|

市场调查报告书

商品编码

1435203

光伏玻璃:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Solar Photovoltaic Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

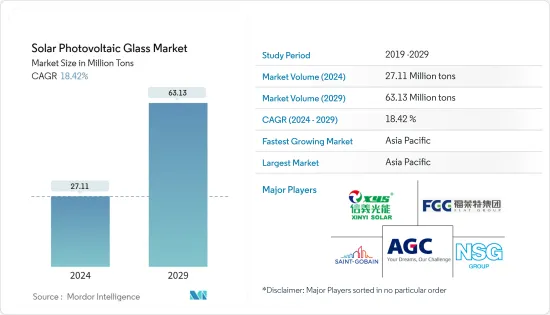

预计2024年太阳能玻璃市场规模为1528万吨,预计2029年将达到3003万吨,在预测期内(2024-2029年)复合年增长率为14.47%增长。

冠状病毒感染疾病(COVID-19) 的爆发对多个行业产生了短期和长期影响,包括影响太阳能玻璃市场的製造业和建设业。该行业受到供应链中断和化学品製造公司停产的广泛影响。这是因为封锁和劳动力短缺对市场产生了不利影响。

主要亮点

- 推动太阳能玻璃市场的主要因素是非住宅领域需求的增加和政府补贴计画的增加。

- 太阳能玻璃安装和维护的高资本成本预计将阻碍所研究市场的成长。

- 为了减少空气污染而对生产绿色电力的需求不断增长,为太阳能玻璃市场的成长提供了各种机会。

- 亚太地区主导太阳能玻璃市场,其中中国、日本和印度是主要消费国。

光伏(PV)玻璃市场趋势

非住宅领域的需求增加

- 太阳能玻璃是一种将光能转换为电能的技术。这种玻璃采用透明半导体光伏电池,也称为太阳能电池。这些电池夹在两块玻璃之间,使它们能够捕捉阳光并将其转换为电能。

- 太阳能电池产生的电力可减少碳排放和温室气体排放,并确保节省能源成本。这些产品之间的太阳能效率和光传输方面的差异为建筑设计提供了多种选择。

- 光伏玻璃可以轻鬆整合到建筑物和屋顶系统中,从而可以透过创造性的建筑设计经济地利用太阳能并产生可再生能源。

- 此外,由于印度工业活动的活性化,工业电力需求预计将增加。因此,屋顶太阳能光电安装成为企业自力更生的强力选择,印度屋顶太阳能光电市场可望扩大。例如,2022年第四季(Q4),印度屋顶太阳能装机量较上季成长近51%,从320兆瓦增加到483兆瓦。这相当于与前一年同期比较增长 20%。工业部门约占年内总装置量的42%。因此,屋顶太阳能光电装置的增加预计将为太阳能光电玻璃市场创造上行需求。

- 印度政府宣布投资 31.65 兆美元,根据智慧城市计画建造 100 个城市。 100个智慧城市和500个城市有潜力吸引价值2兆卢比(约281.8亿美元)的投资。该专案预计将于2019年至2023年完成,为光伏玻璃在非住宅领域的应用创造空间。

- 非住宅领域引领着光伏电池的使用,其中中国、英国、美国、印度、日本和马来西亚在光伏玻璃市场中发挥重要作用。

- 由于所有这些因素,太阳能玻璃市场预计在预测期内稳定成长。

亚太地区主导市场

- 预计亚太地区将主导太阳能玻璃市场。在中国、印度和日本等新兴国家,电力供应危机正在扩大该地区使用太阳能玻璃的内部发电范围。

- 最大的太阳能玻璃生产商位于亚太地区。太阳能玻璃製造领域的领先公司包括晶科太阳能、三菱电机公司、Onyx Solar Group LLC、晶澳太阳能和Infini。

- 根据国际可再生能源机构(IRENA)预测,2022年印度太阳能发电容量将达到62.8吉瓦以上,较2021年成长21.5%。因此,由于太阳能发电容量的增加,预计太阳能发电的需求将会增加。国内太阳能发电玻璃市场。

- 太阳能电池产生的电力可减少碳排放和温室气体排放,并确保节省能源成本。

- 此外,日本正在寻求透过努力减少核能在其能源结构中的份额来扩大装置容量,目标是到2030年将装置容量增加到近108吉瓦。然而,在这些领域中,由于住宅太阳能普及较高,地面安装领域预计将以最快的速度增长,从而为大型公用事业规模计划创造了对大型中央逆变器的需求。我是。

- 中国是全球最大的太阳能玻璃生产国。 2022年7月,中国工业与资讯化部透露,截至6月底,全国太阳能玻璃产能达到6.4万吨/日,涵盖38家企业的348条生产线。目前已运作生产线313条,总合5.9万吨。

- 上述因素和政府支持正在推动预测期内太阳能光电玻璃市场需求的增加。

光伏玻璃产业概况

太阳能玻璃市场本质上是整合的。该市场的主要企业(排名不分先后)包括信义光能控股有限公司、福莱特玻璃集团有限公司。株式会社、AGC株式会社、日本板硝子株式会社、圣戈班、入子集团新能源株式会社等

