|

市场调查报告书

商品编码

1644422

应用控制:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Application Control - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

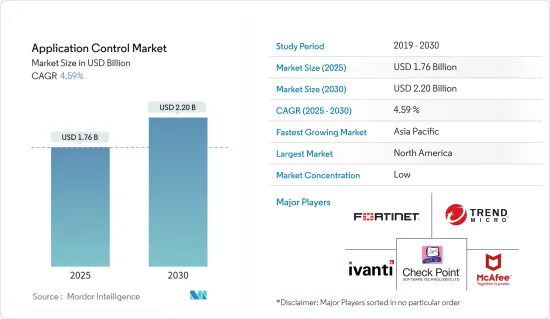

预计 2025 年应用控制市场规模为 17.6 亿美元,到 2030 年将达到 22 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.59%。

网路攻击的增加、连接设备和网路基地台的大量增加大大增加了对更好的业务应用程式监控和控制的需求。因此,对全面的端点访问保护和覆盖的需求急剧增加,使得其在各行各业中受到欢迎。

主要亮点

- 网路攻击的增加以及连接设备和网路基地台的增加,大大增加了对企业应用程式进行加强监控和控制的需求。因此,对全面的端点存取安全和覆盖的需求急剧增加,使得它在各行各业中受到欢迎。因此,应用程式控制市场中的各种市场参与企业现在提供广泛的商业产品,透过启用各种控制(包括执行、监控和身份验证)来实现对企业应用程式的高级保护。

- 此外,基于应用程式控制的解决方案提供广泛的用途,包括网路安全、伺服器管理、端点保护和身分验证,同时也为最终使用组织带来好处。过去几年来,应用程式控制获得了很大的发展动力,这主要是由于平衡负载、提高效能和处理与应用传输相关的更高级要求的需求日益增长。这些解决方案提供了保持您的应用程式和伺服器正常运作所需的可用性、可扩展性、效能、安全性、自动化和控制。

- 这些功能还可以帮助想要迁移或已经迁移到云端环境的组织。数位转型正在推动新的架构和优化工作。这对 ADC 的影响是巨大的,因为它们对于应用程式架构和 IT 最佳化至关重要。例如,几乎所有电子商务网站都使用应用程式交付控制器来提高其应用程式的可用性和可靠性。如今,企业和公司一样,都在经历数位转型。网站的可靠性、灵活性、可扩展性和效能对于您的网站基础架构和您的业务同样重要。

- 资料流量的快速爆炸性成长要求网路系统能够容纳增加的应用层流量。市场上现有的解决方案必须应对这些类型的巨大负载。扩展应用程式的需求不断增加,这些应用程式在许多情况下由来自不同供应商的解决方案组成,并且向网路添加新服务会增加网路复杂性和故障点。因此,向用户提供这些服务可能会变得更加复杂,并且会出现严重的延迟,这可能导致收益来源的损失和用户体验的下降。

- COVID-19 疫情对多个关键 IT 和技术领域产生了长期影响。例如,几家 IT 和其他大型科技公司预计製造业、服务业、医疗保健和零售业等各行业的商业合约数量将下降。然而,由于其在公共事业和必要的日常业务中的重要性,BFSI、IT和电信、航太和国防等重要业务在疫情期间在各国受到的影响较小。

应用控制市场趋势

零售预计将占据很大市场份额

- 随着网路化的提升、多通路业务的发展、智慧零售应用解决方案的演进,零售市场变得充满活力。此外,电子商务的快速崛起使得商业情报能够追踪用户与电子商务商店的互动方式,并且可以进一步利用这些资讯来改善客户购物和服务体验。电子商务也使零售商能够根据顾客行为做出更明智、更有效的决策。这些资料是即时提供的,有助于企业快速调整价格或更改产品供应。这些发展使得网路购物更具吸引力,零售商正在采用应用程式控制器来减少载入时间。

- 零售业中物联网连接设备的数量正在呈指数级增长。例如,根据ENTO的报告,在欧盟地区,2019年零售业使用的连网型设备数量为228万台,预计2025年将成长到309万台。亚马逊还在其西雅图总部附近开设了一家名为 Amazon Go 的实体杂货店。实体店将使用新设计的摄影机、感测器和智慧型手机组成的广泛网路来准确确定每个消费者从货架上挑选哪些商品。识别产品后,该技术会将其添加到数位购物车中。零售业的这些发展推动了 ADC 提高可扩展性和减少伺服器工作负载流量的需求。

- 此外,零售商正在投资多重云端、多地点和多平台负载平衡策略,零售商行动应用程式网站的访客可能会根据国家/地区看到不同语言的内容。因此,这些功能吸引了来自世界各地的更多客户,并采用 ADC 来减轻伺服器的负载。

