|

市场调查报告书

商品编码

1433931

生质能源:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Bioenergy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

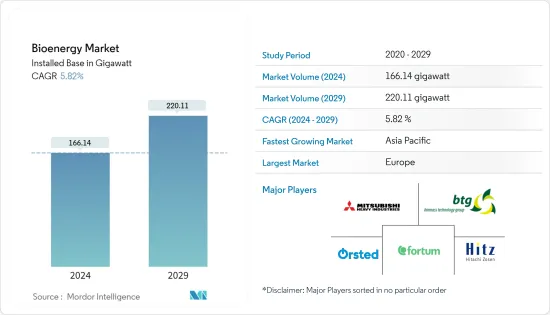

从装置容量来看,生质能源市场规模预计将从2024年的166.14吉瓦成长到2029年的220.11吉瓦,在预测期间(2024-2029年)复合年增长率为5.82%。

主要亮点

- 从中期来看,增加生质能源投资和降低生质能源设施发电成本等因素预计将在预测期内推动市场发展。

- 另一方面,建厂的高额初始投资可能会阻碍市场成长。工厂生产必须充足且一致,以支付安装和营运成本。

- 儘管如此,新兴的废弃物技术,如德国最近在废弃物生物处理方面的创新技术Dendro Liquid Energy(DLE),已接近「零废弃物」技术;在生质能源领域具有巨大潜力。

- 预计欧洲将主导全球市场,大部分需求来自挪威、英国国家。

生质能源市场趋势

生物质预计将主导市场

- 生质能源是来自生物材料的能量,其特征是储存化学能的有机材料,例如木材或肥料。

- 根据国际能源协会统计,现代生质能源是全球最大的再生能源来源,占可再生能源的55%,占全球能源供应的6%以上。现代生质能源的采用呈上升趋势,2010年至2021年平均每年增长约7%。

- 根据国际可再生能源协会预测,2022年全球生质能源装置容量约为148.9吉瓦,较2021年成长5%。

- 生物质供应来自多种原料,包括木材燃料、林业残留物、木炭、颗粒、农作物和残留物、城市和工业废弃物、沼气和生质燃料。供应可大致分为三个主要部门:林业、农业和生质燃料。浪费。

- 2023年6月,印度政府主动推动永续能源实践,电力部宣布修订生物质混烧政策。该修正案将允许发电厂以基准价格购买生物质颗粒燃料,减少进口依赖并促进采用生物质作为再生能源来源。

- 根据美国能源情报署(EIA)2023年6月收集的资料,截至2023年3月,美国緻密生物质燃料总产能达1336万吨,目前所有产能均已运作中或被列为暂停产状态。中止运作。其中东部地区产能196万吨,南部地区产能1051万吨,西部地区产能88.42万吨。

- 因此,随着全球对再生能源来源的需求不断增加,生物质发电预计在预测期内将呈现显着成长。

预计欧洲将主导市场

- 预计生质能源在未来十年仍将发挥重要作用,以实现 2030 年可再生能源目标。因此,欧盟 (EU) 成员国已将生质能源选项纳入其国家可再生能源行动计画 (NREAP)。

- 生物质是一种重要的再生能源来源,也是实现欧洲可再生能源目标(即 2030 年可再生能源在欧盟能源结构中占 45%)的关键要素。

- 2022年,生质能源占欧洲可再生能源装置容量的5.8%。在德国,预计到 2023 年,生质能源将占总装置容量的 6.7%。

- 2023年6月,西班牙能源部宣布计划将其2030年沼气和绿色氢气产量目标增加一倍。修订后的计画设定了2030年电解槽11吉瓦(GW)的目标,将先前的4GW和沼气产量目标提高到20兆瓦时(TWh)。

- 德国是生质能源的重要国家之一,该国正在不断扩大其生质能源产能。 2023年2月,沼气厂设计、建造和营运方面的专家德国BioEnergy获得了BlueHills Capital Projects (Pty)的合同,将在马拉威中部的Nhotakota区建造一座56MWel沼气厂。有限的。沼气厂将使用从周围人工林收穫的纳皮尔草来供应。

- 此外,义大利等国家可能会支持该地区生质能源产业的成长。 2023年6月,Enterra从联合信贷银行获得了3,800万美元的计划融资,用于义大利的一座生物质工厂。这座位于普利亚南部福贾的 13 兆瓦发电厂利用生质能生产电能和热能。

- 因此,即将推出的计划和未来几年实现碳中和环境的目标预计将在预测期内为该地区带来优势。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第二章调查方法

第三章执行摘要

第四章市场概况

- 介绍

- 到 2028 年实际和预测的生质能源装置容量

- 最新趋势和发展

- 政府法规政策

- 市场动态

- 促进因素

- 转向可再生能源

- 利用生质能源降低发电成本

- 抑制因素

- 初始投资高

- 促进因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔

- 类型

- 固体生物质

- 沼气

- 可再生废弃物

- 其他类型

- 科技

- 气化

- 快速热解

- 发酵

- 其他技术

- 按地区分類的市场分析(到 2028 年的市场规模和需求预测(仅按地区))

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 卡达

- 北美洲

第六章 竞争形势

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- Mitsubishi Heavy Industries Ltd

- MVV Energie AG

- A2A SpA

- Hitachi Zosen Corp.

- BTG Biomass Technology Group

- Babcock & Wilcox Volund AS

- Biomass Engineering Ltd

- Orsted AS

- Enerkem

- Fortum Oyj

第七章 市场机会及未来趋势

- 先进的技术

简介目录

Product Code: 67322

The Bioenergy Market size in terms of installed base is expected to grow from 166.14 gigawatt in 2024 to 220.11 gigawatt by 2029, at a CAGR of 5.82% during the forecast period (2024-2029).

