|

市场调查报告书

商品编码

1435772

工作流程自动化:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Workflow Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

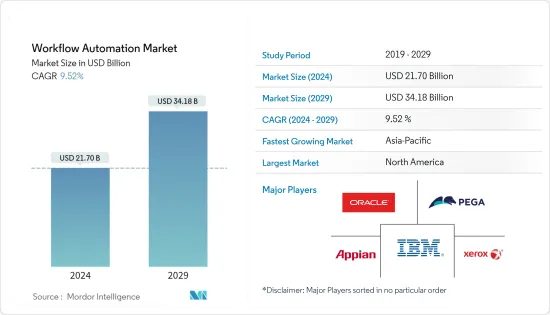

工作流程自动化市场规模预计到 2024 年为 217 亿美元,预计到 2029 年将达到 341.8 亿美元,在预测期内(2024-2029 年)复合年增长率为 9.52%。

工作流程的概念是从製造和办公室的流程概念演变而来的。这些流程自工业化时代以来就已经存在,是透过关注工作活动的平凡方面来显着提高效率的结果。他们通常将工作活动划分为明确定义的任务、规则、角色和程序,并规范大多数製造和管理任务。最初,过程完全由人类操纵物理物件来执行。

主要亮点

- 从资讯科技简介开始,职场流程由资讯系统部分或完全自动化,其中电脑程式执行任务并执行先前由人类执行的规则。工作流程自动化的开发是为了透过将最佳实践纳入製造和控制工作流程来提高生产力和品质。这样可以轻鬆定义工作流程,并根据从执行特定阶段的各个阶段的资料来源和网路位置检索的资料产生作业单。系统可以自动移动作业单,无需外部因素的干预,还可以随时直观地显示作业单的状态。这个系统还可以适应某些阶段的变化。

- 组织对工作流程软体的需求不断增长,导致快速投资开发更复杂、更有效率的软体。 Signavio 表示,62% 的组织对其多达 25% 的业务进行建模,但只有 2% 的组织对所有流程进行建模。此外,13% 的受访组织表示他们正在大规模实施智慧自动化解决方案。 23% 已实施自动化,37% 正在试行自动化。

- 组织对工作流程软体的需求不断增长,导致快速投资开发更复杂、更有效率的软体。从电脑视觉、认知自动化、机器学习到机器人流程自动化,人工智慧和相关新技术的采用正在增加。这种技术的融合创造了自动化功能,可以显着提高客户业务。

- 与实施新技术不同,工作流程自动化可能会对人类和非人类帐户造成网路攻击的风险。因此,流程自动化的安全性变得极为重要。 RPA 机器人通常处理敏感资料并将其从一个系统传输到另一个系统。如果资料无法受到保护,资料可能会被利用,并使企业损失数百万美元。

- 新型冠状病毒肺炎(COVID-19)的爆发暴露了供应链的脆弱性。对大多数 IT 组织而言,脆弱的生态系统包括关键 IT 服务的提供者。此外,在家工作的要求使服务供应商能够确保关键任务企业客户拥有所需的工具和技术,以实现所提供服务的速度、安全性、品质和整体有效性。这样做是必要的。

工作流程自动化市场趋势

软体产业预计将大幅成长

- 由于新兴应用和经营模式以及设备成本的降低,物联网在各行业的采用正在迅速增加。随着物联网连接的激增,我们看到对用于自动化工作流程的工具的巨大需求,例如工作流程自动化软体、工作流程管理软体、工作流程系统和业务流程自动化 (BPA)。工作流程自动化软体具有多种优势,包括付加功能和整合功能,可扩展可实施的自动化范围。这种采用将进一步增加整个工作流程自动化市场对软体产业的需求。

- 一些功能包括减少实施和维护软体所需的 IT 支援量的能力。业务用户可以透过直觉的视觉化介面轻鬆存取某些功能,从而加快自动化速度,并使业务团队能够在优化工作流程中发挥共同创造性的作用。低程式码还可以减轻 IT 积压的压力。例如,Integrify 是一个低程式码工作流程自动化平台,提供易于使用的建构器、灵活的客製化、多种定价选项和专用的客户支援。

