|

市场调查报告书

商品编码

1641912

行动加密:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Mobile Encryption - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

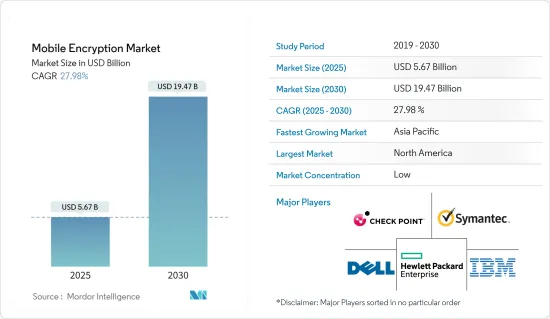

行动加密货币市场规模预计在 2025 年为 56.7 亿美元,预计到 2030 年将达到 194.7 亿美元,预测期内(2025-2030 年)的复合年增长率为 27.98%。

随着企业适应日益普遍的监管和合规要求以及更严格的内部政策,主要企业采用加密的数量和范围都在增长。

主要亮点

- 行动加密是使用某种语言或代码对资料进行加密的过程,只有获得授权的个人才能使用正确的解密金钥来破解。由于人们对资料安全和隐私的担忧日益加剧,市场正在迅速扩张。由于大多数人依赖行动装置来储存敏感资讯(如财务资料、个人资讯和机密商业机密),对行动加密解决方案的需求变得越来越重要。

- 高阶威胁的出现和演变、云端服务的日益普及、行动装置的广泛使用和虚拟是扰乱行动加密市场的关键因素。严格的合规和监管要求的需求以及对智慧财产权安全和隐私日益增长的担忧是推动市场发展的主要因素。此外,各类终端用户中「物联网」的日益增长的趋势也是推动行动加密市场扩张的关键因素。

- 行动加密可保护客户资料不被外部人员获取,确保其隐私和安全。随着智慧型手机付款的使用增加,数位付款的数量急剧增加。为了改善现有的付款系统,公司正在将区块链融入行动付款中。区块链最大的特点就是有效性,为安全可靠的交易树立了标竿。

- BYOD(自带设备)现象及其在几乎所有组织中的迅速普及,迫使人们从根本上重新思考安全方法,从而导致组织采用许多不同的加密技术。因此,有效、安全地管理策略和金钥已成为日益艰鉅的挑战。

- 随着组织部署越来越多的行动劳动力,过去几年对行动加密的需求急剧增加。行动劳动力有许多好处,包括提高生产力、降低开支和提高灵活性。随着越来越多的企业继续采用行动工作者,市场在过去几年中实现了显着增长,而且这一趋势预计还将继续下去。

- 不同行业对加密的综合使用有很大差异。具体而言,采用率最高的是监管严格且依赖行动的行业,例如金融服务和 IT 服务,而采用率最低的是监管较少的行业,例如製造业和消费品。

- 此外,一个主要的障碍是组织没有意识到行动加密解决方案的重要性。加密解决方案的复杂性、加密技术缺乏行业标准以及对加密可能对设备性能产生影响的担忧是进一步的限制。

- 新冠疫情的封锁和限制导致行动技术的使用比平常更高。随着安全设备互通性需求的增加并成为新常态,对行动加密的需求预计将大幅增加。

行动加密货币市场趋势

BFSI 预计将占据主要市场占有率

- 为了确保行动应用程式的安全,银行采用了许多加密技术。对于传输中的资料,常见的技术有传输层安全性(TLS)和安全通讯端层(SSL),而对于静止的资料,常见的技术有高级加密标准(AES)和RSA(RSA)。是一种技术。为了进一步保护客户讯息,银行还可以采用多因素身份验证和设备指纹识别等额外的安全措施。推动这一成长的原因是银行业对付款安全解决方案的需求不断增长,以便为消费者提供更安全的服务。

- 目前已确定的将影响这一细分市场的趋势之一是,使用加密的 OTP SMS 越来越受欢迎,可以避免网路钓鱼、中间人攻击和恶意软体木马等可能的攻击。就是其中之一。由于客户的大部分银行帐户资讯和密码都储存在他们的行动装置上,甚至个人照片(在网路上申请贷款时)也是一个重大的安全隐患。 SSL/TLS 支援透过网路安全传输个人资料,例如信用卡资讯、密码和其他敏感个人资讯。

- 银行和金融机构使用 SSL/TLS 加密流量来解决其中的几个问题,包括控制存取、保护机密性和减少针对特定通讯协定的攻击。随着线上交易变得越来越复杂,付款提供者正在努力跟上技术以提供更好的安全性。由于目前大多数线上付款都是行动支付或应用程式内付款,传统的 PCI-DSS 标准需要进行适当升级。

