|

市场调查报告书

商品编码

1433494

紫外线固化黏剂:市场占有率分析、产业趋势与统计、成长预测(2024-2029)UV-Curable Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

UV固化黏剂市场规模预计2024年为47.9亿美元,预计到2029年将达到62.5亿美元,预计在预测期内(2024-2029年)将以5.46%的复合年增长率成长。

新型冠状病毒感染疾病(COVID-19)的爆发导致世界各地的国家封锁,扰乱了製造活动和供应链,并导致生产停止,这对 2020 年的市场产生了负面影响。然而,到了2021年,情况开始好转,从而恢復了市场的成长轨迹。

主要亮点

- 推动该市场研究的主要因素是软包装应用中对紫外线黏剂的需求不断增长,以及由于有利的环境法规而导致的需求不断增长。

- 另一方面,紫外线固化黏剂的高製造成本和替代黏剂的可用性预计将阻碍市场成长。

- 医疗产业不断增长的需求以及具有环境和社会效益的新製程的研发预计将为所研究的市场提供机会。

- 亚太地区主导全球市场,最大的消费来自中国、日本和印度等国家。

UV固化黏剂的市场趋势

包装产业实现强劲成长

- 紫外光固化黏剂用于包装领域,因为它可以快速黏合塑胶、橡胶、金属、玻璃和陶瓷等不同材料。

- 卓越的强度和弹性、耐受恶劣环境的能力以及出色的防潮性等特性使紫外线固化黏剂非常适合包装应用。

- 由于人们越来越认识到使用紫外线固化黏剂的好处,欧洲和北美塑胶包装产业对紫外线固化黏剂的需求一直在增加。这些黏剂消除了翻盖式封装中对热和射频 (RF) 密封的需要。

- 根据印度包装工业协会(PIAI)统计,2019年印度包装市场规模约505亿美元。预计到2025年将达到2,048.1亿美元,2020年至2025年复合年增长率为26.7%。因此,包装行业的成长预计将增加对UV固化黏剂的需求。

- 软包装用于南美洲、非洲和亚太地区低收入国家的食品包装应用。在经济持续扩张和食品和饮料产业加速发展的支持下,软包装在新兴经济体中越来越受欢迎,需求也越来越大。

- 在需要耐候性的产品包装应用中,紫外线固化黏剂越来越多地用于层压薄膜、纸张和箔片。

- 随着电子商务、电子零售、线上食品订购和配送服务的不断发展,对包装材料特别是软包装的需求不断增加。这可能会增加预测期内对紫外线固化黏剂的需求。在德国,2021年和2022年纸包装产业与前一年相比显着成长。

- 上述因素正在推动UV固化黏剂市场的成长。

亚太地区主导市场

- 预计亚太地区将主导全球紫外线固化黏剂市场。中国、印度和日本等国家对包装和医疗行业投资的增加以及电气和电子设备产量的增加正在增加该地区紫外线固化黏剂的使用。

- 在亚太地区,由于生活方式的改变、人们可支配收入的增加、专业人士数量的增加以及对快餐的日益偏好,对加工食品的偏好正在增加。消费者更喜欢即食食品,因为它们所需的烹饪时间显着减少、新鲜、包装美观且耐用,并且能够满足调查市场的需求。

- 人均收入的上升和电商巨头的崛起,使中国成为全球最大的包装材料消费国。根据印度塑胶工业协会统计,印度包装工业位居世界第五,每年以约22-25%的速度成长。由于高技术纯熟劳工和低廉的人事费用,食品包装和加工成本可比欧洲低40%。人口的增长和对包装的需求的增加预计将推动市场的发展。

- 此外,由于经济扩张和高购买力中阶的壮大,近年来中国包装产业持续快速成长。食品包装是包装产业的主要参与者,在中国总市场中占有很大份额。根据Interpack统计,在中国食品包装领域,预计2023年包装总数将达到4,470亿件,显示包装业对紫外光固化黏剂的需求不断增加。

- 另一方面,日本是技术进步中心,拥有活跃的研发基地,用于研发更新、更高效的紫外线固化黏剂。这些因素导致了该国用于包装、电气和汽车应用的新型紫外线固化黏剂产品的出现。

- 上述因素预计将增加预测期内紫外线固化黏剂市场成长的需求。

UV固化黏剂产业概况

紫外线固化黏剂市场得到整合,少数厂商占据了市场需求的很大一部分。这些主要企业包括 Dymax Corporation、3M、HB Fuller、Henkel AG &Company KGaA 和 DELO Industrial Adhesives。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 软包装应用中对 UV黏剂的需求增加

