|

市场调查报告书

商品编码

1435954

服务履行 - 市场占有率分析、产业趋势与统计、成长预测(2024 年 - 2029 年)Service Fulfillment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

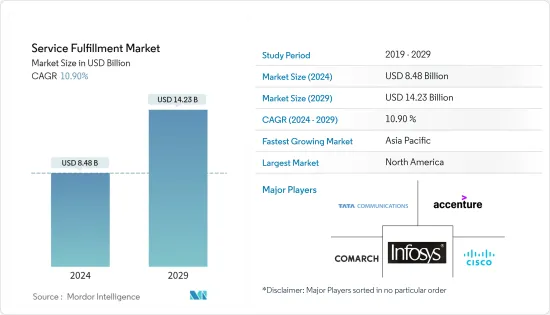

2024年服务履行市场规模预计为84.8亿美元,预计到2029年将达到142.3亿美元,在预测期内(2024-2029年)CAGR为10.90%。

由于跨行业引入了多种技术,服务提供者正在建立提供服务的能力,同时缩短下一代产品和服务的上市时间。物联网、连网设备、5G 技术、数位化等技术增加了对增强连接解决方案的需求。

主要亮点

- 服务履行是一套综合工具,可协助简化 CSP 和组织的各种任务,以缩短上市时间、优化成本并提高自动化程度。网路优化对于满足新的和不断增长的服务履行需求至关重要。

- 动态服务履行流程或软体可以建立基于元件的服务并简化新产品的发布。它使订单到现金流程自动化,以优化供应链活动、资本支出和营运费用。供应链管理解决方案简化了网路设备采购,同时合理化了供应商生态系统。

- 快速的连接设备和用户扩张推动了全球服务履行市场。此外,该产业对电信营运技术的大规模支出需求不断增加。此外,轻鬆存取关键管理解决方案正在推动该行业向前发展。资料服务收入的成长推动了全球服务履行市场的需求。

- 此外,自动化可以提高企业生产力,这始终是人们所希望的。挑战在于以具有成本效益的方式实现这一目标。云端有效地简化了 IT 基础架构的自动化和使用,例如伺服器虚拟化和配置。儘管如此,由于复杂性较高,网路自动化的发展速度较慢,尤其是在通讯服务供应商(CSP) 网路中,这些网路通常跨越越来越多的领域(云端、行动、WAN 和IT),并且需要更高水准的投资。

- COVID-19 大流行影响了全球的服务履行。大流行期间的主要挑战是与劳动力相关的问题。大流行后,随着虚拟化网路功能迅速采用可用元件以创建客户服务,市场迅速成长。

服务履行市场趋势

分析软体细分市场占有重要市场份额

- 分析包括网路管理、库存管理和服务订单管理在内的软体部分,在预测期内在服务履行市场中占据重要的市场份额。随着5G 技术、物联网、人工智慧、数位化等多项技术进步的推出,通讯服务供应商(CSP) 面临着持续的压力,需要增强和超越不断增长的客户期望,同时最大限度地降低营运成本,而且跨平台、系统的可见性很少、工具和碎片资料。

- 爱立信预计,到2028年,全球5G用户数将增加至46.2411亿,其中东北亚、东南亚、印度、尼泊尔和不丹预计将成为地区用户数最多的地区。随着用户数量的不断增加,5G连线数、随着互联设备、行动装置、应用程式以及先进技术和功能的部署,他们越来越依赖增强的网路基础设施和增强的连接解决方案,以实现与各种端点的基本连接。

- 随后,组织和通讯服务供应商越来越多地投资于新的网路架构,这些架构结合了先进的管理工具,利用人工智慧和机器学习等技术来推动自主网路的采用。因此,CSP 正在联繫服务履行解决方案供应商,透过采用软体解决方案来增强其供应链活动。

- 市场的另一个趋势是,由于网路流量和网路处理的增加,特别是来自区域网路的网路流量和网路处理的持续评估和效能的需求,这需要即时串流网路分析并允许客户追踪其网路的运作状况。网路并持续监控流量。这些发展进一步促进了市场对网路管理软体的需求。

北美有望成为最大市场

- 由于对跨各种平台(例如视讯串流、视讯通话平台和电话会议等)的增强连接解决方案的需求增加,北美地区对服务履行解决方案和服务的需求正在增加。

- 再加上3G、4G、5G等各种网路上用户的快速成长,推动玩家采用服务履行。此外,该地区已成为 5G 部署的主要枢纽,加拿大服务提供者越来越多地投资购买 5G 牌照。