- 此外,撷取和整合传入资料对于任何团队来说都是困难的,工作流程自动化软体提供了可定製表单等功能,可透过标准化流程、避免错误和消除重复资料输入来简化请求管理。推广功能性解决方案。此入口网站可让您轻鬆组织表单并与内部或外部合作伙伴安全地共用它们。在工作流程自动化中发挥重要作用的其他功能包括整合、范本和规则的存在以及条件逻辑。

- 例如,2023 年 10 月,商业软体低程式码开发平台 Retool Inc. 宣布全面推出 Retool Workflows。这种高度创新的自动化工具旨在透过允许开发人员优先考虑编码并与监控和维护工具一起无缝地自动化任务来显着帮助开发人员。 Retool Workflows 允许开发人员提供使用者友好且具有视觉吸引力的介面,该介面提供了广泛的编码原型製作和建构。此外,该工具还有助于基于触发器的资料提取、转换和载入。

预计亚太地区在预测期内成长最快

- 随着中国市场竞争的加剧,国内各产业都在透过数位转型改善工作流程。例如,东风日产启动了数位转型计划,以简化和加快一系列新车的行销流程。该公司启动了数位转型策略,以推动更好地利用资料,旨在改善现有工作流程、简化内部业务并提高整体效率。作为该计划的一部分,该公司部署了 UiPath,一种机器人流程自动化 (RPA) 软体,以自动执行重复的数位任务。

- 中国联通智慧网路研发中心于2021年与华为合作,基于华为AUTIN系统开发并部署了人工智慧驱动的网路管理和营运平台。该公司推出了基于人工智慧的网路管理和营运平台,利用资料来简化和自动化全国网路营运、规划和管理,同时随着5G网路和服务的推出提高成本效率和客户体验,提高永续性。

- 自动化是与未来工作方式相关的最重要部分之一,日本正在透过人工智慧进行创新。野村研究认为,到 2035 年,日本人工智慧领域将取得重大进展。 Abeja 和 NEC 等自动化公司正在透过创新来提高生产效率,从而推动日本的 GDP 成长。

- 自动化在印度的经济发展中发挥了重要作用。该国目前正在透过引进技术和创新在大多数行业进行转型。国家人工智慧战略(NSAI)强调,人工智慧预计到 2035 年将使印度年增长率加快 1.3%。

- 东南亚和澳洲是亚太地区的其他重要地区。东南亚的公司正在让员工为以人工智慧为中心的未来做好准备,并拥抱新技术。为此,公司需要透过适当的技能提升策略来缩小技能差距。数位化不仅将帮助该地区为当地企业建立具有全球竞争力的合作伙伴关係,还将增加全球扩张的潜力并支持成功的技术和知识转移。

工作流程自动化产业概述

工作流程自动化市场分散且竞争激烈。该市场由IBM公司、甲骨文公司、Pegasystems公司、施乐公司和Appian公司等几家主要企业组成。这些公司正在利用策略合作倡议来提高市场占有率和盈利。

- 2023 年 11 月:全球云端平台和人工智慧主导的财务、采购和客户服务功能流程自动化解决方案的产业领导者 Esker 宣布 Teknion 将使用 Esker 的应付帐款自动化解决方案来提高业务效率,并宣布已被选中。 Teknion 旨在利用 Esker 的创新技术简化其全球站点的系统和 ERP 工作流程。 Teknion 特别寻求一种结合自动化和人工智慧的解决方案,以有效地结合来自多个 ERP 的讯息,从而实现财务系统的持续转型。

- 2023 年 9 月:Salesforce 为 Slack 平台引进了一些令人印象深刻的进步。这包括整合 Slack 的原生生成人工智慧功能、帮助结构化工作流程的清单功能以及对我们的自动化平台的各种增强功能。同时,Slack 也取得了重大进展,推出了自己的 Slack AI,该人工智慧利用了自己的本地法学硕士技术。此外,Slack 还为工作流程自动化添加了有价值的功能,包括列出有组织的任务、核准和资讯的能力。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争公司之间的敌对关係

