|

市场调查报告书

商品编码

1433520

物联网晶片:全球市场占有率分析、产业趋势与统计、成长预测(2024-2029)Global IoT Chip - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

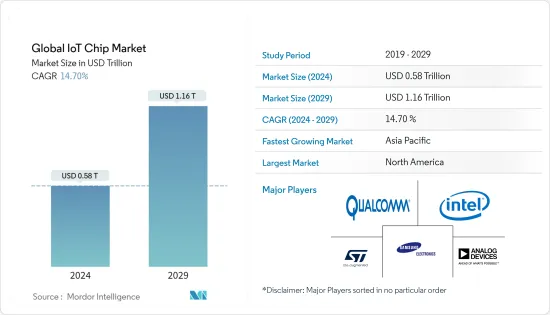

预计2024年全球物联网晶片市场规模将达到5,800亿美元,预计2029年将达到1.16兆美元,在预测期(2024-2029年)将成长14.70%,预计将以复合年增长率成长。

疫情期间,需求侧和供给侧因素减缓了部分产业物联网连结数的成长。随着公司倒闭或削减支出,一些物联网合约被取消或推迟。医疗保健、消费性电子、工业、汽车、BFSI 和零售等各个最终用户领域对自动化的需求不断增长,物联网设备的应用不断扩大,进一步推动了物联网设备的采用。

主要亮点

- 这一成长主要归因于不同通讯协定,这显着推动了跨多个最终用户行业的物联网晶片市场的成长。

- 2022 年 3 月,在麻省理工学院 (MIT) 工作的两位印度研究人员开发了一款低功耗安全晶片,旨在防止物联网 (IoT) 装置上的旁道攻击 (SCA)。 SCA 利用漏洞允许从系统硬体行为的间接影响中收集信息,而不是直接攻击程式或软体。

- 随着物联网设备数量的快速增加,建构这些物联网设备的晶片需求预计也会在预测期内增加。这使得降低消费量和晶片小型化成为製造商的首要任务。

- 5G 的日益普及将为物联网 (IoT) 设备提供快速且有效率的连接。预计对 5G 技术部署的投资将在预测期内及以后推动市场成长。 5G技术的整合被认为是下一代行动互联网连接,预计将提供比当前技术更快、更可靠的连接。因此,快速成长的物联网领域和配套晶片製造商预计将在预测期内增加对物联网晶片的需求。

- 软体漏洞和网路攻击等日益严重的安全问题可能会阻止许多客户使用物联网设备。物联网中的这些安全问题对于医疗保健、金融、製造、物流、零售和其他已经开始实施物联网系统的行业的组织来说尤其重要。

- COVID-19大流行导致全球供应链严重短缺,对市场产生了重大影响。此外,世界各国政府对人员流动的限制也影响了生产。然而,随着世界从大流行中恢復,对更自动化和复杂流程的需求已成为成功的关键方面。因此,未来更多物联网设备的市场预计将扩大,将对全球物联网晶片产生强劲需求。

物联网晶片市场趋势

工业部门预计将显着成长

- 工业4.0和物联网已成为开发、生产和物流链的主流新技术手段。由于机器对机器连接性、嵌入式感测器的增加以及车间和现场对工厂效率日益增长的需求,工业 4.0 的日益普及使製造业对物联网的需求保持在顶峰。

- 根据《经济时报》的一项研究,2022 年 7 月印度蜂巢式物联网模组和晶片组的出货有所增加,其中高通以 42% 的份额领先市场。该公司正在扩大其物联网晶片组产品组合,瞄准零售、工业和智慧城市等行业的优质 4G 和 5G 解决方案。

- 大多数製造商正在部署物联网设备,以利用预测性维护和进阶资料分析。这可以提高生产力和可用性,从而增加您的业务产品的价值。例如,GE 正在透过工业分析探索物联网机会。此外,Apotex 还升级了其製造流程,以实现手动流程自动化。这包括实施 RFID、分类和流程跟踪,以确保批量生产的一致性。这使公司能够即时了解其製造业务。

