|

市场调查报告书

商品编码

1435205

橡胶添加剂:市场占有率分析、产业趋势、成长预测(2024-2029)Rubber Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

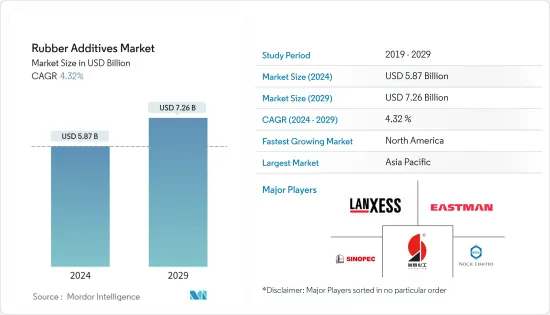

橡胶添加剂市场规模预计到 2024 年为 58.7 亿美元,预计到 2029 年将达到 72.6 亿美元,在预测期内(2024-2029 年)增长 4.32%。复合年增长率为

由于汽车製造和供应链陷入停滞,COVID-19感染疾病影响了橡胶添加剂市场。世界各地实施封锁导致运输延误并扰乱进出口活动。不过,随着限制措施逐步解除,该产业已恢復良好。电动车销量的成长和电子设备需求的扩大推动了过去两年市场的復苏。

主要亮点

- 橡胶和轮胎行业的成长以及建设产业非轮胎行业需求的增加是推动所研究市场需求的关键因素。

- 另一方面,与其处置相关的环境问题预计将阻碍市场成长。

- 开发新的添加剂来生产高性能橡胶,提高最终产品的耐用性可能是未来的机会。

- 亚太地区主导着橡胶添加剂市场,其中印度、中国和日本推动了消费。

橡胶助剂市场趋势

主导市场的轮胎细分市场

- 研究期间,轮胎产业占据橡胶助剂市场的最大份额。天然橡胶主要与顺丁橡胶、苯乙烯-丁二烯橡胶等合成橡胶配合用于製造轮胎。

- 由于高品质轮胎製造技术的进步,轮胎市场持续成长。设备自动化和巨量资料的广泛采用正在推动市场成长。此外,为了生产经济高效且高品质的轮胎,一些製造商使用自动化的一步式轮胎製造流程。

- 根据美国轮胎製造商协会 (USTMA) 的数据,2021 年美国轮胎总出货量为 3.352 亿条,而 2022 年为 3.421 亿条。

- 中国是全球最大的轮胎生产国和消费国。我国有各领域大、中、小型轮胎生产企业300多家。中国的轮胎工业无论金额或产量均位居世界第一。根据中国橡胶工业协会轮胎产业统计,2021年排名前38的会员企业总合生产轮胎5,2922万条,与前一年同期比较成长11.28%。

- 此外,法国领先轮胎製造商米其林表示,自2022年起,卡车和客车轮胎市场的新车装备持续表现良好,欧洲和北美订单饱和。在北美,由于新排放气体标准预计将于 2024 年生效,汽车轮胎的购买量支撑了需求。

- 考虑到上述所有事实和因素,预计在预测期内轮胎应用中橡胶添加剂的使用和需求将会增加。

亚太地区主导市场

- 预计亚太地区将在整个预测期内占据主导地位。随着中国、印度和韩国等国家加速在汽车应用中的使用以及增加其在电气和电子应用中的使用,该地区橡胶添加剂的消费量将会增加。我是。

- 橡胶助剂广泛应用于橡胶及相关製品的加工。汽车产业轮胎製造对橡胶的需求不断增长,推动了橡胶添加剂市场的发展。国内汽车工业的復苏和其他橡胶工业的恢復预计将在不久的将来推动所研究的市场。

- 中国是世界上最大的天然橡胶消费国,占全球消费量的37%,但缺乏合适的土地,只能生产国内所需量的一小部分。因此,中国政府开始鼓励中国企业投资橡胶生产。因此,它有潜力成为该国的橡胶添加剂,因为它可用于天然橡胶和合成橡胶的加工。

