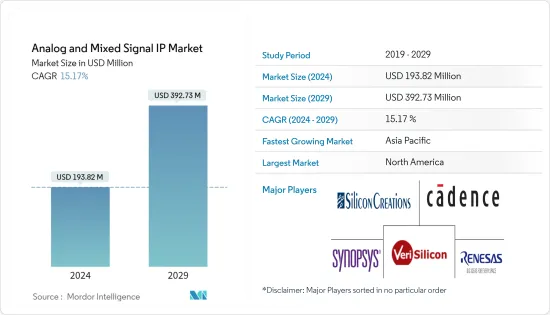

预计2024年类比混合讯号IP市场规模为1.9382亿美元,预估至2029年将达3.9273亿美元,复合年增长率预估为15.17%。

2020年初半导体市场的低迷很大程度上是由于COVID-19大流行对整个产业的影响。由于 COVID-19 在全球蔓延而实施的封锁不仅影响了设备製造,也减少了消费者需求。

根据消费者科技协会统计,2020年美国消费性电子产业成长率下降2.2%,这是美国消费性电子产业几年来首次出现成长下滑。

主要亮点

- 在过去的十年中,积体电路变得越来越复杂和昂贵。业界已开始采用新的设计和重用技术,统称为晶片系统(SoC)、系统级封装 (SiP) 和板载系统 (SoB) 设计。随着这种向小型化的转变,采用此类解决方案的公司已经开始面临这种模式转移带来的重复使用和整合挑战。为了解决此类问题,IP封锁已成为业界最有希望为最终用户提供的解决方案。

- 随着这种向小型化的转变,采用此类解决方案的公司已经开始面临这种模式转移带来的重复使用和整合挑战。为了解决此类问题,IP封锁已成为业界最有希望为最终用户提供的解决方案。

- 可重复使用元件也称为智慧财产权 (IP) 区块或 IP 核,通常是称为软核心的可合成暂存器传输级 (RTL) 设计,或称为硬核心的布局级设计。重复使用的概念运行在模组、平台和晶片级别,涉及使 IP 足够通用、可配置或可编程,以便在广泛的应用中使用。

模拟混合讯号IP市场的趋势

通讯预计将占据较大份额

- 通讯基础设施是推动市场的关键因素之一,主要得益于4G网路和部分5G网路的出现。无线基础设施(特别是 4G 和 5G 网路)製造商不断减小新无线基础设施安装的尺寸和成本,同时维持高标准的效能、功能和服务品质。

- 5G 基础设施预计将彻底改变各种宽频服务领域,并增强多个最终用户的垂直连线。据GSMA称,新的5G网路部署路线已实现约45%的城市覆盖率。中国和印度等国家也计划在2020年之前引入5G网络,而开发5G网络将需要对5G相容基础设施进行大量资本投资。

- 英特尔等重要厂商于 2019 年 1 月宣布推出专用下一代行动基地台设计的新晶片系统(SoC)。同样,覆铜板 (CCL) 专业公司 Iteq 预计将获得来自中国的 5G 基础设施订单。中国政府正大力投资5G服务的开发与部署,华为等本土企业也积极参与。

- Zinwell是有线和无线广播及宽频通讯设备的领先製造商,推出了jjPlus最新的65W磁共振无线电源模组,整合了MaxLinear的AirPHY多Gigabit调变解调器技术和类比混合讯号IP,厚度高达20厘米到第三代ZRA-003 设备,可以透过玻璃窗和结构墙传输电力和Gigabit资料。该解决方案将推动对类比混合讯号 IP 整合的需求,因为它支援Gigabit速度的 4G/LTE 或 5G 毫米波无线宽频服务。

预计北美将占据最大的市场占有率

- 对类比/数位混合讯号 IP 的需求是由于越来越多地使用这些产品作为建构模组而推动的。美国通讯业正在积极投资5G基础设施。该国的终端用户产业占全球5G技术消费的大部分。在北美地区,美国在地区5G投资、部署和应用方面占据主导地位。

