|

市场调查报告书

商品编码

1433849

ICS(工业控制系统)安全:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Industrial Control Systems (ICS) Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

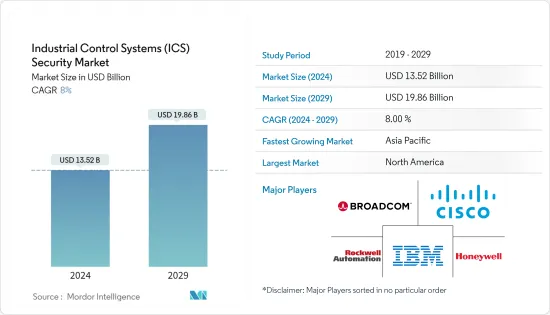

ICS(工业控制系统)安全市场规模预计到 2024 年为 135.2 亿美元,预计到 2029 年将达到 198.6 亿美元,预测期内(2024-2029 年)复合年增长率为 8。经过 %。

主要亮点

- 向工业 4.0 的过渡预计将带来效率和生产力的许多进步,以及工业流程工作方式的许多变化。与传统製造流程相比,效率的提高和生产成本的降低正在推动自动化的采用,并推动对 ICS 的需求。然而,随着网路攻击和网路安全威胁呈指数级增长,ICS解决方案的采用带来了安全需求。

- 网路威胁的增加正在推动全球工业控制系统和安全市场的销售成长。网路攻击的增加导致製造、化学、能源和其他行业越来越多地采用 ICS。随着骇客试图闯入商业网络,ICS 安全性的使用显着增加。此外,先进技术的采用正在产生大量资料,增加了对ICS安全的需求,从而推动了全球市场的收益成长。

- 政府与持续改进计划 (CIP) 相关的严格规则和法规,旨在增加 ICS 安全解决方案的采用,以及工业中物联网 (IoT) 等先进技术的采用,正在增加对 ICS 安全市场的需求。工业网路基础设施连接大量感测器和控制器,安全性难以保证。物联网技术和其他网路设备在工业中的日益使用正在扩大犯罪分子的威胁面。组织的物联网应用需要 ICS 安全性,这将推动市场发展。

- COVID-19 大流行和全部区域封锁规定影响了工业活动。疫情增加了消费者对网路的依赖,进一步扩大了ICS市场。 COVID-19 的爆发迫使製造业重新评估传统生产流程,主要推动整个生产线的数位转型和智慧製造实践。製造商也被迫设计和实施多种新的敏捷方法来监控产品和品管。

- 许多组织中 ICS 硬体和软体的老化加剧了复杂性。由于传统 ICS 对工厂功能的重要性,大多数组织仍然使用传统 ICS。 ICS 的老化为网路攻击留下了充足的机会并增加了复杂性。此外,安全系统和平台的成本是阻碍组织部署ICS保全服务的另一个因素。由于多种原因,证明安全解决方案成本的合理性非常困难。

ICS安全市场趋势

汽车产业预计将占据较大份额

- ICS 为汽车产业提供了快速回应市场需求、减少製造停机时间、提高供应链效率和扩大生产力的机会。

- 机器人和感测器等现场设备和 ICS 为汽车行业提供了快速响应市场需求、减少製造停机时间、提高效率和扩大生产力的机会。

- 汽车产业是重要产业之一,在全球自动化製造设备中占有很大份额。各种汽车製造商的生产设施都实现了自动化,以保持效率。以电动车(EV)取代传统汽车的趋势日益增长,预计将进一步增加汽车产业的需求。例如,IEA表示,全球电动车销量将从2020年的300万辆翻倍至2021年的660万辆。

- 多家汽车相关企业正在与 ICS 供应商合作升级其设备。例如,ICONICS 与 S&T Technologies 签署了合作协议,后者提供物联网软体框架 SUSiEtec。该协议规定,S&T Technologies 将把 SCADA 功能整合到 SUSiEtec 软体框架中。

- 儘管汽车产业大幅放缓,但主导电动车製造商为首的汽车生产设施中安装的智慧/网路连线 ICS 解决方案的数量不断增加,这显着增加了对 ICS 安全解决方案的需求。

预计北美将占据最大份额

- 北美是实施 ICS 安全解决方案的先驱。该地区对最新技术进步也高度敏感,例如将云端和物联网与ICS安全解决方案相集成,以建立整体安全存取机制并实施安全管治框架。官民合作关係和国际合作正在为该地区带来有效的工业控制系统安全和復原力。

