|

市场调查报告书

商品编码

1433508

云端监控:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Cloud Monitoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

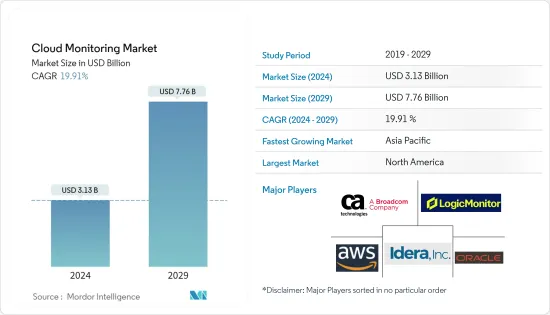

云端监控市场规模预计 2024 年为 31.3 亿美元,预计到 2029 年将达到 77.6 亿美元,预测期内(2024-2029 年)复合年增长率为 19.91%

主要亮点

- 云端监控市场是指提供监控和管理云端基础的基础架构、应用程式和服务的工具、解决方案和服务的产业。云端监控涉及收集、分析和视觉化与云端资源的效能、可用性和安全性相关的资料。

- 云端监控解决方案可协助组织维持云端环境平稳运作、侦测和解决效能问题、最佳化资源利用率并确保遵守服务等级协定。这些解决方案通常提供即时监控、效能分析、警报、日誌分析、安全监控和容量规划等功能。

- 最终用户产业正在采用云端来实现规模和敏捷性。然而,清楚地了解云端环境的效能可能很困难。智慧管理复杂且不断变化的应用程式和基础架构需要像云端一样动态的监控解决方案。

- 此外,银行、金融服务和保险 (BFSI)、资讯技术 (IT) 和零售等行业越来越多地采用云端技术,正在推动云端监控市场的成长。云端监控是整体云端管理策略的关键要素,它允许 IT 管理员查看云端基础的资源的运作状态。

- 客户关係管理、人力资本管理、企业资源管理和其他财务应用程式等软体即服务 (SaaS) 产品的采用正在不断增长,特别是在正在实施云端监控的大型组织中。被创建。

- 在云端环境中实现全面的可视性可能很困难,特别是那些具有复杂架构、分散式系统以及多重云端或混合云端配置的环境。组织可能难以有效监控和管理云端资源,从而导致营运效率降低、效能问题风险增加以及潜在的停机时间。可见性限制可能是由于不同云端平台之间缺乏标准化监控介面、监控工具不足以及难以关联不同来源的资料等因素所造成的。

- 随着组织迅速过渡到远距工作环境,COVID-19感染疾病加速了云端技术的采用。云端平台对于确保业务连续性和实现远端协作至关重要。对云端的日益依赖增加了对云端监控解决方案的需求,以确保云端环境的效能、可用性和安全性。即使在疫情大流行之后,由于各种最终用户对云端的采用率不断增加,市场仍继续快速成长。

云端监控市场趋势

最终用户增加云端采用预计将推动市场成长

- 提高最终用户的云端采用率是云端监控市场的关键驱动力。随着越来越多的组织将其基础架构、应用程式和资料迁移到云端中,云端环境的有效监控和管理变得至关重要。

- 云端监控涉及收集、分析和视觉化有关云端资源和服务的效能、可用性和安全性的资料。这有助于组织确保其云端基础架构的最佳运行,识别和解决效能问题,并确保遵守服务等级协定。

- 云端环境提供了根据需求扩展或缩减资源的能力。然而,这种动态性质使得资源难以监控和管理。云端监控工具提供资源使用情况的即时可见性,以确保最佳的可扩展性和成本效率。

- 组织越来越多地将IT基础设施从本地迁移到云端环境,例如 Amazon Web Services (AWS)、Microsoft Azure、Oracle、阿里巴巴、IBM Cloud 和 Google Cloud Platform。在此过渡期间,监控解决方案对于追踪云端中应用程式和基础架构组件的效能至关重要。据 Flexera Software 称,到 2023 年,47% 的受访者将已经在 Amazon Web Services (AWS) 上运行关键工作负载。

- 云端基础的应用程式通常具有复杂的架构,其中包含各种元件、微服务和相依性。监控这些分散式环境需要专用的工具来追踪不同服务的效能并提供对系统互动和依赖关係的洞察。

