|

市场调查报告书

商品编码

1435962

资料弹性:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Data Resiliency - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

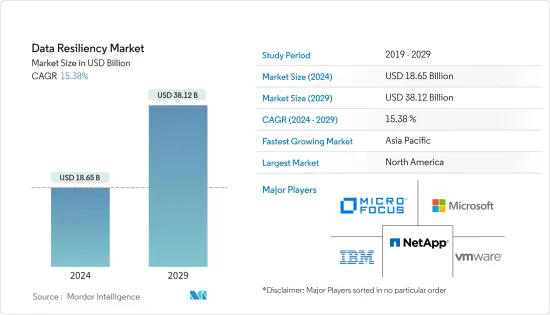

资料弹性市场规模预计到 2024 年为 186.5 亿美元,预计到 2029 年将达到 381.2 亿美元,预测期内(2024-2029 年)复合年增长率为 15.38%。

随着已开发国家和新兴国家的网路普及迅速提高,资料漏洞不断增加,这主要是由于所有行动装置无线网路的扩展。因此,资料弹性有望成为世界上每个组织的重要组成部分。

主要亮点

- 去年,网路攻击的数量激增。这迫使企业将安全放在首位。服务供应商现在正在竭尽全力保护客户的服务基础设施。重要的是,该解决方案不仅实现了安全解决方案,而且还具有防御所有类型攻击并快速恢復的能力。

- 世界各地的企业和政府机构正在从测试环境转向将许多业务关键型工作负载和运算实例放置在云端。此外,作为数位转型策略的关键部分,物联网、云端和巨量资料分析在多个组织中的迅速采用也增加了资料中心的压力,从而导致市场成长。

- 根据 Datrium Inc. 的报告《2019 年企业资料弹性与灾难灾害復原状况》,超过 50% 的受访者表示他们的组织曾回答我经历过灾难復原事件。此外,89% 的 IT 领导者表示勒索软体是其组织资料安全的主要威胁。 IT 领导者也表示,他们对此最大的担忧是生产力下降 (74%) 以及在这种情况下无法经营业务 (65%)。

- 无论是本地、公有、私有或混合模式,转向多重云端架构都变得越来越普遍。 Teradici Corporation 的一项研究表明,目前超过一半的 IT 专业人员在多重云端环境中业务,近十分之一的人在其组织内使用五个或更多云。

- 目前,世界各地的各个企业都在专注于管理冠状病毒大流行的影响,并正在建立更新、更强大的业务,以确保面对当前和未来的破坏性事件时的业务弹性。我们正在考虑实用的方法。主动的业务连续性和弹性策略对于实现数位业务至关重要。这主要需要在基础设施中建立强大的弹性,同时减少停机时间和相关成本。

资料弹性市场趋势

BFSI 细分市场预计将大幅成长

- 由于庞大的客户群和金融资讯受到威胁,金融业是遭受多次资料外洩和网路攻击的重要产业之一。

- 资料外洩会导致成本飙升和有价值的客户资讯遗失。根据 Verizon 发布的 2019 年资料外洩调查报告,金融服务和保险领域的所有网路事件中有 88% 是出于经济动机。网路攻击者寻求以最简单的方式获取经济利益,攻击金融服务业。

- 为了保护其 IT 流程和系统、保护客户的关键资料并遵守政府法规,私人和公共银行机构都在寻求防止这些攻击并更快地恢復。我们专注于实施最新技术。此外,客户期望的提高、技术力的提高和监管要求也迫使银行机构采取积极主动的安全措施。

- 此外,最近的冠状病毒爆发影响了世界各地的金融市场和机构。在这样的时期,BFSI 部门需要製定紧急时应对计画来应对这场流行病带来的所有威胁,这预计将增加该行业对资料復原解决方案的需求。

预计北美将占据重要市场占有率

- 北美地区已成为全球所有主要组织的主要枢纽。多个行业的扩张和连网型设备的快速成长正在推动该地区对弹性解决方案的需求。

- 此类攻击的风险增加,可能影响从个人到企业再到政府的市场。因此,保护敏感资料在该地区变得非常重要。据白宫经济顾问委员会称,有害网路活动每年给美国经济造成约 570 亿美元至 1,090 亿美元的损失。

- 就在 2019 年 10 月,该国 DCH Health Systems 营运的三家医疗服务提供者遭到名为 Ryuk 的勒索软体攻击。所有这些医疗中心都已实施紧急程序以确保患者安全,该公司正在努力诊断攻击。预计该国所有行业的此类网路攻击都会增加,这可能会增加市场对弹性解决方案的需求。