- 此外,需要遵守欧盟GDPR等法规,对位于不同地点的伺服器进行资料安全和隐私管理,这也对零售业的ADC提出了要求。总体而言,随着物联网的不断融入以及零售业采用数位技术使支付和其他交易更快、更自动化,所研究行业对 ADC 的需求将会增加。

- 可以透过多种方式控制电子商务应用程式以确保正常的功能和安全性。业务流程中常用的控制包括存取控制、资料加密、审核追踪和防火墙。增加线上消费可能会促进所研究市场的成长。例如,根据销售团队 的数据,2022 年第四季度,所有垂直行业的线上消费者平均每次造访的花费略低于 3 美元。食物和饮料是消费者花费最多的类别,平均每次花费超过 4 美元,其次是奢侈服饰,花费近 3.50 美元。

北美可望主导市场

- 北美是世界各地各大组织的主要基地。因此,这些行业的扩张和成长,加上这些行业对技术的日益采用,正在推动该地区企业对应用程式部署的需求。因此,确保资料安全已成为该地区的首要任务,从而导致应用程式控制解决方案的采用率不断提高。

- 此外,云端基础的应用程式的日益普及也推动了该地区对资料中心的需求。例如,Cloudscene 最近的一份报告发现,微软在北美资料中心提供了 18 个云端入口,而亚马逊、Google、阿里巴巴和 IBM 分别提供了 18、11、10 和 9 个云端入口。此外,全部区域日益严重的网路安全威胁促使企业选择更灵活、更具成本效益的应用交付控制器。

- 该地区拥有许多主要企业的应用程式交付控制器解决方案供应商,包括 F5 Networks、Fortinet、Juniper Networks、A10 Networks 和 Array Networks。该地区的市场参与者正在透过推出新的解决方案来响应数位转型和业务需求。例如,Fortinet推出了FortiADC 6.1,可提供应用程式加速和进阶保全服务。

- 多家公司正在致力于开发创新解决方案,以满足该地区中小企业对具有成本效益的云端运算解决方案的需求。例如,应用程式安全性、视觉性和控制领域的先驱 Snapt 最近宣布了 Nova 2 版,这是 Snapt 集中式 ADC 平台的第二代。这个云端基础的ADC 包括负载平衡器、WAF、GSLB 和 Web 加速器。 Nova 是一个超大规模、集中式平台,用于大规模部署、控制和监控 ADC。

- SAP 表示,截至 2022 年 7 月的第二季度,各种规模的企业都选择 SAP 来支援其云端迁移。这表明 RISE with SAP 解决方案在北美公司中继续被广泛采用。公共云端的采用在客户中持续成长,今年稍早已有数百家公司选择了 RISE 和 SAP。

应用控制行业概况

应用控制市场的竞争格局较为分散,全球有多家解决方案供应商。这些解决方案提供者不断创新,为市场提供更强大的解决方案。此外,市场参与者正在进行策略合作,以加强其全球立足点和市场影响力。

- 2023 年 7 月 - Fortinet 发布了在企业资料中心部署 FortiGate 新世代防火墙 (NGFW) 和 FortiGuard 人工智慧安全服务的成本节约和业务优势的分析,显示三年内投资收益(ROI) 超过 300%,回收期为六个月。 FortiGate 3200F 和 900G 威胁防护透过启用防火墙、IPS、应用程式控制和反恶意软体以及日誌记录来衡量。

- 2023 年 4 月-诺基亚推出四款第三方 MX Industrial Edge (MXIE) 应用程序,帮助组织在强化、安全的内部部署边缘连接、收集和分析来自操作技术(OT) 资产的资料。资产密集型产业将从诺基亚的 OT Edge 生态系统中立方法中受益最多,该方法利用了许多关键数位化推动因素的创新。新应用程式还利用了诺基亚 MXIE 中最近发布的 GPU 功能。这种强大的内部部署 OT 边缘解决方案可协助您即时、最接近源头地处理资料,同时保持资料主权。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 市场驱动因素

- 由于越来越多地采用来自不同来源的应用程序, IT基础设施变得越来越复杂

- 更多采用资料安全措施

- 组织越来越多地采用 BYOD 趋势

- 市场限制

- 对最终使用者体验的影响

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 购买者/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 市场影响评估

第五章 市场区隔

- 按组织规模

- 中小型企业

- 大型企业

- 按组件

- 解决方案

- 服务

- 按应用程式类型

- 基于网路

- 云端基础

- 行动应用程式

- 其他应用

- 按最终用户产业

- BFSI

- 卫生保健

- 资讯科技/通讯

- 政府和国防

- 零售

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第六章 竞争格局

- 公司简介

- Trend Micro Inc.

- McAfee, LLC

- Fortinet, Inc.

- Ivanti Inc.

- Checkpoint Software Technologies Ltd.

- Veracode, Inc.

- WatchGuard Technologies, Inc.

