|

市场调查报告书

商品编码

1433782

智慧卡:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Smart Card - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

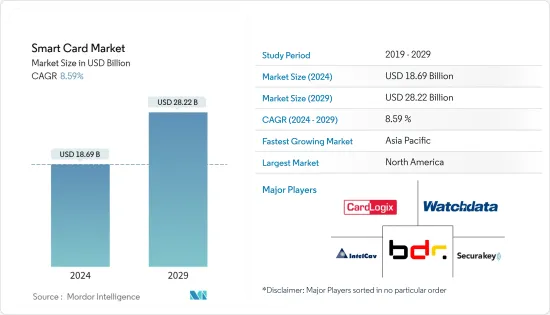

全球智慧卡市场规模预计将在 2024 年达到 186.9 亿美元,并在 2024-2029 年预测期内以 8.59% 的复合年增长率增长,到 2029 年将达到 282.2 亿美元。

数位化程度的提高、网路购物需求的增加、医疗保健需求、存取控制应用等是推动智慧卡市场成长的主要因素。

主要亮点

- 智慧卡提供了一种安全的方式来识别和验证持卡人以及希望存取该卡的第三方。例如,持卡人可以使用 PIN 码或生物识别资料进行身份验证。智慧卡还提供了一种在卡上安全储存资料并透过加密保护通讯安全的方法。

- 随着最近针对高级智慧卡安全应用的其他安全和隐私问题的引入,多年来对智慧卡在各种终端行业市场中的使用的需求不断增加。在全球范围内,银行和金融业预计将占据智慧卡市场的很大份额。由于关键的金融业务是该行业的核心,因此安全性仍然是首要关注点。这推动了先进身份验证解决方案的采用,并加速了智慧卡在行业中的接受度。

- 用于存取控制和其他应用的智慧卡需要很高的初始成本,因为它们使用高品质的读卡机和晶片来实现其功能。部署读卡机和晶片需要额外的成本,这增加了智慧卡的整体成本并限制了智慧卡的成长。

- 疫情期间,专注于通讯和医疗保健的智慧卡业务受到的影响小于其他行业。医疗保健资料的激增给提供高效的患者照护和隐私带来了新的挑战。智慧卡透过提供安全储存(磁条卡上可以储存超过 150 个位元组)和轻鬆的资料分发来解决这两个挑战。医疗保健支出的增加预计将推动智慧卡在医疗保健市场的使用。

- 例如,根据 Medicare & Medicaid Services 的数据,到 2027 年,美国医疗保健支出预计将达到约 6 兆美元。此外,COVID-19 的出现促使多个国家製定疫苗接种预防计划,预计这也将促进市场成长。数位凭证预计将在管理这场流行病方面发挥重要作用。

智慧卡市场趋势

BFSI 引领市场

- 在 BFSI 行业中使用智慧卡有很多好处,包括安全资料传输和个人资讯安全。智慧卡还在银行、金融服务和保险 (BFSI) 行业中用作付款授权卡、存取控制卡以及信用卡和签帐金融卡。智慧卡可以用作电子钱包,储存的钱可以使用加密通讯协定转移到自动贩卖机或帐户。

- 银行业早已认识到磁条卡技术的优势,并已转向记忆体晶片或卡上微处理器技术。然而,在过去十年中,由于诈欺的增加,对安全付款的智慧卡的需求增加。

- 新银行的扩张和数位金融科技领域对全球研究市场产生了直接影响。印度是采用无现金交易的开发中国家的一个例子。政府机构正在协助推广卡片和其他无现金付款方式的使用,刺激智慧卡补充品市场。

- 金融机构对智慧卡技术的使用和各种合作协议进一步支持了市场扩张。例如,ICICI银行去年与Greater Chennai Corporation和Chennai Smart City Limited合作推出了“Namma Chennai智慧卡”,旨在为Chennai人们提供各种支付的统一解决方案。

亚太地区将经历最高的成长

- 随着智慧卡在亚太地区的使用越来越广泛,来自 BFSI、医疗保健、零售和政府部门的需求可能会主导市场。

- 由于中国拥有庞大的消费群以及主要智慧卡製造商的存在,该地区对智慧卡的需求预计将强劲。智能卡已被许多银行机构采用,有助于市场扩张。

- 例如,中国建设银行(CCB)去年宣布正在测试生物识别「硬钱包」智慧卡,该卡允许用户储存数位人民币并使用央行数位货币进行支付。现在可以透过指纹进行确认。借助最先进的指纹认证和识别技术,储存在卡片上的价值得到进一步保护。