- 自2005年以来,中国已成为全球最大的轮胎生产国和消费国。儘管轮胎生产和消费经历了非常健康的成长,但近年来,特别是近两年,轮胎市场对于在该国经营的国内外企业来说非常艰难。然而,随着汽车生产和各种最终用户产业中橡胶添加剂的使用不断扩大,预计预测期内的消费量将增加。

- 国际汽车製造组织(OICA)的数据显示,儘管全球经济不确定性,但中国汽车产量2021年成长7%,2022年成长3%。

- 此外,该协会表示,印度、澳洲和韩国的汽车产量到2022年将分别成长24%、13%和9%。

- 国家统计局数据显示,2022年我国电子资讯製造业稳定成长,生产、投资均呈现强劲扩张态势。根据工业信部统计,同期,规模以上付加与前一年同期比较% ,成长率高于全部工业4个百分点。这增加了电线的使用。

- 印度的电子工业是世界上成长最快的工业之一。近日,电子和资讯技术部发布了印度电子製造业愿景文件第二卷,指出电子製造业预计到2025-26年将达到3000亿美元。

- 所有上述因素都可能推动亚太地区橡胶添加剂市场在预测期内的成长。

橡胶助剂产业概况

全球橡胶助剂市场本质上是部分一体化的,前五家企业占了市场总量的40%以上。领先的公司也专注于研发活动,为产品开发开发创新技术,进行併购以增加市场占有率,并提高其在市场上的有效性和专业化程度。我们正在优化我们的供应链。研究市场的主要企业包括中国三信化学控股有限公司、莱茵化学(朗盛)、酵母化学公司、中国石油化学股份有限公司(中石化)、NOCIL LIMITED等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 轮胎橡胶工业的成长

- 建设产业对非轮胎领域的需求不断扩大

- 其他司机

- 抑制因素

- 橡胶助剂的环境限制

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 买方议价能力

- 供应商的议价能力

- 替代品的威胁

- 新进入者的威胁

- 竞争程度

第五章市场区隔(以金额为准的市场规模)

- 类型

- 活化剂

- 硫化抑制剂

- 塑化剂

- 其他类型

- 目的

- 胎

- 输送带

- 电缆

- 其他用途

- 填料

- 碳黑

- 碳酸钙

- 二氧化硅

- 其他填料

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲

- 亚太地区

第六章 竞争形势

- 併购、合资、联盟、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- BASF SE

- Behn Meyer

- China Petrochemical Corporation(SINOPEC)

- China Sunsine Chemical Holdings Limited

- Eastman Chemical Company

- Emery Oleochemicals

- Kemai Chemical Co. Ltd

- MLPC International(Arkema Group)

- NOCIL LIMITED

- PUKHRAJ ZINCOLET

- Rhein Chemie(Lanxess)

- Sumitomo Chemical Co. Ltd

- Thomas Swan & Co. Ltd

第七章 市场机会及未来趋势

- 电动车需求增加

- 生物基橡胶助剂的开发

The Rubber Additives Market size is estimated at USD 5.87 billion in 2024, and is expected to reach USD 7.26 billion by 2029, growing at a CAGR of 4.32% during the forecast period (2024-2029).

The COVID-19 pandemic affected the rubber additives market as automotive manufacturing and supply chains were halted. The introduction of lockdowns across the world caused transportation delays and hindered import-export activities. However, the sector is recovering well since restrictions were gradually lifted. An increase in electric vehicle sales and growing demand for electronic appliances have led the market recovery over the last two years.

Key Highlights

- The growing rubber and tire industry along with increasing demand from the non-tire segment of the construction industry are the key attributes driving the demand for the market studied.

- On the flipside, environmental concerns related to its disposal are expected to hinder the growth of the market.

- The development of new additives to produce high-performance rubbers that increase the durability of the end product is likely to act as an opportunity in the future.

- Asia-Pacific region dominated the market for rubber additives with India, China, Japan driving the consumption.

