|

市场调查报告书

商品编码

1437494

摩托车燃油喷射系统:市场占有率分析、产业趋势与统计、成长预测(2024-2029)2 Wheeler Fuel Injection System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

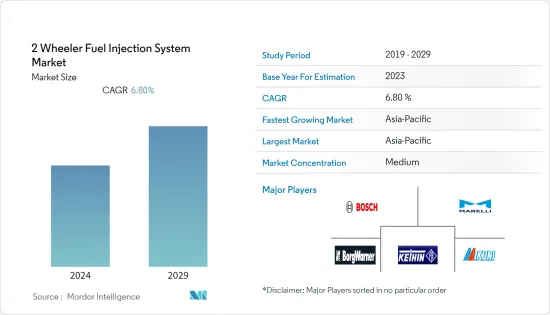

以 Equal-6.80 计算的两轮车燃油喷射系统市场规模预计将从 2024 年的 119.4 亿美元增长到 2029 年的 165.9 亿美元,预测期内(2024-2029 年)复合年增长率为 6.80%。到美元。

从中期来看,由于政府对两轮车排放的严格规则和法规以及汽车化油器桿的低效率,对更清洁、更有效率的车辆的需求不断增加,预计将推动市场的发展。

由于存在许多未铺砌的道路以及不同国家不同家庭的私人购买者的承受能力相对较低,导致购买者选择两轮车辆,例如摩托车、轻型机踏车和Scooter。上述因素的综合作用将在未来几年在全球创造对摩托车燃油喷射系统的巨大需求。

线控 (RbW) 技术的快速采用可使用致动器、感测器和电控系统来节流电线并调节引擎内的燃料和空气供应,以实现高效率和高性能。此前,RbW 仅在工厂出货在高端自行车上。然而,它现在已被引入中阶自行车,例如 KTM Duke 390。

随着摩托车製造商开发出具有更好燃油喷射系统的更小型发动机,发动机尺寸正在不断缩小。小型化使引擎运转到更高的负载,从而提高引擎效率。轻型引擎有助于提高燃油效率。电动二轮车在全球范围内的日益普及可能会阻碍燃油喷射系统市场的成长。

摩托车燃油喷射系统市场趋势

摩托车占据市场主导地位

由于都市化加快、可支配收入增加以及对负担得起且有效的交通的需求等因素,摩托车的销量大幅增长。本田、Yamaha、川崎等日本摩托车製造商主导市场。

同时,收入的增加、政府的倡议和基础设施的扩大是人们将注意力从升级旧摩托车转向购买入门级小客车的一些主要原因。这表明该国对汽车市场的依赖程度正在增加,同时逐渐转向更昂贵的更大引擎的两轮(运动)汽车和电动车市场。

汽车产业的快速技术进步迫使(并在某种程度上迫使)製造商依赖未来新的汽车技术,并在核心设计和产品研发方面投入大量资金。我就是。虽然大多数拥有可行创新资源的製造商都在削减开支,但有些製造商在车辆的核心设计上遇到了困难,以满足市场需求,与市场上的其他参与者进行创新和製定策略,往往依赖私人合作伙伴关係。

这一新的伙伴关係和协作浪潮将帮助市场参与者进行技术和关键资讯的受控共用,从而为整个市场在满足买家需求方面带来巨大利益。结果,汽车製造商之间的製造联盟在撒哈拉以南地区激增,该地区汽车行业的技术进步相对缓慢。例如,

2022 年 7 月,TVS Motor Company 宣布推出高阶车型 TVS RONIN,这是业界首款「现代復古」自行车。 TVS RONIN 从头开始设计,是受当今新时代骑手启发的生活方式宣言。

2022 年 5 月,TVS 汽车公司宣布在肯亚推出限量版 TVS HLX 125 Gold 和 TVS HLX 150 Gold 车型。据该公司称,发布这两款名人限量型号是为了纪念TVS HLX系列全球销量突破200万台。