- 此外,工业物联网趋势是由美国智慧製造领导联盟 (SMLC) 等智慧工厂倡议推动的。由于需要收集、处理大量机器和感测器资料并形成决策,这将促进和促进製造智慧的广泛采用。

- 2022年6月,外交部宣布欧洲物联网(IoT)解决方案市场正在加速发展。德国、英国和荷兰在物联网采用方面领先欧洲,其次是东欧和北欧国家。製造业、家庭、医疗保健和金融业处于他采用物联网的最前沿,但零售和农业也出现了令人印象深刻的成长。这些多个领域的进步将利用整个欧洲的物联网晶片市场。

- 将eLTE、NB-IoT晶片等无线晶片引入製造终端多年来一直备受关注。例如,华为与产业合作伙伴合作生产用于传统製造的智慧终端,用于上传设备资料和接收命令。透过在製造终端上添加eLTE或NB-IoT晶片,并将终端产生的资料透过eLTE或NB-IoT网路传输,可以撷取製造资料并下发指令。

亚太地区预计将出现显着成长

- 亚太地区占物联网支出的最大份额,其中新加坡和韩国是采用物联网晶片的主要市场。根据经济合作暨发展组织,韩国是第一个每个栖息地网路连线数量最多的重要市场。

- 2022 年 7 月,铠侠株式会社和西部数据公司宣布,其位于四日市工厂的合资企业 Fab7 製造工厂获得日本政府批准最多 929 亿日圆的核准。这笔赠款是政府特别计画的一部分,旨在鼓励企业投资尖端半导体製造设施并确保日本半导体生产的稳定性。该地区的此类合作可能有助于物联网晶片市场的成长。

- 随着智慧城市对物联网晶片和 IC 的需求不断增长,以及连网型车辆和智慧交通系统等领域对家庭自动化的需求不断增长,物联网基础设施有潜力推动自动化和交通进入新阶段,其中包括对更好的无线技术的需求连接解决方案。

- 此外,亚洲各国政府正将物联网深度融入长期发展计划中。例如,中国中央政府已选择200多个城市试办智慧城市计划。城市包括北京、上海、广州和杭州。此外,印度将 100 个城市转变为智慧城市的愿景预计将透过智慧家庭和汽车产业推广电子产品。

- 2022 年 5 月,Cyient 与印度海得拉巴理工学院 (IITH) 以及 IITH 内成立的新兴企业WiSig Networks 合作,推出印度首款设计和工程晶片 Koala NB-IoT SoC(窄频SoC)。释出。双方签署的谅解备忘录(MOU)建立了充满活力的半导体设计和创新生态系统,服务全球,进一步促进印度发展成为全球电子製造和设计中心。技术、印度)目标打造

- 由于製造业等行业越来越多地使用连网型设备,预计该地区将成为物联网支出的主要提供者。 5G 的日益普及将增加物联网服务并推动未来几年的市场成长。

物联网晶片产业概况

全球物联网 (IoT) 晶片市场竞争适中,存在大量区域参与者。两家公司都利用策略联合倡议和收购来增加市场占有率和盈利。

- 2021 年 6 月 - RAIN RFID 供应商和网路业者Impinj Inc. 协助物联网设备製造商满足零售、供应链、物流和消费性电子产品等市场对连网产品不断增长的需求。宣布推出三款新的RAIN RFID读取器晶片。

- 2021 年 6 月 - 高通推出七款全新物联网晶片组,针对物流、仓储、智慧相机、视讯协作和零售等应用。该公司还表示,这些新的物联网解决方案为智慧设备提供了广泛的连接解决方案和关键功能,提供长寿命的硬体和软体选项,并提供至少八年的长期支援。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 技术简介