- 该地区的几家银行已与 IC 卡生产公司合作,在该国建立各种类型的 IC 卡。 Axis银行、ICICI银行和SBM银行是去年下半年或第一季发行IC卡的印度银行。

- 此外,东京电子公司 MoriX Co. 去年与 Fingerprint Cards AB 合作,使用 Fingerprints 的 T 型模组开发并推出了生物识别付款卡。这些卡预计将使用传统的自动化製造技术与付款卡整合。

- 为了支持市场扩张,新的倡议和开拓正在鼓励其他最终用户使用智慧卡。香港智慧卡营运商之一八达通最近为中国300多个城市的大众交通工具用户推出了交通卡。作为该公司海外发展计画的一部分,八达通交通卡用户将能够在当地支付公车、火车和渡轮等大众交通工具。八达通卡的储值限额最初为 3,000港币(386 美元),第二阶段将迁移至数位八达通卡。

智慧卡产业概况

由于有多家跨国公司,智慧卡市场呈现碎片化状态。主要参与者包括 HID Global Corporation、CardLogix Corporation 和 Thales Group。该市场的主要企业正在推出创新的新产品并建立合作伙伴关係和联盟,以获得竞争优势。

2023 年 1 月,东南亚领先的安全智慧卡解决方案和数位安全供应商 dzcard 开设了一个新的研发中心,致力于下一代卡技术,重点关注永续性。该实验室位于泰国曼谷,将作为与 dzcard 的客户和合作伙伴共同创造产品的平台。该实验室的重点是创建和评估永续性发展的解决方案和产品。我们致力于利用环保生产技术,运用永续资源,创造对环境影响较小的产品。他们的目标是开发智慧卡解决方案,不仅满足客户需求,而且迈向更永续的未来。

2023 年 4 月,印度为使用坎普尔地铁的乘客推出了 GoSmart 全国通用移动卡。 NCMC 卡最初在北方邦坎普尔地铁推出。这张卡的主要优点是它是一张可兑换的交通卡,这意味着它可以在全国其他符合 NCMC 标准的零售商店、停车场、地铁、巴士和其他交通服务中使用。旅客可以使用 NCMC 卡轻鬆游历全国。这样可以实现平稳运动并节省时间和精力。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

年表

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 产业价值链分析

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 扩大个人识别和存取控制应用的部署

- 广泛应用于旅游识别和交通

- 非接触式付款需求不断成长

- 市场限制因素

- 对隐私/安全问题和标准化的担忧

第六章市场区隔

- 按类型

- 接触底座

- 非接触式

- 按最终用户产业

- 资讯科技/通讯

- 政府

- 运输

- 其他最终用户产业(教育、医疗保健、娱乐等)

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 欧洲其他地区

- 亚太地区

- 中国

- 日本

- 印度

- 其他亚太地区

- 其他地区

- 北美洲

第七章 竞争形势

- 公司简介

- CardLogix Corporation

- Watchdata Technologies

- Bundesdruckerei GmbH

- IntelCav

- Secura Key

- Alioth LLC

- Gemalto NV(Thales Group)

- Giesecke & Devrient GmbH(MC Familiengesellschaft mbH)

- HID Global Corporation(Assa Abloy AB)

- IDEMIA France SAS

- Infineon Technologies AG

- Fingerprint Cards AB

- Samsung Electronics Co. Ltd

- CPI Card Group Inc.

- KONA I Co. Ltd

第八章供应商定位分析

第九章投资分析

第10章市场的未来

The Smart Card Market size is estimated at USD 18.69 billion in 2024, and is expected to reach USD 28.22 billion by 2029, growing at a CAGR of 8.59% during the forecast period (2024-2029).

The rising digitalization, increasing demand from online shopping, demand for healthcare, and access control applications are the primary factors augmenting the growth of the smart card market.

Key Highlights

- Smart cards provide methods to securely identify and authenticate the cardholder and third parties who want access to the card. For instance, a cardholder can use a PIN code or biometric data for authentication. Smart cards also provide a way to securely store data on the card and protect communications with encryption.