- 此外,预计人工智慧(AI)的加入将提高金融加密软体的效率和有效性。同时,它可以帮助组织和客户满足日益增长的资料保护需求。因此,我们可以预见银行和金融领域将迅速采用基于人工智慧的加密软体。

- 银行必须在资料的整个生命週期中维护资料的完整性。因此,银行必须制定适合其需求的适当的威胁侦测和回应程序。因此,银行可以透过实施资料遮罩和加密软体等各种安全标准来维护资料完整性。因此,银行、金融和保险 (BFSI) 行业对金融加密软体的需求预计将上升。

- 过时的 SSL 标准阻碍了 EMV 三域安全 (3DS) 等新倡议的使用。使用两种平行演算法对通讯进行加密目前被认为是最强大的加密形式,密码学家预测双单元加密在整个预测期内仍将保持这种状态。

预计北美将占据较大的市场占有率

- 在北美,美国企业越来越依赖电脑网路和电子资料来进行日常业务,个人和财务资讯透过行动电话传输并储存在云端的情况正在增加。此外,BYOD 趋势的显着上升也推动了对智慧卡、实体令牌和 KPI 等高级身份验证方法的需求,以存取敏感资讯并登入用户端伺服器。

- 这项优势源自于加拿大和美国等国家不断提高的监管标准,要求银行加强资料隐私。为了保护隐私,公共银行和私人银行都对加密软体的需求越来越大。此外,网路攻击和对关键业务资讯的威胁的激增预计将刺激该地区的市场扩张。

- 在美国,估计约有 51% 的行动装置具有全碟加密功能,预计未来几年这一数字还会增加。然而,随着全盘加密的广泛采用,几乎所有这些设备都有可能无法被执法部门存取。这就是政府监管加密货币市场的原因。谷歌等科技巨头面临限制和障碍。

- AAG IT Services 估计,到 2021 年,一半的美国网路用户的帐户将遭到入侵。十分之一的美国公司没有针对网路攻击的防御措施。此外,2022 年上半年网路犯罪影响了 5,335 万美国个人。因此,日益严格的个人资讯保护法和行动付款技术有望为该领域开闢新的产业前景。

- 苹果是行动全盘加密领域的领导者,美国大约 55% 的行动装置运行 iOS。北美的恶意资料外洩事件正在增加,并且是最大的加密服务市场。

行动加密行业概览

全球行动加密货币市场是分散的,因为行动加密货币生态系统由各种行动加密货币解决方案和服务供应商组成。主要企业正在部署各种策略,如新产品发布、临床试验和市场计划,透过大量投入研发、合资、伙伴关係和收购来扩大其在这个市场的影响力和创新。市场的主要企业包括 IBM 公司、HP Enterprises、戴尔、赛门铁克和 Checkpoint Software。

- 2022 年 10 月 - 全球领先的网路安全解决方案供应商 Check Point Software Technologies Ltd. 获得了以色列公司 Check Point 的认可,后者是开发人员的开发人员优先安全工具的领先创新者。新兴企业Spectral。此次收购增强了 Check Point 的云端解决方案 Check Point CloudGuard,使其具备了以开发人员为先的安全功能,从而提供最广泛的云端应用程式安全解决方案,包括基础设施即程式码(IaC) 扫描和硬编码机密检测。

- 2022 年 12 月 - RingCentral, Inc. 宣布正在扩展其旗舰产品 RingCentral MVP 的端对端加密 (E2EE) 功能,除了视讯之外,还包括电话通话和通讯。 E2EE技术保护使用者的通讯内容不被未授权存取。这不仅可以防止外部入侵和攻击,还可以确保注重安全的组织的特权讨论的隐私。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查结果

- 调查前提

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 市场驱动因素与限制因素简介

- 市场驱动因素

- 企业对安全通讯的需求日益增加

- 资料安全和智慧财产权隐私问题日益令人担忧

- 市场限制

- 缺乏意识和熟练劳动力

- 价值链/供应链分析

- 产业吸引力-波特五力分析

- 购买者/消费者的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 按组件

- 解决方案

- 服务

- 按应用

- 磁碟加密

- 文件/资料夹加密

- Web通讯加密

- 云端加密

- 其他应用

- 依部署类型

- 本地

- 云

- 按公司规模

- 中小企业

- 大型企业

- 按最终用户

- BFSI

- 航太和国防

- 卫生保健

- 政府及公共机构

- 电讯

- 零售

- 其他最终用户

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第六章 竞争格局

- 公司简介

- Dell

- Check Point Software Technologies, Ltd

- Hewlett Packard Enterprise

- IBM Corporation

- KoolSpan, Inc.

- MobileIron, Inc.

- SecurStar GmbH

- Silent Circle, LLC

- Sophos Ltd.

