|

市场调查报告书

商品编码

1433825

SLS(选择性雷射烧结):市场占有率分析、产业趋势与统计、成长预测(2024-2029)Selective Laser Sintering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

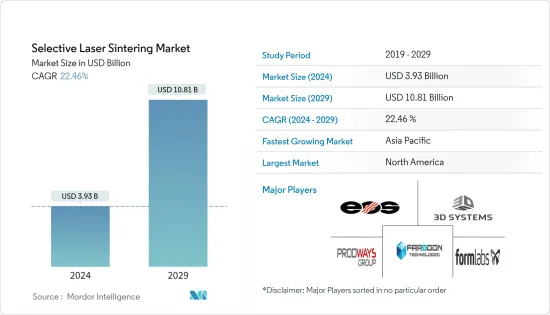

预计2024年SLS(选择性雷射烧结)市场规模为39.3亿美元,预计2029年将达到108.1亿美元,复合年增长率预计为22.46%。

SLS 是一种积层製造(AM) 技术,是一种将高功率雷射光束定向到粉末材料床(通常是尼龙或聚酰胺)以烧结所需物体各层的製程。此层完成后,物体上覆盖一层新的粉末,并烧结另一层。

主要亮点

- 由于已开发国家的研发设施的存在,预计 SLS 设备市场将受到需求不断增长的推动。雷射烧结印表机的日益普及是由于可以使用非金属粉末来创建原型模型和零件。雷射烧结印表机在列印金属零件时也是最准确的。

- 由于与用于列印应用的其他技术相比,SLS 具有多种优势,因此被认为是最受欢迎的技术之一,预计在预测期内将出现强劲增长。

- SLS以尼龙粉末作为原料,作为光固化成形法中所使用的光敏树脂的替代。世界各地的公司和研究机构已经确定使用这种材料和技术来解决树脂暴露在阳光下变得脆弱等问题。此外,SLS 也被证明具有成本和材料友善性,因为它在列印后不需要专用的支撑结构。此外,SLS 提高了耐用性,并且可以像功能部件和原型一样发挥作用。

- SLS 进一步在航太、国防和汽车等各个垂直领域中广泛应用。随着航太发展模式转移,越来越多的国家准备发射人造卫星,SLS列印的需求预计将增加。

- 各种航太公司正在采用这项技术来促进高效生产。例如,在航空航太领域,美国太空总署和私人公司正在致力于用更少的零件製造火箭发动机(在相对论性太空的情况下,是整个火箭)。这些零件是使用 SLS 以及金属粉末(例如耐高温的铬镍铁合金铜超合金粉末)的铺设和熔化逐层建造的。 SLS 技术有几个优点。例如,可以在短短几天内将多个零件列印为一个统一的零件,从而减少螺母、螺栓和焊接的数量,从而减轻火箭的重量。如果火箭在测试过程中出现故障,可以对 3D 建模软体进行更改以建立新火箭并快速设定另一次测试。

- 此外,2021 年 12 月,积层製造零件製造商 Primaeam Solutions Pvt Ltd 在印度清奈开设了一个新的积层製造客户经验中心—医疗保健创新与孵化中心。这个占地 10,000 平方英尺的中心提供电子束熔化 (EBM)、SLS (SLM)、熔融沉积建模(FDM)、光固化成形法(SLA)、多射流融合(MJF)、纤维增强连续丝製造(CFF)等服务。技术,我们将成为增材製造服务行业的杰出参与者。

- COVID-19 大流行对世界各地的中小企业和大型企业造成了经济混乱。这是因为製造业的很大一部分涉及工厂车间的工作,人们在工厂车间进行密切接触以提高生产率。

SLS市场趋势

航太和国防工业预计将占据主要市场占有率

- 航太是目前大多数技术的早期采用者。飞机和发动机製造商都依靠 3D 列印技术来开发轻量化零件以提高效率。

北美预计将占据主要市场占有率

- 北美是许多开发、采用和投资增材製造的公司的所在地。该地区对原型製作的需求不断增长,这是该地区市场的主要驱动力。此外,北美对 SLS 的需求受到各行业对研发和测试的日益关注的推动。