亚太地区预计将成为成长最快的地区

- 亚太地区 (APAC) 的云端监控市场正在显着成长。该地区越来越多地采用云端技术、数位转型计画以及资料中心的激增,都有助于亚太地区云端监控市场的扩张。

- 中国、日本、新加坡和澳洲等亚太国家的云端采用率正在迅速增加。银行、医疗保健、製造和零售等行业的组织正在将其基础设施和应用程式迁移到云端。这种广泛的采用增加了对云端监控解决方案的需求,以确保云端环境的效能、可用性和安全性。

- 亚太地区国家正积极推行数位转型,以加强业务营运、改善客户体验并推动创新。云端技术在实现数位转型方面发挥关键作用,监控这些云端环境以确保无缝营运和资源的最佳利用非常重要。

- 根据中国资讯通讯研究院(CAICT)统计,2022年中国云端运算业务成长56.6%,达到2,091亿元人民币(329亿美元)。预计未来三年市场将快速扩张,到2023年将突破4,000亿元。

- 由于对云端服务的需求不断增长以及企业产生的资料量不断增加,亚太地区正在对资料中心进行大量投资。云端监控解决方案对于管理和监控这些资料中心的效能并确保服务的高效运作和高可用性至关重要。

云端监控产业概况

云端监控市场适度分散,主要参与者包括 AWS、Broadcom Inc. (CA Technologies)、IDERA Inc.、LogicMonitor Inc. 和 Oracle Corporation。市场参与者正在采取合作伙伴关係、创新和收购等策略来增强其产品供应并获得永续的竞争优势。

2023 年 4 月,Amazon Web Services (AWS) 推出了 AWS 云端营运能力。 AWS 云端营运涵盖五个基本解决方案领域:云端财务管理、云端管治、云端监控和可观察性、云端合规性和审核以及云端营运管理。新的能力允许客户选择检验的AWS 合作伙伴,这些合作伙伴透过跨多个领域的整合方法提供全面的解决方案。

2022 年 6 月,思科发布了 AppDynamics Cloud,这是一个云端原生可观测平台,适用于建置在日益复杂的分散式架构和服务上的现代应用程式。它专为简单性、效用和直觉性而设计,使 IT 团队能够创造组织、客户和最终用户当今所需的出色数位体验。目前的 AppDynamics 客户可以升级到 AppDynamics Cloud 并继续使用现有的应用程式效能监控 (APM) 代理程式或同时为两个平台提供服务。 AppDynamics Cloud 支援 AWS 云端原生託管 Kubernetes配置,并计划扩展到 Microsoft Azure、Google Cloud Platform 和其他云端供应商。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 评估 COVID-19 对产业的影响

- 产业价值链分析

第五章市场动态

- 市场驱动因素

- 扩大最终用户对云端的采用

- 有效管理云端平台效能和安全性的需求日益增长

- 市场挑战

- 可见度有限且成本高

第六章市场区隔

- 按型号

- IaaS

- SaaS

- PaaS

- 按最终用户产业

- BFSI

- 零售

- 资讯科技/通讯

- 卫生保健

- 政府机关

- 製造业

- 其他最终用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 新加坡

- 澳洲

- 其他亚太地区

- 拉丁美洲

- 墨西哥

- 巴西

- 其他拉丁美洲

- 中东/非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 其他中东和非洲

- 北美洲

第七章 竞争形势

- 公司简介

- AWS

- Broadcom Inc.(CA Technologies)

- IDERA Inc.

- LogicMonitor Inc.

- Oracle Corporation

- Microsoft Corporation

- IBM Corporation

- Datadog Inc.

- Zenoss Inc.

第八章 市场机会及未来趋势

第九章投资分析

The Cloud Monitoring Market size is estimated at USD 3.13 billion in 2024, and is expected to reach USD 7.76 billion by 2029, growing at a CAGR of 19.91% during the forecast period (2024-2029).

Key Highlights

- The cloud monitoring market refers to the industry that provides tools, solutions, and services for monitoring and managing cloud-based infrastructure, applications, and services. Cloud monitoring involves collecting, analyzing, and visualizing data related to the performance, availability, and security of cloud resources.