- Symantec Corporation

- T-Systems International GmbH

第七章投资分析

第八章 市场机会与未来趋势

The Mobile Encryption Market size is estimated at USD 5.67 billion in 2025, and is expected to reach USD 19.47 billion by 2030, at a CAGR of 27.98% during the forecast period (2025-2030).

As organizations have adapted to increasingly pervasive regulatory and compliance mandates and more stringent internal policies, encryption deployments have increased in number and scope in significant enterprises.

Key Highlights

- Mobile encryption is the process of encoding data in a language or code only authorized individuals with the right decryption key can decipher. Due to increased worries about data security and privacy, the market is expanding quickly. The demand for mobile encryption solutions is becoming increasingly critical as most people utilize mobile devices to store sensitive information like financial data, personal information, and confidential corporate information.

- Increasing and evolving advanced threats, the enhanced adoption of cloud services, mobile device proliferation, and virtualization are the major factors creating disruptive changes in the mobile encryption market. The need for stringent compliance and regulatory requirements and increasing concern for the security and privacy of intellectual property are the major factors driving the market. Also, the rising trend of the Internet of Things among various end-user verticals is a crucial factor facilitating the expansion of the mobile encryption market.

- Mobile encryption safeguards customer data by making it unintelligible to outsiders, ensuring it remains private and secure. The number of digital payments has increased dramatically as a result of the rise in smartphone payment usage. To improve the present payment system, businesses are integrating blockchain with mobile payment. The most important feature of blockchain is its effectiveness, which establishes a benchmark for safe and secure transactions.

- The "bring your own device" (BYOD) phenomenon and its incredibly fast and pervasive adoption by almost every organization necessitated a fundamental rethinking of security approaches, and it has been found that organizations are deploying many disparate encryption platforms. As a result, managing policies and keys efficiently and securely is an increasingly troublesome challenge.

- The demand for mobile encryption has grown dramatically over the years as organizations increasingly deploy a mobile workforce. A mobile workforce has many advantages, including increased productivity, lower expenses, and more flexibility. As more businesses continue to employ a mobile workforce, the market has consequently experienced considerable expansion over the past few years, and this trend is projected to continue in the years to come.

- The comprehensive use of encryption varies considerably by industry segment. Specifically, heavily regulated and mobile-dependent industries, such as financial services and IT services, have the highest use rate, and less regulated industries, such as manufacturing and consumer products, have the lowest use rate.

- Additionally, one major barrier is that organizations do not recognize the importance of mobile encryption solutions. Concerns regarding the complexity of encryption solutions, the absence of industry standards for encryption technology, and the possible effects of encryption on device performance are some further limitations.

- COVID Lockdowns and limitations increased mobile technology use more than usual. As the need for security device interoperability grows and becomes the new standard, there will be a significant rise in demand for mobile encryption.

Mobile Encryption Market Trends

BFSI is Expected to Hold a Major Market Share

- For the security of their mobile apps, banks employ a number of encryption techniques. For data in transit, common techniques include Transport Layer Security (TLS) and Secure Sockets Layer (SSL), whereas for data at rest, common techniques include Advanced Encryption Standard (AES) or RSA. To further safeguard customer information, banks may additionally employ extra security measures like multi-factor authentication and device fingerprinting. The banking industry's expanding requirement for payment security solutions to offer its consumers a more secure service is what is causing the growth.

- Among the current identified trends influencing this segment of the market, the usage of encrypted OTP SMS is one of them, along with a PIN to avoid any possible attacks like phishing, man-in-the-middle attacks, and malware Trojans. As more of the bank account information and passwords of customers come on mobile devices, even personal pictures (while applying for loans online) have become a major security concern. SSL/TLS enables secure transmissions of private data over the internet, including credit card details, passwords, and sensitive personal information.

- Banks and financial institutions use SSL/TLS to encrypt their traffic to address these multiple issues, including controlling access, protecting confidentiality, and reducing exposure to protocol-specific attacks. With the increased sophistication of online transactions, payment providers are catching up with the technologies to provide better security. The majority of online payments are now mobile or in-app payments; the traditional PCI-DSS standards have to be suitably upgraded.

- Moreover, it is projected that the efficiency and effectiveness of financial encryption software would grow with the addition of artificial intelligence (AI). At the same time, it helps organisations and customers meet the growing demand for data protection. As a result, it is anticipated that encryption software powered by artificial intelligence would be quickly adopted by the banking and finance sector.

- The integrity of the data must be maintained by the banks throughout the life of the data. As a result, it is essential for banks to put in place the appropriate threat detection and response procedures in accordance with their needs. Thus, by imposing various security standards, such as data masking and encryption software by banks, the data integrity can be preserved. As a result, it is anticipated that the banking, finance, and insurance (BFSI) industry will see an increase in demand for financial encryption software.

