|

市场调查报告书

商品编码

1435916

相转移催化剂:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Phase Transfer Catalyst - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

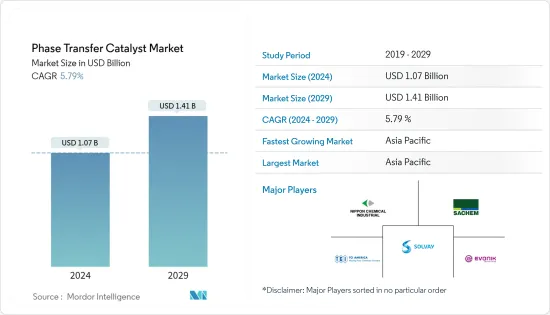

相转移催化剂市场规模预计到 2024 年为 10.7 亿美元,预计到 2029 年将达到 14.1 亿美元,在预测期内(2024-2029 年)增长 5.79%,复合年增长率为

相转移催化剂是将反应物从一个相移动到发生反应的另一个步骤的催化剂。相转移催化剂在製药领域的应用不断增加正在推动市场成长。

主要亮点

- 然而,全球冠状病毒的爆发可能会阻碍所研究市场的成长。

- 相转移催化剂在精细化工和有机中间体生产领域的日益增长的应用很可能为未来五年的相转移催化剂市场提供机会。

- 亚太地区主导了全球市场,最大的消费来自中国和印度等国家。

相转移催化剂的市场趋势

主导市场的药品

- 製药业可能会成为一个主要领域,因为在有机合成中采用绿色化学时,会确保严格的法规要求使用相转移催化剂。

- 在製药工业中,药物中常用相转移催化剂,它是透过一系列化学反应形成的复杂多功能分子。製药业的不断增长预计将推动市场成长。

- 此外,西部地区对医药产业有害化合物使用的严格规定,意味着相转移催化剂在医药产业中不再需要使用有机溶剂和危险、不方便、昂贵的反应物,这也导致消费量增加。

- 此外,COVID-19感染疾病大流行的爆发已成为製药业的主要成长推动者。

- 相转移催化剂提高了化学反应的生产率和产率,因此在一些工业反应中消费量显着增加。预计这将在预测期内推动市场成长。

- 所有上述因素预计将在预测期内推动相转移催化剂市场。

亚太地区主导市场

- 由于相转移催化剂广泛应用于製药和农化产业,亚太地区是最大且成长最快的相转移催化剂市场。

- 根据国际製药工程师协会的数据,亚太地区的药品市场是仅次于北美的全球第二大药品市场。

- 预计亚太地区医药市场在预测期内将以超过 8% 的复合年增长率成长。此外,COVID-19的感染疾病已成为製药业成长的正面因素。

- 亚太地区拥有近30%的地球可用土地和60%的人口。该地区的人口结构在维持农业实践的适宜性方面发挥重要作用,预计这将导致该地区农化产品的利用率增加,进一步推动市场成长。

- 因此,所有这些市场趋势预计将在预测期内推动该地区相转移催化剂市场的需求。

相转移催化剂产业概述

全球相转移催化剂市场本质上是分散的,因为市场参与者众多,但市场占有率并不大。主要企业包括 SACHEM, Inc.、TCI、 工业、Evonik Industries AG 和 Solvay。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 拓展相转移催化剂在医药领域的应用

- 其他司机

- 抑制因素

- 由于COVID-19感染疾病的爆发,情况不利

- 其他限制

- 产业价值链分析

- 波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代产品的威胁

- 竞争程度

第五章市场区隔

- 类型

- 铵盐

- 鏻盐

- 其他的

- 最终用户产业

- 药品

- 化学品

- 农药

- 其他的

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 中东和非洲其他地区

- 亚太地区

第六章 竞争形势

- 併购、合资、合作与协议

- 市场占有率/排名分析

- 主要企业采取的策略

- 公司简介

- Alfa Aesar, Thermo Fisher Scientific.

- Cayman Chemical

- Central Drug House

- Dishman Group

- Evonik Industries AG

- Nippon Chemical Industrial CO., LTD

- SACHEM, Inc.

- Solvay

- Strem Chemicals, Inc.

