|

市场调查报告书

商品编码

1433936

感知无线电市场占有率分析、产业趋势与统计、成长预测(2024-2029)Cognitive Radio - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

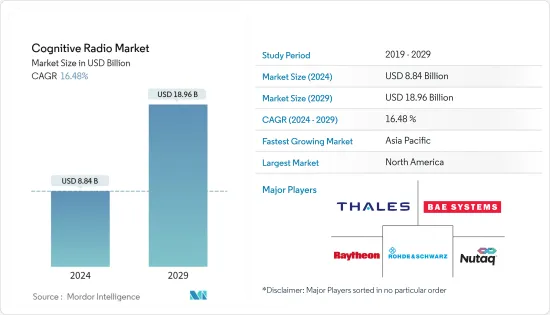

感知无线电市场规模预计在2024年为88.4亿美元,预计到2029年将达到189.6亿美元,在预测期内(2024-2029年)复合年增长率为16.48%。

新的5G技术将用于应对未来无线技术带来的大量行动资料流量。更多容量将需要更多频谱,从而将 CR 整合到 5G 网路中。 CR 的重点是更有效地利用频谱,同时适应提供最佳的通讯频道。

主要亮点

- 当今世界,经济和通讯基础设施紧密相互依存。感知无线电将透过多种方式提高频谱效率,使行动通讯范式更加个人化。 CR 识别频谱中的空閒通道,并透过动态改变传输参数将它们用于通讯。提高了通路资源的有效利用。

- 要在现实场景中实施该技术,必须克服几个技术障碍。感知无线电需要灵敏地区分衰退的主讯号和閒置频段讯号。在严重衰退的情况下,具有本地感测功能的单一感知无线电可能无法实现这种更高的灵敏度,因为所需的感测时间可能比感测週期长。

- 在 COVID-19感染疾病期间和之后,许多日常业务变得越来越依赖网路。网路流量的显着变化增加了对更多频率的频谱的需求,从而创造了对感知无线电市场的需求。

- 农村宽频通讯业者广泛使用感知无线电将有助于独立的农村通讯业者避免在未开发的农村市场部署无线电的高成本和有限的频谱问题,这将增加无线电在公共方面的使用。

感知无线电市场趋势

随着5G应用的到来,通讯领域蓄势待发

- 大多数无线通讯系统基于固定频率分配,导致频谱利用率较低。工业应用、联网汽车和其他 IT 支援的应用对物联网的需求不断增长,加速了对更多频谱的需求。因此,感知无线电在这里发挥关键作用,因为它会自动侦测无线电频谱内的可用频道,并允许同时进行更多通讯,而不会打扰授权使用者。

- 根据GSMA统计,截至2022年11月底,已有87个国家超过225家业通讯业者推出5G服务。到年终,5G行动连线数预计将达到15亿。这种成长将需要不同频宽的额外频谱资源。

- 为了提升大容量情境下的动态使用者体验,中兴通讯与中国电信共同开发了基于中兴通讯Radio Composer的自适应时空认知网路。网路方案分析不同时间内流量空间的分布趋势。

爱立信和 AXIAN Telecom 宣布建立合作伙伴关係,在马达加斯加提供更快、更可靠的行动服务,同时降低网路能耗并加强 5G 生态系统。透过此次合作,AXIAN 旨在加速马达加斯加和坦尚尼亚的数位化,增加网路容量并为客户提供更快的速度。

亚太地区在预测期内成长最快

- 亚太地区国家处于 5G 行动技术的前沿。第一个商用5G网路已在韩国推出。儘管5G技术的建立还需要时间,但预计到2025年连线数将达到18亿。

- 700 MHz频宽,特别是 3500 MHz 频段,是目前 5G 的建议频率,应尽可能成为奖项的主要关注点。 3500 MHz 内的确切频谱范围因国家而异。可能需要进行广泛的重组工作,以最大限度地提高可用频宽,同时确保行动电话营运商能够获得无干扰的频谱。

- Nokia、Docomo 和 NTT 正在合作开发新的 6G 技术。三人预计将致力于开发新的频谱技术、感测器网路以及专门的认知和自动化架构。

- 日本内务部(MIC)将推出频谱竞标,其中包括毫米波(mmWave)频谱。该频谱预计将用于固定无线接入,以增加体育场和其他大型场馆的覆盖范围,并在住宅提供宽频。

感知无线电产业概述

该市场竞争适度,满足需求的参与者较少。这些感知无线电提供者正在与多家公司签约并对其进行投资,以帮助他们扩展服务。随着对快速、稳定的网路连接的需求的增加,增强型感知无线电解决方案的发展将进一步扩展网路连接的范围。服务于该领域的主要企业包括 BAE Systems PLC、Thales Group、Raytheon Company 和 Rohde &Schwarz GmbH &Co. KG。