全球范围内的上述发展可能表明预测期内市场将显着增长。

亚太地区预计将成为成长最快的地区

亚太地区在市场上占据主导地位,预计该地区在预测期内将呈现最高成长率。

在亚太地区,印度摩托车市场自2016年以来一直是全球最大的摩托车市场,Hero、TV、本田等主要製造商纷纷进入该市场。随着女性进入劳动市场以及对舒适和便利的需求增加,对高度便利的Scooter的需求持续增加。

此外,由于对高性能和巡洋舰摩托车的需求不断增加,中型和大型摩托车的高价位市场也在扩大。全国中小企业的快速扩张很可能为汽车零件製造商创造机会。

在预测期内,全部区域两轮车最后一英里交付的快速扩张可能会显着增长。两轮车在交通拥挤和狭窄的道路和小巷中比四轮车更容易操纵,这在拥挤的都市区是一个很大的优势。此外,它可以轻鬆定制以满足特定的业务需求,例如添加宅配箱或货架来运输货物或更换座位以适应乘客。

从长远来看,企业可以透过使用两轮车来节省燃料成本,两轮车通常比四轮车消耗更少的燃料。两轮车有时比四轮车行驶得更快。这对于需要快速交付货物或快速提供运输服务的企业尤其重要。

另一方面,在预测期内,两轮车租赁和共享服务的扩张可能会显示市场的显着成长。

摩托车燃油喷射系统产业概况

Marelli Holdings、Mikuni Corporation、Denso Corporation 和 Robert Bosch GmbH 等主要公司主导着摩托车燃油喷射系统市场。多家两轮车製造商已在全球推出新车型,预计市场在预测期内将大幅成长。例如,2023年6月,Adishwar Auto Ride India Pvt. Ltd.宣布将于明年将其Keeway品牌下的两款新復古骑行自行车SR 250和SR 125本地化。两种型号均配备电子燃油喷射系统。

Yamaha Motor Co, Ltd.于 2023 年 1 月在非洲地区推出了YamahaYZ65。 YZ65 由液冷 65cc二行程引擎提供动力,可提供卓越的动力和性能。

2022年3月,Aprila推出了燃油喷射二行程发动机,该发动机在燃烧室上方装有燃油喷射器和压缩空气喷射设备。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场驱动因素

- 全球摩托车销售成长

- 市场限制因素

- 电动二轮车越来越受欢迎

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代产品的威胁

- 竞争公司之间的敌意强度

第五章市场区隔(按金额分類的市场规模 - 美元)

- 按类型

- 直接燃油喷射系统

- 端口燃油喷射系统

- 按车型

- Scooter

- 摩托车

- 按位移

- 200cc以下

- 200~500cc

- 500~1000cc

- 1000cc以上

- 按销售管道

- OEM

- 售后市场

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 埃及

- 其他中东和非洲

- 北美洲

第六章 竞争形势

- 供应商市场占有率

- 公司简介

- Robert Bosch GmbH

- Marelli Holdings Co., Ltd.

- Denso Corporation

- Mikuni Corporation

- Hitachi Astemo, Ltd.

- DUCATI Energia Spa

- Walbro LLC

- EDELBROCK, LLC.

- SEDEMAC Mechatronics Pvt Ltd.

- UCAL Systems Inc.

第七章市场机会与未来趋势

The 2 Wheeler Fuel Injection System Market size in terms of Equal-6.80 is expected to grow from USD 11.94 billion in 2024 to USD 16.59 billion by 2029, at a CAGR of 6.80% during the forecast period (2024-2029).

Over the medium term, owing to the stringent government rules and regulations regarding two-wheeler emissions, increasing demand for cleaner and more efficient vehicles, and inefficiency of car carburetor stems are likely to drive the market.

The high number of unpaved roads and the relatively low individual buyer affordability that is observed across different households of various countries leads the buyer to opt for a two-wheeler, including a motorcycle, a moped, and a scooter. Combining the above factors creates a significant demand for two-wheeler fuel injection systems across the globe in the coming years.

The rapid adoption of Ride-by-wire (RbW) technology, as it uses actuators, sensors, and the Electronic Control Unit to throttle wire to regulate fuel and air supply in the engine, thus providing high efficiency and performance. Earlier, RbW was factory-installed only in high-end bikes. However, now it is introduced in mid-segment bikes, such as the KTM Duke 390.