- 评估 COVID-19 对产业的影响

第五章市场动态

- 市场驱动因素

- 对连网型设备和穿戴式装置的需求增加

- 工业 4.0 趋势不断发展,采用尖端技术

- 市场限制因素

- 资料安全和隐私问题阻碍了物联网设备的普及

- 不同平台之间的通讯协定缺乏标准化

第六章市场区隔

- 副产品

- 处理器

- 感应器

- 连线IC

- 储存装置

- 逻辑元件

- 其他产品

- 按最终用户

- 卫生保健

- 消费性电子产品

- 工业的

- 车

- BFSI

- 零售

- 楼宇自动化

- 其他最终用户

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第七章 竞争形势

- 公司简介

- Qualcomm Technologies Inc.

- Intel Corporation

- Texas Instruments Incorporated

- NXP Semiconductors NV

- Cypress Semiconductor Corporation

- Mediatek Inc.

- Microchip Technology Inc.

- Samsung Electronics Co. Ltd

- Silicon Laboratories Inc.

- Invensense Inc.

- STMicroelectronics NV

- Nordic Semiconductor ASA

- Analog Devices Inc.

第八章投资分析

第9章市场的未来

The Global IoT Chip Market size is estimated at USD 0.58 trillion in 2024, and is expected to reach USD 1.16 trillion by 2029, growing at a CAGR of 14.70% during the forecast period (2024-2029).

Due to demand-side and supply-side factors, the growth in the number of IoT connections slowed down in specific sectors during the pandemic. Some IoT contracts were canceled or postponed due to firms going out of business or scaling back their spending. The rising demand for automation and the growing application of IoT devices across various end-user verticals, such as healthcare, consumer electronics, industrial, automotive, BFSI, and retail, are further driving the adoption of IoT devices.

Key Highlights

- The growth is primarily attributed to the integration of connectivity competence in a wide range of devices and applications, coupled with the development of different networking protocols that have appreciably driven the growth of the IoT chip market across multiple end-user industries.

- In March 2022, two Indian researchers working at the Massachusetts Institute of Technology (MIT) built a low-power security chip designed to prevent side-channel attacks (SCA) against Internet of Things (IoT) devices. SCA uses vulnerabilities to allow information gleaned from the indirect effects of the behavior of system hardware rather than directly attacking programs and software.

- With the rapid increase in the number of IoT devices, the chip requirement for building these IoT devices is also expected to rise over the forecast period. Along with this, reducing energy consumption combined with the miniaturization of chips will be the priority of manufacturers.

- The increased deployment of 5G provides quick and efficient connectivity for Internet-of-Things (IoT) devices. Investments in the deployment of 5G technology are expected to drive market growth during the forecast period and beyond. The integration of 5G technology is seen as the next generation of mobile internet connectivity and is expected to offer faster and more reliable connections than current technologies. Thus, the booming IoT space and the supporting chip makers are expected to increase demand for IoT chips during the forecast period.

- Rising security concerns, such as software vulnerabilities and cyberattacks, may discourage many customers from using IoT devices. Such security concerns in the Internet of Things are particularly essential to organizations in healthcare, finance, manufacturing, logistics, retail, and other industries that have already started adopting IoT systems.

- With the COVID-19 outbreak worldwide, the market was significantly affected as severe supply chain shortages occurred across the globe. Moreover, the restriction imposed by governments across the globe on the movement of people also impacted production. However, as the world recovers from the pandemic, the need for more automated and advanced processes has become a key aspect of success. As such, the market for more IoT-enabled devices is anticipated to rise in the future, thereby creating strong demand for IoT chips across the globe.

IoT Chip Market Trends

Industrial Segment is Expected to Witness Significant Growth

- Industry 4.0 and the IoT have become mainstream for new technological approaches in development, production, and logistics chains. The growing adoption of industrial 4.0 has kept IoT demand in manufacturing at maximum through increasing machine-to-machine connections and embedded sensors and the increasing need for factory efficiency on the floor and on the field.