- 此外,2020 年 3 月,为弹性企业提供安全多重云端资料平台的供应商 Datrium 宣布在资料弹性和耐用性、伺服器重复资料删除、增强储存效能、加密方面取得进步,并宣布已获得五项新的美国专利为了安全。压缩和资料路径监控提高了网路弹性。

资料弹性产业概述

资料弹性市场竞争非常激烈,因为市场上有多家供应商为国内和国际市场提供服务。该市场似乎适度集中,参与者采取产品创新、併购和策略合作伙伴关係等策略来扩大影响力并保持市场竞争力。市场参与者包括 IBM 公司、微软公司和 NetApp 公司。

- 2020 年 6 月 - 全球领先的跨云端和本地环境资料管理企业软体供应商 Commvault 宣布与 Microsoft 达成一项多年协议,以整合上市、工程和服务。使用 Microsoft Azure 销售该公司的 Metallic 软体即服务 (SaaS)资料保护产品组合。它主要透过简单的 SaaS 管理提供规模和可靠的安全性。

- 2020 年 6 月 - 网路保护公司 Acronis 宣布与亚太地区领先的网路安全经销商之一 ACE Pacific Group 建立多年合作伙伴关係。此次合作主要是透过 ACE Pacific Group 广泛的销售管道提供对 Acronis 网路保护解决方案的全面存取。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 市场驱动因素

- 多个来源产生的资料快速成长

- 日益增长的隐私问题和日益增长的资料安全需求

- 市场限制因素

- 开放原始码方案的可用性

- 波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代产品的威胁

- 竞争公司之间的敌意强度

第五章市场区隔

- 按发展

- 本地

- 云

- 按最终用户/行业

- BFSI

- 资讯科技和通讯

- 政府

- 製造业

- 卫生保健

- 其他最终用户

- 地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第六章 竞争形势

- 公司简介

- Acronis International GmbH

- Asigra Inc.

- Carbonite, Inc.(OpenText Corporation)

- CenturyLink, Inc.

- Commvault Systems, Inc.

- IBM Corporation

- Microsoft Corporation

- NetApp, Inc.

- Veritas Technologies LLC

- VMware, Inc.(Dell Technologies Inc.)

- Micro Focus International plc

第七章 投资分析

第八章市场机会及未来趋势

The Data Resiliency Market size is estimated at USD 18.65 billion in 2024, and is expected to reach USD 38.12 billion by 2029, growing at a CAGR of 15.38% during the forecast period (2024-2029).

With the rapidly increasing penetration of the internet among developed and developing countries, also the expanding wireless network for all the mobile devices has primarily increased the vulnerability of data, which is expected to make data resiliency an essential and integral part of every single organization across the globe.

Key Highlights

- The previous year has seen a rapid increase in the number of cyberattacks. This has forced companies to adopt security-first thinking. The service providers are now putting much more effort in order to secure the service infrastructure of their clients. The solutions are not only about having a security solution in place but also the ability to defend and recover fast against any type of attack.

- Enterprises and government organizations across the globe are moving from test environments to placing more of their work-critical workloads and compute instances into the cloud. Further, owing to the rapidly increasing adoption of IoT, cloud, and big data analytics across multiple organizations as a major part of their digital transformation strategy, the burden on the data centers is also increasing leading to the growth of the market.

- According to Datrium Inc. report, 'The State of Enterprise Data Resiliency and Disaster Recovery 2019, more than 50% of the respondents indicated that their organization experienced a DR event in the past 24 months. Moroever, 89% of the IT leaders reported that ransomware is the major threat to organizations' data security. The IT leaders also expressed that their top concerns regarding this was the loss of productivity (74%) and the inability to operate their businesses (65%) under these circumstances.

- Whether on-premise, public, private, or a hybrid model, the move towards a multi-cloud architecture is increasingly becoming popular. A research from Teradici Corporation has revealed that more than half of the IT professionals are currently operating in a multi-cloud environment, with almost one in every ten using five or more clouds within their organizations.

- Various enterprises across the globe are currently focused on managing the impact of the coronavirus pandemic and are looking at newer and robust practices in order to help ensure their business resiliency now and during any other future disruptive events. A proactive business continuity and resiliency strategy is becoming very crucial to enable digital businesses, which primarily requires building a robust resiliency into the infrastructure, while reducing downtime and associated costs.