Rubber Additives Market Trends

Tire Segment to Dominate the Market

- The tire industry accounts for the largest share of the rubber additives market during the study period. Natural rubber in combination with synthetic rubbers like butadiene rubber or styrene butadiene rubber is majorly used in tire manufacturing.

- The tire market continues to grow due to technological advances in manufacturing high-quality tires. Increasing device automation and big data adoption is boosting the market growth. Additionally, for cost-effective and high-quality tire production, some manufacturers are using an automated, one-step tire manufacturing process.

- According to the United States Tire Manufacturers Association (USTMA), total U.S. tire shipments of 342.1 million units in 2022, compared to 335.2 million units in 2021.

- China is the world's largest tire producer and consumer. There are more than 300 large, medium, and small tire manufacturers in all segments of China. China's tire industry is the largest in the world in terms of value and volume. According to China Rubber Industry Association's Tire Industry, the top 38 member companies produced a total of 529.22 million tires in 2021, an increase of 11.28% from previous year.

- Furthermore, according to the French tire manufacturing giant Michelin, in original equipment, the truck and bus tire market continued to perform well in Europe and North America against a backdrop of saturated order books since 2022. In North America, demand was supported by purchases of vehicles in anticipation of a new emissions standard coming into force in 2024.

- Considering all the above facts and factors, the usage and demand of rubber additives for tire applications are expected to grow in the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is expected to dominate through the forecast period. With the accelerating usage of rubber additives in automotive and increasing application in electrical and electronucs applications in countries such as China, India, and South Korea, the consumption of rubber additives is growing in the region.

- Rubber additives are widely used in the processing of rubber and its allied products. The growing demand for rubber in tire manufacturing in the automotive sector has been driving the market for rubber additives. The recovering automotive industry and resuming of other rubber-based industries in the country are expected to drive the market studied in the near future.

- China is the world's largest consumer of natural rubber, accounting for 37% of global consumption, but lacks suitable land to produce only a fraction of what it needs domestically. As a result, the Chinese government began encouraging Chinese companies to invest in rubber production. Thus, there is a potential for rubber additives in the country as they are used both to process natural and synthetic rubber.

- Since 2005, China has been the world's largest tire producer and consumer. Although tire production and consumption have enjoyed a very healthy growth, the last few years, especially the last two years, the market has been very tough for domestic and foreign companies operating in the country. However, as the automotive production and usage of rubber additives in different end-user industies constinues to expand, the consumption is projected to increase during the forecast period.

- According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), despite the global economic unceratinities prevailing, the country's motor vehicle production registered an increase of 7% in 2021 and 3% in 2022.

- In addition, according to the association, motor vehicle production in India, Australia, and South Korea registered annual increases of 24%, 13%, and 9%, respectively, in 2022.

- According to the National Statistics Bureau, China's electronic information manufacturing sector recorded steady growth in 2022, signaling strong expansion in terms of production and investment. According to the Ministry of Industry and Information Technology, the added value of large companies in this sector increased by 7.6% year-on-year in this period, making the industry 4% higher than all industries. This is boosting the usage of electric cables.

- The Indian electronics industry is one of the fastest growing industries in the world. Recently, the Ministry of Electronics and Information Technology released Volume 2 of its vision document on electronics manufacturing in India, stating that the electronics manufacturing industry is anticipated to reach USD 300 billion by 2025-26.

- All factors above are likely to fuel the growth of rubber additives market in Asia-Pacific over the forecasted time frame.