Key Highlights

- Over the medium term, factors such as increasing investments in bioenergy, and declining electricity generation costs from bioenergy facilities are expected to drive the market during the forecast period.

- On the other hand, the high initial investment for establishing plants may resist market growth. The plant output must be sufficient and consistent to cover the installation and operating costs.

- Nevertheless, Emerging waste-to-energy technologies, such as Dendro Liquid Energy (DLE), a recent German innovation in the biological treatment of waste, present high potential in the bioenergy field, being close to 'zero-waste' technology.

- Europe is expected to dominate the world's market, with most of the demand coming from countries such as Norway, Germany, and the United Kingdom.

Bioenergy Market Trends

Biomass is Expected to Dominate the Market

- Bioenergy is energy derived from biological materials characterized as organic materials with stored chemical energy like wood and manure.

- According to Internation Energy Association, Modern bioenergy is the largest renewable energy source globally, accounting for 55% of renewable energy and over 6% of the global energy supply. The adoption of modern bioenergy has increased on average by about 7% per year between 2010 and 2021 and is on an upward trend.

- According to the International Renewable Association, in 2022, the global installed capacity for bioenergy accounted for about 148.9 GW, with a 5% increase from 2021.

- Biomass supply comes from various feedstock - wood fuel, forestry residues, charcoal, pellets, agriculture crops and residues, municipal and industrial waste, biogas, biofuels, etc. Broadly, the supply can be classified into three main sectors - forestry, agriculture, and waste.

- In June 2023, the Indian government took the initiative to promote sustainable energy practices, and the Ministry of Power announced the revision of the biomass co-firing policy. This revision will enable power plants to purchase biomass pellets at benchmark prices, reducing import dependencies and enhancing the adoption of biomass as a renewable energy source.

- In June 2023, data gathered by the Energy Information Administration (EIA) showed that the total United States densified biomass fuel capacity reached 13.36 million tons in March 2023, with all of that capacity listed as currently operating or temporarily not in operation. Capacity included 1.96 million tons in the East, 10.51 million in the South, and 884,200 tons in the West.

- Therefore, with the increasing demand for renewable energy sources worldwide, biomass-based electricity generation is expected to witness a significant growth rate during the forecast period.

Europe is Expected to Dominate the Market

- Bioenergy is expected to remain crucial over the next decade to reach renewable energy targets in 2030. Hence, the European Union (EU) member states incorporated the bioenergy option in their National Renewable Energy Action Plans (NREAPs).

- Biomass is an essential renewable energy source and is a key factor in reaching the European renewable energy target by 2030, where the target for the share of renewables in the EU energy mix to 45% by 2030

- Bioenergy contributed to 5.8% of the total renewable energy installed capacity in Europe in 2022. Germany is expected to have 6.7% of its total installed capacity from bioenergy in 2023.

- In June 2023, the Energy Ministry of Spain announced plans to double its 2030 biogas and green hydrogen production targets. The revised plan sets a 2030 target of 11 gigawatts (GW) of electrolyzers, up from a previous target of 4 GW and biogas production to 20 terawatt hours (TWh).

- Germany is one of the crucial players in bioenergy, and the country is constantly expanding its bioenergy capacity. In February 2023, BioEnergy Germany company, which specializes in the design, construction, and operation of biogas plants, secured a contract for the construction of a 56 MWel biogas plant in Nkhotakota District in the Central Region of Malawi by BlueHills Capital Projects (Pty) Limited. The biogas plant will be fed with Napier grass from the surrounding plantations.

- Further, countries like Italy are likely to support the region's growth in the bioenergy sector. In June 2023, Enterra secured USD 38 million in project financing from UniCredit for a biomass plant in Italy. Located in Foggia in the southern region of Apulia, the 13 MW plant produces electric and thermal energy from biomass.

- Hence, with the upcoming projects and the targets to achieve a carbon-neutral environment during the upcoming years, the region is expected to have dominancy during the forecast period.

Bioenergy Industry Overview

The bioenergy market is semi fragmented. Some of the major players in the market (in no particular order) include Mitsubishi Heavy Industries Ltd, Hitachi Zosen Corp., BTG Biomass Technology Group, Babcock & Wilcox Volund AS, Biomass Engineering Ltd., and Orsted AS.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Bioenergy Installed Capacity Historic and Forecast, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Shift towards Renewable Energy

- 4.5.1.2 Less Electricity Generation Cost from Bioenergy

- 4.5.2 Restraints

- 4.5.2.1 High Initial Investments

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Solid Biomass

- 5.1.2 Biogas

- 5.1.3 Renewable Waste

- 5.1.4 Other Types

- 5.2 Technology

- 5.2.1 Gasification

- 5.2.2 Fast Pyrolysis

- 5.2.3 Fermentation

- 5.2.4 Other Technologies

- 5.3 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Chile

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Qatar

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Mitsubishi Heavy Industries Ltd

- 6.3.2 MVV Energie AG

- 6.3.3 A2A SpA

- 6.3.4 Hitachi Zosen Corp.

- 6.3.5 BTG Biomass Technology Group

- 6.3.6 Babcock & Wilcox Volund AS

- 6.3.7 Biomass Engineering Ltd

- 6.3.8 Orsted AS

- 6.3.9 Enerkem

- 6.3.10 Fortum Oyj

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advanced Technologies