|

市场调查报告书

商品编码

1435213

丙烯酸表面涂料:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Acrylic Surface Coating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

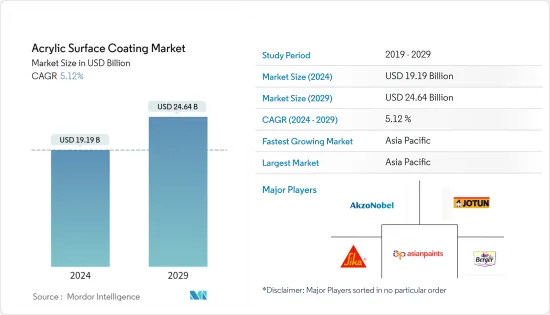

丙烯酸表面涂料市场规模预计到2024年为191.9亿美元,预计到2029年将达到246.4亿美元,在预测期内(2024-2029年)增长5.12%,复合年增长率增长。

建筑涂料应用的增加预计将推动市场成长。另一方面,全球汽车生产放缓预计将阻碍市场成长。

主要亮点

- 由于建设产业需求的增加,丙烯酸表面涂料市场预计在预测期内将成长。

- 亚太地区主导全球市场,主要消费国为中国、印度和日本。

亚克力表面涂料市场趋势

建筑业的需求不断成长

- 丙烯酸表面涂料广泛应用于建筑和施工,因为它们惰性,并且在暴露于室外条件下时具有良好的保色性。丙烯酸有型态,包括乳化(乳胶)、清漆、瓷漆和粉末。

- 丙烯酸类聚合物的主要成分是丙烯酸和甲基丙烯酸,聚合物结构难以吸收紫外线。与油基涂料、醇酸树脂和环氧树脂相比,它具有更强的耐候性和抗氧化性,因此在建筑和施工中的应用越来越多。

- 南非政府制定了《2050年国家基础建设计画》,旨在2050年发展能源、交通、数位通讯和水务等基础设施。到2040年,基础建设投资将达到3,300亿美元。

- 此外,美国人口普查局编制的额外统计数据显示,2022 年美国年度新建建筑面积将为 16,575.90 亿美元,而 2021 年为 14,998.22 亿美元。美国,2022 年美国住宅建筑年价值为 8,491.64 亿美元,而 2021 年为 7,406.45 亿美元。 2022 年,该国年度非住宅建筑价值将为 8,084.27 亿美元,而 2021 年为 7,591.77 亿美元,市场消费下降。

- 据加拿大建筑协会称,建筑业是加拿大最大的雇主之一,为国家的经济成功做出了重大贡献。该产业每年产值约 1,410 亿美元,占该国国内生产总值(GDP) 的 7.5%。

- 建设产业在丙烯酸表面涂料的使用方面处于领先地位,其中中国、德国、美国、印度和日本在市场上发挥主要作用。

亚太地区主导市场

- 预计亚太地区在预测期内将主导丙烯酸表面涂料市场。建筑业的成长增加了中国、印度和日本等国家对丙烯酸表面涂料的需求。

- 最大的丙烯酸表面涂料生产商位于亚太地区。製造丙烯酸表面涂料的一些领先公司包括亚洲涂料公司、伯杰涂料印度有限公司、阿克苏诺贝尔公司、佐敦公司和西卡公司。

- 中国的「十四五」规划重点在于能源、交通、水利系统和都市化领域的新型基础设施计划。据计算,「十四五」期间(2021-2025年)新基建投资总额预计将达到约27兆元(4.2兆美元)。

- 中国的都市化位居世界前列。 2022年中国的都市化64.7%,这项都市更新政策旨在发展更绿色、更有效率的城市,因为政府的目标是改善中国城市的居住条件。

- 印度庞大的建筑业可望成为全球第三大建筑市场。印度政府实施的智慧城市计划、全民住宅等多项政策预计将为印度建设产业提供动力。

- 印度统计与计画实施部的数据显示,2022年第四季建筑业占GDP的比重达372.6亿美元,高于2022年第三季329.5亿美元的GDP比重。

- 除纸张涂料外,丙烯酸表面涂料还用作油漆、纺织品和皮革饰面、地板抛光剂和航太应用中的保护涂料。

- 上述因素和政府支持将有助于预测期内丙烯酸表面涂料市场需求的增加。

亚克力表面涂料产业概况

全球丙烯酸表面涂料市场部分分散,主要参与者只占该行业的一小部分。市场上的主要企业包括亚洲涂料、Berger Paints India Limited、Akzo Nobel NV、Jotun、Sika AG 等(排名不分先后)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 扩大建筑涂料的应用

- 汽车产业应用快速拓展

- 其他司机

- 抑制因素

- 与低VOC相关的严格环境法规

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(以金额为准的市场规模)

- 目的

- 水性的

- 溶剂型

- 粉底

- 其他用途

- 最终用户产业

- 建筑/施工

- 住宅

- 非住宅

- 车

- 航太

- 其他最终用户产业

- 建筑/施工

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲

- 亚太地区

第六章 竞争形势

- 併购、合资、联盟、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- 3M

- Akzo Nobel NV

- Arkema Group

- Asian Paints

- BASF SE

- Berger Paints India Limited

- Dow

- Jotun

- PPG Industries Inc.

