|

市场调查报告书

商品编码

1433922

精简型用户端:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Thin Client - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

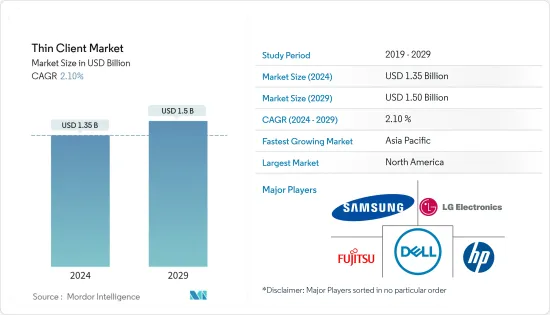

精简型用户端市场规模预计到 2024 年为 13.5 亿美元,预计到 2029 年将达到 15 亿美元,在预测期内(2024-2029 年)复合年增长率为 2.10%。

精简型用户端市场预计将在预测期内成长,主要是由于这些设备提供的成本和能源消费量降低、集中且易于存取的可管理性以及增强的基础设施安全性等优势。

主要亮点

- 各行业都在寻求低成本设备,以显着减少桌面空间并轻鬆更换/升级旧系统。精简型用户端系统满足这些要求。它还可以减少一段时间内的能源消耗。这是各行业对这些设备的需求不断增加的主要原因。由于这些设备的安全优势,医疗保健产业也广泛采用这些设备作为计算解决方案。相较之下,IT和通讯业安装这些设备主要是为了促进虚拟网路的发展。在企业和其他区域部署精简型用户端设备可以透过限制使用者侵入本机电脑设定来提供更高的安全相关优势。该应用程式将使您的系统更加安全和受到保护。

- 包括大学、研究机构和研究实验室在内的各种教育机构越来越多地实施精简型用户端解决方案,以集中管理 IT 管理部门的显示器并降低能耗。这些设备还可以减少系统升级的成本以及每次登入时设定 PC 或笔记型电脑所需的时间。

- 云端运算的日益普及也推动了市场的成长。一些组织使用云端运算来降低成本并存取未安装在电脑或伺服器上的资料和应用程式。云端已经成为一种基础设施,可以以动态可扩展和虚拟的方式快速提供运算资源作为公共事业。世界各地的组织正在转向混合和多重云端环境。精简型用户端有助于提供相对便宜且安全的硬体解决方案,从而推动市场成长。

- 由于多家企业越来越多地采用工作空间即服务 (WaaS),预计在预测期内市场需求将会增加。 WaaS 是多个组织用来为其员工提供应用程式远端存取的虚拟桌面。然而,新兴国家云端运算的网路问题预计将限制所研究市场的成长。

- 从事地缘政治敏感产业的能源公司经常成为网路攻击的目标,尤其是来自外国政府的网路攻击。然而,使用云端作为虚拟桌面的基础,您可以集中储存敏感资讯并设定身份验证策略来保护您的云端环境。预计这一因素将产生精简型用户端市场的需求。

- 在过去的几十年里,远距工作的趋势一直在稳步增长。然而,COVID-19 的影响在很短的时间内急剧加速了这一趋势,迫使各种规模的企业迅速适应世界各国政府建议的自我隔离措施。疫情要求更多的人远距工作,引发了人们对员工之间资料共用安全性的担忧。这推动了精简型用户端设备的需求采用。

精简型用户端市场趋势

医疗保健产业预计将推动市场成长

- 医疗保健提供者严格提供最高标准的患者照护。他们对用于改善每个护理阶段患者体验的技术非常敏感。从急诊室入院到復健和门诊护理,该技术可显着影响患者的治疗结果,并对医疗保健提供者的生产力和营运成本产生重大影响。对于整个医疗保健行业无处不在的桌面计算基础设施来说尤其如此。传统的桌面 PC 模型、资料和应用程式本地驻留在分布在网路上的各个 PC 上,通常会形成单独配置和管理的 PC丛集。这些与敏感的患者资料相关,并且通常具有很少或没有参数一致性。

- 然而,使用精简型用户端,资料和应用程式可以在资料中心或云端基础架构中远端管理、储存和集中。精简型用户端只是存取门户,管理员和临床医生可以在其凭证允许的情况下即时存取应用程式和病患资料。

- 由于其架构的性质,精简型用户端提供了各种安全优势,有助于确保符合 HIPAA 和其他医疗保健法规,同时最大限度地减少安全威胁。透过使用者身份验证和权限检验来严格控制授权使用者对云端基础的资料和应用程式的存取。这些安全措施可以透过 USB/连接埠保护、智慧卡和防火墙进一步增强。