- Cloud monitoring solutions help organizations ensure the smooth functioning of their cloud environments, detect and address performance issues, optimize resource utilization, and ensure compliance with service-level agreements. These solutions typically offer features such as real-time monitoring, performance analytics, alerting, log analysis, security monitoring, and capacity planning.

- End-user industries are incorporating the cloud for scale and agility. However, gaining a clear view of performance in cloud environments can be challenging. To intelligently manage complex, ever-changing applications and infrastructure, a monitoring solution is needed that's as dynamic as the cloud.

- Moreover, the growing adoption of cloud technology across industries such as banking, financial services, and insurance (BFSI), information technology (IT), retail, and other industries is driving the growth of the cloud monitoring market. Cloud monitoring is a crucial component of an overall cloud management strategy, enabling IT administrators to review the operational status of cloud-based resources.

- The growing deployment of software-as-a-service (SaaS) offerings such as customer relationship management, human capital management, enterprise resource management, and other financial applications form a favorable environment for adopting cloud monitoring, especially in large organizations.

- Cloud environments, especially those with complex architectures, distributed systems, and multi-cloud or hybrid cloud setups, can pose difficulties in achieving comprehensive visibility. Organizations may struggle to monitor and manage their cloud resources effectively, resulting in reduced operational efficiency, increased risk of performance issues, and potential downtime. Limited visibility can arise from factors such as the lack of standardized monitoring interfaces across different cloud platforms, inadequate monitoring tools, and difficulties correlating data from disparate sources.

- The COVID-19 pandemic accelerated the adoption of cloud technologies as organizations rapidly transitioned to remote work setups. Cloud platforms became essential for ensuring business continuity and enabling remote collaboration. This increased reliance on the cloud created a greater need for cloud monitoring solutions to ensure cloud environments' performance, availability, and security. Post-pandemic also, the market is growing rapidly with the growth in cloud adoption across various end users.

Cloud Monitoring Market Trends

Growth in Cloud Adoption Across End Users is Expected to Drive the Market Growth

- The growth in cloud adoption across end users has been a significant driver for the cloud monitoring market. Effective monitoring and managing cloud environments become crucial as more organizations migrate their infrastructure, applications, and data to the cloud.

- Cloud monitoring involves collecting, analyzing, and visualizing data regarding the performance, availability, and security of cloud resources and services. It helps organizations ensure the optimal functioning of their cloud infrastructure, identify and address performance issues, and ensure compliance with service-level agreements.

- Cloud environments offer the ability to scale resources up or down based on demand. However, this dynamic nature makes monitoring and managing resources challenging. Cloud monitoring tools provide real-time visibility into resource utilization, ensuring optimal scalability and cost efficiency.

- Organizations are increasingly moving their IT infrastructure from on-premises to cloud environments such as Amazon Web Services (AWS), Microsoft Azure, Oracle, Alibaba, IBM Cloud, Google Cloud Platform, and others. During this migration, monitoring solutions are essential for tracking the performance of applications and infrastructure components in the cloud. According to Flexera Software, in 2023, 47 percent of respondents are already running significant workloads on Amazon Web Services (AWS).

- Cloud-based applications often have complex architectures with various components, microservices, and dependencies. Monitoring these distributed environments requires specialized tools to track performance across different services and provide insights into system interactions and dependencies.

Asia-Pacific Expected to be the Fastest Growing Region

- The Asia-Pacific (APAC) region has been witnessing significant growth in the cloud monitoring market. The increasing adoption of cloud technologies, digital transformation initiatives, and the proliferation of data centers in the region have contributed to the expansion of the cloud monitoring market in APAC.

- APAC countries such as China, Japan, Singapore, and Australia have experienced a surge in cloud adoption. Organizations in various sectors, including banking, healthcare, manufacturing, and retail, are migrating their infrastructure and applications to the cloud. This widespread adoption has increased the demand for cloud monitoring solutions to ensure cloud environments' performance, availability, and security.

- APAC countries actively pursue digital transformation initiatives to enhance business operations, improve customer experiences, and drive innovation. Cloud technologies play a vital role in enabling digital transformation, and monitoring these cloud environments is crucial to ensure seamless operations and optimal utilization of resources.

- According to the China Academy of Information and Communications Technology (CAICT), China's cloud computing business increased by 56.6% in 2022 to CNY 209.1 billion (USD 32.9 billion). The market is expected to expand quickly in the next three years, surpassing CNY 400 billion by 2023.