Engine downsizing is on the rise as two-wheeler makers are developing smaller engines with better fuel injection systems. Downsizing shifts the engine operation to high loads where high engine efficiency exists. The lightweight engine helps to enhance fuel efficiency. The rising popularity of electric two-wheelers across the globe is likely to hinder the growth of the fuel injection system market.

2 Wheeler Fuel Injection System Market Trends

Motorcycles Dominating the Market

Motorcycles have grown significantly as a result of factors like rising urbanization, rising disposable incomes, and the need for affordable and effective transportation. Japanese motorcycle manufacturers like Honda, Yamaha, Suzuki, and Kawasaki dominate the market.

On the other hand, rising incomes, government initiatives, and the expansion of infrastructure are some of the primary reasons why people are shifting their focus away from upgrading their older motorcycles and toward purchasing entry-level passenger cars. It demonstrates that the nation is increasing its reliance on the automobile market while gradually shifting to more expensive motorcycle markets featuring larger engines (sports vehicles) and electric vehicles.

The rapid technological advancements in the automobile industry have driven (in a way, forced) the manufacturers to resort to new and upcoming vehicle tech and invest significantly into the research and development of the core design and products. While most of the manufacturers with viable resources for innovation cut, some of the manufacturers tend to stumble at the core design of the vehicles to meet market needs and resort to innovations and strategic partnerships with other players in the market.

This new wave of partnership and collaboration helps the players in the market to execute a controlled sharing of technologies and key information, leading to the overall immense benefit for the market to cater to the demand from the buyers. Consequently, the sub-Saharan region, with its relatively slow technological advancement in the automotive industry, witnessed a surge in the manufacturer partnerships between the automotive manufacturers. For instance,

In July 2022, July 2022: TVS Motor Company announced a premium model with the launch of the industry's first 'modern-retro' motorcycle - the TVS RONIN. Designed ground up, the TVS RONIN is a lifestyle statement that takes inspiration from the modern, new-age rider.

In May 2022, TVS Motor Company announced the introduction of limited edition TVS HLX 125 Gold and TVS HLX 150 Gold models in Kenya. According to the company, the two celebrity limited edition models were released to commemorate global sales of over two million units of the TVS HLX series.

The development mentioned above across the globe is likely to witness major growth for the market during the forecast period.

Asia-Pacific is Expected to be the Fastest Growing Region

Asia-Pacific dominates the market, and the region is expected to witness the fastest growth rate during the forecast period.

In Asia-Pacific, the Indian motorcycle market has been the largest in the world since 2016, with the presence of major manufacturers such as Hero, TVs, and Honda. With the social advancement of women and the growing demand for comfort and convenience, the demand for scooters has been continually increasing as they are convenient.

Additionally, the premium price market segment for mid and large-sized motorcycles is also expanding, owing to a growing demand for high-performance and cruiser bikes. The rapid expansion of small and medium-scale industries across the country is likely to create an opportunity for vehicle parts manufacturers.

The Rapid expansion of last-mile delivery through two-wheelers across the region is likely to witness major growth during the forecast period. Two-wheelers are easier to maneuver through traffic and narrow streets and alleys than four-wheeled vehicles, making them a significant advantage in congested urban areas. Additionally, they can be easily customized to meet specific business requirements, such as by adding delivery boxes or racks to transport goods or by modifying the seating to accommodate passengers.

Businesses can save money over time on fuel costs by using two-wheeled vehicles, which typically use less fuel than four-wheeled vehicles. Two-wheeled vehicles can sometimes move faster than four-wheeled vehicles. This is especially important for businesses that need to deliver goods quickly or provide transportation services quickly.

The expansion of two-wheeler rental and sharing services, on the other hand, is likely to witness major growth for the market during the forecast period.