- In July 2022, according to Economic Times's survey, cellular IoT module chipset shipments grew in India, and Qualcomm led the market with a 42% share. The company has been broadening its IoT chipset portfolio, targeting premium 4G and 5G solutions for verticals such as retail, industrial, smart cities, and more.

- Most manufacturers implement IoT devices to leverage predictive maintenance and sophisticated data analytics. This improves productivity and availability and adds value to their business offerings. For instance, GE is looking for opportunities in the IoT with industrial analytics. In addition, Apotex upgraded its manufacturing processes to automate manual processes. This includes ensuring consistent batch production by introducing RFID, sorting, and process flow tracking. Due to this, the company had real-time visibility into manufacturing operations.

- Furthermore, the industrial IoT trend is aided by smart factory initiatives, such as the Smart Manufacturing Leadership Coalition (SMLC) in the United States. This drives and facilitates the broad adoption of manufacturing intelligence due to massive amounts of machine and sensor data that need collection, processing, and formation of decisions.

- In June 2022, the Ministry of Foreign Affairs stated that the European market for Internet of Things (IoT) solutions is accelerating. Germany, the UK, and the Netherlands lead Europe in IoT adoption, while Eastern European and Nordic countries follow closely. The manufacturing, home, healthcare, and financial sectors are at the forefront of his IoT adoption, but retail and agriculture are also seeing impressive growth. Such advancement in multiple sectors will leverage the IoT chip market across Europe.

- The deployment of the wireless chip, including eLTE or NB-IoT chip for their manufacturing terminal, has been gaining traction over the years. For instance, Huawei collaborated with industrial partners to make smart terminals used in traditional manufacturing for uploading equipment data and receiving commands. eLTE or NB-IoT chip is added to the manufacturing terminal for transmitting data generated by the terminal via the eLTE or NB-IoT network, enabling manufacturing data to be collected and commands issued.

Asia Pacific is Expected to Witness Significant Growth

- Asia-Pacific accounts for a significant share of spending in IoT, with Singapore and South Korea as major markets adopting IoT chips. According to the Organization for Economic Co-operation and Development, South Korea is the first prominent market to connect more to the internet per habitat.

- In July 2022, KIOXIA Corporation and Western Digital Corporation announced their joint venture Fab7 manufacturing facility at Yokkaichi Plant had received approval from the Japanese government for a subsidy of up to JPY 92.9 billion. The subsidy is granted under a special government program to promote corporate investment in state-of-the-art semiconductor manufacturing facilities and ensure the stable production of semiconductors in Japan. Such collaborations in the region will help the IoT chip market to grow.

- IoT's infrastructure includes the demand for better wireless connectivity solutions to enable new phases in automation and transportation owing to the rise in demand for IoT chips and ICs in smart cities and domestic automation in the areas such as connected automobiles and smart transportation systems.

- Further, Asian governments are deeply integrating IoT in their long-term development projects. For instance, China's central government selected over 200 cities to pilot smart city projects. The cities include Beijing, Shanghai, Guangzhou, and Hangzhou. Furthermore, India's vision to transform 100 cities into smart cities is expected to promote electronics through smart homes and the automotive sector.

- In May 2022, Cyient partnered with IIT Hyderabad, India (IITH) and WiSig Networks, a start-up company founded in IITH, to launch India's first designed and engineered chip, Koala NB-IoT SoC (Narrowband IoT SoC). The Memorandum of Understanding (MOU) signed between the two aligns with the goals of MEITY (Ministry of Electronics and Information Technology, India) to build a vibrant semiconductor design and innovation ecosystem to serve the Indian world and further promote its development into a global electronics manufacturing and design hub.

- The region is expected to be a prominent provider of IoT spending as there is increased use of connected devices in sectors such as manufacturing. Increased adoption of 5G is helping the market grow in the upcoming years as there is an increase in IoT services.

IoT Chip Industry Overview

The Global Internet of Things (IoT) Chip Market is moderately competitive, with a considerable number of regional players. The companies are leveraging strategic collaborative initiatives and acquisitions to increase market share and profitability.