- 儘管该行业目前正在走向数位化,但众所周知,它抵制变革,因为不可靠的技术失败可能会导致影响患者健康的问题。偏离指定的工作流程可能会对医院运作产生负面影响。儘管犹豫不决,该行业必须加快技术采用,以维持符合不断变化的法规和协议。

- 这些需求正在推动围绕着最大化我们提供的能力而设计的强大合作伙伴结构。例如,Stratodesk 是现代工作空间安全管理端点的先驱,于 2023 年 3 月宣布,几款 LG 商业解决方案精简型用户端将获得Stratodesk NoTouch OS 认证,允许IT 团队使用这两个平台。我们很自豪地宣布,我们可以让您有信心、弹性从世界任何地方部署承包设备。私有云端和公共云端。 Stratodesk 可自动交付最新的应用程式和 Web 技术,让您的共同客户可以使用熟悉的 Windows 或非 Windows 商业软体轻鬆地在任何地方保持工作效率。

预计北美将占据主要市场占有率

- 北美预计将主导市场,主要是由于越来越多地采用云端技术和需要活动性和弹性的先进技术导向产品等因素。该地区的大多数企业都可以获得 IT 支援。该地区市场领导的存在、大量的云端服务供应商以及不断增加的託管伺服器数量是该地区市场成长的重要因素。

- 该地区的组织是新技术的早期采用者,这是该地区优势的关键驱动力。领先的云端服务供应商在该地区云端基础的精简型用户端部署的成长中发挥关键作用。

- 云端运算和虚拟在广播领域变得越来越重要。透过网路通讯协定远端存取的虚拟机器和电脑可以对现场可用的实体硬体进行最佳补充。

- 北美 IT 和电讯业是其他区域市场中最大的市场之一。处理大量敏感资讯的行业(例如银行、医疗保健和政府机构)正在寻求精简型用户端解决方案。您可以比胖客户更好地维护知识产权的完整性。

- 硬体开发也投入了大量精力,供应商定期发布竞争版本。 2022 年 2 月,IGEL Ready 计画合作伙伴 OnLogic 宣布推出新的 IGL130 和 IGL160 IGEL Ready精简型用户端。这些新系统采用无风扇温度控管和 AMD Ryzen 嵌入式处理,将 IGEL 着名的通用桌上型硬体系列的性能与源自其工业应用血统的 OnLogic 的可靠运作相结合。该产品计划在美国进行首次发布,然后再进军海外市场。

精简型用户端产业概述

精简型用户端市场竞争非常激烈,因为有许多大公司向国内和国际市场提供产品。该市场似乎适度集中,主要企业采取产品和服务创新、合作、併购和收购等策略来扩大其地理覆盖范围并保持领先于竞争对手。该市场的主要企业包括戴尔公司、惠普开发公司、三星集团和 LG 电子公司。

- 2022 年 10 月:升腾和卡巴斯基签署协议,在 CyberImmune 端点方面展开合作。作为合作伙伴关係的一部分,卡巴斯基将提供KasperskyOS作业系统以及相关的网路免疫产品和解决方案,升腾将提供硬体。

- 2022 年 8 月:10ZiG 推出 7500q精简型用户端系列。配备 1.10-2.60 GHz(突发)Intel四核心处理器、15.6 吋显示器、FHD (1920 x 1080)、16:9 面板、8GB DDR4 2,666 MHz RAM、2 个 USB 连接埠 2.0、1 个 USB 连接埠。 3.0、1 个 USB 连接埠 C、1 个 HDMI、1 个 SD 读卡机、电池续航时间长达 10 小时。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 产业价值链分析

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 加强网路基础设施安全

- 降低成本和能源消耗

- 市场挑战

- 云端运算新兴国家的网路问题

第六章市场区隔

- 按类型

- 硬体

- 软体服务

- 按最终用户

- BFSI

- 资讯科技/通讯

- 卫生保健

- 政府机关

- 其他最终用户(零售、製造、教育)

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第七章 竞争形势

- 公司简介

- Dell Inc.

- HP Development Company LP

- Samsung Group

- LG Electronics Inc.

- NEC Corporation

- Fujitsu Ltd

- Lenovo Group Limited

- Cisco Systems Inc.

- Advantech Co. Ltd

- Siemens AG

- IGEL Technology GmbH

第八章投资分析

第九章 市场机会及未来趋势

The Thin Client Market size is estimated at USD 1.35 billion in 2024, and is expected to reach USD 1.5 billion by 2029, growing at a CAGR of 2.10% during the forecast period (2024-2029).

The thin client market is anticipated to grow during the forecast period, primarily due to the advantages, such as cost reduction and lesser energy consumption, centralized and accessible manageability, and the enhanced infrastructure security these devices offer.