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 非住宅领域的需求增加

- 增加政府补贴制度

- 其他司机

- 抑制因素

- 安装和维护资本成本高

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(以金额为准的市场规模)

- 类型

- 薄膜硅玻璃

- 碲化镉薄膜玻璃

- 结晶太阳能电池玻璃

- 非晶质玻璃

- 其他类型

- 目的

- 住宅

- 非住宅

- 商业的

- 工业/设施

- 其他用途

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲

- 亚太地区

第六章 竞争形势

- 併购、合资、联盟、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Canadian Solar

- INFINI Co. Ltd

- JA SOLAR Technology Co.,Ltd.

- Jinko Solar

- KANEKA CORPORATION

- KYOCERA Corporation

- Mitsubishi Electric Corporation

- Onyx Solar Group LLC.

- SunPower Corporation

- Trina Solar

第七章 市场机会及未来趋势

- 绿色电力生产需求不断成长

- 一种采用薄膜技术的新型太阳能电池技术现已上市,该技术在太阳能电池上使用了窄的碲化镉涂层。

The Solar Photovoltaic Glass Market size is estimated at 15.28 Million tons in 2024, and is expected to reach 30.03 Million tons by 2029, growing at a CAGR of 14.47% during the forecast period (2024-2029).

The COVID-19 outbreak brought several short-term and long-term consequences in various industries, such as manufacturing and construction affecting the solar photovoltaic glass market. The industry was widely impacted due to supply chain disruption and a halt in the production of chemical manufacturing companies. It is due to lockdown and workforce shortages, thus, adversely affecting the market.

Key Highlights

- Major factors driving the solar photovoltaic glass market are increasing the demand from non-residential sector and increasing number of subsidy schemes from government.

- High capital costs for installation and maintenance of photovoltaic glass is expected to hinder the growth of the market studied.

- The growing demand for producing green electricity to reduce air pollution is offering various opportunities for the growth of solar photovoltaic glass market.

- Asia-Pacific region dominated the market for solar photovoltaic glass with China, Japan, and India representing major countries for consumption.

Solar Photovoltaic (PV) Glass Market Trends

Increasing Demand from Non-Residential Sector

- Solar photovoltaic glass is a technology that enables the conversion of light into electricity. The glass is incorporated with transparent semiconductor-based photovoltaic cells, which are also known as solar cells. These cells are sandwiched between two sheets of glass, which enables them to capture these solar rays and convert them into electricity.

- The power generated from solar photovoltaic cells reduces carbon footprints and greenhouse gas emissions and also ensures energy cost savings. Variance in photovoltaic efficiency and light penetration among these products enables multiple options for architectural design.

- Solar photovoltaic glass can be easily integrated into buildings and rooftop systems, thereby creating renewable energy through the economical use of solar energy and creative architectural design.

- Moreover, due to the rise of industrial activity in India, industry power demand will increase. As a result, rooftop solar installations would provide a robust option for enterprises to become self-reliant, which is expected to increase the rooftop solar market in India. For instance, in the fourth quarter (Q4) of 2022, India's rooftop solar installations increased by almost 51% quarter-over-quarter, adding 483 MW compared to 320 MW. This represents a year-on-year growth of 20%. The industrial sector accounted for approximately 42% of all installations during the year. Therefore, increasing rooftop solar installations is expected to create an upside demand for the solar photovoltaic glass market.

- The Indian government has announced an investment worth USD 31,650 billion for the construction of 100 cities under the smart cities plan. 100 smart cities and 500 cities are likely to invite investments worth INR 2 trillion (~USD 28.18 billion). This is expected to complete between 2019 and 2023, creating scope for the application of solar photovoltaic glass in the non-residential sector.

- Non-residential sector leads in the utilization of solar photovoltaic cells, with China, the United Kingdom, the United States, India, Japan, and Malaysia playing a major role in the solar photovoltaic glass market.

- Due to all such factors, the market for solar photovoltaic glass is expected to have steady growth during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region is expected to dominate the market for solar photovoltaic glass market. In developing countries, such as China, India, and Japan, the crisis in the supply of electricity has resulted in increasing the scope for the self-production of electricity using solar photovoltaic glass in the region.

- The largest producers of solar photovoltaic glasses are located in the Asia-Pacific region. Some of the leading companies in the production of solar photovoltaic glasses are Jinko Solar, Mitsubishi Electric Corporation, Onyx Solar Group LLC, JA Solar Co. Ltd, and Infini Co. Ltd.

- According to the International Renewable Energy Agency (IRENA), solar photovoltaic energy capacity in India reached over 62.8 gigawatts in 2022, a 21.5% increase over 2021. As a result, an increase in the capacity of solar photovoltaic energy is expected to boost the solar photovoltaic glass market in the country.

- The power generated from solar photovoltaic cells reduces carbon footprints and greenhouse gas emissions and also ensures energy cost savings.

