|

市场调查报告书

商品编码

1435807

铝罐:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Aluminum Cans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

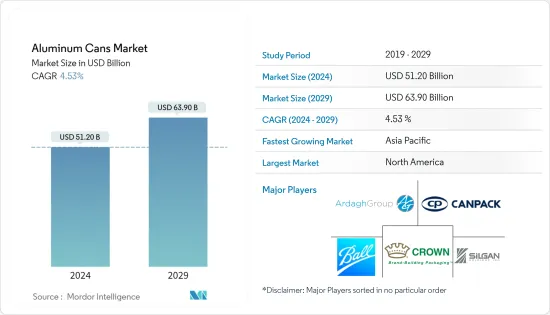

铝罐市场规模预计到2024年为512亿美元,预计到2029年将达到639亿美元,在预测期内(2024-2029年)复合年增长率为4.53%。

主要亮点

- 铝罐具有能长期保存食品品质的优点。铝罐可提供近 100% 的防护,免受光、氧气、湿气和其他污染物的影响。铝罐不生锈且耐腐蚀,因此在所有包装中保存期限最长。

- 铝罐在食品和饮料行业中的使用增加可归因于其保护性能、永续性优势和消费者便利性。随着製造商和消费者都认识到铝包装的好处,这一趋势预计将持续下去。铝是地球上回收率最高的材料,可回收率约 100%。铝在回收过程中不会腐烂。因此,它可以根据需要多次回收。回收铝可以节省数百万吨的温室气体排放、能源、电力和运输燃料。使用回收材料生产铝罐所消耗的能源不到用矾土生产新铝罐所需能源的 5%。

- 与竞争的包装类型相比,铝罐具有更高的回收率,并且含有更多的回收成分。据铝业协会称,它是市场上回收率最高的材料之一。 2022 年 4 月,波尔公司与 Recycle Aerosol LLC 合作,提高美国铝气雾罐的回收率。此次合作将增加气雾罐的回收利用,并建立一个封闭回路型系统,将用过的气雾罐回收成新的气雾罐。用再生铝製造铝产品具有能源效率和碳效率。用于生产铝气雾剂的合金的高纯度提高了效率,并且还减少了对主要从回收的铝气雾剂瓶和罐中获取的原始铝的需求。

- 然而,铝罐包装面临来自替代包装解决方案的激烈竞争。塑胶、纸张和玻璃包装解决方案是业内可用的替代包装选择。此外,电子商务的重要性在世界范围内日益增加,预计将影响整个包装行业。而且,塑胶包装的逐渐加强对市场构成了威胁,这主要集中在聚对聚对苯二甲酸乙二酯(PET)等塑胶作为替代品的普及。 PET 塑胶有可能取代食品和饮料行业的铝罐解决方案。

- 同时,消费者对小尺寸和多包装包装形式的偏好等趋势正在支持铝罐数量的增加,特别是在即食食品领域。因此,新兴地区的大多数公司都提供迷你罐装产品,与传统罐装产品相比,迷你罐装产品的容量通常较小,成本较低。例如,海鲜罐头食品创新在东南亚正在显着成长。

- 此外,随着新型冠状病毒感染疾病(COVID-19)在全球持续肆虐,所有产业都受到供应链中断和政府为遏制感染传播而实施的封锁的严重影响。俄罗斯和乌克兰之间的战争也导致多个国家受到经济制裁,导致大宗商品价格飙升,供应链受到扰乱,全球多个市场受到影响,导致行业贸易中断。战争迫使欧洲铝公司减产,造成金属短缺。由于乌克兰战争导致依赖俄罗斯供应的欧洲製造商严重短缺,大宗商品贸易商正在争夺来自中国的铝出货量的微薄利润。欧洲正在经历能源成本上涨。

铝罐市场趋势

成本和便利性优势增加了对罐头食品和饮料的需求

- 年轻人和个人消费者正在消费更多的罐头食品和饮料。这些用户时间紧迫且预算有限,因此他们选择成本更低、便利性更高的产品。世界各地新兴国家生活方式的改变和都市化的提高导致消费者选择易于准备的食品。此外,随着家庭规模的缩小和生活方式的改变,人们在家中准备和食用餐的时间减少,从而导致人们转向食品、冷冻和已调理食品。哪些食品是最常见的包装型态?