- 由于成长放缓,5G 的超高速无线网路特性预计将为电讯业带来急需的推动力。美国美国电讯协会估计,到 2025 年,美国通讯业者将花费约 1,040 亿美元。预计通讯服务供应商必须将其现有的 4G 网路升级到即将推出的 5G 标准,从而全面部署 5G 无线服务。

- 2019 年 10 月,Analogue 宣布推出 Analog Game Boy Pocket,这是復古游戏装置的现代版本。该公司推出的关键组件是第二个 FPGA(除了用于影像处理的FPGA 之外,该 FPGA 可以在比原始 Game Boy 更高解析度 10 倍的显示器上显示高解析度影像)。第二个 FPGA 将允许復古游戏社群建立和移植核心,以便在他们的口袋里运行其他游戏,类似于 MiSTER FPGA 装置的工作方式。

- 预计加拿大将为军事计划(包括服饰)提供足够的支出和资金。加拿大政府正在重点关注「综合士兵系统」计划,该项目将把士兵套装与电子设备、武器结合起来,并在士兵穿越战场时提供士兵之间的通讯。预计这将对该地区的市场成长产生积极影响。

类比和混合讯号 IP 产业概述

随着全球厂商致力于消费性电子、汽车等各种应用中的讯号集成,类比混合讯号IP高度分散,从而在竞争对手之间造成激烈的竞争。主要参与者包括 Cadence Design Systems Inc.、台积电、Global Foundries Inc. 和三星电子。

- 2020 年 5 月 - Synopsys, Inc. 宣布推出基于台积电 5nm 製程技术的最广泛的高品质 IP 产品组合,用于高效能运算晶片系统(SoC)。基于台积电製程的 DesignWare IP 产品组合包括适用于最广泛使用的高速通讯协定的介面和基础 IP,加速了高阶云端运算、AI 加速器、网路和储存应用的 SoC 的开发。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 市场驱动因素

- 提高 AMS 区块的再生性

- 无线通讯的普及

- 市场限制因素

- 类比混合讯号 (AMS) 设计复杂性和灵敏度

- 评估 COVID-19 对产业的影响

第五章市场区隔

- 设计

- 硬/软IP

- 硬IP

- 产品

- A2D 和 D2A 转换器

- 电源管理模组

- RF

- 其他产品

- 最终用户产业

- 消费性电子产品

- 通讯业

- 车

- 工业

- 其他最终用户产业

- 地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第六章 竞争形势

- 公司简介

- Cadence Design Systems Inc.

- Silicon Creations LLC

- VeriSilicon Holdings Co. Ltd

- Renesas Electronics Corporation

- Synopsys Inc.

- ARM Holdings PLC

- Xilinx Inc.

- Intel Corporation

- Analog Devices Inc.

- Maxim Integrated Products Inc.

- Texas Instruments Limited

第七章 投资分析

第八章市场的未来

The Analog and Mixed Signal IP Market size is estimated at USD 193.82 million in 2024, and is expected to reach USD 392.73 million by 2029, growing at a CAGR of 15.17% during the forecast period (2024-2029).

The semiconductor market's downturn at the start of 2020 is significantly owing to the COVID-19 pandemic's impact on the entire industry. The lockdowns that have been enforced by the spread of COVID-19 across the world have not only affected the manufacturing of devices but also reduced consumer's demand.

According to the Consumer Technology Association, the growth rate of the consumer electronics industry in the United States fell by 2.2% in 2020, which was the first decrease in the growth rate in the consumer electronics landscape of the United States after several years.

Key Highlights

- Over the past decade, the integrated circuits have become increasingly complex and expensive. The industry started to embrace new design and reuse methodologies that are collectively referred to as system-on-chip (SoC), System-in-Package (SiP), and System-on-Board (SoB) design. With this shift toward miniaturization, the companies incorporating such solutions started facing the challenges for the re-usage and integration issues encountered in this paradigm shift. To solve such problems, IP blocks emerged as the most prominent solution for the industry end-users.

- Over the past decade, integrated circuits have become increasingly complex and expensive. The industry started to embrace new design and reuse methodologies that are collectively referred to as system-on-chip (SoC), System-in-Package (SiP), and System-on-Board (SoB) design.

