|

市场调查报告书

商品编码

1433885

机器人软体:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Robot Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

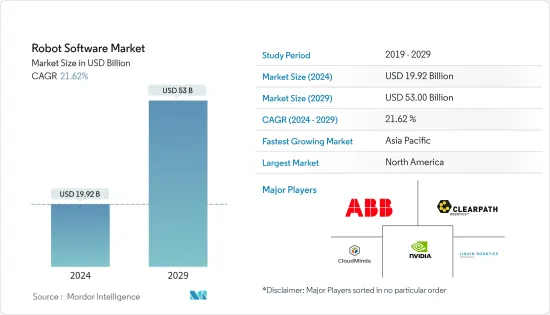

预计2024年全球机器人软体市场规模将达199.2亿美元,2024-2029年预测期间复合年增长率为21.62%,到2029年将达530亿美元。

主要亮点

- 机器人软体可实现智慧、运动、安全性和生产力功能,使机器人能够看到、感觉、学习和维护安全。这些特性和优点使用户能够快速轻鬆地运作并以最佳生产力运作机器人。推动机器人软体市场的关键因素是人工智慧的引入、速度的提高、品质的提高、人事费用的降低、准确性的提高以及生产的扩充性。

- 机器人在製造、电气和电子、汽车、食品和饮料以及製程控制等各种最终用户行业中越来越多的采用被认为是机器人软体平台市场的主要成长动力。机器人在各个最终用户行业中的使用不断增加,有助于满足客製化需求,同时降低人事费用。

- 自从机器人发明以来,软体在机器人领域发挥了重要作用。透过引入新的软体功能,可以改进机器人的控制、快速自订序列并且易于使用,该软体预计将在未来几年进一步推动机器人技术的采用。

- 然而,资料安全和日益增加的网路攻击正在阻碍市场成长。此外,机器人犯罪的增加阻碍了机器人在各个领域的引入,从而降低了机器人软体引入的前景。缺乏熟练的专业知识也是这个市场的主要限制。

- COVID-19 为扩大机器人软体的使用和改进机器人调查提供了坚实的动力。疫情期间,多家公司安装了机器人来消毒区域并向隔离人员运送食品。一些公司设计了机器人软体来帮助人们追踪社区中的 COVID-19。

机器人软体市场趋势

工业机器人占据大部分应用

- 工业物联网 (IIoT) 等技术的出现对于智慧工厂概念与工业 4.0 的结合至关重要,它正在增加工业机器人在製造业中的采用。工业机器人通常用来取代人类工人,以高精度执行危险或重复性任务。

- 为了有效率地操作机器人,机器人软体至关重要,可以根据製造商的需求来操作机器人。该软体是人类能力的延伸。它反映了人类的愿景,随着每一代和技术的进步而变得更加清晰。随着工业领域机器人技术的显着成长,对机器人软体的需求也显着增加。

- 根据自动化促进协会统计,2021年北美地区工业机器人订单量为39,708台,较2017年的历史高点成长了14%。此外,自动化技术的普及正在增加汽车产业对机器人的需求。例如,根据自动化推进协会的数据,2021 年第四季度,汽车客户购买了总订单的 39%。

- 此外,人工智慧和机器学习能力正在迅速渗透工业机器人技术。机器人技术与人工智慧技术相结合的最重要好处之一是透过预测性维护增加运作和生产力。透过整合人工智慧和工业机器人技术,机器人可以监控自身的准确性和性能,并在需要维护时提供讯号,以避免代价高昂的停机时间。

- 此外,2023 年 5 月,Alphabet 在其工业机器人业务部门 Intrinsic 下推出了首款产品,名为 Flowstate。它是一个直观的基于网路的开发环境,允许公司创建机器人工作流程,并为用户提供开始建立机器人系统的基础。它还包括用于测试您的设计的模拟功能。特别是,该软体旨在帮助非专业人士理解和利用机器人系统。

亚太地区预计将出现显着成长

- 预计亚太地区在预测期内将呈现显着的成长机会。对该地区机器人软体市场成长做出贡献的主要国家是中国、日本、新加坡、韩国和印度。该地区国家越来越多地在所有行业中实施机器人技术。