- 由于有利的环境法规,需求增加

- 其他司机

- 抑制因素

- 生产紫外线固化黏剂的高成本

- 替代黏剂的可用性

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(以金额为准的市场规模)

- 树脂型

- 硅胶

- 丙烯酸纤维

- 聚氨酯

- 环氧树脂

- 其他树脂类型

- 最终用户产业

- 医疗保健

- 电力/电子

- 运输

- 包装

- 家具

- 其他最终用户产业

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲

- 亚太地区

第六章 竞争形势

- 併购、合资、联盟、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- 3M

- DELO

- Dymax

- Epoxy Technology Inc.

- HB Fuller Company

- Henkel AG & Co. KGaA

- Master Bond Inc.

- Panacol-Elosol GmbH

- Parson Adhesives, Inc.

- Permabond

- Sika AG

- Heraeus Holding

- Dexerials Corporation

- EpoxySet, Inc.

第七章 市场机会及未来趋势

- 医疗产业需求增加

- 研究和开发可带来环境和社会效益的新工艺

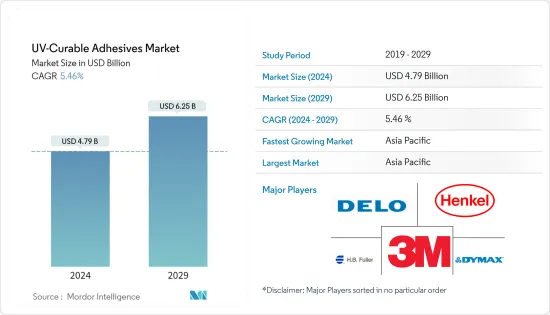

The UV-Curable Adhesives Market size is estimated at USD 4.79 billion in 2024, and is expected to reach USD 6.25 billion by 2029, growing at a CAGR of 5.46% during the forecast period (2024-2029).

Due to the COVID-19 outbreak, nationwide lockdowns worldwide, disruption in manufacturing activities and supply chains, and production halts negatively impacted the market in 2020. However, the conditions started recovering in 2021, thereby restoring the growth trajectory of the market

Key Highlights

- The major factors driving the market studied are the rising demand for UV adhesives in flexible packaging applications and increasing demand due to favorable environmental regulations.

- On the flip side, the high cost of producing UV-curable adhesives and the availability of alternative adhesives are expected to hinder the market's growth.

- An increase in demand from the medical industry and research and development in novel processes offering environmental and social benefits are expected to act as opportunities for the market studied.

- Asia-Pacific dominated the market worldwide, with the largest consumption from countries like China, Japan, and India.

UV-Curable Adhesives Market Trends

Packaging Segment to Witness Strong Growth

- UV-curable adhesives find their applications in the packaging sector, owing to their ability to create quick bonds between different materials, such as plastic, rubber, metal, glass, and ceramic.

- Properties such as superior strength and flexibility, ability to withstand extreme environments, and excellent moisture resistance make UV-curable adhesives suitable for packaging applications.

- The demand for UV-curable adhesives from the plastic packaging industry is consistently increasing in Europe and North America, with growing awareness about the benefits of using UV-curable adhesives. These adhesives eliminate heat and Radio Frequency (RF) sealing of clamshell packages.

- According to the Packaging Industry Association of India (PIAI), Indian Packaging Market accounted for around USD 50.5 billion in 2019. It is expected to reach USD 204.81 billion by 2025 growing at a CAGR of 26.7% during 2020-2025. Therefore, the growth in the packaging industry is expected to increase the demand for UV-curable adhesives.

- Flexible packaging is used in food packaging applications in low-income South America, Africa, and Asia-Pacific countries. The popularity and demand for flexible packaging are rising in emerging economies, and the demand is supported by continued economic expansion and an acceleration in the food and beverage industry.

- The UV-curable adhesive usage as laminating films, papers, and foils is increasing in product packaging applications where weather resistance is required.

- With the growing trend of e-commerce, e-retail, and online food orders and delivery services, the demand for packaging materials, especially flexible packaging, is increasing. It will likely drive the demand for UV-curable adhesives during the forecast period. In Germany, the paper packaging industry grew significantly in 2021 and 2022 compared to previous years.

- The factors above are driving the UV-curable adhesives market growth.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region is expected to dominate the global UV-curable adhesives market. With growing investments in the packaging and medical industry and increasing electrical and electronics production in countries such as China, India, and Japan, the usage of UV-curable adhesives is increasing in the region.

