|

市场调查报告书

商品编码

1433490

太阳能建筑一体化(BIPV):市场占有率分析、产业趋势与统计、成长预测(2024-2029)Building Integrated Photovoltaic (BIPV) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

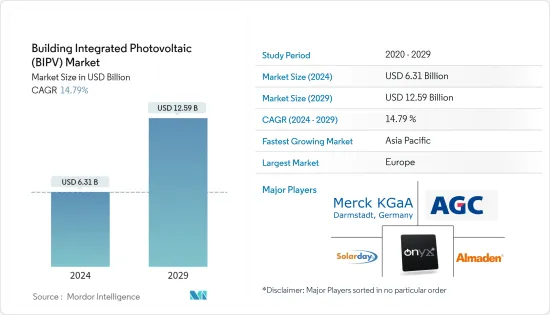

预计2024年太阳能建筑一体化市场规模为63.1亿美元,在预测期内(2024-2029年)预计到2029年将达到125.9亿美元,复合年增长率预计为14.79%。

主要亮点

- 从中期来看,透过自我消费降低水电费和减少建筑物碳排放等因素预计将在预测期内推动市场发展。

- 另一方面,与屋顶太阳能发电系统相比,安装成本较高可能会对市场成长产生负面影响。

- 儘管如此,全球可再生能源发电的趋势不断增长,为 BIPV 系统带来了巨大的机会。几乎所有国家的政府都在致力于制定可再生能源为导向的能源政策,以实现碳中和目标。鼓励工商部门采用清洁能源产出方式。

- 由于太阳能技术成本下降,亚太地区预计在预测期内将增长更快。

太阳能建筑一体化市场趋势

结晶光伏可望主导市场

- 大多数用于屋顶和建筑幕墙应用的太阳能电池板由硅晶型组成。这些厚玻璃比其他技术产生更多的功率(在阳光下每英尺光伏阵列产生 10 至 12 瓦)。

- 随着全球光电模组安装量的不断增加,BIPV系统的安装量也进一步增加。 2022年太阳能发电总装置容量约为1046.6GW,较2021年的855.2GW增加。

- 德国玻璃和建筑材料製造商格林策巴赫集团于2022年9月宣布,其子公司Envelon将在德国巴伐利亚州开设太阳能建筑一体化(BIPV)组件生产工厂,年产能高达30万平方公尺。

- 2021年12月,义大利太阳能板製造商Solarday推出了红、绿、金、灰四种颜色的玻璃结晶PERC BIPV面板。本产品的功率转换效率为17.98%,温度係数为-0.39%/℃。除了更高的电力转换能力之外,改变颜色还可以增加建筑物的美学价值。

- 预计此类发展将对市场开拓产生压倒性影响。

亚太地区预计将出现显着成长

- 亚太地区已成功以最具成本效益的方式将太阳能技术引入许多产业。该地区的技术已达到成熟阶段,价格不断下降。

- 中国、印度、日本和东协等国家已经在太阳能发电领域证明了自己的实力,为 BIPV、屋顶和许多其他应用提供了新技术和创新技术。中国太阳能产业各项技术的生产规模均占全球50%以上,并预计在不久的将来继续保持领先地位。

- 这一发展也发生在该地区的其他地区。 2021年9月,日本玻璃、化学品和高科技材料製造商AGC Inc.宣布,其BIPV玻璃已选定于2024年在新加坡科技大学榜鹅新校区安装。

- 2023 年 5 月,澳洲智慧建筑材料公司 ClearVue Technologies Limited 宣布正式发布改进的产品设计,用于将 Solar Vision 玻璃整合到嵌装玻璃单元或 IGU 中。同时,我们将发布全新的一体化太阳能建筑幕墙解决方案。

- 由于这些发展,预计亚太地区在未来几年将呈现最高成长率。

太阳能建筑一体化产业概况

全球太阳能建筑一体化(BIPV)市场适度整合。市场的主要企业(排名不分先后)包括ONYX Solar Group LLC、Merck KGaA、AGC Inc.、Solarday、常州阿尔玛顿等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 调查先决条件