2 Wheeler Fuel Injection System Industry Overview

Major players, such as Marelli Holdings Co. Ltd., Mikuni Corporation, Denso Corporation, Robert Bosch GmbH, and others, dominate the 2-wheeler fuel injection system market. Several two-wheeler manufacturers are introducing new models across the globe, which in turn is anticipated to witness major growth for the market during the forecast period. For instance, in June 2023, Adishwar Auto Ride India Pvt. Ltd. announced the localization of the two Neo-Retro rides motorcycles from the Keeway brand, i.e., SR 250 and SR 125, in the coming year. Both models are equipped with an electronic fuel injection system.

In January 2023, Yamaha Motor launched the Yamaha YZ65 in the African region. The YZ65 is powered by a liquid-cooled 65cc two-stroke engine that delivers impressive power and performance.

In March 2022, Aprilla introduced a fuel-injected two-stroke that incorporates a fuel injector above the combustion chamber, as well as a provision for injecting compressed air.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rise in Two-Wheeler Sales Across the Globe

- 4.2 Market Restraints

- 4.2.1 Rising Popularity of Electric Two-wheelers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Type

- 5.1.1 Direct Fuel Injection System

- 5.1.2 Port Fuel Injection System

- 5.2 By Vehicle Type

- 5.2.1 Scooters

- 5.2.2 Motorcycles

- 5.3 By Engine Displacement

- 5.3.1 Less than 200 cc

- 5.3.2 200 to 500 cc

- 5.3.3 500 to 1000 cc

- 5.3.4 Greater than 1000 cc

- 5.4 By Sales Channel

- 5.4.1 Original Equipment Manufacturers (OEM)

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle-East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Robert Bosch GmbH

- 6.2.2 Marelli Holdings Co., Ltd.

- 6.2.3 Denso Corporation

- 6.2.4 Mikuni Corporation

- 6.2.5 Hitachi Astemo, Ltd.

- 6.2.6 DUCATI Energia Spa

- 6.2.7 Walbro LLC

- 6.2.8 EDELBROCK, LLC.

- 6.2.9 SEDEMAC Mechatronics Pvt Ltd.

- 6.2.10 UCAL Systems Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

汽车燃油喷射帮浦市场规模、份额及成长分析(按泵浦类型、燃油类型、车辆类型、最终用户和地区划分)-2026-2033年产业预测

汽车燃油喷射帮浦市场规模、份额及成长分析(按泵浦类型、燃油类型、车辆类型、最终用户和地区划分)-2026-2033年产业预测 化学注射帮浦市场:依产品类型、应用、国家及地区划分-全球产业分析、市场规模、市占率及2025-2032年预测

化学注射帮浦市场:依产品类型、应用、国家及地区划分-全球产业分析、市场规模、市占率及2025-2032年预测 汽车燃油喷射帮浦市场(按技术、应用、燃料类型和分销管道)—2025-2032 年全球预测汽车燃油喷射系统市场(按喷射类型、系统类型、车辆类型、燃料类型和应用划分)-全球预测,2025-2032年

汽车燃油喷射帮浦市场(按技术、应用、燃料类型和分销管道)—2025-2032 年全球预测汽车燃油喷射系统市场(按喷射类型、系统类型、车辆类型、燃料类型和应用划分)-全球预测,2025-2032年 摩托车电子控制燃油喷射系统的全球市场

摩托车电子控制燃油喷射系统的全球市场 两轮车燃油喷射系统市场 - 全球产业规模、份额、趋势、机会和预测,按引擎尺寸、车辆类型、需求类别、地区和竞争细分,2019-2029F

两轮车燃油喷射系统市场 - 全球产业规模、份额、趋势、机会和预测,按引擎尺寸、车辆类型、需求类别、地区和竞争细分,2019-2029F 汽车用空气/燃料管理零件的全球市场规模:各产品,各用途,各地区,范围及预测汽车燃油喷射帮浦测试仪市场报告:2030 年趋势、预测与竞争分析汽车燃油喷射帮浦市场,按类型、按燃料、按压力、按车型、按配销通路、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

汽车用空气/燃料管理零件的全球市场规模:各产品,各用途,各地区,范围及预测汽车燃油喷射帮浦测试仪市场报告:2030 年趋势、预测与竞争分析汽车燃油喷射帮浦市场,按类型、按燃料、按压力、按车型、按配销通路、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测