|

市场调查报告书

商品编码

1435877

鼠李醣脂:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Rhamnolipids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

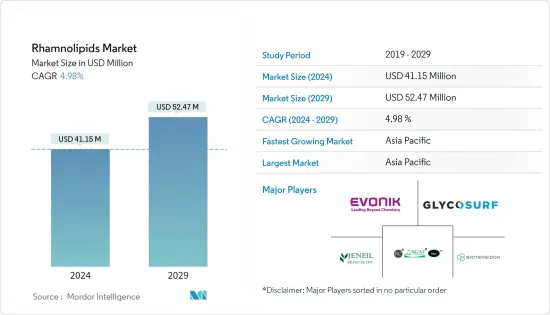

鼠李醣脂市场规模预计到 2024 年为 4,115 万美元,预计到 2029 年将达到 5,247 万美元,在预测期内(2024-2029 年)复合年增长率为 4.98%。

冠状病毒感染疾病(COVID-19) 的传播导致全球封锁、供应链和製造活动崩坏以及生产停顿,所有这些都对 2020 年的市场产生了负面影响。然而,情况在 2021 年开始改善,预计市场将在预测期内恢復上升趋势。

主要亮点

- 推动所研究市场的主要因素是界面活性剂对鼠李醣脂的需求不断增加。此外,个人保健产品需求的增加预计也将刺激市场需求。

- 另一方面,鼠李醣脂的高生产成本阻碍了市场成长。

- 石油和天然气行业对生物表面活性剂的需求不断增长,预计将为预测期内的市场成长提供各种机会。

- 亚太地区是最大的市场,由于中国、印度和日本等国家的消费量不断增加,预计亚太地区将成为预测期内成长最快的市场。

鼠李醣脂市场趋势

界面活性剂对鼠李醣脂的需求不断增加

- 鼠李醣脂生物界面活性剂比合成界面活性剂更容易受到大自然的攻击。它们被认为是合成表面活性剂的更好替代品,因为它们对皮肤温和,具有冲洗作用,并且非常环保。

- 基于鼠李醣脂的清洁剂在耐洗牢度、颜色强度和色差值方面表现出与合成清洁剂相当的清洗性能。

- 鼠李醣脂生物界面活性剂用于清洁剂、地板清洁剂、餐具清洁剂和其他清洗产品。许多公司正在向市场推出使用生物表面活性剂的清洗和清洁剂产品。

- 例如,赢创工业股份公司宣布推出永续鼠李醣脂 REWOFERM RL 100生物界面活性剂,满足清洗解决方案市场对低排放、低影响清洗产品的需求,以永续循环经济。

- 根据德国化妆品、洗护用品、香水和清洁剂协会 IKW 的数据,2022 年德国肥皂和合成清洁剂的收益约为 4.62 亿欧元(约 4.868 亿美元)。

- 此外,根据加拿大统计局的数据,2023年前三个月加拿大肥皂和清洗产品製造商的月销售额为3.9558亿加元(约3.04亿美元),与前一年同期比较增加了约2,000万日元。 。同期销量。

- 根据巴西地区统计研究所预测,2022年巴西肥皂和清洁剂生产收益预计将超过45.2亿美元。该机构还预计 2023 年收益约为 45.6 亿美元。

- 因此,由于上述因素,界面活性剂鼠李醣脂的应用很可能在预测期内成为主导。

亚太地区主导市场

- 目前,由于工业和最终用途的需求,亚太地区在界面活性剂、润滑剂和药品全球市场中占据最大份额。

- 据印度工业和国内贸易促进部称,该国2022年计划对肥皂、化妆品和洗护用品行业的投资约为22.6亿卢比(约2,870万美元)。

- 截至 2022 年 6 月,印度清洁剂市场规模为 1,200 亿印度卢比(约 1.5 亿美元)。国家都市化的不断提高,增加了对更高品质产品的需求。为了满足对优质清洁剂的需求,印度的顶级品牌正在开发包装更好的产品,只需一次洗涤即可提供更多好处。

- 中国也是化妆品的主要消费国之一。 2022年,中国批发零售企业化妆品零售额总计约3,936亿元人民币(约570亿美元)。然而,根据中国国家统计局的数据,这比上年略有下降,当时零售总额约为 4,026 亿元人民币(约 586 亿美元)。

- 此外,根据日本经济产业省的数据,2023 年 4 月国内厕所和洗手剂产量约为 972 万件。

- 此外,印度是全球製药业的重要且不断增长的参与者。印度是全球主要学名药供应国之一,占全球供应量的20%。印度药品出口到全球200多个国家,其中美国是主要市场。此外,印度学名药满足了美国40% 的学名药需求和英国30% 的仿製药需求。国内製药公司由约10,500家公司组成。

- 因此,由于上述因素,亚太地区很可能在预测期内主导鼠李醣脂市场。

鼠李醣脂产业概况

全球鼠李醣脂市场本质上是部分一体化的,只有少数主要企业主导市场。主要企业包括(排名不分先后)Evonik Industries AG、Jeneil、GlycoSurf、AGAE Technologies, LLC 和 Biotensidon GmbH。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 界面活性剂对鼠李醣脂的需求不断增加