- APAC has seen significant investments in data centers driven by the growing demand for cloud services and the increasing volume of data generated by businesses. Cloud monitoring solutions are essential for managing and monitoring the performance of these data centers, ensuring efficient operations and high availability of services.

Cloud Monitoring Industry Overview

The cloud monitoring market is moderately fragmented, with the presence of major players like AWS, Broadcom Inc. (CA Technologies), IDERA Inc., LogicMonitor Inc., and Oracle Corporation. Players in the market are adopting strategies such as partnerships, innovations, and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

In April 2023, Amazon Web Services (AWS) launched the AWS Cloud Operations Competency. AWS Cloud Operations covers five fundamental solution areas: cloud financial management, cloud governance, cloud monitoring and observability, cloud compliance and auditing, and cloud operations management. Due to the new competence, customers can select verified AWS partners that provide comprehensive solutions with an integrated approach across several domains.

In June 2022, Cisco released AppDynamics Cloud, a cloud-native observability platform for modern applications built on increasingly complex, distributed architectures and services. It is designed for simplicity, usefulness, and intuitiveness, and it enables IT teams to create the excellent digital experiences that organizations, customers, and end users currently demand. Current AppDynamics customers may upgrade to AppDynamics Cloud and continue to use their existing application performance monitoring (APM) agents or feed both platforms concurrently. AppDynamics Cloud supports AWS cloud-native, managed Kubernetes deployments, with a planned extension to Microsoft Azure, Google Cloud Platform, and other cloud providers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Industry

- 4.4 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth in Cloud Adoption Across End Users

- 5.1.2 Rising Need for Efficiently Managing the Performance and Security of Cloud Platforms

- 5.2 Market Challenges

- 5.2.1 Limited Visibility and High Costs

6 MARKET SEGMENTATION

- 6.1 By Model

- 6.1.1 IaaS

- 6.1.2 SaaS

- 6.1.3 PaaS

- 6.2 By End-User Industry

- 6.2.1 BFSI

- 6.2.2 Retail

- 6.2.3 IT and Telecommunications

- 6.2.4 Healthcare

- 6.2.5 Government

- 6.2.6 Manufacturing

- 6.2.7 Other End-User Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Spain

- 6.3.2.5 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 Singapore

- 6.3.3.4 Australia

- 6.3.3.5 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.4.1 Mexico

- 6.3.4.2 Brazil

- 6.3.4.3 Rest of Latin America

- 6.3.5 Middle East and Africa

- 6.3.5.1 United Arab Emirates

- 6.3.5.2 Saudi Arabia

- 6.3.5.3 Rest of Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 AWS

- 7.1.2 Broadcom Inc. (CA Technologies)

- 7.1.3 IDERA Inc.

- 7.1.4 LogicMonitor Inc.

- 7.1.5 Oracle Corporation

- 7.1.6 Microsoft Corporation

- 7.1.7 IBM Corporation

- 7.1.8 Datadog Inc.

- 7.1.9 Zenoss Inc.

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 INVESTMENT ANALYSIS

2024 年云端监控世界市场报告

2024 年云端监控世界市场报告 全球云端监控市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势和预测

全球云端监控市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势和预测 云端监控市场规模、份额和趋势分析报告:2023-2030 年按类型、服务模式、公司规模、行业、地区和细分市场进行的预测

云端监控市场规模、份额和趋势分析报告:2023-2030 年按类型、服务模式、公司规模、行业、地区和细分市场进行的预测 云端监控市场报告:2030 年趋势、预测与竞争分析

云端监控市场报告:2030 年趋势、预测与竞争分析 云监控市场:按组件、服务模式和应用划分 - COVID-19、俄罗斯-乌克兰衝突和高通胀的累积影响 - 2023-2030 年全球预测

云监控市场:按组件、服务模式和应用划分 - COVID-19、俄罗斯-乌克兰衝突和高通胀的累积影响 - 2023-2030 年全球预测 到 2028 年的云监控市场预测-按服务模型、组件、组织规模、类型、云架构、最终用户和地区进行的全球分析

到 2028 年的云监控市场预测-按服务模型、组件、组织规模、类型、云架构、最终用户和地区进行的全球分析