- The outdated SSL standards prevent the use of new initiatives like EMV Three-Domain Secure (3DS), a messaging mechanism that enables customers to authenticate themselves with their card issuer when making card-not-present online purchases.. Communication that uses two algorithms for encryption that work side-by-side is currently considered the strongest encryption, with cryptologists predicting double-cell encryption to remain so over the forecast period.

North America is Expected to Hold a Major Market Share

- In the North American region, the United States business sector increasingly depends on computer networks and electronic data to conduct its daily operations, and growing pools of personal and financial information are also transferred and stored in the cloud using phones. Furthermore, a significant increase in the BYOD trend is also favoring the conditions for advanced authentication methods, such as smart cards, physical tokens, and KPIs, to access sensitive information or log in to client servers.

- The dominance can be attributed to the more stringent regulatory standards in nations like Canada and the United States, which oblige banks to increase data privacy. In order to protect privacy, both public and private banks have increased their demand for cryptographic software. Additionally, the regional market expansion is anticipated to be fueled by the surge in cyberattacks and the threat to business-critical information.

- It is estimated that around 51% of mobile devices in the United States have full disk encryption, which is expected to increase in the coming years. However, with the growth in the adoption of full disk encryption, almost all these devices could become inaccessible to law enforcement. As a result, the government is regulating the encryption market. Companies like Google and other tech giants are facing restrictions and obstacles.

- AAG IT Services estimates that in 2021, 1 in 2 American internet users had their accounts breached. One in ten US businesses do not have any protection against cyberattacks. In addition, cybercrime had an impact on 53.35 million US individuals in the first half of 2022. Therefore, rising privacy laws and mobile payment technology are anticipated to open up new industry prospects in the area.

- Apple is the largest provider of mobile full-disk encryption, and around 55% of the mobile devices in the United States run on iOS. With increased malicious data breaches occurring in the North American region, it has become the largest market for encryption services.

Mobile Encryption Industry Overview

The Global Mobile Encryption Market is fragmented, as the mobile encryption ecosystem comprises various mobile encryption solutions and service providers. The major players deploy various strategies, such as new product launches and clinical trials, and are also taking market initiatives and innovations through high expenditure on research and development, joint ventures, partnerships, acquisitions, and others to increase their footprints in this market. Some of the major players in the market are IBM Corporation, HP Enterprises, Dell, Symantec, and Checkpoint Software, among others.

- October 2022 - Check Point Software Technologies Ltd., a top global provider of cyber security solutions, acquired Spectral, an Israeli startup that was a key innovator in developer-first security tools created by developers for developers. With this purchase, Check Point was expected to increase the developer-first security capabilities of its cloud solution, Check Point CloudGuard, and offer the broadest range of cloud application security use cases, including infrastructure as code (IaC) scanning and hardcoded secret detection.

- December 2022 - RingCentral, Inc. announced that it is extending End-to-End Encryption (E2EE) capabilities in its flagship RingCentral MVP product to encompass both phone and messaging in addition to video. E2EE technology shields users' communication content from being accessed by unauthorised parties. This offers protection against infiltration and attacks from outside parties as well as privacy for privileged discussions for security-conscious organisations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Growing demand for secure communication in enterprises

- 4.3.2 Increasing concern for data security and privacy of intellectual property

- 4.4 Market Restraints

- 4.4.1 Lack of awareness and skilled workforce

- 4.5 Value Chain / Supply Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers/Consumers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 Application

- 5.2.1 Disk Encryption

- 5.2.2 File/Folder Encryption

- 5.2.3 Web Communication Encryption

- 5.2.4 Cloud Encryption

- 5.2.5 Other Applications

- 5.3 Deployment Type

- 5.3.1 On-premise

- 5.3.2 Cloud

- 5.4 Enterprise Size

- 5.4.1 SMEs

- 5.4.2 Large Enterprises

- 5.5 End Users

- 5.5.1 BFSI

- 5.5.2 Aerospace and Defense

- 5.5.3 Healthcare

- 5.5.4 Government and Public Sector

- 5.5.5 Telecom

- 5.5.6 Retail

- 5.5.7 Other End Users

- 5.6 Geography

- 5.6.1 North America

- 5.6.2 Europe

- 5.6.3 Asia Pacific

- 5.6.4 Latin America

- 5.6.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Dell

- 6.1.2 Check Point Software Technologies, Ltd

- 6.1.3 Hewlett Packard Enterprise

- 6.1.4 IBM Corporation

- 6.1.5 KoolSpan, Inc.

- 6.1.6 MobileIron, Inc.

- 6.1.7 SecurStar GmbH

- 6.1.8 Silent Circle, LLC

- 6.1.9 Sophos Ltd.

- 6.1.10 Symantec Corporation

- 6.1.11 T-Systems International GmbH