第二章调查方法

第三章执行摘要

第四章市场概况

- 介绍

- 市场规模及需求预测:至2028年(单位:百万美元)

- 最新趋势和发展

- 政府法规政策

- 市场动态

- 促进因素

- 透过内部发电降低能源成本

- 住宅领域太阳能发电模组安装量增加

- 抑制因素

- 与屋顶太阳能发电系统相比,安装成本更高

- 促进因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

第五章市场区隔

- 类型

- 薄膜光电

- 结晶光电

- 最终用户

- 住宅

- 商业/工业

- 地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 法国

- 英国

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 其他中东/非洲

- 北美洲

第六章 竞争形势

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- Onyx Solar Group LLC

- Merck KGaA

- Nanoflex Power Corporation

- Hanergy Holding Group Ltd.

- AGC Inc.

- Polysolar Domestic

- Issol SA

- Changzhou Almaden Co. Ltd

- Solarday

- Ertex solartechnik GmbH

第七章 市场机会及未来趋势

- 世界可再生能源发电趋势

简介目录

Product Code: 62629

The Building Integrated Photovoltaic Market size is estimated at USD 6.31 billion in 2024, and is expected to reach USD 12.59 billion by 2029, growing at a CAGR of 14.79% during the forecast period (2024-2029).

Key Highlights

- Over the medium term, factors such as the reduction in energy bills due to self-power consumption and the reduction in the building's carbon footprint are expected to drive the market during the forecast period.

- On the other hand, the high installation cost compared to rooftop PV systems is likely to negatively impact the market growth.

- Nevertheless, the inclination towards renewables-based power generation worldwide is an enormous opportunity for BIPV systems. The governments of almost all countries are moving towards renewables-oriented energy policies to reach their carbon neutrality goals. The industrial and commercial sectors are even incentivized to adopt cleaner energy generation methods.

- Due to declining solar technology costs, Asia-Pacific is expected to grow faster during the forecast period.

Building Integrated Photovoltaics Market Trends

Crystalline PV Expected to Dominate the Market

- Most solar panels for roof and facade applications are made up of crystalline silicon. They are thick glasses that produce more power (10-12 watts per ft² of PV array under the full sun) than other technologies.

- The increasing installation of solar PV modules across the globe is further increasing the installation of BIPV systems. In 2022, the total solar PV installed capacity was around 1046.6 GW, which increased from 855.2 GW in 2021.

- In September 2022, Grenzebach Group, a glass and building materials producer in Germany, announced the inauguration of a building-integrated PV (BIPV) module production plant by the company's subsidiary Envelon in Bavaria region in Germany with a capacity of up to 300,000 sq. meter annual capacity.

- In December 2021, Italian solar panel manufacturer Solarday launched a glass-glass monocrystalline PERC BIPV panel in red, green, gold, and grey. The power conversion efficiency of the product is 17.98%, and its temperature coefficient is -0.39% per degree Celsius. Along with higher power conversion capability, it also adds aesthetic value to buildings by varying colors.

- Such developments are expected to have an overwhelming effect on the market development.

Asia-Pacific Expected to Witness Significant Growth

- The Asia-Pacific region has successfully implemented solar PV technologies in many industries in the most cost-effective way. The technology in the region has reached the maturity stage and has witnessed continuously plummeting prices.

- Countries like China, India, Japan, and ASEAN have proved themselves in solar power generation with new innovative technologies for BIPV, rooftops, and many other applications. China's production scale for each technology in the PV industry accounts for more than 50% of the world and is expected to remain at the top in the near future.

- The developments happened in other parts of the region too. In September 2021, AGC Inc., the Japanese manufacturer of glass, chemicals, and high-tech materials, announced that its BIPV glass had been selected to be installed at the Singapore Institute of Technology's new Punggol campus, which is scheduled to be open by 2024.