- In Asia-Pacific, the demand for packaged food is growing, owing to lifestyle changes, the growing disposable income of people, the increasing number of working professionals, and the growing preference for fast food. Consumers prefer ready-to-consume foods because they require considerably less time for cooking, are fresh, and contain attractive and sturdy packaging, supporting the demand for the market studied.

- China is the world's largest packaging consumer globally, owing to growing per capita income and rising e-commerce giants. India's packaging industry is the fifth-largest globally, growing at about 22-25% per year, as per the Plastics Industry Association of India. Packaging and processing food costs can be 40% lower than in Europe because of highly skilled labor and cheap labor costs. The growing population and increasing demand for packaging are expected to drive the market.

- Furthermore, the Chinese packaging industry grew rapidly and consistently in recent years, owing to the expanding economy and rising middle class with greater purchasing power. Food packaging is a major player in the packaging industry, accounting for a significant share of the total market in China. According to Interpak, in China, in the foodstuff packaging category, total packaging is expected to reach 447 billion units in 2023, indicating an increased demand for UV-curable adhesives from the packaging industry.

- On the other hand, Japan is a hub for technological advancements and hosts an active R&D base for R&D of newer and more efficient UV-curable adhesives. Due to these factors, novel UV-curable adhesive products are emerging for applications in the country's packaging, electrical, and automotive sectors.

- The abovementioned factor is expected to boost the demand for UV-curable adhesives market growth during the forecast period.

UV-Curable Adhesives Industry Overview

The UV-curable adhesives market is consolidated, where few players account for a significant portion of the market demand. These major players include Dymax Corporation, 3M, H.B. Fuller, Henkel AG & Company KGaA, and DELO Industrial Adhesives.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand for UV Adhesives in Flexible Packaging Application

- 4.1.2 Increasing Demand Due to Favourable Environmental Regulations

- 4.1.3 Others Drivers

- 4.2 Restraints

- 4.2.1 High Cost Associated with the Production of UV-Curable Adhesives

- 4.2.2 Availability of Alternative Adhesives

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Resin Type

- 5.1.1 Silicone

- 5.1.2 Acrylic

- 5.1.3 Polyurethane

- 5.1.4 Epoxy

- 5.1.5 Other Resin Types

- 5.2 End-user Industry

- 5.2.1 Medical

- 5.2.2 Electrical and Electronics

- 5.2.3 Transportation

- 5.2.4 Packaging

- 5.2.5 Furniture

- 5.2.6 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 DELO

- 6.4.3 Dymax

- 6.4.4 Epoxy Technology Inc.

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Master Bond Inc.

- 6.4.8 Panacol-Elosol GmbH

- 6.4.9 Parson Adhesives, Inc.

- 6.4.10 Permabond

- 6.4.11 Sika AG

- 6.4.12 Heraeus Holding

- 6.4.13 Dexerials Corporation

- 6.4.14 EpoxySet, Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increase in Demand From Medical Industry

- 7.2 Research and Development in Novel Processes Offering Environmental and Social Benefits

紫外线固化黏剂市场:按类型、按最终用途行业、按应用、按技术、按原材料、按基材、按固化方法、按黏度、按产品形式 - 2025-2030 年全球预测

紫外线固化黏剂市场:按类型、按最终用途行业、按应用、按技术、按原材料、按基材、按固化方法、按黏度、按产品形式 - 2025-2030 年全球预测 全球紫外线固化黏剂市场(2024-2028)

全球紫外线固化黏剂市场(2024-2028) 2024-2032 年按树脂类型、基材、最终用户和地区分類的紫外线固化黏合剂市场报告

2024-2032 年按树脂类型、基材、最终用户和地区分類的紫外线固化黏合剂市场报告 2024 年 UV黏剂世界市场报告

2024 年 UV黏剂世界市场报告 紫外线固化黏合剂市场 - 2018-2028 年全球产业规模、份额、趋势、机会和预测,按树脂类型、按应用、地区和竞争细分

紫外线固化黏合剂市场 - 2018-2028 年全球产业规模、份额、趋势、机会和预测,按树脂类型、按应用、地区和竞争细分 UV 粘合剂市场 - 副产品(有机硅、丙烯酸、聚氨酯、环氧树脂)、最终用户(医疗、电子、汽车、化妆品、工业装配)及预测:2023-2032 年

UV 粘合剂市场 - 副产品(有机硅、丙烯酸、聚氨酯、环氧树脂)、最终用户(医疗、电子、汽车、化妆品、工业装配)及预测:2023-2032 年