- Comodo Group, Inc.

- VMware, Inc.

- Thycotic Software, LLC

第七章投资分析

第八章 市场机会与未来趋势

The Application Control Market size is estimated at USD 1.76 billion in 2025, and is expected to reach USD 2.20 billion by 2030, at a CAGR of 4.59% during the forecast period (2025-2030).

The rising number of cyberattacks and considerable growth in connected devices and access points has significantly raised the demand for superior business application monitoring and control. As a result, the demand for comprehensive end-point access protection and coverage has increased dramatically, gaining popularity across a wide range of industry verticals.

Key Highlights

- The growing number of cyberattacks, combined with an increase in connected devices and access points, has significantly raised the demand for enhanced monitoring and control of enterprise applications. As a result, the demand for comprehensive end-point access security and coverage has increased dramatically, gaining popularity across a wide range of industry verticals. As a result, various market participants in the application control market presently offer extensive business products that permit advanced protection of enterprise applications by enabling varying degrees of control, such as execution, monitoring, and authentication, among other controls.

- Further, the application control-based solutions offer a broad range of uses, including network security, server management, end-point protection, and authentication, among other benefits to the end-user organization. Application control has gained significant traction in the past few years, primarily owing to the rising need for load balancing, improving performance, and handling much more advanced requirements associated with application delivery. These solutions provide availability, scalability, performance, security, automation, and control essential to keep the applications and servers running in their power band.

- These capabilities also aid organizations that want to or have already migrated to the cloud environments. Digital transformation has been inspiring new architectures and optimization initiatives. It significantly impacts ADCs as they are crucial to application architectures and IT optimization. For example, almost any E-commerce website uses an application delivery controller to improve the availability and reliability of its applications. Currently, businesses have been undergoing digital transformation as their enterprise counterparts. Website reliability, flexibility, scalability, and performance are as essential to website infrastructure as they are to an enterprise.

- The exponential explosion in data traffic has been demanding that network systems be capable of handling the increasing rates of application layer traffic. The solutions offered in the market must handle these types of huge loads. The increasing need to scale out applications, which in various cases consists of solutions from different vendors, along with adding new services to the network, can result in increased complexities and increased points of failure in the network. As a result, delivering these services to the consumers becomes more complex and can result in major delays, leading to loss of revenue streams and lowered subscriber quality of experience.

- The global COVID-19 pandemic caused long-term impacts in various major IT and technology sectors. For example, several IT and other big technology organizations anticipated fewer commercial contracts across various industrial verticals such as manufacturing, service sector, healthcare, and retail. However, due to their importance in utilities and necessary everyday operations, critical businesses such as BFSI, IT & telecom, aerospace & defense, and others experienced minor impacts during the pandemic across different nations.

Application Control Market Trends

Retail is Expected to Hold the Significant Share of the Market

- With the improvement of the Web, the development of multi-channel operations, and the evolution of intelligent retail application solutions, the retail market has become dynamic. Moreover, with the rapid rise of e-commerce, business intelligence is being enabled to track how users interact with e-Commerce stores, and this information can be used further to enhance the customer shopping and service experience. E-Commerce also allows retailers to make smart, efficient decisions based on customer behavior. This data can be viewed in real-time, allowing businesses to adjust prices quickly or alter merchandise offerings. Such developments increase the attraction towards online shopping, and retailers are adopting Application Controller to reduce load times.

- The number of IoT-connected devices in the retail sector is exponentially increasing. For instance, in the EU region, the number of connected devices used in the retail industry was 2.28 million units in 2019, and it is expected to grow to 3.09 million units by 2025, as per the ENTO reports. Also, Amazon opened Amazon Go, a physical grocery store near its Seattle headquarters. The brick-and-mortar store uses a broad network of newly designed cameras, sensors, and smartphones to determine the exact product each consumer takes off a shelf. After identifying the product, the technology adds it to a digital cart. Such developments in the retail sector increase the need for ADCs to improve scalability and reduce server workload traffic.

- Furthermore, retailers are investing in multi-cloud, multi-location, and multi-platform load balancing strategies where visitors to the retail mobile application sites might view the content in different languages depending on the customers based on the country they are located in. Therefore, such capabilities attract more customers worldwide, and to reduce the server workload, ADCs are being adopted.

- The need for regulatory compliance for servers located in different locations, such as GDPR in the European Union, for governing data security and privacy also demands the ADCs in retail sectors. Overall, the demand for ADC increases across the studied sector with the increased incorporation of IoT and the introduction of digital technologies in retail to automate payments and other transactions faster.

- E-commerce applications can be controlled through various means to ensure proper functionality and security. Some commonly used controls in business processes include access controls, data encryption, audit trails, and firewalls. The rise in online spending would allow the studied market to grow. For instance, according to Salesforce, In the fourth quarter of 2022, online shoppers across all verticals spent an average of slightly under three dollars per visit. Food and beverage is the category in which consumers spend the most money each visit on average, at more than four dollars, followed by luxury clothes at almost USD 3.5.