- 据加拿大统计局称,加拿大企业计划在2021年花费219亿美元用于内部工业研发,2022年花费224亿美元。这种研发成长预计将提振北美 SLS 市场。

- 该地区的公司正在组建策略联盟,为更广泛的客户群提供解决方案。例如,2022年5月,美国Essentium Inc与蓝色雷射解决方案供应商Nuburu合作开发基于蓝色雷射的金属增材製造平台。

- 因此,製造商有望能够製造出具有高分辨率和快速吞吐量的生产级金属零件。此外,作为协议的一部分,Nubl 将许可积层製造专利。

- 3D 列印等新技术的日益使用预计也将推动该地区的 SLS 市场。例如,根据世界经济论坛的数据,到2022年,美国接受调查的企业中有47%预计将使用3D列印技术。

SLS产业概述

SLS 市场主要由在全球营运的老牌公司和一些在整合市场空间中争夺注意力的区域参与者组成。包括 3D Systems Inc.、EOS GmbH Electro Optical Systems、Ricoh Company Ltd. 和 Fathom Manufacturing 在内的多家在该领域拥有丰富专业知识的参与者的加入,预计将进一步加剧竞争对手之间的竞争。

- 2022 年 6 月 - 3D Systems 和 EMS GRILTECH 宣布建立策略合作伙伴关係,以加强积层製造材料的开发。两家公司推出了 Durafoam PAx Natural,这是一种新型尼龙共聚物,设计用于商用 SLS 印表机。

- 2021 年 11 月 - 赢创工业股份公司宣布扩大其 RESOMER PrintPowder 聚合物生产线,可实现植入式医疗设备的 3D 列印。这种新型粉末可在全球范围内使用 SLS 方法进行 3D 列印。这种新型粉末具有广泛的可客製化机械性能和劣化率,使其可用于更复杂和客製化的医疗设备,包括各种整形外科、牙科和软组织应用。

- 2021 年 2 月 - 3D Systems 宣布在南卡罗来纳州罗克山扩建计划,在现有总部园区基础上增加 100,000 平方英尺。此次扩建将整合材料製造、品质和物流业务,并创建和扩大材料开发实验室,以提高业务效率、加速解决方案开发并缩短上市时间。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- COVID-19 市场影响评估

- 3D列印技术分析(FDM、SLA、SLS;材料与技术的定性分析;桌上型工业SLS和传统工业SLS列印机的比较)

第五章市场动态

- 市场驱动因素

- 缩短最终产品进入市场的时间

- 各地区政府措施的活性化

- 市场挑战

- 额外的资本投资和大规模生产的限制

第六章市场区隔

- 按材质

- 金属

- 塑胶

- 按成分

- 硬体

- 软体

- 服务

- 按最终用户产业

- 车

- 航太/国防

- 卫生保健

- 电子产品

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 世界其他地区

第七章 竞争形势

- 公司简介

- 3D Systems Inc.

- EOS GmbH Electro Optical Systems

- Farsoon Technologies

- Prodways Group

- Formlabs Inc.

- Ricoh Company Ltd

- Concept Laser GmbH(General Electric)

- Renishaw PLC

- Sinterit Sp. Zoo

- Sintratec AG

- Sharebot SRL

- Red Rock SLS

第八章投资分析

第9章市场的未来

The Selective Laser Sintering Market size is estimated at USD 3.93 billion in 2024, and is expected to reach USD 10.81 billion by 2029, growing at a CAGR of 22.46% during the forecast period (2024-2029).

Selective Laser Sintering (SLS), an additive manufacturing (AM) technique, is a process in which a high-powered laser beam is aimed into powdered material (typically nylon or polyamide) bed to sinter a layer of the desired object. Following the completion of that layer, the object is covered with a new layer of powder, and another layer is sintered.

Key Highlights

- The market for SLS equipment is anticipated to be driven by the rising demand from developed countries, owing to the presence of research and development facilities in the countries. The adoption of laser sintering printers has increased due to the ease of availability of non-metal powders to create prototype models and parts. Also, laser sintering printers are the most precise when printing metal parts.