- 替代品的威胁

- 市场驱动因素

- 各产业的物联网采用率不断提高

- 在业务流程管理中更多地采用 RPA

- 市场限制因素

- 资料安全问题

第五章市场区隔

- 按配置

- 本地

- 云

- 按解决方案

- 软体

- 服务

- 按最终用户产业

- 银行

- 电信

- 零售

- 製造/物流

- 医疗保健/製药

- 能源/公共产业

- 其他最终用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 其他亚太地区

- 世界其他地区(拉丁美洲、中东和非洲)

- 北美洲

第六章 竞争形势

- 公司简介

- IBM Corporation

- Oracle Corporation

- Xerox Corporation

- Pegasystems Inc.

- Appian Corporation

- Bizagi

- Software AG

- IPsoft Inc.

- Newgen Software Technologies Limited

- Nintex Global Limited

第七章 投资分析

第八章市场趋势与未来机会

The Workflow Automation Market size is estimated at USD 21.70 billion in 2024, and is expected to reach USD 34.18 billion by 2029, growing at a CAGR of 9.52% during the forecast period (2024-2029).

The workflow concept has evolved from the notion of process in manufacturing and the office, and such processes have existed since the time of industrialization and are the outcome of a search to surge efficiency by concentrating on the routine aspects of work activities. They typically separate work activities into well-defined tasks, rules, roles, and procedures that regulate most of the manufacturing and office work. Initially, processes were carried out entirely by humans who manipulated physical objects.

Key Highlights

- With the introduction of information technology, processes in the workplace are partially or totally automated by information systems through computer programs performing tasks and enforcing rules that humans previously implemented. Workflow automation is developed to enhance productivity and quality by incorporating best practices in workflow processes involved in manufacturing as well as management. It facilitates defining workflow processes from the data fetched from the data sources and the network location of the various stages at which the execution of that particular stage is performed, along with the generation of job ticket. The system is able to move the job ticket automatically without any intervention of any external factor along with providing the user, a visual display of status of any job ticket at any point of time. The system is also adaptable to changes at a particular stage.

- The growing demand for workflow software from organizations is leading to rapid investment in the development of more sophisticated and efficient software. According to Signavio, 62% of the organizations have modeled up to 25% of their businesses, but a meager 2% have all their processes modeled. Moreover, 13% of the surveyed organizations say that they are implementing intelligent automation solutions at scale; 23% are implementing, and 37% are piloting automation.

- The increasing demand for workflow software by organizations is leading to rapid investment in the development of more sophisticated and efficient software. There is increasing adoption of artificial intelligence and related new technologies ranging from computer vision, cognitive automation, and machine learning to robotic process automation. This convergence of technologies produces automation capabilities that dramatically elevate business value and competitive advantages for customers.

- Unlike any new technology implementation, workflow automation can create risks for cyberattacks directed at both human and non-human accounts. As a result, process automation security is of critical importance. RPA bots often work on confidential data, transferring it from one system to another. If data is not protected, it can be leveraged, costing businesses millions.

- With the onset of COVID-19, the vulnerability of supply chains has been exposed. For most IT organizations, a fragile ecosystem includes providers of critical IT services. In addition, work-from-home mandates led the service providers to ensure that mission-critical enterprise customers have the necessary tools and technologies to enable the speed, security, quality, and overall efficacy of services provided.

Workflow Automation Market Trends

Software Segment is Expected to Register Significant Growth

- The adoption of IoT is surging among industries owing to the emergence of applications and business models and reduced device costs. With surging IoT connective, the tools used to automate workflows, including workflow automation software, workflow management software, workflow systems, or business process automation (BPA) are observing significant demand. The workflow automation software has various advantages, including value-adding features, and provides integration capabilities to increase the range of automation one can implement. Such adoption will bring more demand for the software segment across the workflow automation market.