Data Resiliency Market Trends

BFSI Segment is Expected to Witness Significant Growth

- The financial industry has been one of the critical sectors that suffer several data breaches and cyber-attacks, owing to the large customer base that the industry serves and the financial information that is at stake.

- Data breaches lead to an exponential rise in costs and loss of valuable customer information. According to the data breach investigations report, 2019, released by Verizon, 88 percent of all cyber incidents in the financial services and insurance sector were done with financial motivation. Cyber attackers in pursuit of the easiest path possible to financial gain attack the financial services industry.

- With an aim to secure their IT processes and systems, secure customer critical data, and comply with government regulations, both private and public banking institutes are focused on implementing the latest technology to prevent these attacks and recover faster. Additionally, with greater customer expectation, growing technological capabilities, and regulatory requirements, banking institutions are pushed to adopt a proactive approach to security.

- Moreover, the recent coronavirus outbreak has affected the financial markets and institutions across the globe. In these times, the BFSI sector's must have contingency plans put in place in order to meet all the threats that is being posed posed by this pandemic, which is expected to drive the demand for data resiliency solutions in the industry.

North America is Expected to Hold a Significant Market Share

- The North American region has been a primary hub for all the major organizations across the globe. The expansion of the multiple industries and the rapid growth of connected devices is driving the demand for resiliency solutions in the region.

- The rising risks of such attacks that can impact the market vary from individuals to corporates to the governments. Thus, securing crucial data has become very crucial in the region. According to the White House Council of Economic Advisers, the United States economy loses approximately USD 57 billion to USD 109 billion per year to harmful cyber activity.

- Recently in October 2019, the three healthcare providers operated by DCH Health Systems in the country were attacked by ransomware strain known as Ryuk. All these healthcare centers have implemented emergency procedures to ensure the safety of their patients, and the company is working on the attack diagnosis. Such cyber-attacks are expected to increase in the country across the domains, which may fuel the demand for resiliency solutions in the market.

- Moreover, in Mar 2020, Datrium, a provider of the secure multicloud data platform for the resilient enterprise, announced it has been awarded with five new US patents for data resiliency and durability, advancements in server-powered deduplication, enhanced storage performance, encryption and compression, and data path monitoring for improved network resilience.

Data Resiliency Industry Overview

The Data Resiliency Market is highly competitive owing to the presence of multiple vendors in the market providing services to domestic and international markets. The market appears to be moderately concentrated with players adopting strategies such as product innovation, mergers, and acquisitions, strategic partnerships in order to expand their reach and stay competitive in the market. Some of the players in the market are IBM Corporation, Microsoft Corporation, NetApp, Inc., among others.

- Jun 2020 - Commvault, a prominent global enterprise software provider in the management of data across the cloud and on-premise environments, announced that it has entered into a multi-year agreement with Microsoft that will integrate the go-to-market, engineering and sales of the company's Metallic Software-as-a-Service (SaaS) data protection portfolio with Microsoft Azure, primarily delivering scale and trusted security with simple SaaS management.

- Jun 2020 - Acronis, a player in the cyber protection domain, announced the signing of a multiyear partnership with ACE Pacific Group, which is one of the APAC region's cybersecurity distributors. The partnership will primarily enable the full access to Acronis' cyber protection solutions across the ACE Pacific Group's wide distribution channels.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Growth in Data being Generated from Multiple Sources

- 4.2.2 Increasing Privacy Concerns and Rising Need for Data Security

- 4.3 Market Restraints

- 4.3.1 Availability of open-source alternatives

- 4.4 Porters 5 Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Deployment

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.2 By End-user Vertical

- 5.2.1 BFSI

- 5.2.2 IT & Telecommunication

- 5.2.3 Government

- 5.2.4 Manufacturing

- 5.2.5 Healthcare

- 5.2.6 Other End-user Vertical

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Latin America

- 5.3.5 Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Acronis International GmbH

- 6.1.2 Asigra Inc.

- 6.1.3 Carbonite, Inc. (OpenText Corporation)

- 6.1.4 CenturyLink, Inc.

- 6.1.5 Commvault Systems, Inc.

- 6.1.6 IBM Corporation

- 6.1.7 Microsoft Corporation

- 6.1.8 NetApp, Inc.

- 6.1.9 Veritas Technologies LLC

- 6.1.10 VMware, Inc. (Dell Technologies Inc.)

- 6.1.11 Micro Focus International plc