- 由于中国在「十三五」规划中明确将人工智慧和机器人技术列为优先重点,预计中国市场在人工智慧和机器人技术方面的支出将增加。中国国家发展和改革委员会宣布了一项为期三年的人工智慧实施计划,预计将加速采用尖端技术,帮助中国在 2030 年成为超级大国。

- 根据 IFR 的数据,2021 年所有新部署的机器人中有 73% 安装在亚洲。 2021年出货为35.4万台,较2020年成长33%。迄今为止,电子业采用的设备最多(123,800 台安装),其次是汽车行业(72,600 台安装)和金属和机械行业(36,400 台安装)的强劲需求。

- 日本也是世界领先的机器人製造国之一。据IFR称,2021年日本将成为仅次于中国的第二大工业机器人市场。 2021年,安装数量成长22%,达到47,182台。日本运作库存为393,326辆,2021年成长5%。

- 该地区的公司致力于开发创新解决方案,以保持市场竞争力。例如,亚马逊于2022年5月宣布将在印度开设一个新的消费机器人软体开发中心,为全球开发解决方案。印度中心将为亚马逊的国际机器人部门提供支持,该部门于 2021 年推出了该公司的首款机器人 Astro。

机器人软体产业概况

由于机器人领域的应用渗透到各个行业,机器人软体市场适度分散。机器人软体公司不断致力于开发先进技术,以增强机器人流程并帮助增强製造业流程。市场上一些知名的供应商包括 ABB Ltd、Clearpath Robotics、NVIDIA Corporation 和 CloudMinds Technology Inc.。

2022 年 11 月,Clearpath Robotics 宣布推出 OutdoorNav 自主导航软体平台,旨在帮助车辆开发商、OEM和机器人研究人员加速机器人和自动驾驶车辆的开发流程。该平台相容于该公司的Jackal UGV、Husky UGV、Warthog UGV等户外移动平台,以及具有线控驾驶功能的第三方工业车辆,并可提供可靠的基于GPS的导航。

2022年5月,ABB Robotics推出快速对中软体。预计这将使製造商能够将六轴机器人的速度提高约 70%,精度提高 50%,从而显着缩短上市时间,同时显着缩短上市时间。我是。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 组织对自动化和安全性的需求不断增长

- 中小型企业快速采用机器人软体以降低人事费用和能源成本

- 市场挑战

- 实施成本上升以及对软体的恶意软体攻击增加

第六章市场区隔

- 依软体类型

- 辨识软体

- 模拟软体

- 预测性维护软体

- 资料管理与分析软体

- 通讯管理软体

- 按机器人类型

- 工业机器人

- 服务机器人

- 按介绍

- 本地

- 一经请求

- 按公司规模

- 中小企业

- 大公司

- 按行业分类

- 车

- 零售/电子商务

- 政府/国防

- 卫生保健

- 运输/物流

- 製造业

- 资讯科技/通讯

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第七章 竞争形势

- 公司简介

- ABB Ltd

- Clearpath Robotics

- NVIDIA Corporation

- CloudMinds Technology Inc.

- Liquid Robotics Inc.

- Brain Corporation

- AIBrain Inc.

- Furhat Corporation

- Neurala Inc.

第八章投资分析

第九章 市场机会及未来趋势

The Robot Software Market size is estimated at USD 19.92 billion in 2024, and is expected to reach USD 53 billion by 2029, growing at a CAGR of 21.62% during the forecast period (2024-2029).

Key Highlights

- Robot software enables functions for intelligence, motion, safety, and productivity and gives the power to get the robots to see, feel, learn, and maintain security. These characteristics and benefits allow users to instantly and easily get their robots up and running at optimum productivity. The major factors driving the robot software market are the adoption of artificial intelligence, enhanced speed, improved quality, reduced labor cost, increased accuracy, and production scalability.

- Rising adoption of robots across various end-user industries such as manufacturing, electrical and electronics, automotive, food and beverage, and process controls are seen as primary growth drivers for the robotics software platforms market. The growing utilization of robots in varied end-user industries helps meet customized demand while simultaneously helping lower labor costs.