- The demand for smart cards has been growing each year with applications in various end-use industry markets due to the recent introduction of other security and privacy issues for advanced smart card security applications. Globally, the banking and finance industry is expected to account for a significant share of the smart card market. With critical financial operations being the industry's core, security remains the primary focus. This supports the adoption of advanced authentication solutions and promotes the acceptance of the smart card within the sector.

- The initial cost required for the smart card used for access control and other applications is high as it uses readers and chips of high quality for its functioning. The deployment of readers and chips requires additional costs, which increases the overall cost of smart cards, restraining the growth of smart cards.

- During the COVID-19 pandemic, the business for smart cards specific to telecommunications and healthcare was less affected than other verticals. The upsurge of healthcare data brings up new challenges in providing efficient patient care and privacy. Smart cards solved both challenges by providing secure storage (dramatically more than 150 bytes that can be stored on a magnetic stripe card) and easy data distribution. Increasing healthcare expenditure is anticipated to propel the use of smart cards in the healthcare market.

- For instance, according to the Centers for Medicare & Medicaid Services, US health spending is projected to reach nearly USD 6 trillion by 2027. Moreover, the emergence of COVID-19 has prompted several nations to develop vaccination-proofing plans, which are also anticipated to aid market growth. Digital credentials are expected to play a major role in managing the pandemic.

Smart Card Market Trends

BFSI is Expected to Drive Market

- Smart card use in the BFSI industry has many advantages, including secure data transfers and the security of private information. Smart cards are also used as payment authentication cards, access control cards, and credit or debit cards in the banking, financial services, and insurance (BFSI) industry. By loading the smart card with money that can be transferred using cryptographic protocols to a vending machine or an account, they can be used as electronic wallets.

- The banking sector has long recognized the advantages of magnetic stripe card technology and has transitioned to memory chip or microprocessor-on card technology. However, the necessity for smart cards for protected payments has grown over the past decade due to a rise in fraud rates.

- The expansion of neo-banks and the field of digital financial technology has had a direct impact on the market under study globally. India is one example of a developing nation that has embraced cashless transactions. Government agencies have supported them in promoting the use of cards and other cashless payment methods, fueling a supplementary market for smart cards.

- The market's expansion has been further aided by financial institutions' use of smart card technology and different collaboration agreements. For instance, ICICI Bank declared last year that it partnered with Greater Chennai Corporation and Chennai Smart City Limited to launch the Namma Chennai Smart Card, which aims to offer the people of Chenna, India, a uniform solution for a variety of payments.

Asia Pacific to Witness Highest Growth

- Since smart cards are more widely used in the Asia Pacific area, demand from the BFSI, healthcare, retail, and government sectors is likely to dominate the market.

- A big consumer base and the presence of major smart card manufacturers in China are expected to result in a strong demand for smart cards in the region. Smart cards were adopted by a number of banking institutions, which helped the market expand.

- For instance, China Construction Bank (CCB) declared last year that they are testing a biometric 'hard wallet' smart card that enables users to store digital yuan and confirm payments made using the central bank's digital currency with their fingerprints. With the help of cutting-edge fingerprint authentication and recognition, the stored value on the card is further protected.

- To establish various types of smart cards in the nation, several banks operating in the region have partnered with smart card creators. Axis Bank, ICICI Bank, and SBM Bank are a few Indian banks that released smart cards in the latter or first quarter of the previous year.

- In addition, MoriX Co., a Tokyo-based electronics company, collaborated with Fingerprint Cards AB last year to develop and introduce biometric payment cards using the T-Shape module from Fingerprints. These cards are anticipated to be integrated with payment cards using conventional automated manufacturing techniques.

- To support market expansion, new initiatives, and developments are encouraging other end users to use smart cards. Transit cards were recently offered for users of public transportation in more than 300 Chinese cities by Octopus, one of the smart card operators in Hong Kong. Users of Octopus transit cards will be able to pay for public transportation in mainland China's buses, trains, and ferries as part of the company's offshore development plan. The maximum top-up amount for the Octopus card will initially be HKD 3,000 (USD 386), with the option to convert to digital Octopus cards in a phase two launch.

Smart Card Industry Overview

The Smart Card Market is fragmented because of the presence of several global companies. Some of the key players are HID Global Corporation, CardLogix Corporation, Thales Group, etc. Key players in this market are introducing new innovative products and forming partnerships and collaborations to gain competitive advantages.