- June 2021 - Impinj Inc., which is a RAIN RFID provider and Internet of Things provider, announced the introduction of three new RAIN RFID reader chips that enable IoT device manufacturers to meet the increasing demand for item connectivity in applications such as retail, supply chain and logistics, and consumer electronics, among other markets.

- June 2021 - Qualcomm launched seven of its new IoT chipsets that were targeted at devices meant for logistics, warehousing, smart cameras, video collaboration, and retail, among other applications. The company also stated that these new IoT solutions offer significant capabilities for a wide range of connected solutions and smart devices with extended life hardware and software options to achieve long-term support for a minimum of eight years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Technology Snapshot

- 4.4 Assessment of COVID-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand of Connected and Wearable Devices

- 5.1.2 Adoption of Advance Technologies Due to Rising Trend of Industry 4.0

- 5.2 Market Restraints

- 5.2.1 Issues Related to Security and Privacy of Data to Hinder the Adoption of IoT Devices

- 5.2.2 Lack of Standardization of Communication Protocol across Different Platforms

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Processor

- 6.1.2 Sensor

- 6.1.3 Connectivity IC

- 6.1.4 Memory Device

- 6.1.5 Logic Device

- 6.1.6 Other Products

- 6.2 By End-user

- 6.2.1 Healthcare

- 6.2.2 Consumer Electronics

- 6.2.3 Industrial

- 6.2.4 Automotive

- 6.2.5 BFSI

- 6.2.6 Retail

- 6.2.7 Building Automation

- 6.2.8 Other End-users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Qualcomm Technologies Inc.

- 7.1.2 Intel Corporation

- 7.1.3 Texas Instruments Incorporated

- 7.1.4 NXP Semiconductors NV

- 7.1.5 Cypress Semiconductor Corporation

- 7.1.6 Mediatek Inc.

- 7.1.7 Microchip Technology Inc.

- 7.1.8 Samsung Electronics Co. Ltd

- 7.1.9 Silicon Laboratories Inc.

- 7.1.10 Invensense Inc.

- 7.1.11 STMicroelectronics NV

- 7.1.12 Nordic Semiconductor ASA

- 7.1.13 Analog Devices Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

物联网晶片市场:2025 年至 2030 年预测

物联网晶片市场:2025 年至 2030 年预测 2025年窄频物联网晶片组全球市场报告

2025年窄频物联网晶片组全球市场报告 物联网晶片市场规模、份额及成长分析(按硬体、功耗、最终用途和地区)—产业预测,2025 年至 2032 年交通运输物联网晶片市场:2025-2030 年预测政府物联网晶片市场 - 2025-2030 年预测

物联网晶片市场规模、份额及成长分析(按硬体、功耗、最终用途和地区)—产业预测,2025 年至 2032 年交通运输物联网晶片市场:2025-2030 年预测政府物联网晶片市场 - 2025-2030 年预测 全球物联网 (IoT) 晶片市场 (2024-2028)

全球物联网 (IoT) 晶片市场 (2024-2028) 物联网晶片市场:按产品、最终用途划分 - 2025-2030 年全球预测物联网晶片市场:按硬体、功耗、应用划分 - 2025-2030 年全球预测

物联网晶片市场:按产品、最终用途划分 - 2025-2030 年全球预测物联网晶片市场:按硬体、功耗、应用划分 - 2025-2030 年全球预测 物联网晶片市场 - 按产品、最终用户、地区和竞争细分的全球产业规模、份额、趋势、机会和预测,2019-2029 年

物联网晶片市场 - 按产品、最终用户、地区和竞争细分的全球产业规模、份额、趋势、机会和预测,2019-2029 年 2030 年物联网晶片市场预测:按类型、形式、连接技术、应用、最终用户和地区进行的全球分析

2030 年物联网晶片市场预测:按类型、形式、连接技术、应用、最终用户和地区进行的全球分析