- Selective Laser Sintering (SLS) has been identified as one of the most-preferred technology and is expected to witness robust growth during the forecast period, owing to its various benefits over other technologies used for printing applications.

- SLS utilizes nylon powder as raw material as a substitute for the photosensitive resin used in Stereolithography. Companies and research organizations across the globe have been identified to take advantage of this material and technology to tackle concerns, such as the brittle nature of the resin when exposed to sunlight. In addition, SLS has also been proven to be cost and material friendly, as it does not require any dedicated support structure post-printing. In addition, SLS provides enhanced durability and can perform as well as either functional parts or prototypes.

- SLS further finds a wide array of applications across various verticals, such as aerospace, defense, and automotive, among others. With space exploration witnessing a paradigm shift, the demand for SLS printing is expected to mount, with an increasing number of countries gearing up to launch satellites.

- Various aerospace companies are adopting the technology to foster efficient production. For instance, in the space flight branch of aerospace, NASA and private companies are working to build rocket engines (and even entire rockets in the case of Relativity Space) with fewer parts, which is a crucial capability of 3D printing and a way to reduce production time and costs. Using selective laser sintering and the laying down and melting of metal powder (for example, Inconel copper super alloy power that can withstand high temperatures), parts are built up layer by layer. The SLS technique offers several benefits, like multiple parts can be printed as one unified part in just days; the rocket's weight can be reduced with fewer nuts, bolts, and welds. If the rocket proves faulty during a test, changes can be made to the 3D modeling software for a new rocket, and another test can be quickly set up.

- Further, in December 2021, Primaeam Solutions Pvt Ltd, an additive parts manufacturing company, inaugurated its new Additive Manufacturing Customer Experience Centre, Innovation & Incubation Centre for Healthcare, in Chennai, India. The 10,000 sq. ft. center would allow the company to develop its position as a prominent player in the additive manufacturing service bureau with technologies such as Electron Beam Melting (EBM), Selective Laser Sintering (SLM), Fused Deposition Modelling (FDM), Stereolithography (SLA), Multi Jet Fusion (MJF), and Continuous Filament Fabrication with Fiber reinforcement (CFF).

- The COVID-19 pandemic outbreak has created economic turmoil for small, medium, and large-scale industries worldwide. Adding to the woes, country-wise lockdown inflicted by the governments across the globe (to minimize the spread of the virus) has further resulted in industries taking a hit and disruption in supply chain and manufacturing operations across the world, as a large part of manufacturing includes work on the factory floor, where people are in close contact as they collaborate to boost the productivity.

Selective Laser Sintering (SLS) Market Trends

Aerospace and Defense Industry is Expected to Hold Significant Market Share

- The aerospace industry has an early rate of adoption of most of the technologies in the current generation. Both aircraft and engine manufacturers have been relying on 3D printing technology in order to develop lightweight parts to gain efficiency.

- 3D printing has been used by the National Aeronautics and Space Administration (NASA) for decades for the purposes of prototyping and creating functional parts and, most recently, for building construction systems for the Moon and Mars.

- Bell Textron Inc. was one of the first aerospace companies to experiment with additive manufacturing. The first use of SLS was for quick prototypes of tooling and experimental parts. However, as the additive manufacturing industry progressed, the company understood the need to allow the additive manufacturing industry to mature. Since the start of additive efforts, Bell Textron has produced over 550 parts widely spread among its products with just SLS. While a majority of parts produced are experimental, it is to be noted that over 200 of those 550 parts are for production purposes.

- Moreover, in July 2022, GKN Aerospace expanded its range of metal additive manufacturing machines at the company's global technology center in the United Kingdom by installing RenAM 500 Flex. The RenAM 500Q Flex is a four-laser Additive Manufacturing machine that is expected to optimize Additive Manufacturing for aerospace applications.

- Furthermore, according to the US Census Bureau, it is expected that the revenue of aerospace products and parts manufacturing in the United States will amount to about USD 264.4 billion by 2024. Moreover, It is likely that the revenue of aerospace products and parts manufacturing in Canada will amount to approximately USD 19.3 billion by 2024. Such developments would drive the market's growth positively.