- 据国防安全保障部 (DHS) 称,私营部门拥有美国85% 的关键基础设施,包括石油和天然气、银行和金融、交通、公共产业、电网和国防。同时,公共部门负责监管其余部分。例如,在该地区的能源和电网领域,国土安全部、能源部(DOE)和国防部(DOD)要求公私监管合作,以保护操作技术和工业控制系统来自网路威胁。此外,云端基础的ICS 安全解决方案和服务在该地区越来越受欢迎。

- 加拿大製造商依靠创新和技术投资来保持竞争力。不断上升的投入和人事费用,以及来自全球大型製造商的竞争,促使加拿大投资 ICS 和相关技术,以保持竞争力并维持营运报酬率。

- 此外,根据加拿大政府2021年版本,预计製造业对加拿大GDP的贡献率将超过10%。製造业是加拿大新技术研究、开发和实施的最大投资者。

- 最近,MITRE 公司发布了工业控制系统 ATT&CK,这是针对 ICS 的网路攻击行为的分类。该攻击针对金融和间谍动机的攻击以及行业意识,推出解决製造业和公共产业领域的关键基础设施运营问题。

- 然而,国家对监管的抵制以及确保工业控制系统安全的日益复杂性可能会阻碍关键基础设施网路安全立法的通过。

ICS安全产业概述

ICS 安全市场竞争激烈,由多家大型企业组成。许多公司透过推出新产品、建立合作伙伴关係和收购公司来扩大市场份额。

- 2021 年 9 月Honeywell收购了非上市公司 Performix Inc.,该公司是一家面向製药製造和生物技术行业的製造执行系统 (MES) 软体提供商。此次收购建立在Honeywell的策略之上,即为生命科学客户打造全球领先的整合软体平台,以最高的品质水准提供更快的合规性、更高的可靠性和更高的生产量。我们正在努力实现这一目标。

- 2021 年 8 月 - 总部位于美国加州的领先网路安全解决方案供应商 CyberProof 宣布与总部位于以色列特拉维夫-雅法的工业网路网路安全解决方案供应商 Radiflow 建立合作伙伴关係。此次合作也增强了 Cyber Proof 提供整合到资讯技术 (IT) 或操作技术(OT) 系统中的全面託管检测和回应 (MDR) 服务的能力。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 产业价值链分析

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 网路攻击增加

- IT 与 OT 网路融合

- 市场限制因素

- 安全系统实施的复杂性

- ICS安全产业各种经营模式的出现

第六章市场区隔

- 最终用户产业

- 汽车产业

- 化工/石化

- 电力/公用事业

- 药品

- 食品和饮料

- 油和气

- 其他的

- 地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 其他亚太地区

- 拉丁美洲

- 中东/非洲

- 北美洲

第七章 竞争形势

- 公司简介

- Darktrace Ltd

- FireEye Inc.

- IBM Corporation

- Cisco Systems Inc.

- Fortinet Inc.

- Check Point Software Technologies Ltd

- Honeywell International Inc.

- Broadcom Inc.(Symantec Corporation)

- AhnLab Inc.

- McAfee LLC(TPG Capital)

- Rockwell Automation Inc.

- Dragos Inc.

第八章投资分析

第9章市场的未来

简介目录

Product Code: 66569

The Industrial Control Systems Security Market size is estimated at USD 13.52 billion in 2024, and is expected to reach USD 19.86 billion by 2029, growing at a CAGR of 8% during the forecast period (2024-2029).

Key Highlights

- The transition to Industry 4.0 is expected to bring many advances in efficiency and productivity, as well as many changes in the way the industrial processes work. Compared to the conventional manufacturing process, improved efficiency and reduction in production costs have boosted the adoption of automation, driving the demand for industrial control systems. However, the adoption of ICS solutions brings along the need for security, as there is an exponential rise in cyber-attacks and network security threats.

- The growing number of cyber threats has fueled revenue growth in the worldwide industrial control systems security market. With the increasing number of cyber-attacks, the adoption of industrial control systems is increasing in the manufacturing, chemical, energy, and other industries. With increasing attempts by hackers to enter business networks, the use of ICS security is growing significantly. Furthermore, the adoption of advanced technologies is resulting in the generation of massive amounts of data, increasing demand for ICS security, and as a result, driving revenue growth in the global market.