- In May 2023, a smart building materials Australian company, ClearVue Technologies Limited, announced the official release of its improved product design for integrating solar vision glass into glazing units or IGUs. At the same time, the Company releases its new integrated solar facade solutions.

- Owing to such developments, Asia-Pacific is expected to have the highest growth rate in the coming years.

Building Integrated Photovoltaics Industry Overview

The global building integrated photovoltaic (BIPV) market is moderately consolidated. The key players in this market (not in particular order) include ONYX Solar Group LLC, Merck KGaA, AGC Inc., Solarday, and Changzhou Almaden Co. Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD million, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Reduction in Energy Bills Due to Self-Power Consumption

- 4.5.1.2 Increasing Installation of Solar PV Modules in Residential Segment

- 4.5.2 Restraints

- 4.5.2.1 High Installation Cost as Compared to Rooftop PV Systems

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Thin Film PV

- 5.1.2 Crystalline PV

- 5.2 End-User

- 5.2.1 Residential

- 5.2.2 Commercial & Industrial

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Onyx Solar Group LLC

- 6.3.2 Merck KGaA

- 6.3.3 Nanoflex Power Corporation

- 6.3.4 Hanergy Holding Group Ltd.

- 6.3.5 AGC Inc.

- 6.3.6 Polysolar Domestic

- 6.3.7 Issol SA

- 6.3.8 Changzhou Almaden Co. Ltd

- 6.3.9 Solarday

- 6.3.10 Ertex solartechnik GmbH

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Inclination towards Renewables-based Power Generation Across the World

02-2729-4219

+886-2-2729-4219

建筑整合式光电市场:依产品类型、技术、应用、最终用户、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测

建筑整合式光电市场:依产品类型、技术、应用、最终用户、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测 建筑一体成型光伏建筑幕墙市场(按技术类型、组件、材料类型、设计、安装类型和最终用户划分)—2025-2032 年全球预测按产品类型、整合模式、应用和施工阶段分類的建筑一体化光伏市场—2025-2032年全球预测

建筑一体成型光伏建筑幕墙市场(按技术类型、组件、材料类型、设计、安装类型和最终用户划分)—2025-2032 年全球预测按产品类型、整合模式、应用和施工阶段分類的建筑一体化光伏市场—2025-2032年全球预测 2025年全球建筑整合型太阳能发电市场报告

2025年全球建筑整合型太阳能发电市场报告 建筑一体化光伏市场规模、份额、趋势及预测(按产品类型、应用、最终用途和地区),2025 年至 2033 年

建筑一体化光伏市场规模、份额、趋势及预测(按产品类型、应用、最终用途和地区),2025 年至 2033 年 便携式光电整合市场规模及预测(2021 - 2031 年)、趋势及成长机会分析报告(按应用和地理划分)

便携式光电整合市场规模及预测(2021 - 2031 年)、趋势及成长机会分析报告(按应用和地理划分) 欧洲、中东和北非、北美便携式光伏一体化市场规模及预测(2021 - 2031 年)、区域份额、趋势和成长机会分析报告涵盖范围:按应用和地理划分

欧洲、中东和北非、北美便携式光伏一体化市场规模及预测(2021 - 2031 年)、区域份额、趋势和成长机会分析报告涵盖范围:按应用和地理划分 建筑整合型太阳能发电(BIPV):技术与全球市场

建筑整合型太阳能发电(BIPV):技术与全球市场 全球建筑一体化光伏市场研究报告-产业分析、规模、份额、成长、趋势与预测 2025 年至 2033 年太阳能建筑一体化市场报告:趋势、预测和竞争分析(至 2031 年)

全球建筑一体化光伏市场研究报告-产业分析、规模、份额、成长、趋势与预测 2025 年至 2033 年太阳能建筑一体化市场报告:趋势、预测和竞争分析(至 2031 年)

▼