2022 年 10 月,STC 采用爱立信技术,确保在网路高流量高峰期间提供主动支援并改善客户体验。基于人工智慧的认知软体解决方案利用自动化、巨量资料扩充性、速度、准确性和一致性来改善网路优化。该解决方案预计将有助于减少虚拟路测和远端自动频谱分析等营运活动中的碳排放。

2022年6月,印度理工学院Mandi开发了一款协作频谱感测器,提供尖端的通讯解决方案并提高射频频谱的再生性。该解决方案的想法是,次要用户使用的行动电话等无线设备可以安装自己的传感器,可以检测主要用户未使用的频谱空洞,并可以在主信道不可用时使用.就是这个意思。或者拥挤。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 市场驱动因素

- 优化频谱利用率的需求日益增加

- 加大终端产业5G服务应用开发力度

- 市场限制因素

- 缺乏足够的运算安全基础设施

- 产业吸引力-波特五力分析

- 买家/消费者的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 产业价值链分析

- 评估 COVID-19 对产业的影响

第五章市场区隔

- 按用途

- 频谱感知和分配

- 位置侦测

- 认知路由

- QoS(服务品质)最佳化

- 其他用途

- 按服务

- 专业服务

- 管理服务

- 按最终用户产业

- 通讯业

- IT和IT公司

- 政府/国防

- 运输

- 其他最终用户产业

- 地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 韩国

- 其他亚太地区

- 拉丁美洲

- 中东/非洲

- 北美洲

第六章 竞争形势

- 公司简介

- BAE Systems PLC

- Thales Group

- Raytheon Company

- Innovation Nutaq Inc.(NuRAN Wireless Inc.)

- Shared Spectrum Company

- Rohde & Schwarz GmbH & Co KG

- Spectrum Signal Processing(Vecima)

- Rockwell Collins Inc.(United Technologies Company)

第七章 投资分析

第八章 市场机会及未来趋势

The Cognitive Radio Market size is estimated at USD 8.84 billion in 2024, and is expected to reach USD 18.96 billion by 2029, growing at a CAGR of 16.48% during the forecast period (2024-2029).

The emerging 5G technologies are used to meet future wireless technologies' heavy mobile data traffic. More capacity will demand more spectrum, resulting in the integration of CR in 5G networks. The focus of CR is to enable much more efficient use of the spectrum, though it adapts itself to provide the optimum communications channel.

Key Highlights

- In today's world, the economy and communication infrastructure closely depend on each other. With improved spectrum utilization efficiency in numerous dimensions, cognitive radio will make the mobile communication paradigm more personal. CR identifies the free channels in the spectrum and uses them for communication by dynamically changing the transmission parameters, leading to better utilization of channel resources.

- Some technical hurdles must be overcome before the technology can be implemented in a real-world scenario. To differentiate between a primary signal that is fading and white space, cognitive radios must be more sensitive. A single cognitive radio using local sensing may not be able to achieve this improved sensitivity in cases of severe fading since the necessary sensing time may be longer than the sensing period.

- There was an increased reliance on the internet for numerous daily tasks during and after the COVID-19 pandemic. The heavy shift towards network traffic urged the need for more spectrums with multiple frequencies, which created a demand for the cognitive radio market.

- The extensive usage of cognitive radio by rural broadband telcos helps independent local carriers get around the issue of high costs and limited spectrum to deploy wireless in underdeveloped rural markets, thereby increasing its use for public safety.

Cognitive Radio Market Trends

Telecommunication Sector is Gaining Traction Due to Emergence of 5G Applications

- As most wireless communication systems are based on fixed frequency allocation, this results in low spectrum utilization. The growing demand for IoT for industrial use, connected vehicles, and other IT-enabled applications is accelerating the need for more spectrums. Cognitive radio hence plays an important role here as it automatically detects available channels in a wireless spectrum, enabling more communication to run concurrently without obstructing the licensed users.

- According to the GSMA, at the end of November 2022, more than 225 operators from 87 countries launched 5G services. By the end of 2023, the number of 5G mobile connections is expected to reach 1.5 billion. This growth will require additional spectrum resources in different frequency bands.

- To enhance dynamic user experiences in high-capacity scenarios, ZTE Corporation and China Telecom jointly developed a self-adaptive spatiotemporal cognitive network based on ZTE's Radio Composer. The network solution analyzes the traffic space distribution trend in different periods.

Ericsson and AXIAN Telecom announced a partnership to provide faster and more reliable mobile services throughout Madagascar while reducing network energy consumption and enhancing the 5G ecosystem. Through this partnership, AXIAN aims to boost digitalization across Madagascar and Tanzania, increasing network capacities and providing enhanced speeds to its customers.

Asia-Pacific to Register the Fastest Growth During the Forecast Period

- Countries in the Asia-Pacific region have been at the forefront of 5G mobile technologies. The first commercial 5G network was launched in South Korea. Though establishing 5G technology will take time, it is expected that it will reach 1.8 billion connections by 2025.