- Since the invention of robots, software has played a key role in the field of robotics. With the introduction of new software features that enable better control of the robot, quick customization of sequences, and ease of use, the software is expected to further boost the adoption of robotics in the coming years.

- However, data security and increasing cyberattacks are hindering market growth. Also, increasing robot crimes are impeding the adoption of robots in various sectors, thus, reducing the robot software adoption prospects. Also, the lack of skilled expertise is another major restraining factor for this market.

- COVID-19 provided a solid push to expand the usage of robot software and improve robotics research. During the pandemic, various companies have installed robots to disinfect areas and deliver food to quarantined people. Some companies designed robot software to help people track COVID-19 in their communities.

Robot Software Market Trends

Industrial Robots to Have the Majority Application

- With the advent of technologies like the Industrial Internet of Things (IIoT), vital to the smart factory concept coupled with Industry 4.0, industrial robot adoption is increasing across the manufacturing industries. An industrial robot is generally used in place of human laborers to perform dangerous or repetitive tasks with high accuracy.

- In order to make the robots perform efficiently, robot software is essential to operate the robots according to the needs of the manufacturers. This software is an extension of human capability. It reflects the human vision that gets keener with every generation and every technological leap. With the enormous growth of robotics in the industrial sector, the need for robotic software is also increasing substantially.

- According to Association for Advancing Automation, industrial robots ordered in North America in 2021 were 39,708 units, up by 14% from the previous high in 2017. Moreover, the widespread adoption of automated technology is raising the demand for robots in the automotive industry. For instance, in Q4 2021, automotive-related customers purchased 39% of the total orders, as per Association for Advancing Automation.

- Moreover, Artificial Intelligence and machine learning capabilities have been rapidly making their way into industrial robotics technology. One of the most significant benefits derived from the merging of robotics and AI technology is increased uptime and productivity from predictive maintenance. With AI integrated with industrial robotics technology, robots are able to monitor their own accuracy and performance, providing signals when maintenance is required to avoid expensive downtime.

- Furthermore, in May 2023, Alphabet launched the first product under its industrial robotics business unit Intrinsic, called Flowstate, which is an intuitive, web-based developer environment where companies can create robotic workflows, offering users the foundation to begin building robotic systems, as well as simulation capabilities to test designs. In particular, the software is aimed at helping non-experts understand and leverage robotic systems.

The Asia-Pacific Region Expected to Register Significant Growth

- The Asia-Pacific region is expected to exhibit significant growth opportunities over the forecast period. The major economies contributing to the growth of the robot software market in this region are China, Japan, Singapore, South Korea, and India. The countries in this region are increasingly adopting robotics across industries.

- The Chinese market is expected to increase its expenditure on AI and robotics, as the country has categorically prioritized its focus on AI and robotics in its 13th five-year plans. China's National Development and Reform Commission has announced an AI three-year implementation program expected to accelerate the adoption of advanced technologies to help the country become a superpower by 2030.

- According to IFR, 73% of all newly deployed robots in 2021 were installed in Asia. 354,000 units were shipped in 2021, up by 33% compared to 2020. The electronics industry adopted by far the most units (123,800 installations), followed by strong demand from the automotive industry (72,600 installations) and the metal and machinery industry (36,400 installations).

- Also, Japan is the predominant robot manufacturing country in the world. According to IFR, Japan emerged as the second largest market for industrial robots after China in 2021. Installations increased by 22% in 2021, with 47,182 units. Japan's operational stock was 393,326 units, increasing by 5% in 2021.

- Companies in the region are looking to develop innovative solutions to remain competitive in the market. For instance, in May 2022, Amazon announced that it would open a new consumer robotics software development center in India to develop solutions for the world. The India center will help Amazon's International robotics division, which launched its first robot Astro in 2021.

Robot Software Industry Overview

The Robot Software Market is moderately fragmented owing to the penetration of robotics globally with applications in various industries. Robotic software companies are constantly focusing on developing advanced technologies that would enhance the robotic processes and help the manufacturing industries to intensify their process. Some of the prominent vendors in the market include ABB Ltd, Clearpath Robotics, NVIDIA Corporation, and CloudMinds Technology Inc.