Key Highlights

- Various industries seek low-cost devices that significantly decrease desk space and offer an easy replacement/upgrade for conventional systems. The thin client systems qualify for these requirements. They can also reduce energy consumption over a period, which is the primary reason for the increasing demand for these devices in various industries. The healthcare industry is also witnessing an extensive adoption of these devices as a computing solution, owing to their security benefits. In contrast, the IT and telecom industry is installing these devices primarily to facilitate the development of a virtual network. Implementing thin client devices in enterprises or other areas can provide better security-related advantages, as they limit the user from any intrusion in a local machine setting. This application renders the system more secure and protected.

- Various educational institutions, such as colleges, research institutes, and labs, are increasingly adopting thin client solutions to control the monitors centrally at the IT control department, thereby reducing energy consumption. These devices also decrease the cost of system upgrades and the time consumed in setting up the PC or laptop at each login.

- The growing adoption of cloud computing is also driving market growth. Several organizations use cloud computing to reduce costs and access the data and applications not installed on the computers or servers. Clouds emerged as an infrastructure that may enable the rapid delivery of computing resources as a utility in a dynamically scalable and virtual manner. Various organizations across the world are moving to a hybrid and multi-cloud environment. A thin client contributes to a comparatively less expensive and secure hardware solution, driving the market's growth.

- With the rising adoption of workspace-as-a-service (WaaS) in several enterprises, the market is anticipated to witness augmented demand during the forecast period. WaaS is a desktop virtualization used by multiple organizations to provide their employees access to applications remotely. However, network issues in developing countries for cloud computing are expected to restrain the growth of the studied market.

- Energy companies operating in a geopolitically sensitive industry face frequent cyberattack targets, especially from foreign governments. However, using the cloud as a base for desktop virtualization allows sensitive information to be stored centrally, and authentication policies can be set to secure the cloud environment. This factor is anticipated to generate demand for the thin client market.

- The trend toward remote work has been steadily growing for the past decades. However, the effect of COVID-19 dramatically accelerated this trend in an extremely short period, forcing companies, irrespective of their size, to adapt quickly to the self-isolation measures recommended by governments worldwide. With the pandemic requiring more people to be working remotely, the concern regarding the security of data sharing among employees increased. This has been driving the adoption of the demand for thin-client devices.

Thin Client Market Trends

The Healthcare Segment is Expected to Drive the Market's Growth

- Healthcare providers are stringent in offering the highest standards of patient care. They are acutely attuned to the technologies they use to improve the patient experience at every stage of care. From admissions to the emergency room to rehabilitation and outpatient care, the technology can significantly impact patient outcomes and critically impact providers' productivity and operational costs. This holds especially true for the ubiquitous desktop computing infrastructure across the healthcare domain. The legacy desktop PC model, data, and applications reside locally on individual PCs distributed across the network, often yielding a cluster of individually configured and managed PCs. These are associated with sensitive patient data, often with little to no parameter uniformity.

- However, with thin clients, data and applications are remotely administered, stored, and centralized in the data center or cloud infrastructure. The thin client is simply the access portal, giving administrators and clinicians immediate access to their applications and patient data as their credentials allow.

- By the nature of their architecture, thin clients offer various security advantages to help ensure compliance with HIPAA and other healthcare regulations while minimizing exposure to security threats. Authorized user access to cloud-based data and applications is strictly controlled via user authentication and permissions verification. USB/port protections, smart cards, and firewalls can further augment these security measures.

- Although the industry is currently transitioning into digitization, it has been notoriously recognized to be resistant to changes since any failure of unreliable technology translates into issues that affect patient health. Any deviation from predetermined workflows can adversely affect a hospital's operations. Despite the hesitancy, the industry must accelerate technology adoption to remain compliant with the constantly changing regulations and agreements.

- Such needs have encouraged robust partnership structures designed around maximizing offering capabilities. For instance, in March 2023, Stratodesk, the pioneer of securely managed endpoints for modern workspaces, announced that several LG Business Solutions Thin Clients are now certified with Stratodesk NoTouch OS, providing IT teams with the confidence and flexibility to deploy the turnkey devices from both private and public clouds. Stratodesk makes it easier for joint customers to stay productive from anywhere using Windows or non-Windows business software that they are familiar with by automating the delivery of the latest applications and web technologies.

North America is Expected to Hold a Major Market Share

- North America is expected to dominate the market, primarily due to the factors such as the increasing adoption of cloud technology and highly technology-oriented products, which require activity and flexibility. IT support is available to the majority of companies in the region. The presence of market leaders, a significant number of cloud service providers, and an increasing number of hosted servers in the area are essential contributors to the market's growth in the region.

- The organizations in the region are early adopters of new technologies, which is the primary driving force behind the region's dominance. Large cloud service providers play a significant role in the region's growth of cloud-based thin client deployment.

- Cloud computing and virtualization are becoming increasingly important in broadcasting. The physical hardware available on site can be optimally supplemented by virtual machines and computers, remotely accessed via network protocols.