- 铝罐最广泛用于饮料,市场对便携性的需求导致了罐装葡萄酒、鸡尾酒、硬饮料和无酒精饮品采用金属包装的最显着趋势。根据饮料的性质,金属罐在饮料行业中的使用可大致分为酒精饮料和非酒精饮料。虽然金属罐历来用于盛装啤酒等酒精饮料,但金属罐越来越多地用于盛装传统上装在玻璃瓶中的其他类型的酒精饮料,例如葡萄酒。

- 罐装食品因其便携性和易用性而在千禧世代和 Z 世代中流行。製造商也以罐装包装出售产品,因为这种设计很受年轻人欢迎。例如,2022年,全球销售了115.82亿罐红牛。这相当于成长了 18.1%。集团收益成长 23.9%,从 78.16 亿欧元(85.2 亿美元)增至 96.84 亿欧元(92.9 亿美元)。

- 出于多种原因,包括导热性、卫生和安全性,铝罐成为食品包装的首选,使其成为家庭和工业领域的便利选择。因此,铝罐广泛应用于食品业,用于包装肉类和鱼贝类、水果和蔬菜、已烹调用餐、宠物食品、汤料和调味品等。如此广泛的终端用户市场创造了食品业对铝罐的巨大需求。铝也广泛用于食品接触材料,因为含铝的食品接触材料是食品铝的人为来源。

- 此外,由于疫情导致消费行为发生变化,人们开始注重储存保质期长的食品,导致食品包装中铝罐的使用量增加,预计这将产生长期的积极影响。 。对所研究市场成长的影响。自封锁期以来,欧洲罐头鱼的销售量激增,尤其是在西班牙、法国和义大利等喜爱鱼类的南欧国家。根据挪威统计局的数据,挪威罐头鱼的消费者物价指数(CPI)在过去几年从2018年的111.4点上升到2022年的125.3点。

- 环保组织的努力和公众的环境意识正在提高世界各地用户的环保意识。消费者越来越多地放弃使用塑料,而对回收产品的需求却在增加。因此,对铝罐等金属包装产品的需求不断增加。

北美占有很大的市场份额

- 由于对永续包装材料的使用和消费的担忧日益增加,北美在收益方面占据了最大的市场占有率。它占世界铝罐消费量的三分之一以上。

- 碳酸软性饮料、能量饮料、碳酸水、精酿啤酒等产品稳定成长。铝罐是最永续的饮料包装之一,可以无限回收。它还可以快速冷却,为印刷提供优质的金属画布,更重要的是,可以保护您喜爱的饮料的风味和完整性。

- 此外,随着美国个人保健部门的扩张,对气雾罐的需求也预计会增加。个人护理业务的成长主要与消费者可支配收入的增加及其购买奢侈品的能力有关。气雾剂用于多种个人保健产品。因此,预计市场将受益于销售量的增加。

- 此外,对除臭剂/止汗剂生产的需求不断增长,导致过去几年北美生产线安装数量的增加。由于个人保健部门对除臭剂、造型慕丝、髮胶喷雾、髮胶和剃须摩丝等不同产品类型的需求不断增加,北美在调查市场中占据了很大份额。根据美国人口普查和西蒙斯全国消费者调查 (NHCS) 的资料,2020 年有 2.987 亿美国人使用除臭剂/止汗剂。预计到 2024 年,这一数字将增至 3,0,604 万。

- 随着加拿大从疫情中恢復过来,加拿大政府也为加拿大企业提供了支持。政府强调透过投资创新促进强劲和持续的经济復苏的重要性,这将使该国实现其低碳成长潜力。预计政府将进行重大投资,帮助加拿大铝业减少温室气体排放。他们表示,零碳铝冶炼是一种创新,将有助于加拿大实现其经济和气候变迁目标。

- 与竞争的包装类型相比,铝罐具有更高的回收率,并且含有更多的回收成分。据铝业协会称,它是市场上回收率最高的材料之一。回收可节省生产新金属所需能源的 90% 以上,进而降低生产成本。在美国,全部区域每出货三个铝罐,就会回收两个铝罐。

- 此外,2022 年 4 月,波尔公司宣布与 Recycle Aerosol LLC 建立战略合作伙伴关係,以提高美国铝气雾罐的回收率。此次合作将增加气雾罐的回收利用,并建立一个封闭回路型系统,将用过的气雾罐回收成新的气雾罐。用再生铝製造铝产品具有很高的能源效率和碳效率。