- According to Stockholm International Peace Research Institute (SIPRI), the United States led the ranking of countries with maximum military spending in 2021, with 801 USD billion dedicated to the military, which was 38 percent of the global military expenditure of USD 2.1 trillion.

North America is Expected to Hold Major Market Share

- North America is home to many companies developing, adopting, or investing in additive manufacturing. There has been a growth in the demand for prototyping in the region which has been majorly driving the market in the region. Further, the demand for SLS in North America is driven by a higher focus on research and development and increased testing in various industries.

- According to Statistics Canada, Canadian businesses intend to spend USD 21.9 billion on in-house industrial research and development in 2021, while USD 22.4 billion is expected to be spent in 2022. Such growth in research and development is expected to push the market for Selective Laser Sintering in North America.

- Companies in the region are doing strategic collaborations to provide their solutions to a broader customer base. For instance, in May 2022, Essentium Inc, a US-based company, partnered with Nuburu, a blue laser solution provider, to develop a blue laser-based metal Additive Manufacturing platform.

- The resulting machine is hoped to enable manufacturers to create production-grade metal parts with high resolution and fast throughput. Further, as a part of the contract, Nuburu will license its additive manufacturing application patents.

- The increase in the usage of new technologies, such as 3D printing, is also expected to drive the market of SLS in the region. For instance, according to World Economic Forum, it is expected that by 2022, 47% of the surveyed companies in the United States will use 3D printing technology.

Selective Laser Sintering (SLS) Industry Overview

The Selective Laser Sintering Market majorly comprises incumbents operating globally, along with a few regional players vying for attention in a consolidated market space. The presence of several players, such as 3D Systems Inc., EOS GmbH Electro Optical Systems, Ricoh Company Ltd., and Fathom Manufacturing, among others with considerable expertise in the field, is expected to intensify the competitive rivalry further.

- June 2022 - 3D Systems and EMS GRILTECH announced the strategic partnership to enhance additive manufacturing materials development. Both companies will introduce a novel nylon copolymer - DuraForm PAx Natural- designed to be used with any commercially-available selective laser sintering (SLS) printer.

- November 2021 - Evonik Industries AG announced that it offers a broader range of RESOMER PrintPowder polymers to enable the 3D printing of personalized implantable medical devices. The new powders are available globally for 3D printing through selective laser sintering (SLS). Due to a broader range of customizable mechanical properties and degradation rates, the new powders could be used for more complex and tailored medical devices, including diverse orthopedic, dental, or soft tissue applications.

- February 2021 - 3D Systems announced the expansion plan of its Rock Hill, South Carolina, location, adding 100,000 square feet to its existing headquarters campus. This expansion will enable the company to consolidate its materials manufacturing, quality, and logistics operations, with new and expanded materials development laboratories to improve operational efficiencies, accelerate solution development, and reduce time to market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porters Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of COVID-19 on the Market

- 4.4 Analysis of 3D Printing Technologies (FDM, SLA, SLS; Qualitative Analysis on Materials and Technologies; Benchtop Industrial SLS Vs Traditional Industrial SLS Printers)

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Reduced Time for the End Product to Reach the Market

- 5.1.2 Increased Government Initiatives Across Various Regions

- 5.2 Market Challenges

- 5.2.1 Additional Capital Expenditure and Restrictions in Mass Production

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Metal

- 6.1.2 Plastic

- 6.2 By Component

- 6.2.1 Hardware

- 6.2.2 Software

- 6.2.3 Services

- 6.3 By End-user Industry

- 6.3.1 Automotive

- 6.3.2 Aerospace and Defense

- 6.3.3 Healthcare

- 6.3.4 Electronics

- 6.3.5 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia Pacific

- 6.4.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 3D Systems Inc.

- 7.1.2 EOS GmbH Electro Optical Systems

- 7.1.3 Farsoon Technologies

- 7.1.4 Prodways Group

- 7.1.5 Formlabs Inc.

- 7.1.6 Ricoh Company Ltd

- 7.1.7 Concept Laser GmbH (General Electric)

- 7.1.8 Renishaw PLC

- 7.1.9 Sinterit Sp. Zoo

- 7.1.10 Sintratec AG

- 7.1.11 Sharebot SRL

- 7.1.12 Red Rock SLS