- The North American IT and telecommunications industry is one of the largest among other regional markets. Industries such as banking, healthcare, and government organizations, which handle a large amount of sensitive information, are looking forward to adopting thin client solutions. They can preserve the integrity of the intellectual property better than a fat client.

- Hardware development has also been considerably worked on, with regular competitive releases by vendors. In February 2022, OnLogic, an IGEL Ready program partner, announced the availability of the new IGL130 and IGL160 IGEL Ready thin clients. These new systems, which feature fanless thermal management and AMD Ryzen Embedded processing, combine the performance of IGEL's famous Universal Desktop line of hardware with OnLogic's dependable operation derived from its industrial application lineage. The product is expected to register an initial release in the States before working towards overseas markets.

Thin Client Industry Overview

The thin client market is highly competitive due to the presence of many large players in the market providing products in the domestic and international markets. The market appears to be mildly concentrated, with the key players adopting strategies like product and service innovations, partnerships, mergers, and acquisitions to extend their geographic reach and stay ahead of the competitors. Some of the major players in the market are Dell Inc., H.P. Development Company LP, Samsung Group, and L.G. Electronics Inc.

- October 2022: Centerm and Kaspersky signed an agreement to collaborate on Cyber Immune Endpoints. Kaspersky plans to provide the KasperskyOS operating system and related cyber immune products and solutions as part of the collaboration, while Centerm plans to provide hardware.

- August 2022: The 7500q thin client series was introduced by 10ZiG. It has an Intel Quad Core processor with 1.10 to 2.60 GHz (Burst), a 15.6" display, FHD (1920 x 1080), a 16:9 panel, 8GB DDR4 2,666 MHz RAM, 2 x USB Port 2.0, 1 x USB Port 3.0, 1 x USB Port C, 1 x HDMI, and 1 x SD Card Reader, and a battery life of up to 10 hours.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Enhanced Network Infrastructure Security

- 5.1.2 Reduction of Cost and Energy Consumption

- 5.2 Market Challenges

- 5.2.1 Network Issues in Developing Countries for Cloud Computing

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Hardware

- 6.1.2 Software and Services

- 6.2 By End User

- 6.2.1 BFSI

- 6.2.2 IT and Telecom

- 6.2.3 Healthcare

- 6.2.4 Government

- 6.2.5 Other End Users (Retail, Manufacturing, Education)

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Dell Inc.

- 7.1.2 HP Development Company LP

- 7.1.3 Samsung Group

- 7.1.4 LG Electronics Inc.

- 7.1.5 NEC Corporation

- 7.1.6 Fujitsu Ltd

- 7.1.7 Lenovo Group Limited

- 7.1.8 Cisco Systems Inc.

- 7.1.9 Advantech Co. Ltd

- 7.1.10 Siemens AG

- 7.1.11 IGEL Technology GmbH

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

精简型用户端市场:按产品、型号、应用程式和最终用户产业划分 - 2025-2030 年全球预测

精简型用户端市场:按产品、型号、应用程式和最终用户产业划分 - 2025-2030 年全球预测 瘦客户端市场规模、占有率、预测、趋势:按类型、连接类型、最终用户 - 到 2031 年的全球预测

瘦客户端市场规模、占有率、预测、趋势:按类型、连接类型、最终用户 - 到 2031 年的全球预测 2024-2028 年全球精简型用户端市场

2024-2028 年全球精简型用户端市场 全球精简型用户端市场:产业分析、规模、占有率、成长、趋势、预测,2024-2033 年

全球精简型用户端市场:产业分析、规模、占有率、成长、趋势、预测,2024-2033 年 全球瘦客户端市场规模:按硬体类型、部署类型、最终用户产业、地区、范围和预测

全球瘦客户端市场规模:按硬体类型、部署类型、最终用户产业、地区、范围和预测 精简型用户端市场规模、份额、趋势分析报告:按类型、外形尺寸、应用、地区、细分市场预测,2024-2030 年

精简型用户端市场规模、份额、趋势分析报告:按类型、外形尺寸、应用、地区、细分市场预测,2024-2030 年 2024 年精简型用户端全球市场报告

2024 年精简型用户端全球市场报告 全球瘦客户端市场 - 全球产业分析、规模、份额、成长、趋势、预测 (2031) - 按外形尺寸、按应用、按地区

全球瘦客户端市场 - 全球产业分析、规模、份额、成长、趋势、预测 (2031) - 按外形尺寸、按应用、按地区 到 2030 年精简型用户端市场预测:按组件、外形尺寸、应用和地区进行的全球分析

到 2030 年精简型用户端市场预测:按组件、外形尺寸、应用和地区进行的全球分析 全球精简型电脑市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势和预测

全球精简型电脑市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势和预测