In January 2023, a new innovation center dedicated solely to next-generation card technologies with a dedication to sustainability was inaugurated by dzcard, the top secured smart card solution and digital security provider in Southeast Asia. The lab, which is situated in Bangkok, Thailand, will serve as a platform for the co-creation of goods with dzcard's clients and partners. The lab's focus is on creating and evaluating solutions and products that are sustainability-oriented. They are dedicated to utilizing environmentally friendly production techniques, employing sustainable resources, and creating items that have less of an impact on the environment. Their objective is to develop smart card solutions that not only satisfy client needs but also work toward a more sustainable future.

In April 2023, for passengers using the Kanpur metro in India, the GoSmart National Common Mobility Card was launched. The NCMC card was initially introduced in Uttar Pradesh by the Kanpur Metro. The primary advantage of this card is that it is an interchangeable transport card, meaning that it may be used for other NCMC-compliant retail, parking, metro, bus, and other transportation services throughout the nation. Travelers can easily traverse the entire nation with the NCMC card. Along with facilitating smooth mobility, this also helps travelers save time and energy.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Deployment in Personal Identification and Access Control Applications

- 5.1.2 Extensive Use in Travel Identity and Transportation

- 5.1.3 Growing Demand for Contactless Payments

- 5.2 Market Restraints

- 5.2.1 Privacy and Security Issues and Standardization concerns

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Contact-based

- 6.1.2 Contact-Less

- 6.2 By End-user Vertical

- 6.2.1 BFSI

- 6.2.2 IT & Telecommunication

- 6.2.3 Government

- 6.2.4 Transportation

- 6.2.5 Other End-User Industries (Education, Healthcare, Entertainment, etc.)

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 Rest of Asia-Pacific

- 6.3.4 Rest of the World

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 CardLogix Corporation

- 7.1.2 Watchdata Technologies

- 7.1.3 Bundesdruckerei GmbH

- 7.1.4 IntelCav

- 7.1.5 Secura Key

- 7.1.6 Alioth LLC

- 7.1.7 Gemalto NV (Thales Group)

- 7.1.8 Giesecke & Devrient GmbH (MC Familiengesellschaft mbH)

- 7.1.9 HID Global Corporation (Assa Abloy AB)

- 7.1.10 IDEMIA France SAS

- 7.1.11 Infineon Technologies AG

- 7.1.12 Fingerprint Cards AB

- 7.1.13 Samsung Electronics Co. Ltd

- 7.1.14 CPI Card Group Inc.

- 7.1.15 KONA I Co. Ltd

8 VENDOR POSITIONING ANALYSIS

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

2024-2032 年智慧卡 IC 市场报告(按类型、介面、架构类型、应用、最终用途产业和地区)

2024-2032 年智慧卡 IC 市场报告(按类型、介面、架构类型、应用、最终用途产业和地区) 2024-2032 年智慧卡市场报告(按类型、组件、应用、最终用户和地区划分)

2024-2032 年智慧卡市场报告(按类型、组件、应用、最终用户和地区划分) 交通智慧卡市场 - 全球产业规模、份额、趋势、机会和预测,按卡类型、最终用户、地区、竞争细分,2019-2029F

交通智慧卡市场 - 全球产业规模、份额、趋势、机会和预测,按卡类型、最终用户、地区、竞争细分,2019-2029F 中国的智慧卡市场

中国的智慧卡市场 2024 年交通卡市场报告(按产品(公车卡、地铁卡等)、类型(非接触式交通卡、接触式交通卡、组合/混合交通卡)、应用(交通、交通管理等)和区域-2032

2024 年交通卡市场报告(按产品(公车卡、地铁卡等)、类型(非接触式交通卡、接触式交通卡、组合/混合交通卡)、应用(交通、交通管理等)和区域-2032 2024-2028年全球智慧卡IC市场

2024-2028年全球智慧卡IC市场 智慧卡 MCU:市场占有率分析、产业趋势与统计、成长预测(2024-2029 年)

智慧卡 MCU:市场占有率分析、产业趋势与统计、成长预测(2024-2029 年) 用于非接触式票务的安全 IC 技术

用于非接触式票务的安全 IC 技术 用于非接触式票务的智慧卡技术

用于非接触式票务的智慧卡技术 2024年智能卡IC全球市场报告

2024年智能卡IC全球市场报告