In November 2022, Clearpath Robotics introduced its OutdoorNav autonomous navigation software platform, which is designed to help vehicle developers, OEMs, and robotics researchers accelerate the development process for their robots and autonomous vehicles. The platform is compatible with the company's outdoor mobile platforms, like the Jackal UGV, Husky UGV, and Warthog UGV, and third-party industrial vehicles with drive-by-wire control, and can provide them with reliable GPS-based navigation.

In May 2022, ABB Robotics launched its High-Speed Alignment software, which was expected to give manufacturers the ability to increase the speed of 6-axis robots by around 70% and accuracy by 50% - significantly reducing time-to-market while increasing accuracy levels.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in need for automation and safety in organizations

- 5.1.2 Rapid adoption of robot software by SMEs to reduce labor and energy costs

- 5.2 Market Challenges

- 5.2.1 High cost of implementation and rise in malware attacks on the software

6 MARKET SEGMENTATION

- 6.1 By Software Type

- 6.1.1 Recognition Software

- 6.1.2 Simulation Software

- 6.1.3 Predictive Maintenance Software

- 6.1.4 Data Management and Analysis Software

- 6.1.5 Communication Management Software

- 6.2 By Robot Type

- 6.2.1 Industrial Robots

- 6.2.2 Service Robots

- 6.3 By Deployment

- 6.3.1 On-Premise

- 6.3.2 On-Demand

- 6.4 By Enterprise Size

- 6.4.1 Small and Medium Enterprises

- 6.4.2 Large Enterprises

- 6.5 By End-user Vertical

- 6.5.1 Automotive

- 6.5.2 Retail and E-commerce

- 6.5.3 Government and Defense

- 6.5.4 Healthcare

- 6.5.5 Transportation and Logistics

- 6.5.6 Manufacturing

- 6.5.7 IT and Telecommunications

- 6.5.8 Other End-user Verticals

- 6.6 By Geography

- 6.6.1 North America

- 6.6.2 Europe

- 6.6.3 Asia-Pacific

- 6.6.4 Latin America

- 6.6.5 Middle-East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Ltd

- 7.1.2 Clearpath Robotics

- 7.1.3 NVIDIA Corporation

- 7.1.4 CloudMinds Technology Inc.

- 7.1.5 Liquid Robotics Inc.

- 7.1.6 Brain Corporation

- 7.1.7 AIBrain Inc.

- 7.1.8 Furhat Corporation

- 7.1.9 Neurala Inc.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

2024-2032 年按软体类型、机器人类型、部署模式、企业规模、最终用途产业和地区分類的机器人软体市场报告

2024-2032 年按软体类型、机器人类型、部署模式、企业规模、最终用途产业和地区分類的机器人软体市场报告 机器人软体市场 - 按软体类型、按机器人类型(工业机器人、服务机器人)、按部署模式、按企业规模、按最终用途行业和预测 2024 - 2032

机器人软体市场 - 按软体类型、按机器人类型(工业机器人、服务机器人)、按部署模式、按企业规模、按最终用途行业和预测 2024 - 2032 机器人软体平台市场:按机器人类型、功能、部署和最终用户划分 - 2024-2030 年全球预测

机器人软体平台市场:按机器人类型、功能、部署和最终用户划分 - 2024-2030 年全球预测 视觉引导机器人软体市场规模和预测、全球和地区份额、趋势和成长机会分析报告范围:按类型、技术、应用和垂直领域

视觉引导机器人软体市场规模和预测、全球和地区份额、趋势和成长机会分析报告范围:按类型、技术、应用和垂直领域 2024 年机器人软体全球市场报告

2024 年机器人软体全球市场报告 全球机器人软件平台市场 - 2023-2030

全球机器人软件平台市场 - 2023-2030 机器人软体的全球市场

机器人软体的全球市场 行动机器人平台的全球市场 2023-2027

行动机器人平台的全球市场 2023-2027 全球机器人软件市场——按软件类型、机器人类型、部署模式、公司规模、最终用户和地区划分的市场规模、细分市场、前景和收入预测(2022-2028 年)

全球机器人软件市场——按软件类型、机器人类型、部署模式、公司规模、最终用户和地区划分的市场规模、细分市场、前景和收入预测(2022-2028 年)