- Moreover, Japan is trying to expand its installed solar capacity due to efforts to reduce the share of nuclear in their energy mix and aims to expand installed solar capacity to nearly 108 GW by 2030. However, due to the high solar penetration rate in the residential sector, the ground-mounted segment is expected to grow at the fastest pace, creating a demand for larger, central inverters for large utility-scale projects.

- China is the world's largest solar PV glass manufacturer. In July 2022, China's Ministry of Industry and Information Technology revealed that the country's solar glass capacity reached 64,000 metric tons (MT) per day across 348 production lines from 38 companies at the end of June. Currently, 313 production lines with a combined capacity of 59,000 MT are operational.

- The aforementioned factors, coupled with government support, are contributing to the increasing demand for the solar photovoltaic glass market during the forecast period.

Solar Photovoltaic (PV) Glass Industry Overview

The solar photovoltaic glass market is consolidated in nature. The major players in this market (not in a particular order) include Xinyi Solar Holdings Limited, Flat Glass GroupCo. Ltd., AGC Inc., Nippon Sheet Glass Co. Ltd., Saint-Gobain, and Irico Group New Energy Company Limited among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Non-residential Sector

- 4.1.2 Increasing Number of Subsidy Schemes from Government

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Capital Costs for Installation and Maintenance

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Thin Film Silicon Glass

- 5.1.2 Cadmium Telluride Thin Film Glass

- 5.1.3 Crystalline Solar Glass

- 5.1.4 Amorphous Silicon Solar Glass

- 5.1.5 Other Types

- 5.2 Application

- 5.2.1 Residential

- 5.2.2 Non-residential

- 5.2.2.1 Commercial

- 5.2.2.2 Industrial/Institutional

- 5.2.2.3 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Canadian Solar

- 6.4.2 INFINI Co. Ltd

- 6.4.3 JA SOLAR Technology Co.,Ltd.

- 6.4.4 Jinko Solar

- 6.4.5 KANEKA CORPORATION

- 6.4.6 KYOCERA Corporation

- 6.4.7 Mitsubishi Electric Corporation

- 6.4.8 Onyx Solar Group LLC.

- 6.4.9 SunPower Corporation

- 6.4.10 Trina Solar

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for Producing Green Electricity

- 7.2 New Models Of Solar Cells Made of Thin Film Technology that use Narrow Coatings of Cadmium Telluride in Solar Cells, which have Higher Efficiency and Lower Cost

2024-2032 年按类型、模组、最终用途产业和地区分類的太阳能光伏玻璃市场报告

2024-2032 年按类型、模组、最终用途产业和地区分類的太阳能光伏玻璃市场报告 全球光伏玻璃市场规模、份额、成长分析(按类型、最终用途)- 产业预测,2024-2031 年

全球光伏玻璃市场规模、份额、成长分析(按类型、最终用途)- 产业预测,2024-2031 年 全球太阳能发电玻璃市场(~2028年):按类型(AR涂层、增强型、TCO涂层)、应用、最终用户(硅晶型光伏组件、薄膜组件、钙钛矿组件)、安装技术和地区

全球太阳能发电玻璃市场(~2028年):按类型(AR涂层、增强型、TCO涂层)、应用、最终用户(硅晶型光伏组件、薄膜组件、钙钛矿组件)、安装技术和地区 光伏玻璃市场、份额、市场规模、趋势、行业分析报告:按类型、按安装、按最终用途、按地区、按细分市场、预测,2023-2032年

光伏玻璃市场、份额、市场规模、趋势、行业分析报告:按类型、按安装、按最终用途、按地区、按细分市场、预测,2023-2032年 全球太阳能发电用钢化玻璃市场的思考与预测(至2029年)

全球太阳能发电用钢化玻璃市场的思考与预测(至2029年) 全球太阳能光电玻璃市场研究报告 - 2023 年至 2030 年产业分析、规模、份额、成长、趋势和预测

全球太阳能光电玻璃市场研究报告 - 2023 年至 2030 年产业分析、规模、份额、成长、趋势和预测 2030年光伏玻璃市场预测:按产品类型、组件、结构、透明度、安装技术、用途和地区进行的全球分析

2030年光伏玻璃市场预测:按产品类型、组件、结构、透明度、安装技术、用途和地区进行的全球分析 光伏玻璃市场:按类型、用途和最终用户划分 - 2023-2030 年全球预测

光伏玻璃市场:按类型、用途和最终用户划分 - 2023-2030 年全球预测 2022-2029年全球太阳能光伏玻璃市场规模研究与预测,按类型(抗反射镀膜玻璃、钢化玻璃、TCO玻璃、其他),按终端用户行业(住宅、商业、公用事业规模)和区域分析

2022-2029年全球太阳能光伏玻璃市场规模研究与预测,按类型(抗反射镀膜玻璃、钢化玻璃、TCO玻璃、其他),按终端用户行业(住宅、商业、公用事业规模)和区域分析 太阳能电池用玻璃的全球市场

太阳能电池用玻璃的全球市场