- Some features include the capability of reducing the amount of IT support required to implement and maintain the software. Business users can conveniently access some features through an intuitive visual interface, making the automation faster and putting business teams in a co-creative role for optimizing workflows. Low code also relieves pressure on the IT backlog. For instance, Integrify is a low-code workflow automation platform that offers an easy-to-use builder, flexible customization, multiple pricing options, and dedicated customer support.

- Moreover, capturing and consolidating incoming data can be challenging for any team, and workflow automation software facilitates a solution with features such as customizable forms to simplify request management by standardizing processes, avoiding errors, and eliminating duplicate data entry. Portals make organizing and securely sharing forms with internal or external partners easy. Other features that play a crucial role in the workflow automation includes integrations, presence of templates and rules as well as conditional logic.

- For instance, In October 2023, Retool Inc., a low-code development platform for business software, announced the general availability of Retool Workflows. This highly innovative automation tool has been designed with the aim of greatly assisting developers by enabling them to prioritize coding and then seamlessly automate tasks alongside monitoring and maintenance tools. With Retool Workflows, developers are offered a user-friendly and visually appealing interface that provides an extensive array of coding tools, allowing for efficient prototyping and construction of periodic jobs, customized alerts, and information management tasks. Furthermore, this tool facilitates data extraction, transformation, and loading based on triggers.

Asia-Pacific Expected to Register the Fastest Growth During the Forecast Period

- With the increasing competition in the Chinese market, various industries in the country have been improving workflow through digital transformation. For instance, Dongfeng Nissan initiated its digital transformation program to improve efficiency and speed up the process of marketing a line of new vehicles. The company launched its digital transformation strategy for promoting the better use of data aimed to improve existing workflows, streamline internal business operations, and promote overall efficiency. As part of the program, the company implemented robotic process automation (RPA) software, UiPath, to automate repetitive digital tasks.

- China Unicom's Intelligent Network Innovation Center worked with Huawei in 2021 to develop and deploy an AI-powered network management and operations platform based on Huawei's AUTIN system. The company deployed an AI-based network management and operations platform to use data to simplify and automate national network operation, planning, and management while improving cost-effectiveness, customer experience, and sustainability as it rolled out 5G networks and services.

- Automation is one of the most crucial parts related to the future of work approach, and Japan is innovating through AI. According to the Nomura Research Institute, the AI sector in the country will see a massive stride by 2035. Automation companies such as Abeja, NEC, and others innovate to bring more production efficiency to push Japan's GDP.

- Automation has been playing a major role in India's economic development. The country is currently witnessing a transition in most sectors through the implementation of technology and innovation. The National Strategy for Artificial Intelligence (NSAI) highlighted that AI is predicted to accelerate India's annual growth rate by 1.3% by 2035.

- Southeast Asia and Australia are prominent regions in the Rest of Asia-Pacific. Southeast Asian companies are preparing employees for an AI-centered future and embracing new technologies. This would require enterprises to plug the skills gap through a proper upskilling strategy. Digitization would help the region to create globally competitive partnerships for local companies as well as improve the potential for global expansion and support a successful technology and knowledge transfer.

Workflow Automation Industry Overview

The Workflow Automation Market is fragemented and highly competitive. This market consists of several major players, such as IBM Corporation, Oracle Corporation, Pegasystems Inc., Xerox Corporation, and Appian Corporation. These companies leverage strategic collaborative initiatives to increase their market share and profitability.

- November 2023: Esker, a global cloud platform and industry leader in AI-driven process automation solutions for Finance, Procurement, and Customer Service functions, announced Teknion has selected Esker's Accounts Payable automation solution to enhance its operational efficiencies. By leveraging Esker's innovative technology, Teknion aims to streamline its systems and ERP workflow across its global sites. Teknion specifically sought a solution incorporating automation and artificial intelligence to effectively combine information from multiple ERPs for their ongoing transformation of financial systems.