- 个人保健产品需求增加

- 其他司机

- 抑制因素

- 鼠李醣脂生产成本高

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代产品的威胁

- 竞争程度

第五章市场区隔(市场规模:数量)

- 类型

- 单鼠李醣脂

- 二鼠李醣脂

- 目的

- 界面活性剂

- 润滑剂

- 农业

- 食品

- 药品

- 其他用途

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲

- 亚太地区

第六章 竞争形势

- 併购、合资、合作与协议

- 市场占有率(%)**/排名分析

- 主要企业采取的策略

- 公司简介

- AGAE Technologies, LLC

- Biosynth

- Biotensidon GmbH

- Evonik Industries AG

- GlycoSurf

- Jeneil

- Merck KGaA

- Rhamnolipid, Inc.

- Stepan Company

- TensioGreen

- Unilever

第七章市场机会与未来趋势

- 石油和天然气产业对生物表面活性剂的需求不断增长

- 其他机会

The Rhamnolipids Market size is estimated at USD 41.15 million in 2024, and is expected to reach USD 52.47 million by 2029, growing at a CAGR of 4.98% during the forecast period (2024-2029).

The COVID-19 outbreak resulted in a global lockdown, a breakdown in supply chains and manufacturing activities, and production halts, all of which had a detrimental effect on the market in 2020. However, things started to get better in 2021, which allowed the market to resume its upward trend for the remainder of the projected period.

Key Highlights

- The major factor driving the market studied is the growing demand for rhamnolipids from surfactants. Moreover, the increasing demand for personal care products is also expected to fuel the market demand.

- On the flip side, the high manufacturing cost of rhamnolipids has hindered the growth of the market.

- The growing demand for bio-surfactants in the oil and gas sector is forecasted to offer various opportunities for the growth of the market over the forecast period.

- Asia-Pacific region represents the largest market and is also expected to be the fastest-growing market over the forecast period owing to the increasing consumption from countries such as China, India, and Japan.

Rhamnolipids Market Trends

Growing Demand of Rhamnolipids from Surfactants

- Rhamnolipid bio-surfactants have the property of getting dreaded easily in nature as compared to synthetic surfactants. They are believed to be a better alternative to synthetic surfactants due to their being skin-friendly, rinse-active, and very environmentally friendly.

- Rhamnolipid-based bio-detergents show comparable washing performance to synthetic detergents in terms of colorfastness to wash, color strength, and the color difference value.

- Rhamnolipid bio-surfactants are used in laundry detergents, floor cleaners, dishwashing liquids, and other cleaning products. Many companies have been introducing bio-surfactant cleaning and detergent products in the market.

- For instance, Evonik Industries AG announced the launch of sustainable rhamnolipid REWOFERM RL 100 biosurfactant meets demand from the cleaning solutions market for low-emission, low-impact cleaning products that enable a circular economy.

- According to IKW, the German Cosmetic, Toiletry, Perfumery and Detergent Association, the revenue from soaps and synthetic detergents in Germany was about EUR 462 million (~USD 486.8 million) in 2022.

- Moreover, according to Statcan, the Canadian Statistics Agency, the monthly manufacturer sales of soap and cleaning compounds in Canada in the first three months of 2023 accounted to be CAD 395.58 million (~USD 304 million), approximately 20% more than the previous year's sales for the same period.

- According to the Brazilian Institute of Geography and Statistics, the revenue generated from the manufacturing of soaps and detergents in Brazil in 2022 is expected to be over USD 4.52 billion. The institution also anticipates revenues of roughly USD 4.56 billion in 2023.

- Hence, owing to the above-mentioned factors, the application of rhamnolipids from surfactant is likely to dominate during the forecast period.

Asia-Pacific Region to Dominate the Market

- Currently, Asia-Pacific accounts for the highest share of surfactants, lubricants, and pharmaceuticals in the global market owing to the demand from the industries and end-use applications.

- According to the Department for Promotion of Industry and Internal Trade in India, the proposed investment value in the soaps, cosmetics, and toiletries sector in the country for year 2022 is around INR 2.26 billion (~USD 28.7 million).

- As of June 2022, the Indian Detergent market size was INR 12,000 crore (~USD 150 million). Due to the increasing urbanization rate in the country, there is an increasing demand for better-quality products. To meet these demands for quality washing powders, the top brands in India are innovating better-packaged products that come with many benefits in a single wash.

- China is also one of the major consumers of cosmetics. In 2022, the retail sales of cosmetics by wholesale and retail companies in China totaled about CNY 393.6 billion (~USD 57 billion). This though, indicated a slight decrease compared to the previous year which had a total retail sale of about CNY 402.6 billion (~USD 58.6 billion), as stated by the National Bureau of Statistics of China.

- Additionally, according to the Ministry of Economy, Trade and Industry in Japan, toilet and hand soap production in the country amounted to around 9.72 million units in the month of April 2023.