- The 700 MHz bands, particularly the 3500 MHz range, are the currently preferred frequencies for 5G and should be the primary focus for awards wherever feasible. The precise range of spectrum within 3500 MHz varies by country. There may be a need for extensive refarming work to ensure that mobile operators have access to a spectrum that does not suffer from interference while maximizing the bandwidth available.

- Nokia, Docomo, and NTT have partnered on emerging 6G technologies. The trio is projected to work to develop new spectrum technologies, a network as a sensor, and cognitive, automated, and specialized architectures.

- Japan's Ministry of Internal Affairs and Communications (MIC) will introduce a spectrum auction, including a millimeter-wave (mmWave) spectrum. The spectrum is expected to be used for fixed wireless access to increase coverage in stadiums and other extensive facilities and deliver broadband in residential areas.

Cognitive Radio Industry Overview

A few players meet the demand, this market has moderate competition. These cognitive radio providers sign contracts and invest with various companies to help expand their services. As the demand for fast and stable network connections increases, they have a broader scope of expansion with the development of enhanced cognitive radio solutions. Some significant companies offering services in this sector include BAE Systems PLC, Thales Group, Raytheon Company, and Rohde & Schwarz GmbH & Co. KG.

In October 2022, STC adopted Ericsson's technologies to ensure proactive support and elevate customer experiences during surges in high traffic on the network. The AI-based Cognitive Software solution leverages automation, big data scalability, speed, accuracy, and consistency for improved network optimization. The solution was expected to contribute to reducing carbon dioxide emissions from operational activities like the use of virtual drive testing and remote automatic spectrum analysis.

In June 2022, the Indian Institute of Technology, Mandi, developed cooperative spectrum sensors to offer cutting-edge telecom solutions and improve the radio-frequency spectrum's reusability. The idea of this solution was that a wireless device, such as a cell phone, used by the secondary user could be fitted with a unique sensor that could detect spectrum holes that the primary user does not use and use them when the main channel is unavailable or crowded.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Need to Optimise the Spectrum Utilisation

- 4.2.2 Rising Development of 5G Service Applications Among End-user Industries

- 4.3 Market Restraints

- 4.3.1 Lack of Proper Computational Security Infrastructure

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Industry Value Chain Analysis

- 4.6 Assessment of COVID-19 impact on the industry

5 MARKET SEGMENTATION

- 5.1 By Application

- 5.1.1 Spectrum Sensing & Allocation

- 5.1.2 Location Detection

- 5.1.3 Cognitive Routing

- 5.1.4 QoS (Quality of Service) Optimisation

- 5.1.5 Other Applications

- 5.2 By Service

- 5.2.1 Professional Services

- 5.2.2 Managed Services

- 5.3 By End-user Industry

- 5.3.1 Telecommunication

- 5.3.2 IT & ITes

- 5.3.3 Government & Defense

- 5.3.4 Transportation

- 5.3.5 Other End-user Industries

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 South Korea

- 5.4.3.4 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.5 Middle East & Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 BAE Systems PLC

- 6.1.2 Thales Group

- 6.1.3 Raytheon Company

- 6.1.4 Innovation Nutaq Inc. (NuRAN Wireless Inc.)

- 6.1.5 Shared Spectrum Company

- 6.1.6 Rohde & Schwarz GmbH & Co KG

- 6.1.7 Spectrum Signal Processing (Vecima)

- 6.1.8 Rockwell Collins Inc. (United Technologies Company)

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

感知无线电市场:按组件、应用和最终用户划分 - 2025-2030 年全球预测

感知无线电市场:按组件、应用和最终用户划分 - 2025-2030 年全球预测 感知无线电市场规模、份额、趋势分析报告:2025-2030 年按组件、应用、最终用途、地区和细分市场进行的预测

感知无线电市场规模、份额、趋势分析报告:2025-2030 年按组件、应用、最终用途、地区和细分市场进行的预测 到 2030 年感知无线电市场预测:按组件、应用、最终用户和地区进行的全球分析

到 2030 年感知无线电市场预测:按组件、应用、最终用户和地区进行的全球分析 全球认知无线电市场规模、份额、成长分析,按组件(硬体、软体)、按应用(认知路由、位置追踪)、按最终用途(电信、政府和国防)- 2024-2031 年产业预测

全球认知无线电市场规模、份额、成长分析,按组件(硬体、软体)、按应用(认知路由、位置追踪)、按最终用途(电信、政府和国防)- 2024-2031 年产业预测 认知无线市场、份额、市场规模、趋势、行业分析报告:按组件、按应用、按最终用途、按地区、按细分市场、预测,2024-2032年

认知无线市场、份额、市场规模、趋势、行业分析报告:按组件、按应用、按最终用途、按地区、按细分市场、预测,2024-2032年 全球认知无线电市场报告

全球认知无线电市场报告 认知无线电市场:按组件、应用和最终用户划分 - 2023-2030 年全球预测

认知无线电市场:按组件、应用和最终用户划分 - 2023-2030 年全球预测 感知无线电的全球市场

感知无线电的全球市场