- Tatva Chintan Pharma Chem Private Limited

- TCI

第七章市场机会与未来趋势

- 扩大精细化学品和有机中间体生产的应用

- 其他机会

The Phase Transfer Catalyst Market size is estimated at USD 1.07 billion in 2024, and is expected to reach USD 1.41 billion by 2029, growing at a CAGR of 5.79% during the forecast period (2024-2029).

Phase transfer catalyst is a catalyst that enables the movement of the reactant from one phase to another step where the reaction occurs. The increasing application of phase transfer catalyst in the pharmaceutical sector has been driving the market growth.

Key Highlights

- However, the outbreak of coronavirus across the globe is likely to hinder the growth of the studied market.

- The growing application of phase transfer catalyst in the field of manufacturing of the fine chemicals and organic intermediates are likely to provide opportunities for the phase transfer catalyst market over the next five years.

- Asia-Pacific dominated the market across the globe with the largest consumption from countries such as China and India.

Phase Transfer Catalyst Market Trends

Pharmaceutical to Dominate the Market

- Pharmaceutical stand to be the dominating segment owing to ensure stringent regulations mandating the use of phase transfer catalyst as the adoption of green chemistry in organic synthesis.

- In the pharmaceutical industry, the phase transfer catalyst is used for medicines which are typically complex multifunctional molecules that are formed by a series of chemical reactions. Increased growth in the pharmaceutical industry is expected to drive the market growth.

- In addition, imposing stringent regulations on the use of harmful compounds in the pharmaceutical industry in the western regions also leads to increased consumption of phase transfer catalysts in the pharmaceutical industry, as they eliminate the need to use organic solvents and dangerous, inconvenient and expensive reactants.

- Further, the outbreak of COVID-19 pandemic disease has become a huge growth catalyst for the pharmaceutical industry.

- Phase transfer catalyst is witnessing a strong rise in consumption in several industrial reactions as it improves productivity and yield of a chemical reaction. This anticipates propelling market growth in the forecast period.

- All the aforementioned factors are expected to drive the phase transfer catalyst market during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia Pacific region stands to be the largest and fastest-growing market for phase transfer catalyst owing to wide usage in the pharmaceutical and agrochemical industry.

- According to the International Society for Pharmaceutical Engineering, the Asia Pacific pharmaceutical market is the second-largest in the world after North America.

- The pharmaceutical market in the Asia-Pacific region is projected to record a CAGR of more than 8% during the forecast period. Furthermore, the outbreak of COVID-19 disease becomes a positive factor for the growth of the pharmaceutical industry.

- Asia-Pacific accounts for almost 30% of land available on earth and 60% of the human population. Population statistics in the region have been responsible for maintaining adequacy in agricultural practices, resulting in greater utilization of agrochemical products in the region which further anticipated to propel the market growth.

- Hence, all such market trends are expected to drive the demand for the phase transfer catalyst market in the region during the forecast period.

Phase Transfer Catalyst Industry Overview

The global phase transfer catalyst market is fragmented in nature owing to the presence of numerous players in the market with no significant market share. Some of the major companies are SACHEM, Inc., TCI, Nippon Chemical Industrial CO., LTD, Evonik Industries AG, and Solvay amongst others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Application of Phase Transfer Catalyst in Pharmaceutical Sector

- 4.1.2 Other Drivers

- 4.2 Restraints

- 4.2.1 Unfavorable Conditions Arising Due to COVID-19 Outbreak

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Ammonium Salts

- 5.1.2 Phosphonium Salts

- 5.1.3 Others

- 5.2 End-user Industry

- 5.2.1 Pharmaceutical

- 5.2.2 Chemical

- 5.2.3 Agrochemical

- 5.2.4 Others

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share/Ranking Analysis**

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Alfa Aesar, Thermo Fisher Scientific.

- 6.4.2 Cayman Chemical

- 6.4.3 Central Drug House

- 6.4.4 Dishman Group

- 6.4.5 Evonik Industries AG

- 6.4.6 Nippon Chemical Industrial CO., LTD

- 6.4.7 SACHEM, Inc.

- 6.4.8 Solvay

- 6.4.9 Strem Chemicals, Inc.

- 6.4.10 Tatva Chintan Pharma Chem Private Limited

- 6.4.11 TCI

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Application in Manufacturing of the Fine Chemicals and Organic Intermediates

- 7.2 Other Opportunities