- Moreover, in the global pharmaceuticals sector, India is a prominent and expanding player. India is one of the world's major suppliers of generic medicines, accounting for 20% of the global supply by volume. Indian drugs are exported to more than 200 countries in the world, with the United States being the key market. Furthermore, India's generic drugs satisfy 40% of the generic drug demand of the United States and 30% of the United Kingdom. The domestic drug manufacturers consist of a chain of around 10,500 companies.'

- Hence, owing to the above-mentioned factors, Asia-Pacific is likely to dominate the rhamnolipids market during the forecast period.

Rhamnolipids Industry Overview

The global rhamnolipids market is partially consolidated in nature with only few major players dominating the market. Some of the major companies are (not in any particular order) Evonik Industries AG, Jeneil, GlycoSurf, AGAE Technologies, LLC, and Biotensidon GmbH among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand of Rhamnolipids from Surfactants

- 4.1.2 Increasing Demand for Personal Care Products

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Manufacturing Cost of Rhamnolipids

- 4.2.2 Other restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Mono-Rhamnolipids

- 5.1.2 Di-Rhamnolipids

- 5.2 Application

- 5.2.1 Surfactants

- 5.2.2 Lubricant

- 5.2.3 Agriculture

- 5.2.4 Food

- 5.2.5 Pharmaceutical

- 5.2.6 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AGAE Technologies, LLC

- 6.4.2 Biosynth

- 6.4.3 Biotensidon GmbH

- 6.4.4 Evonik Industries AG

- 6.4.5 GlycoSurf

- 6.4.6 Jeneil

- 6.4.7 Merck KGaA

- 6.4.8 Rhamnolipid, Inc.

- 6.4.9 Stepan Company

- 6.4.10 TensioGreen

- 6.4.11 Unilever

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand of Bio-surfactants in Oil and Gas Sector

- 7.2 Other Opportunities

亚太地区槐醣脂和鼠李醣脂市场预测至 2030 年 - 区域分析 - 按类型和应用

亚太地区槐醣脂和鼠李醣脂市场预测至 2030 年 - 区域分析 - 按类型和应用 北美槐醣脂和鼠李醣脂市场预测至 2030 年 - 区域分析 - 按类型和应用

北美槐醣脂和鼠李醣脂市场预测至 2030 年 - 区域分析 - 按类型和应用 南美洲和中美洲槐醣脂和鼠李醣脂市场预测至 2030 年 - 区域分析 - 按类型和应用

南美洲和中美洲槐醣脂和鼠李醣脂市场预测至 2030 年 - 区域分析 - 按类型和应用 欧洲槐醣脂和鼠李醣脂市场预测至 2030 年 - 区域分析 - 按类型和应用

欧洲槐醣脂和鼠李醣脂市场预测至 2030 年 - 区域分析 - 按类型和应用 槐醣脂和鼠李醣脂市场预测至 2030 年:按类型、应用和地区分類的全球分析

槐醣脂和鼠李醣脂市场预测至 2030 年:按类型、应用和地区分類的全球分析 生物界面活性剂市场:按类型、按应用划分:2023-2032 年全球机会分析与产业预测

生物界面活性剂市场:按类型、按应用划分:2023-2032 年全球机会分析与产业预测 全球生物界面活性剂市场规模研究与预测,按类型(醣脂、脂肽)、应用(洗涤剂、个人护理、食品加工、农业化学品等)和区域分析,2023-2030

全球生物界面活性剂市场规模研究与预测,按类型(醣脂、脂肽)、应用(洗涤剂、个人护理、食品加工、农业化学品等)和区域分析,2023-2030 南美洲和中美洲生物表面活性剂市场预测至2030 年- 区域分析- 按类型(槐醣脂、鼠李醣脂、甘露糖赤藻醣醇脂质、烷基多醣糖苷、界面活性剂、磷脂质、聚合物等)和应用

南美洲和中美洲生物表面活性剂市场预测至2030 年- 区域分析- 按类型(槐醣脂、鼠李醣脂、甘露糖赤藻醣醇脂质、烷基多醣糖苷、界面活性剂、磷脂质、聚合物等)和应用 北美生物界面活性剂市场预测至2030 年- 区域分析- 按类型(槐醣脂、鼠李醣脂、甘露糖赤藻醣醇脂质、烷基多醣糖苷、界面活性剂、磷脂质、聚合物等)和应用

北美生物界面活性剂市场预测至2030 年- 区域分析- 按类型(槐醣脂、鼠李醣脂、甘露糖赤藻醣醇脂质、烷基多醣糖苷、界面活性剂、磷脂质、聚合物等)和应用 欧洲生物界面活性剂市场预测至2030 年- 区域分析- 按类型(槐醣脂、鼠李醣脂、甘露糖赤藻醣醇脂质、烷基多醣糖苷、界面活性剂、磷脂质、聚合物等)和应用

欧洲生物界面活性剂市场预测至2030 年- 区域分析- 按类型(槐醣脂、鼠李醣脂、甘露糖赤藻醣醇脂质、烷基多醣糖苷、界面活性剂、磷脂质、聚合物等)和应用