- With this shift toward miniaturization, the companies incorporating such solutions started facing the challenges for the reusage and integration issues encountered in this paradigm shift. To solve such issues, IP blocks emerged as the most prominent solution for the industry end-users.

- The reusable components, also called intellectual property (IP) blocks or IP cores are typically synthesizable register-transfer level (RTL) designs referred to as soft cores or layout level designs, referred to as hard cores. The concept of reusage can be carried out at the block, platform, or chip levels and involves making the IP sufficiently general, configurable, or programmable for use in a wide range of applications.

Analog & Mixed Signal IP Market Trends

Telecommunication is Expected Hold a Significant Share

- Telecommunication infrastructure is one of the key factors driving the market, primarily owing to the advent of the 4G network and some parts of the 5G network. Manufacturers of wireless infrastructure, especially 4G and 5G networks, are continuously reducing the size and cost of their newly installed wireless infrastructure while holding towards the high standards of performance, functionality, and quality of service.

- 5G Infrastructure is expected to revolutionize the domain of various broadband services and is expected to empower connectivity across multiple end-user verticals. According to GSMA, around 45% urban coverage level has been achieved for 5G networks in the new deployment trails. Countries like China and India are also planning to implement the 5G network by 2020, and the development of 5G networks requires large amounts of capital investment in 5G capable infrastructure.

- Significant players like Intel have announced a new system on chip (SoC) designed specifically for next-generation mobile base stations in Jan 2019. Similarly, Copper-clad laminate (CCL) specialist Iteq expects orders for 5G infrastructure to pull in from China. The country is investing significantly in the development and deployment of 5G services with the government and local players like Huawei actively taking part

- Zinwell, a leading manufacturer of wired and wireless broadcast and broadband communication equipment has integrated MaxLinear's AirPHY multi-gigabit modem technology with jjPlus's latest 65W magnetic resonant wireless power module integrated with analog mixed-signal IP into its 3rd generation ZRA-003 device, which can transfer power and gigabit data through glass windows or structural walls up to 20cm thick. The solution will enhance the demand of the analog mixed-signal IP integration as the solution will enable 4G/LTE or 5G millimeter wave wireless broadband service with gigabit speeds.

North America is Expected to Hold the Largest Market Share

- The demand for the analog and digital mixed-signal IP is driven by the growing utilization of these products as building blocks. The telecommunication sector in the US has been actively investing in 5G infrastructure. The end-user industry in the country accounts for the significant portion of the global consumption of 5G technology. In the North American region, the US dominates the regional 5G market, regarding investment, adoption, and applications.

- The nature of the 5G superfast wireless networks is expected to provide the needed primary impetus to the telecom industry, which has been experiencing slow growth. The US Telecom Association has estimated that the US telecom operators are expected to spend around USD 104 billion by 2025. It is expected to be essential for the telecom service providers to upgrade existing 4G networks to the upcoming 5G standards and, consequently, execute the full installation of 5G wireless services.

- In October 2019, Analogue announced the launch of its Analogue Game Boy Pocket, which is a modern version of the retro-gaming device. The critical component the company has introduced is the second FPGA (apart from one for image processing to deliver high-resolution image on its 10X high-resolution display compared to the original Game Boy). This second FPGA enables the retro-gaming community to build and port their cores to run other games on the Pocket, similar to how the MiSTER FPGA device works.

- Canada is expected to provide sufficient expenditure and funding for its military programs (including clothing). The Canadian government has been focusing on the Integrated Soldier System Project, which is assimilating the soldier suit with electronic devices, weapons, and feed communication among soldiers as they move through the battlefield. This is expected to impact the market's growth positively in the region.

Analog & Mixed Signal IP Industry Overview

The analog and mixed signal IP is quite fragmented as the global players are engaged in integrating the signal in various applications like consumer electronics, automotive, etc., which gives an intense rivalry among the competitors. Key players are Cadence Design Systems Inc., Taiwan Semiconductor Manufacturing Company Limited, Global foundries Inc., and Samsung Electronics Co. Ltd.