- 市场供应商正在进行合作和收购活动,以加强其在该地区的服务履行产品,并对其进行分析以推动该地区的市场成长。例如,2023年5月,科技驱动的物流平台Flexport收购了Shopify Logistics的资产,包括Deliverr, Inc。透过整合Shopify Logistics,该公司将加强其先进的人工智慧驱动优化,以简化全球供应链,降低成本并提高消费者的可靠性。

- 此外,2022 年12 月,JLL 和American Eagle Outfitters Inc. 全资子公司Quiet Platforms 宣布合作,将于2023 年在美国各地加速建造更多先进的履行设施,为Quiet Platforms 供应链中的零售商和品牌提供服务网路。根据协议条款,两家公司将针对物流房地产开创灵活的租金占收入百分比的模式。

服务履行产业概述

服务履行市场因Comarch SA、Accenture PLC、Cisco Systems, Inc.、Infosys Limited 和TATA Communications Ltd. 等多家参与者的存在而呈碎片化。市场中的参与者正在采取合作伙伴关係和收购等策略来增强其产品供应并获得可持续的竞争优势。

2023 年12 月- Infosys 宣布,透过与Infosys 共同建构的全通路数位履行和高级分析平台,并利用Infosys 的AI 优先产品Infosys Topaz,Spotlight Retail Group 实现了超个人化的线上服务,帮助增强了Spotlight Retail Group 的消费者成长为消费者带来购物体验。客户体验的改善使得客户群在 12-12 个月期间成长了 113%,交易量增加了 93%。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设和市场定义

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 替代产品的威胁

- 竞争激烈程度

- COVID-19 对市场的影响评估

第 5 章:市场动态

- 市场驱动因素

- 网路自动化程度不断提高,对自动化即时服务的需求不断增加

- 将虚拟化网路功能快速采用到可用元件中以建立客户服务

- 市场限制

- 缺乏意识

第 6 章:市场细分

- 按类型

- 软体

- 网路管理

- 库存管理

- 服务订单管理

- 服务

- 软体

- 按部署模式

- 本地部署

- 主办

- 按地理

- 北美洲

- 欧洲

- 亚太

- 世界其他地区

第 7 章:竞争格局

- 公司简介

- Comarch SA

- Accenture PLC

- Cisco Systems, Inc.

- Infosys Limited

- TATA Communications Ltd.

- Amdocs Group

- Suntech SA

- Telefonaktiebolaget LM Ericsson

- NEC Technologies India Private Limited

- Hewlett Packard Enterprise Development LP

- TIBCO Software Inc.

第 8 章:投资分析

第 9 章:市场机会与未来趋势

The Service Fulfillment Market size is estimated at USD 8.48 billion in 2024, and is expected to reach USD 14.23 billion by 2029, growing at a CAGR of 10.90% during the forecast period (2024-2029).

Service providers are building capabilities to provide services while reducing time-to-market for next-generation products and services, owing to the introduction of several technologies across industries. Technologies such as IoT, connected devices, 5G technology, digitization, and increase the demand for enhanced connectivity solutions.

Key Highlights

- Service fulfillment is a combined comprehensive set of tools that assist in streamlining various tasks of CSPs and organizations to reduce time to market, optimize cost, and boost automation. Network optimization becomes essential to meet new and growing service fulfillment needs.

- A dynamic service fulfillment process or software enables the creation of component-based services and simplifies the launch of new products. It automates the order-to-cash process to optimize supply chain activities, capital expenditures, and operating expenses. The supply chain management solutions streamline network equipment procurement while rationalizing the supplier ecosystem.

- Rapid connectivity devices and user expansion drive the global service fulfillment market. Moreover, large-scale expenditures in telecom operating technologies are increasing in demand in this industry. Moreover, simple access to crucial management solutions is propelling this industry forward. Rising income from data services drives demand in the global service fulfillment market.

- Further, automation drives business productivity, which is always desirable. The challenge is achieving it cost-effectively. The cloud has efficiently streamlined the automation and use of IT infrastructures, such as server virtualization and configuration. Still, network automation has been slower to evolve due to higher complexity levels, especially among communication service provider (CSP) networks, which often cross an increased number of domains (cloud, mobile, WAN, and IT) and require higher levels of investment.

- The COVID-19 pandemic impacted service fulfillment throughout the globe. The major challenge during the pandemic was workforce-related issues. Post-pandemic, the market was growing rapidly with the rapid adoption of virtualized network functions into usable components for customer service creation.