- The stringent government rules and regulations related to the Continuous Improvement Programme (CIP) to increase the adoption of ICS security solutions and the adoption of advanced technologies such as the Internet of Things (IoT) in industries has increased demand for the ICS security market. The industrial network infrastructure's large number of connected sensors and controllers has made security more difficult. The growing use of IoT technology and other network devices in industries has expanded the threat surface for criminals. ICS security is necessary for organizations' IoT applications, which will drive the market.

- The COVID-19 pandemic and lockdown restrictions across the region have affected industrial activities. The pandemic increased consumers' dependence on the internet, further increasing the market for industrial control systems. The outbreak of COVID-19 has forced manufacturing industries to re-evaluate their traditional production processes, primarily driving the digital transformation and smart manufacturing practices across the production lines. The manufacturers are also forced to devise and implement multiple new and agile approaches to monitor product and quality control.

- The aging hardware or software of the ICS in many organizations is another factor responsible for increased complexity. Most organizations still use legacy ICS, owing to their importance in the functioning of the plant. This increased age of ICS leaves ample opportunities for cyberattacks and increases complexity. Also, the cost of a security system or platform is another factor hindering the deployment of ICS security services in organizations. Justifying the cost incurred for the security solutions is quite difficult for various reasons.

Industrial Control Systems Security Market Trends

Automotive is Expected to Hold a Significant Share

- ICS offers opportunities to the automotive industry to react faster to the market requirements, reduces manufacturing downtimes, enhances the efficiency of supply chains, and expands productivity.

- Field devices, such as robotics and sensors, and ICS offer opportunities to the auto sector to react faster to market requirements, reduce manufacturing downtimes, enhance efficiency, and expand productivity.

- The automotive industry is among the prominent sectors that hold a significant share of automated manufacturing facilities worldwide. The production facilities of various automakers are automated to maintain efficiency. The rising trend of replacing conventional vehicles with electric vehicles (EVs) is expected to augment the automotive industry's demand further. For instance, IEA states global electric car sales doubled from 3.0 million in 2020 to 6.6 million in 2021.

- Various automotive enterprises are forming partnerships with the ICS providers to upgrade their facilities. For example, S&T Technologies, a provider of IoT software framework, SUSiEtec, and ICONICS signed a collaboration agreement. The contract specifies that S&T Technologies will integrate SCADA capabilities into the SUSiEtec software framework.

- Despite a considerable slowdown in the automotive industry, automotive production facilities led by electric vehicle manufacturers are expected to increase the number of smart/internet-connected ICS solutions installed in a facility, significantly increasing the demand for ICS Security solutions.

North America is Expected to Hold the Largest Share

- North America has been a pioneer in implementing ICS security solutions. This region has also been extremely responsive to the latest technological advancements, such as integrating cloud and IoT with ICS security solutions to set a holistic secure access mechanism and enforce a security governance framework. The Public-Private Partnerships and international partnerships have led to effective ICS security and resilience in the region.

- According to the Department of Homeland Security (DHS), The private sector owns 85% of critical infrastructure in the United States, including oil and gas, banking and finance, transportation, utilities, electric power grids, and defense. In contrast, the public sector regulates the rest. For instance, the region's energy and power grid sectors require public, private, and regulatory collaboration among DHS, the Department of Energy (DOE), and the Department of Defense (DOD) to protect their operational technology and Industrial Control Systems from cyber threats. Furthermore, cloud-based ICS security solutions and services are becoming increasingly popular in this region.

- Canadian manufacturers rely on innovation and investment in technologies to be competitive. The increasing input, labor cost, and competition from large global manufacturers enabled the country to invest in ICS and allied technologies to remain competitive and maintain its operating margins.

- Furthermore, according to the Government of Canada 2021, the manufacturing industry is estimated to contribute more than 10% to the Canadian GDP. The manufacturing sector is the largest investor in the R&D and implementation of new technologies in Canada.

- Recently, MITRE Corporation released ATT&CK for Industrial Control Systems, a taxonomy of cyber attack behavior targeting ICS. The company was launched to address critical infrastructure operations in manufacturing and utility industries with financial and espionage-motivated attacks and industry awareness.

- However, the country's resistance to regulation and growing complexities in securing ICS systems may act as a roadblock to the passage of critical infrastructure cybersecurity legislation.

Industrial Control Systems Security Industry Overview

The Industrial Control System Security Market is highly competitive and consists of several major players. Many companies have been increasing their market presence by introducing new products, entering partnerships, or acquiring companies.