铝罐产业概况

由于全球和本地行业参与者的存在,铝罐市场高度分散。主要参与者包括 Ball Corporation、Crown Holdings, Inc、Silgan Holdings Inc、Silgan Holdings Inc 和 Ardagh Group SA。该市场的供应商根据产品系列、差异化和定价参与。

2023 年 1 月,永续包装解决方案製造商 CANPACK 加入了阿联酋环球铝业公司 (EGA) 在杜拜成立的铝回收联盟。 CANPACK 在阿拉伯联合大公国 (UAE) 拥有重要的铝罐製造厂。该联盟汇集了阿联酋饮料、废弃物和铝业的主要企业,教导人们如何最有效地重复利用用过的饮料瓶并提高铝回收率。

2022 年 12 月,皇冠控股有限公司宣布与可口可乐及其专用印刷和复製工作室生产的软性饮料品牌 Aquarius 合作,在西班牙开展一场智慧且有吸引力的促销宣传活动。相比之下,Aquarius 采用标准 330 毫升铝罐包装。这种永续的包装形式促进了循环经济,并且由于其无限的可回收性,有助于最大限度地减少需要从地球采购的原材料的数量。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 评估 COVID-19 对产业的影响

第五章市场动态

- 市场驱动因素

- 铝罐回收率高

- 由于成本和便利性相关的好处,对罐头食品的需求增加

- 市场限制因素

- 替代包装解决方案的可用性

第六章市场区隔

- 按类型

- 苗条的

- 光滑

- 标准

- 其他的

- 按最终用户产业

- 饮料

- 食品

- 气雾剂

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 泰国

- 其他亚太地区

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲

- 中东/非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 其他中东/非洲

- 北美洲

第七章 竞争形势

- 公司简介

- Ball Corporation

- Ardagh Group SA

- Crown Holdings Inc.

- Silgan Holdings Inc.

- CAN-PACK SA

- CCL Container Inc.(CCL Industries Inc.)

- Tecnocap Group

- Saudi Arabia Packaging Industry WLL(SAPIN)

- Massilly Holding SAS

- CPMC HOLDINGS Limited(COFCO Group)

第八章投资分析

第9章市场的未来

The Aluminum Cans Market size is estimated at USD 51.20 billion in 2024, and is expected to reach USD 63.90 billion by 2029, growing at a CAGR of 4.53% during the forecast period (2024-2029).

Key Highlights

- Aluminum cans offer long-term food quality preservation benefits. Aluminum cans deliver nearly 100% protection against light, oxygen, moisture, and other contaminants. Aluminum cans do not rust and are corrosion-resistant, providing one of the most extended shelf lives considering any packaging.

- The rising application of aluminum cans in the food and beverage industry can be attributed to their protective properties, sustainability advantages, and consumer convenience. This trend is expected to continue as both manufacturers and consumers recognize the benefits associated with aluminum packaging. Aluminum can be the most recycled material on earth, with around a 100% recyclability rate. Aluminium does not decay throughout the recycling process; thus, it can be recycled numerous times. Recycling aluminum saves millions of tonnes of greenhouse gas emissions, energy, power, and transportation fuel. Producing aluminum cans using recycled materials uses less than 5% of the energy required to produce new aluminum cans from Bauxite.

- Aluminum cans have a higher recycling rate and more recycled content than competing package types. According to the Aluminum Association, it's one of the most recycled materials on the market. In April 2022, Ball Corporation partnered with Recycle Aerosol LLC to boost the recycling rates of aluminum aerosol cans in the United States. The collaboration increases aerosol can recycling and establishes a closed-loop system in which used cans are recycled into new aerosol cans. The production of aluminum goods from recycled aluminum is energy- and carbon-efficient. Because the alloys used to make aluminum aerosols are of high purity, there are efficiency improvements that also lessen the demand for virgin aluminum when they are mainly derived from recycled aluminum aerosol bottles and cans.

- However, aluminum can packaging faces high competition from alternative packaging solutions. Plastic, paper, and glass packaging solutions are the alternative packaging options available in the industry. Also, the increasing importance of e-commerce worldwide is expected to influence the overall packaging industry. Moreover, incremental enhancements in plastic packaging are posing a threat to the market, which can primarily be allocated to the popularity of plastics, such as polyethylene terephthalate (PET), as substitutes. PET plastics threaten to displace aluminum can solutions in the food and beverage sector.