Service Fulfillment Market Trends

Software Segment is Analyzed to Hold Significant Market Share

- The software segment including network management, inventory management and service order management is analyzed to hold significant market share in th service fulfillment market over the forecast period. The rollout of several technological advancements, such as 5G technology, IoT, AI, Digitization, and many more, Communication Service Providers (CSPs) face constant pressure to enhance and exceed rising customer expectations while minimizing operational costs, with little visibility across platforms, systems, tools, and fragmented data.

- According to Ericsson, 5G subscriptions are forecast to increase globally to 4624.11 million by 2028, North East Asia, South East Asia, India, Nepal, and Bhutan are expected to have the maximum regional subscriptions.With the increasing number of users, 5G connections, connected devices, mobile devices, applications, and the deployment of advanced technologies and capabilities, they are increasing their dependence on enhanced network infrastructure and enhanced connectivity solutions for essential connectivity to a wide range of endpoints.

- Subsequently, organizations and CSPs are increasingly investing in new network architectures that incorporate advanced management tools to drive the adoption of autonomous networks, leveraging technologies like AI and ML. Hence, the CSPs are contacting Service Fulfillment solution providers to enhance their supply chain activities by adopting software solutions.

- Another trend in the market is the demand for continuous evaluation and performance of networks due to increased network traffic and network processing, particularly from the local area networks, which require real-time streaming network analytics and allows customers to keep track of the health of their network and continuously monitor traffic flows. Such developments further fosters the demand for network management software in the market.

North America is Expected to Register the Largest Market

- The North America region is witnessing an increase in the demand for service fulfillment solutions and services due to an increase in the demand for enhanced connectivity solutions across various platforms, such as video streaming, video calling platforms, and teleconferencing, among various others.

- This, coupled with a rapid increase in subscribers on various networks such as 3G, 4G, 5G, etc., propel the players to adopt service fulfillment. Also, the region has become a major hub for the 5G rollout, with Canadian service providers increasingly investing in procuring 5G licenses.

- Market vendors are entering into partnership and acquisition activities to strengthen their service fulfillment offerings in the region, which is analyzed to drive the market growth in the region. For instance, in May 2023, Flexport, the tech-driven logistics platform, acquired the assets of Shopify Logistics, including Deliverr, Inc. Through the integration of Shopify Logistics, the company will strengthen its advanced AI-driven optimization to streamline the global supply chain, reducing costs and improving consumer reliability.

- Furthermore, in December 2022, JLL and Quiet Platforms, an American Eagle Outfitters Inc. completely owned subsidiary, announced a collaboration to speed the building of additional advanced fulfillment facilities across the United States in 2023 to service retailers and brands in the Quiet Platforms supply chain network. The two businesses would pioneer a flexible rent-as-a-percentage-of-revenue model for logistics real estate under the terms of the agreement.

Service Fulfillment Industry Overview

The Service Fulfillment Market is fragmented with the presence of several players like Comarch SA, Accenture PLC, Cisco Systems, Inc., Infosys Limited, and TATA Communications Ltd. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

In December 2023 - Infosys announced that it has helped enhance Spotlight Retail Group's consumer growth via an omnichannel digital fulfillment and advanced analytics platform built with Infosys and by leveraging Infosys' AI-first offering, Infosys Topaz, Spotlight Retail Group enabled a hyper-personalized online shopping experience for its consumers. The improved customer experience has led to a growth of 113% in customer base over 12 12-month period and 93% in transactions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Network Automation and Increasing Demand for Automated, Real-time Services

- 5.1.2 Rapid Adoption of Virtualized Network Functions into Usable Components for Customer Service Creation

- 5.2 Market Restraints

- 5.2.1 Lack in Awareness

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Software

- 6.1.1.1 Network Management

- 6.1.1.2 Inventory Management

- 6.1.1.3 Service Order Management

- 6.1.2 Services

- 6.1.1 Software

- 6.2 By Deployment Mode

- 6.2.1 On-Premise

- 6.2.2 Hosted

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Comarch SA

- 7.1.2 Accenture PLC

- 7.1.3 Cisco Systems, Inc.

- 7.1.4 Infosys Limited

- 7.1.5 TATA Communications Ltd.

- 7.1.6 Amdocs Group

- 7.1.7 Suntech S.A.

- 7.1.8 Telefonaktiebolaget LM Ericsson

- 7.1.9 NEC Technologies India Private Limited

- 7.1.10 Hewlett Packard Enterprise Development LP

- 7.1.11 TIBCO Software Inc.