- September 2021 - Honeywell acquired privately held Performix Inc., a manufacturing execution system (MES) software provider for the pharmaceutical manufacturing and biotech industries. The acquisition builds on Honeywell's strategy to create the world's leading integrated software platform for customers in the life sciences industry, striving to achieve faster compliance, improved reliability, and better production throughput at the highest levels of quality.

- August 2021 - CyberProof, a leading provider of cyber security solutions based in California, United States., announced a collaboration with Radiflow, a Tel Aviv-Yafo, Israel-based provider of cyber security solutions for industrial networks. In addition, the partnership strengthens CyberProof's ability to provide comprehensive Managed Detection and Response (MDR) services for converged Information Technology (IT) or Operational Technology (OT) systems.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Incidence of Cyberattacks

- 5.1.2 Convergence of IT and OT Networks

- 5.2 Market Restraints

- 5.2.1 Complexity in Implementing the Security Systems

- 5.2.2 Emergence of Various Business Models in ICS Security Industry

6 MARKET SEGMENTATION

- 6.1 End-user Industry

- 6.1.1 Automotive

- 6.1.2 Chemical and Petrochemical

- 6.1.3 Power and Utilities

- 6.1.4 Pharmaceuticals

- 6.1.5 Food and Beverage

- 6.1.6 Oil and Gas

- 6.1.7 Other End-user Industries

- 6.2 Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 France

- 6.2.2.4 Rest of Europe

- 6.2.3 Asia Pacific

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 Japan

- 6.2.3.4 Rest of Asia Pacific

- 6.2.4 Latin America

- 6.2.5 Middle East and Africa

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles *

- 7.1.1 Darktrace Ltd

- 7.1.2 FireEye Inc.

- 7.1.3 IBM Corporation

- 7.1.4 Cisco Systems Inc.

- 7.1.5 Fortinet Inc.

- 7.1.6 Check Point Software Technologies Ltd

- 7.1.7 Honeywell International Inc.

- 7.1.8 Broadcom Inc. (Symantec Corporation)

- 7.1.9 AhnLab Inc.

- 7.1.10 McAfee LLC (TPG Capital)

- 7.1.11 Rockwell Automation Inc.

- 7.1.12 Dragos Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

02-2729-4219

+886-2-2729-4219

2024-2032 年工业控制系统安全市场报告(按组件、系统类型、安全类型、应用和地区)

2024-2032 年工业控制系统安全市场报告(按组件、系统类型、安全类型、应用和地区) 全球工业控制系统安全市场规模、份额、成长分析(按类型、系统类型)- 2023-2030 年产业预测

全球工业控制系统安全市场规模、份额、成长分析(按类型、系统类型)- 2023-2030 年产业预测 工业控制系统安全市场:按组件、安全类型、产业划分 - 全球预测 2024-2030 年

工业控制系统安全市场:按组件、安全类型、产业划分 - 全球预测 2024-2030 年 2024 年工业控制系统 (ICS) 安全全球市场报告

2024 年工业控制系统 (ICS) 安全全球市场报告 工业控制系统 (ICS) 安全市场 - 全球规模、份额、趋势分析、机会、预测报告,2019-2030 年

工业控制系统 (ICS) 安全市场 - 全球规模、份额、趋势分析、机会、预测报告,2019-2030 年 工业控制系统 (ICS) 安全市场规模、份额、趋势分析报告:按组件、按解决方案、按服务、按类型、按最终用途、按地区、按细分市场、预测,2024-2030 年

工业控制系统 (ICS) 安全市场规模、份额、趋势分析报告:按组件、按解决方案、按服务、按类型、按最终用途、按地区、按细分市场、预测,2024-2030 年 工业控制系统 (ICS) 安全的全球市场(~2028 年):按组件、解决方案、服务、安全类型、产业和地区划分

工业控制系统 (ICS) 安全的全球市场(~2028 年):按组件、解决方案、服务、安全类型、产业和地区划分 工业控制系统安全全球市场 2023-2027

工业控制系统安全全球市场 2023-2027 2023-2030 年全球工业控制系统安全市场规模研究与预测(按最终用户划分)和区域分析

2023-2030 年全球工业控制系统安全市场规模研究与预测(按最终用户划分)和区域分析 产业用控制系统(ICS)保全的全球市场:各提供,保全类型,组织规模,用途,最终用途产业 - 预测(~2030年)

产业用控制系统(ICS)保全的全球市场:各提供,保全类型,组织规模,用途,最终用途产业 - 预测(~2030年)

▼