- Meanwhile, consumer trends, such as a preference for small-size and multi-pack packaging formats, support the volume growth of aluminum cans, especially for the ready-to-eat food segment. Hence, most companies across emerging regions offer mini-cans, which usually contain smaller volumes of products at less cost than traditional canned products. For instance, food innovations in canned seafood in Southeast Asia are witnessing significant growth.

- Further, as COVID-19 swept across the world, all industries were affected majorly due to disruption in the supply chains and government-imposed lockdowns in the wake of controlling its spread. Also, the war between Russia and Ukraine resulted in economic sanctions against several countries, high commodity prices, supply chain disruptions, and impacts on many markets worldwide, and caused trade disruptions in the industry. War pushed European aluminum companies to cut production, leading to metal shortages. Commodity traders are competing for scarce profits from shipping aluminum from China as the war in Ukraine has created severe shortages for European manufacturers who rely on Russian supplies. Europe has experienced a surge in energy costs.

Aluminum Cans Market Trends

Increasing Demand for Canned Foods and Beverage Driven by Cost and Convenience-Related Advantages

- Younger populations and individual living consumers are consuming more canned food and beverages. These users have less time and are budget restrained, thus, opting for products with lower costs and higher convenience. Changing lifestyles in developing countries worldwide and the growing rate of urbanization is resulting in consumers opting for easy-to-cook food. Moreover, with the shrinking size of the family, along with the changing patterns in lifestyle, the declining amount of time spent on the preparation of meals and consumption at home is leading to the shift toward more processed, frozen, and pre-prepared foods in which canned foods are the most common form of packaging.

- Aluminum Cans are most widely used for beverages, with the most notable trend of canned wine, cocktails, hard beverages, and soft beverages being packaged in metal, driven by the need for portability in the market. The usage of metal cans in the beverage industry can be widely classified into alcoholic and non-alcoholic drinks based on the nature of the beverage. Alcoholic drinks, such as beer, have historically used metal cans, while other kinds of liquor, like wine, traditionally served in glass bottles, are increasingly adopting metal cans.

- Due to their portability and ease of use, cans are trendy among millennials and GenZ. Additionally, manufacturers are launching the product in can packaging because their design is popular with young people. For instance, 11.582 billion cans of Red Bull were sold worldwide in 2022. This represents an increase of 18.1%. From EUR 7.816 billion (USD 8.52 billion) to EUR 9.684 billion (USD 9.29 billion), group revenue increased by 23.9%.

- Aluminum cans are preferred for food packaging for various reasons, including heat-conductivity, hygiene, and safety, which has made it a convenient choice for the domestic and industrial sectors; owing to this, aluminum cans are widely used in the food industry for the packaging of meat and seafood, fruits and vegetables, ready meals, pet food, soups and condiments, and others. Such a broad end-user market creates significant demand for aluminum cans catering to the food industry. Also, aluminum is extensively used in food contact materials because aluminum-containing food contact materials are an anthropogenic source of dietary aluminum.

- Also, the focus on stockpiling food with long shelf life, owing to the change in consumer behavior as a result of the pandemic, has contributed to the rise in the usage of aluminum cans for packaging food and is expected to leave a long-lasting positive impact on the growth of the studied market. Canned fish sales have boomed since the lockdown period in Europe, particularly in fish-loving Southern European nations such as Spain, France, and Italy. According to Statistics Norway, the consumer price index (CPI) of canned fish in Norway increased in the past few years from 111.4 points in 2018 to 125.3 points in 2022.

- Initiatives by environmental groups and public awareness about the environment have increased awareness among users worldwide. Consumers are increasingly abandoning plastic usage, whereas the demand for recycled products is growing. As a result, it is creating a high demand for metal-packaged products, including aluminum cans.

North America to Hold a Significant Share in the Market

- North America holds the largest market share in revenue due to growing concerns regarding using and consuming sustainable packaging materials. It accounts for over one-third of the total global consumption of aluminum cans.

- There has been a steady growth in products such as sodas, energy drinks, sparkling waters, and, increasingly, craft brew beers. Aluminum cans are one of the most sustainable beverage packages and are infinitely recyclable. They also chill quickly, providing a superior metal canvas to print and, more importantly, protecting the flavor and integrity of your favorite beverages.

- Moreover, the demand for aerosol cans is anticipated to rise along with the personal care sector's expansion in the United States. The growth of the personal care business is primarily related to consumers' increased disposable income and ability to purchase luxury goods. Aerosols are utilized in several personal care products. Thus, the market is projected to profit from their rising sales.