Rubber Additives Industry Overview

The global rubber additives market is partially consolidated in nature, with top 5 players together accounting for more than 40% of the total market. Major players are also focusing on R&D activities, developing innovative techniques for the development of the product, engaging in mergers and acquisitions in order to increase their market share and optimizing supply chain to increase its efficacy and specialization in the market. The key players in the market studied include China Sunsine Chemical Holdings Limited, Rhein Chemie (LANXESS), Eastman Chemical Company, China Petrochemical Corporation (Sinopec), and NOCIL LIMITED, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growth in the Tire and Rubber Industry

- 4.1.2 Growing Demand from the Non-Tire Segment in the Construction Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Environmental Constraints Pertaining to Rubber Chemicals

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of Substitute Products

- 4.4.4 Threat of New Entrants

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Activators

- 5.1.2 Vulcanization Inhibitors

- 5.1.3 Plasticizers

- 5.1.4 Other Types

- 5.2 Application

- 5.2.1 Tires

- 5.2.2 Conveyor Belts

- 5.2.3 Electric Cables

- 5.2.4 Other Applications

- 5.3 Fillers

- 5.3.1 Carbon Black

- 5.3.2 Calcium Carbonate

- 5.3.3 Silica

- 5.3.4 Other Fillers

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Behn Meyer

- 6.4.3 China Petrochemical Corporation (SINOPEC)

- 6.4.4 China Sunsine Chemical Holdings Limited

- 6.4.5 Eastman Chemical Company

- 6.4.6 Emery Oleochemicals

- 6.4.7 Kemai Chemical Co. Ltd

- 6.4.8 MLPC International (Arkema Group)

- 6.4.9 NOCIL LIMITED

- 6.4.10 PUKHRAJ ZINCOLET

- 6.4.11 Rhein Chemie (Lanxess)

- 6.4.12 Sumitomo Chemical Co. Ltd

- 6.4.13 Thomas Swan & Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand From Electric Vehicles

- 7.2 Development of Bio-based Rubber Additives

橡胶添加剂市场规模、份额、成长分析(按类型、应用、填料和地区)—2025-2032 年产业预测

橡胶添加剂市场规模、份额、成长分析(按类型、应用、填料和地区)—2025-2032 年产业预测 橡胶添加剂市场按最终用途、聚合物、类型、应用和形态划分—2025-2032年全球预测

橡胶添加剂市场按最终用途、聚合物、类型、应用和形态划分—2025-2032年全球预测 2025年橡胶添加剂全球市场报告

2025年橡胶添加剂全球市场报告 橡胶添加剂市场报告,按类型(活化剂、促进剂、硫化抑制剂、塑化剂等)、橡胶类型(天然橡胶、合成橡胶)、应用(轮胎、输送带、电缆等)和地区划分,2025 年至 2033 年

橡胶添加剂市场报告,按类型(活化剂、促进剂、硫化抑制剂、塑化剂等)、橡胶类型(天然橡胶、合成橡胶)、应用(轮胎、输送带、电缆等)和地区划分,2025 年至 2033 年 全球 6PPD 市场、表现与预测(2020-2031 年)

全球 6PPD 市场、表现与预测(2020-2031 年) 汽车轮胎橡胶添加剂市场 - 全球产业规模、份额、趋势、机会和预测,按类型、应用、地区和竞争细分,2020-2030F

汽车轮胎橡胶添加剂市场 - 全球产业规模、份额、趋势、机会和预测,按类型、应用、地区和竞争细分,2020-2030F 全球橡胶添加剂市场规模(按类型、应用、最终用户产业、地区、范围和预测)

全球橡胶添加剂市场规模(按类型、应用、最终用户产业、地区、范围和预测) 6PPD的全球市场 - 市场占有率和排行榜,整体销售额,需求的预测(2024年~2030年)橡胶添加剂市场 - 2024 年至 2029 年预测

6PPD的全球市场 - 市场占有率和排行榜,整体销售额,需求的预测(2024年~2030年)橡胶添加剂市场 - 2024 年至 2029 年预测 橡胶添加剂市场- 按类型(促进剂、活化剂、胶溶剂、增塑剂、增粘剂、硫化抑製剂、橡胶抗氧化剂、不溶性硫、抗降解剂)、按应用、按涂层剂和预测, 2024 - 2032 年

橡胶添加剂市场- 按类型(促进剂、活化剂、胶溶剂、增塑剂、增粘剂、硫化抑製剂、橡胶抗氧化剂、不溶性硫、抗降解剂)、按应用、按涂层剂和预测, 2024 - 2032 年