- Sika AG

- Solvay

- The Sherwin-Williams Company

第七章 市场机会及未来趋势

- 生物基压克力型涂料的开发

- 其他机会

The Acrylic Surface Coating Market size is estimated at USD 19.19 billion in 2024, and is expected to reach USD 24.64 billion by 2029, growing at a CAGR of 5.12% during the forecast period (2024-2029).

Increasing applications in architectural coatings are expected to drive the market growth. On the flip side, the slowdown in global automotive production is expected to hinder the growth of the market.

Key Highlights

- The acrylic surface coating market is expected to grow during the forecast period, owing to the increasing demand from the building and construction setor.

- The Asia-Pacific region dominates the global market, with the major consumption being registered in China, India, and Japan.

Acrylic Surface Coating Market Trends

Growing Demand from the Building and Construction Sector

- Acrylic surface coatings are widely used in the building and construction sector because of their inertness and excellent color retention when exposed to outdoor conditions. Acrylics are available in various forms, such as emulsions (latex), lacquers, enamels, and powders.

- The chief component of acrylic polymers is acrylic and methacrylic acid which provide a polymer structure with a little tendency to absorb UV light. It increases its resistance to weathering and oxidation than oil-based paints, alkyds, or epoxies, so its application increased in the buildings & construction sector.

- The South African government devised a 'National Infrastructure Plan 2050' to deliver infrastructure development across energy, transport, digital communications, and water by 2050. USD 0.33 trillion will be invested through 2040 in infrastructure development.

- Further, as per further statistics generated by the US Census Bureau, the annual value for new construction in the United States accounted for USD 1,657,590 million in 2022, compared to USD 1,499,822 million in 2021. Moreover, the annual value of residential construction in the United States was valued at USD 849,164 million in 2022, compared to USD 740,645 million in 2021. The country's annual non-residential construction value was USD 808,427 million in 2022, compared to USD 759,177 million in 2021. It is thereby decreasing the consumption of the market studied in the short term.

- According to the Canadian Construction Association, the construction sector is one of Canada's largest employers and a major contributor to the country's economic success. The industry generates about USD 141 billion annually and contributes 7.5% of the country's Gross Domestic Product (GDP).

- The building & construction industry leads in using acrylic surface coatings, with China, Germany, the United States, India, and Japan playing a major role in the market.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to dominate the market for acrylic surface coatings during the forecast period. The demand for acrylic surface coatings is increasing in countries like China, India, and Japan because of the growing building and construction sector.

- The largest producers of acrylic surface coatings are located in the Asia-Pacific region. Some leading companies producing acrylic surface coatings are Asian Paints, Berger Paints India Limited, Akzo Nobel NV, Jotun, and Sika AG.

- China's 14th Five-Year Plan focuses on new infrastructure projects in energy, transportation, water systems, and urbanization. According to estimates, overall investment in new infrastructure during the 14th Five-Year Plan period (2021-2025) will reach roughly CNY 27 trillion (USD 4.2 trillion).

- China's urbanization rate is among the highest in the world. While China's urbanization rate reached 64.7% in 2022, this urban renewal policy aims to develop greener and more efficient cities as the government seeks to improve China's urban living conditions.

- India's huge construction sector is expected to become the world's third-largest construction market. Various policies implemented by the Indian government, such as the Smart Cities project, Housing for All, etc., are expected to bring impetus to the Indian construction industry.

- As per the Ministry of Statistics and Programme Implementation of India, the construction sector contributed a GDP share amounting to USD 37.26 billion in Q4 2022, higher than the GDP share of USD 32.95 billion in Q3 2022.

- Acrylic surface coatings are used as protective coatings in aerospace applications other than paints, fabric and leather finishes, floor polishes, and paper coatings.

- The above factors and government support contribute to the increasing demand for the acrylic surface coatings market during the forecast period.

Acrylic Surface Coating Industry Overview

The global acrylic surface coating market is partially fragmented, with the major players accounting for a marginal portion of the industry. Some major companies operating in the market are Asian Paints, Berger Paints India Limited, Akzo Nobel NV, Jotun, and Sika AG, among others (not in particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Application in Architectural Coatings

- 4.1.2 Rapidly Growing Application in the Automotive Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations Related to Lower VOC

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Application

- 5.1.1 Water-borne

- 5.1.2 Solvent-borne

- 5.1.3 Powder-based

- 5.1.4 Other Applications

- 5.2 End-user Industry

- 5.2.1 Building and Construction

- 5.2.1.1 Residential

- 5.2.1.2 Non-residential

- 5.2.2 Automotive

- 5.2.3 Aerospace

- 5.2.4 Other End-user Industries

- 5.2.1 Building and Construction

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Akzo Nobel NV

- 6.4.3 Arkema Group

- 6.4.4 Asian Paints

- 6.4.5 BASF SE

- 6.4.6 Berger Paints India Limited

- 6.4.7 Dow

- 6.4.8 Jotun

- 6.4.9 PPG Industries Inc.

- 6.4.10 Sika AG

- 6.4.11 Solvay

- 6.4.12 The Sherwin-Williams Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Bio-based Acrylic Coatings

- 7.2 Other Opportunities