- September 2023: Salesforce has introduced some impressive advancements to its Slack platform. These include integrating Slack-native generative AI capabilities, a helpful lists function for structured workflow, and various enhancements to its automation platform. On the other hand, Slack has also made significant strides by launching its own Slack AI, which is powered by its own native LLM technology. Additionally, Slack has made valuable additions to its workflow automation, such as a lists feature for organized tasks, approvals, and information.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Market Drivers

- 4.3.1 Increasing Adoption of IoT across industries

- 4.3.2 Rise in Implementation of RPA in Business Process Management

- 4.4 Market Restraints

- 4.4.1 Data Security Concerns

5 MARKET SEGMENTATION

- 5.1 By Deployment

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.2 By Solution

- 5.2.1 Software

- 5.2.2 Service

- 5.3 By End-user Industry

- 5.3.1 Banking

- 5.3.2 Telecom

- 5.3.3 Retail

- 5.3.4 Manufacturing and Logistics

- 5.3.5 Healthcare and Pharmaceuticals

- 5.3.6 Energy and Utilities

- 5.3.7 Other End-user Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Rest of Asia-Pacific

- 5.4.4 Rest of the World (Latin America, Middle East and Africa)

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 IBM Corporation

- 6.1.2 Oracle Corporation

- 6.1.3 Xerox Corporation

- 6.1.4 Pegasystems Inc.

- 6.1.5 Appian Corporation

- 6.1.6 Bizagi

- 6.1.7 Software AG

- 6.1.8 IPsoft Inc.

- 6.1.9 Newgen Software Technologies Limited

- 6.1.10 Nintex Global Limited

7 INVESTMENT ANALYSIS

8 MARKET TRENDS AND FUTURE OPPORTUNITIES

2025年工作流程自动化与优化软体全球市场报告

2025年工作流程自动化与优化软体全球市场报告 全球工作流程自动化市场规模、份额、趋势分析报告:按类型、按部署、按营运、按流程、按行业、按组织规模、按地区、2024-2031 年展望和预测

全球工作流程自动化市场规模、份额、趋势分析报告:按类型、按部署、按营运、按流程、按行业、按组织规模、按地区、2024-2031 年展望和预测 工作流程自动化和最佳化软体市场:按部署类型、最终用户划分 - 2025-2030 年全球预测销售流程自动化软体市场:按部署、公司规模和最终用途划分 - 2025-2030 年全球预测

工作流程自动化和最佳化软体市场:按部署类型、最终用户划分 - 2025-2030 年全球预测销售流程自动化软体市场:按部署、公司规模和最终用途划分 - 2025-2030 年全球预测 工作流程自动化市场机会、成长动力、产业趋势分析与预测 2024 - 2032

工作流程自动化市场机会、成长动力、产业趋势分析与预测 2024 - 2032 全球工作流程自动化市场规模依流程、组织规模、组件、部署类型、营运、垂直、地区、范围和预测划分施工工作流程自动化市场机会、成长动力、产业趋势分析及 2024 年至 2032 年预测

全球工作流程自动化市场规模依流程、组织规模、组件、部署类型、营运、垂直、地区、范围和预测划分施工工作流程自动化市场机会、成长动力、产业趋势分析及 2024 年至 2032 年预测 工作流程自动化市场:按产品、类型、部署方法、组织规模、应用程式、产业和地区划分 - 到 2030 年的全球预测工作流程自动化市场 - 2018-2028 年全球产业规模、份额、趋势、机会和预测,按部署、解决方案、最终用户产业、地区和竞争进行细分工作流程的自动化和最佳化软体的全球市场

工作流程自动化市场:按产品、类型、部署方法、组织规模、应用程式、产业和地区划分 - 到 2030 年的全球预测工作流程自动化市场 - 2018-2028 年全球产业规模、份额、趋势、机会和预测,按部署、解决方案、最终用户产业、地区和竞争进行细分工作流程的自动化和最佳化软体的全球市场