- May 2020 - Synopsys, Inc. announced the broadest portfolio of high-quality IP on TSMC's 5nm process technology for high-performance computing system-on-chips (SoCs). The DesignWare IP portfolio on the TSMC process, encompassing interface IP for the most widely used high-speed protocols and foundation IP, accelerates the development of SoCs for high-end cloud computing, AI accelerators, networking, and storage applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Force Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Market Drivers

- 4.4.1 Increasing Reusability of AMS Block

- 4.4.2 Growing Prevalence of Wireless Communications

- 4.5 Market Restraints

- 4.5.1 Complexity and Sensitivity of Analog/Mixed-Signal (AMS) design

- 4.6 An Assessment of the Impact of COVID-19 on the Industry

5 MARKET SEGMENTATION

- 5.1 Design

- 5.1.1 Firm/Soft IP

- 5.1.2 Hard IP

- 5.2 Product

- 5.2.1 A2D and D2A Converter

- 5.2.2 Power Management Modules

- 5.2.3 RF

- 5.2.4 Other Products

- 5.3 End-user Industry

- 5.3.1 Consumer Electronics

- 5.3.2 Telecommunication

- 5.3.3 Automotive

- 5.3.4 Industrial

- 5.3.5 Other End-user Industries

- 5.4 Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia Pacific

- 5.4.4 Latin America

- 5.4.5 Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles*

- 6.1.1 Cadence Design Systems Inc.

- 6.1.2 Silicon Creations LLC

- 6.1.3 VeriSilicon Holdings Co. Ltd

- 6.1.4 Renesas Electronics Corporation

- 6.1.5 Synopsys Inc.

- 6.1.6 ARM Holdings PLC

- 6.1.7 Xilinx Inc.

- 6.1.8 Intel Corporation

- 6.1.9 Analog Devices Inc.

- 6.1.10 Maxim Integrated Products Inc.

- 6.1.11 Texas Instruments Limited

7 INVESTMENT ANALYSIS

8 FUTURE OF THE MARKET

网际网路通讯协定版本 6 市场:按产品类型、最终用户划分 - 2025-2030 年全球预测

网际网路通讯协定版本 6 市场:按产品类型、最终用户划分 - 2025-2030 年全球预测 通讯介面市场:按类型、最终用户产业、应用、资料速率、组件划分 - 2025-2030 年全球预测

通讯介面市场:按类型、最终用户产业、应用、资料速率、组件划分 - 2025-2030 年全球预测 託管多重通讯协定标籤交换 (MPLS) 全球市场

託管多重通讯协定标籤交换 (MPLS) 全球市场 全球託管多重协定标籤交换(MPLS) 市场,2024-2028

全球託管多重协定标籤交换(MPLS) 市场,2024-2028 全球 IPv6 市场:按产品类型、最终用户和地区划分:分析与预测(2024-2034 年)

全球 IPv6 市场:按产品类型、最终用户和地区划分:分析与预测(2024-2034 年) 2024-2032 年按服务(3 级 VPN、2 级 VPN)、最终用户(IT 和电信、医疗保健、BFSI、零售、製造、政府等)和地区分類的託管 MPLS 市场报告

2024-2032 年按服务(3 级 VPN、2 级 VPN)、最终用户(IT 和电信、医疗保健、BFSI、零售、製造、政府等)和地区分類的託管 MPLS 市场报告 託管 MPLS - 市场占有率分析、产业趋势与统计、成长预测(2024 年 - 2029 年)

託管 MPLS - 市场占有率分析、产业趋势与统计、成长预测(2024 年 - 2029 年) 类比和混合讯号 IP 市场报告:2030 年趋势、预测和竞争分析

类比和混合讯号 IP 市场报告:2030 年趋势、预测和竞争分析 2024-2028 年全球汽车通讯协定市场

2024-2028 年全球汽车通讯协定市场 互联网协议地址管理市场 - 全球行业规模、份额、趋势、机会和预测。按组件、部署、组织规模、地区、公司和地理位置细分,2018-2028 年预测和机会。

互联网协议地址管理市场 - 全球行业规模、份额、趋势、机会和预测。按组件、部署、组织规模、地区、公司和地理位置细分,2018-2028 年预测和机会。