North America is Expected to Dominate the Market

- North America is a primary hub for all the major organizations worldwide; hence, the expansion and growth in these industries, coupled with increased adoption of technology across these industries, is driving the demand for the deployment of applications amongst enterprises in the region. Thus, securing the data has become a priority in the region, increasing the adoption of application control solutions.

- The increasing adoption of cloud-based applications has also increased the demand for regional data centers. For instance, according to a report published by Cloudscene recently, Microsoft offers 18 cloud on-ramps in data centers in North America, followed by Amazon, Google, Alibaba, and IBM with 18, 11, 10, and 9 cloud on-ramps in data centers, respectively. Moreover, the rising cybersecurity threats across the region have further encouraged businesses to opt for more agile and cost-effective application delivery controllers, which are scalable and secure, and increase visibility over data traffic and movement across the users.

- The region has many leading Application Delivery Controller solution provider companies, such as F5 Networks, Fortinet, Juniper Networks, A10 Networks, and Array Network. Market players in the region are keeping up with digital innovations and business demands by launching new solutions. For instance, Fortinet launched FortiADC 6.1 to accelerate applications and deliver advanced security services.

- Several companies are working on innovative solutions to tap into the growing SME sector in the region, looking for cost-effective cloud-enabled solutions for their businesses. For instance, Snapt, the pioneering application security, visibility, and control company, recently launched Nova Version 2, the second generation of Snapt's centralized ADC platform. This cloud-based ADC includes a load balancer, WAF, GSLB, and web accelerator. Nova is a hyper-scale-ready, centralized platform for deploying, controlling, and monitoring ADCs at scale.

- In July 2022, in the second quarter of 2022, firms of all sizes chose SAP to support their cloud transitions, according to a statement from SAP. This indicated that the RISE with SAP solution continued to enjoy a high rate of acceptance across businesses in North America. Hundreds of companies chose RISE with SAP in the first part of the year, with public cloud deployments becoming increasingly popular among customers.

Application Control Industry Overview

The competitive landscape of the Application Control Market is fragmented owing to the presence of several solution providers across the globe. These solution providers are increasingly innovating to provide enhanced solutions in the market. The market players are also strategically collaborating to strengthen their global foothold and market presence.

- July 2023 - Fortinet announced an analysis of the cost savings and business benefits of deploying FortiGate Next-Generation firewalls (NGFWs) and FortiGuard AI-Powered Security Services within the enterprise data center, including more than a 300% return on investment (ROI) over three years and payback in six months. FortiGate 3200F and 900G Threat Protection is measured with Firewall, IPS, Application Control and Malware Protection, and Logging enabled.

- April 2023 - Nokia released four third-party MX Industrial Edge (MXIE) applications to assist organizations in connecting, collecting, and analyzing data from operational technology (OT) assets on a strong and secure on-premises edge. Asset-heavy sectors will benefit the most from Nokia's OT edge ecosystem-neutral approach, which taps into innovation from many leading digitalization enablers. The new apps also use the recently released GPU functionality on the Nokia MXIE. This robust on-premises OT edge solution helps process data closest to the source in real time while maintaining data sovereignty.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Deployment of Applications From Various Sources Leading to Complexity in the IT Infrastructure

- 4.2.2 Increasing Adoption of Data Security Measures

- 4.2.3 Increasing Adoption of BYOD Trends in Organizations

- 4.3 Market Restraints

- 4.3.1 Impacting the End-User Experience

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Assessment of Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Size of the Organization

- 5.1.1 Small and Medium Enterprises

- 5.1.2 Large Enterprises

- 5.2 By Component

- 5.2.1 Solutions

- 5.2.2 Services

- 5.3 By Type of Applications

- 5.3.1 Web-based

- 5.3.2 Cloud-based

- 5.3.3 Mobile Applications

- 5.3.4 Other Applications

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare

- 5.4.3 IT and Telecom

- 5.4.4 Government & Defense

- 5.4.5 Retail

- 5.4.6 Other End-user Industries

- 5.5 Geography

- 5.5.1 North America

- 5.5.2 Europe

- 5.5.3 Asia-Pacific

- 5.5.4 Latin America

- 5.5.5 Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Trend Micro Inc.

- 6.1.2 McAfee, LLC

- 6.1.3 Fortinet, Inc.

- 6.1.4 Ivanti Inc.

- 6.1.5 Checkpoint Software Technologies Ltd.

- 6.1.6 Veracode, Inc.

- 6.1.7 WatchGuard Technologies, Inc.

- 6.1.8 Comodo Group, Inc.

- 6.1.9 VMware, Inc.

- 6.1.10 Thycotic Software, LLC