- Additionally, the higher production demands of deodorants/antiperspirants led to the installation of an increasing number of production lines in North America over the past few years. North America accounts for a significant share of the market studied due to the increasing demand from the personal care segment, spanning products of various types, such as deodorants, antiperspirants, hair mousses, hair sprays, shaving mousses, etc. For instance, according to the US Census and Simmons National Consumer Survey (NHCS) data, 298.7 million Americans used deodorants/antiperspirants in 2020. This figure is projected to increase to 306.04 million in 2024.

- Also, as Canada recovered from the pandemic, the Government of Canada provided assistance to its businesses. The government claimed that it was vital to foster a strong and lasting economic recovery by investing in innovation, which could allow the country to achieve its potential for low-carbon growth. The government is expected to invest heavily in helping Canada's aluminum industry eliminate greenhouse gas emissions. They said that zero-carbon aluminum smelting was the kind of innovation thatthat would help meet Canada's economic and climate change objectives.

- Aluminum cans have a higher recycling rate and more recycled content than competing package types. According to the Aluminum Association, it's one of the most recycled materials on the market. Recycling saves more than 90% of the energy required to produce new metal, reducing production costs. In the United States, two aluminum cans are recycled for every three cans shipped across the region.

- Additionally, in April 2022, Ball Corporation announced its strategic partnership with Recycle Aerosol LLC to enhance aluminum aerosol can recycling rates in the United States. The collaboration increases aerosol can recycling and establishes a closed-loop system in which used cans are recycled into new aerosol cans. Utilizing recycled aluminum to manufacture aluminum products is very energy and carbon efficient.

Aluminum Cans Industry Overview

The aluminum cans market is highly fragmented, owing to the presence of various global and local industry players. Some major players are Ball Corporation, Crown Holdings, Inc, Silgan Holdings Inc, Silgan Holdings Inc, and Ardagh Group S.A. Vendors in this market participate based on product portfolio, differentiation, and pricing.

In January 2023, CANPACK, a manufacturer of sustainable packaging solutions, joined the Aluminium Recycling Coalition, established in Dubai by Emirates Global Aluminium (EGA). CANPACK has a significant aluminum can manufacturing facility in the United Arab Emirates (UAE). This Alliance, which brings together key players in the UAE's beverage, waste, and aluminum sectors, teaches people how to reuse used beverage jars most effectively to increase aluminum recycling rates.

In December 2022, Crown Holdings, Inc. announced a collaboration with Aquarius, a refreshing beverage brand produced by Coca-Cola and its dedicated print and reprographics studio, on an intelligent and engaging promotional campaign in Spain. In contrast, Aquarius was available in standard 330ml aluminum cans. This sustainable packaging format advanced a Circular Economy and helped minimize the raw materials required to be sourced from the Earth via its infinite recyclability.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Recyclability Rates of Aluminum Cans

- 5.1.2 Increasing Demand for Canned Foods driven by Cost and Convenience-related Advantages

- 5.2 Market Restraints

- 5.2.1 Availability of Alternative Packaging Solutions

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Slim

- 6.1.2 Sleek

- 6.1.3 Standard

- 6.1.4 Other Types

- 6.2 By End-user Industry

- 6.2.1 Beverage

- 6.2.2 Food

- 6.2.3 Aerosol

- 6.2.4 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Spain

- 6.3.2.5 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 South Korea

- 6.3.3.5 Thailand

- 6.3.3.6 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Mexico

- 6.3.4.3 Rest of Latin America

- 6.3.5 Middle East and Africa

- 6.3.5.1 United Arab Emirates

- 6.3.5.2 Saudi Arabia

- 6.3.5.3 South Africa

- 6.3.5.4 Rest of Middle East & Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Ball Corporation

- 7.1.2 Ardagh Group S.A.

- 7.1.3 Crown Holdings Inc.

- 7.1.4 Silgan Holdings Inc.

- 7.1.5 CAN-PACK SA

- 7.1.6 CCL Container Inc. (CCL Industries Inc.)

- 7.1.7 Tecnocap Group

- 7.1.8 Saudi Arabia Packaging Industry WLL (SAPIN)

- 7.1.9 Massilly Holding SAS

- 7.1.10 CPMC HOLDINGS Limited (COFCO Group)